BIS Working Papers

No 114

Asset prices, financial and

monetary stability: exploring

the nexus

by Claudio Borio and Philip Lowe

Monetary and Economic Department

July 2002

Studia grazie alle numerose risorse presenti su Docsity

Guadagna punti aiutando altri studenti oppure acquistali con un piano Premium

Prepara i tuoi esami

Studia grazie alle numerose risorse presenti su Docsity

Prepara i tuoi esami con i documenti condivisi da studenti come te su Docsity

Trova i documenti specifici per gli esami della tua università

Preparati con lezioni e prove svolte basate sui programmi universitari!

Rispondi a reali domande d’esame e scopri la tua preparazione

Riassumi i tuoi documenti, fagli domande, convertili in quiz e mappe concettuali

Studia con prove svolte, tesine e consigli utili

Togliti ogni dubbio leggendo le risposte alle domande fatte da altri studenti come te

Esplora i documenti più scaricati per gli argomenti di studio più popolari

Ottieni i punti per scaricare

Guadagna punti aiutando altri studenti oppure acquistali con un piano Premium

The relationship between asset prices, credit expansion, and financial instability. It argues that major swings in asset prices have historically accompanied episodes of financial instability, and that indicators of vulnerability should take into account cumulative processes and the interaction of asset prices and credit. The document also explores the role of monetary policy in maintaining financial stability and the difficulties in identifying financial imbalances.

Tipologia: Guide, Progetti e Ricerche

1 / 47

Questa pagina non è visibile nell’anteprima

Non perderti parti importanti!

by Claudio Borio and Philip Lowe

July 2002

BIS Working Papers are written by members of the Monetary and Economic Department of the Bank for International Settlements, and from time to time by other economists, and are published by the Bank. The papers are on subjects of topical interest and are technical in character. The views expressed in them are those of their authors and not necessarily the views of the BIS.

This working paper was written for the Conference on “Changes in risk through time: measurement and policy options” that took place at the BIS on 6 March 2002.

Copies of publications are available from:

Bank for International Settlements Press & Communications CH-4002 Basel, Switzerland

E-mail: [email protected]

Fax: +41 61 280 9100 and +41 61 280 8100

This publication is available on the BIS website (www.bis.org).

© Bank for International Settlements 2002. All rights reserved. Brief excerpts may be reproduced or translated provided the source is cited.

Economic historians will no doubt look back on the last twenty years of the 20th century as those that marked the end of a long inflationary phase in the world economy. Burnt by the experience of the 1970s, policy makers had put in place credible institutional safeguards against monetary instability. They had done so by endowing central banks with clear mandates to maintain price stability and with the necessary autonomy to pursue them. And yet, the same decades will in all probability also be remembered as those that saw the emergence of financial instability as a major policy concern, forcing its way to the top of the international agenda. One battlefront had opened up just as another was victoriously being closed. Ostensibly, lower inflation had not by itself yielded the hoped-for peace dividend of a more stable financial environment.

Is this confluence of events coincidental? What is the relationship between monetary and financial stability? What is an appropriate policy framework to secure both simultaneously? These are some of the questions that we begin to explore in this paper.

There are many possible routes that can be taken to arrive at the heart of these issues. Given the focus of this conference, we start from asset prices. Medium-term swings in asset prices have historically accompanied episodes of widespread financial instability. And in recent years the question of whether monetary policy should respond to asset price "bubbles" has been asked with increasing frequency. Opinions on the subject are just as divided as ever.

We would like to make three points.

First, posing the question in terms of the desirability of a monetary response to "bubbles" per se is not the most helpful approach. Widespread financial distress typically arises from the unwinding of financial imbalances that build up disguised by benign economic conditions. Booms and busts in asset prices, whether characterised as "bubbles" or not, are just one of a richer set of symptoms. It is the combination of these symptoms that matters. Other common signs include rapid credit expansion and, often, above-average capital accumulation. These developments can, jointly, sow the seeds of future instability. As a result the financial cycle can amplify, and be amplified by, the business cycle.

Second, while not disputing the fact that low and stable inflation promotes financial stability, we stress that financial imbalances can and do build up in periods of disinflation or in a low inflation environment. One reason is the common positive association between favourable supply-side developments, which put downward pressure on prices, on the one hand, and asset prices booms, easier access to external finance and optimistic assessments of risk, on the other. A second is that the credibility of the policymakers' commitment to price stability, by anchoring expectations and hence inducing greater stickiness in price and wages, can alleviate, at least for a time, the inflationary pressures normally associated with the unsustainable expansion of aggregate demand. A third is that by obviating the need to tighten monetary policy, such conditions can allow the build up of imbalances to proceed further.

Third, achieving monetary and financial stability requires that appropriate anchors be put in place in both spheres. In a fiat standard, the only constraint in the monetary sphere on the expansion of credit and external finance is the policy rule of the monetary authorities. The process cannot be anchored unless the rule responds, directly or indirectly, to the build up of financial imbalances. In principle, safeguards in the financial sphere, in the form of prudential regulation and supervision, might be sufficient to prevent financial distress. In practice, however, they may be less than fully satisfactory. If the imbalances are large enough, the end-result could be a severe recession coupled with price deflation. While such imbalances can be difficult to identify ex ante, the results presented in this paper provide some evidence that useful measures can be developed. This suggests that, despite the difficulties involved, a monetary policy response to imbalances as they build up may be both possible and appropriate in some circumstances. More generally, co-operation between monetary and prudential authorities is essential.

The outline of the paper is as follows. In Section 2 we document changes in asset prices since the 1970s in a sample of industrial countries. We focus on equity and property prices and present an aggregate asset price index that can serve as a summary measure of asset price developments. In Section 3 we begin to explore more systematically the relationship between financial and real imbalances, on the one hand, and financial instability, on the other. By stressing cumulative processes, we examine to what extent symptoms of financial instability can be detected ex ante in a sample of 34 industrial and middle-income emerging market economies. In Section 4 we then consider the relationship between monetary and financial stability, laying out the conceptual nexus and drawing

on some descriptive empirical evidence. In Section 5 we assess the policy implications. Finally, the conclusions highlight some open questions and issues for future research.

Relevance

Until at least the early 1990s there seemed to be a certain disconnect in the way the economics profession treated asset prices. On the one hand, asset prices stood out in historical accounts of financial instability (see Section 3). In these accounts it is property prices in particular that have been highlighted, although in some accounts equity prices have figured prominently. On the other hand, the mainstream macroeconomics literature examining the link between asset prices and the macro- economy focused almost exclusively on equity prices. Even then, efforts concentrated primarily on understanding the role of equity prices in affecting consumer expenditures, with less attention being paid to their impact on the cost of capital; the work pioneered by Tobin was the main exception. 1

This disconnect is puzzling for a number of reasons. If asset prices swings are a significant cause of financial instability, presumably they should also play a prominent role in determining the level and composition of aggregate demand. Likewise, a much larger proportion of household wealth is typically held in the form of real estate than equity. And commercial property accounts for a sizeable fraction of firms’ assets.

During the last decade this disconnect has began to narrow. Conceptually, the literature on imperfections in the markets for external funding based on information asymmetries has lent intellectual respectability to accounts of the transmission of financial impulses to the real economy that stress the role of asset prices, not least as implicit or explicit measures of collateral. 2 Likewise, the increased incidence and macroeconomic costs of financial instability since the 1980s in industrial and emerging markets has helped to focus attention on the importance of asset prices. 3 Even so, empirical work on the relationship between credit and asset prices, or of the effect of changes in real estate prices on aggregate demand, is still quite limited. 4

Measurement

This comparative neglect helps to explain why available data on property prices are scarce. In fact, when the BIS started to collect them systematically in 1990, obtaining comparable series proved exceedingly hard. 5 Even today, some ten years on, while progress has been made in terms of coverage and quality, it has been far from satisfactory. There is, for instance, hardly any reliable data covering a sufficiently long period for emerging market countries. And comparability across countries is hampered by the heterogeneity of the series (e.g. national averages vs. main cities, basis for the calculation of the price). This dearth of statistics makes it difficult to carry out rigorous cross-country empirical analysis and virtually impossible to address some specific questions.

(^1) The seminal article on this is Tobin (1969).

(^2) The literature is now extensive, including contributions by Greenwald, Stiglitz and Weiss (1984), Bernanke and Gertler (1989) and Kiyotaki and Moore (1997). For surveys, see Gertler (1988) and Bernanke et al (1999). The role of asset prices, however, has a long tradition, including Keynes (1931) and, more recently, Kindleberger (1995). (^3) See e.g. IMF (1998), Bordo et al (2001) and Hoggarth and Saporta (2001).

(^4) Examples of work on the relationship between credit and asset prices include Blundell-Wignall and Bullock (1993), Borio at al (1994), Goodhart (1995), Hofmann (forthcoming). Borio (1997) and BIS (1995) provide some evidence on the cross- country use of real estate as collateral and on its possible link to the transmission mechanism of monetary policy. However, the evidence here is very limited. In a cross-country exercise, the link between real estate prices and consumer expenditure is analysed by Kennedy and Andersen (1994), which in addition contains a useful bibliography; see also Maclennan et al (1998). In the light of recent experience, the Federal Reserve Board is studying this link in more detail, (Greenspan (2001). (^5) See, for instance, the BIS Annual Report (1990).

50

100

150

200

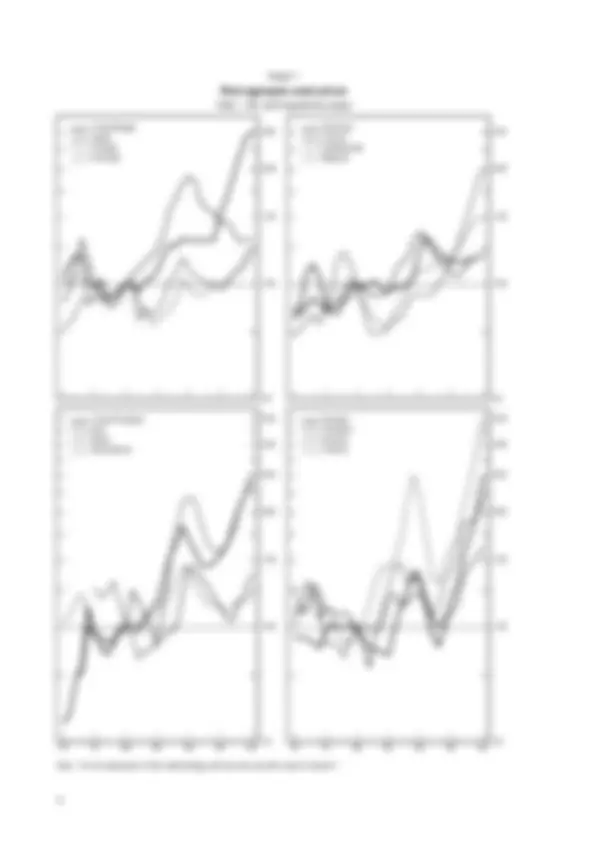

United States 250 Japan Canada Australia

50

100

150

200

Germany 250 France Netherlands Belgium

50

100

150

200

250

300

350

70 75 80 85 90 95 00

United Kingdom Italy Spain Switzerland

50

100

150

200

250

300

350

70 75 80 85 90 95 00

Sweden Denmark Norway Finland

Graph 1

1980 = 100; semi-logarithmic scales

Note: For an explanation of the methodology and sources, see the notes to Graph 2.

Real aggregate asset prices

100

200

300

400

500

600

700

50

60

100

200

300

400

500

40

50

60

100

200

250

60

100

200

250

100

200

300

400

500

70 75 80 85 90 95 00

100

200

300

400

500

650

70 75 80 85 90 95 00

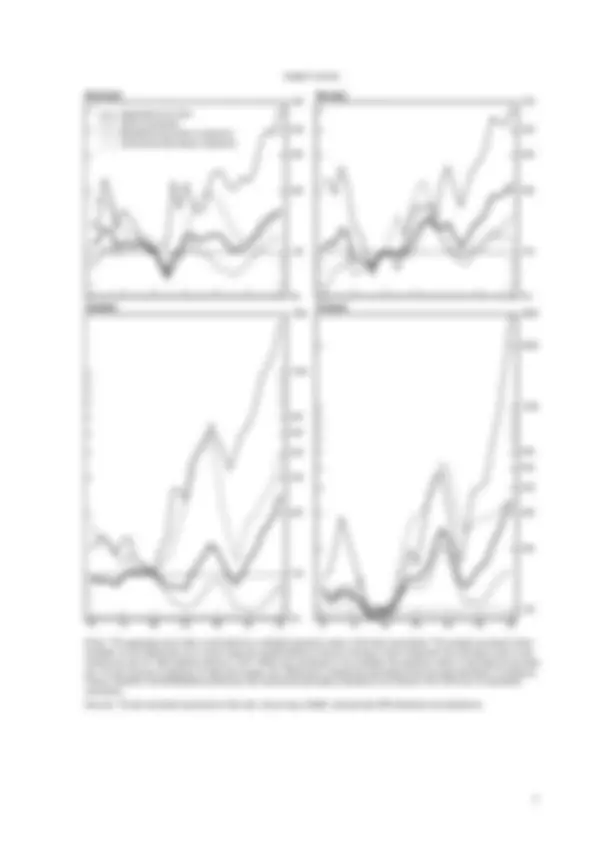

Aggregate price index Equity component Residential real estate component Commercial real estate component

Graph 2

1980 = 100; semi-logarithmic scales

Real asset prices: aggregate and components

United States United Kingdom

Canada Australia

Japan

Switzerland

60

100

200

300

400

550

60

100

200

300

400

550

60

100

200

300

400

500

600

1000

1950

70 75 80 85 90 95 00

100

200

300

400

500

600

1000

2000

2900

70 75 80 85 90 95 00

Aggregate price index Equity component Residential real estate component Commercial real estate component

Graph 2 (cont)

Notes: The aggregate price index is calculated as a weighted geometric mean of the three components. The weights are based, where available, on net wealth data, but in some cases are supplemented by the price change of each component; the calculation uses 5-year windows (6-year for 1995 weights) starting in 1970. Where one component is not available, the geometric mean is calculated on the other two. For the purpose of rebasing, for Italy and Canada, the 1980 level of commercial real estate prices has been estimated. For Belgium, France, Germany, the Netherlands and Norway, the commercial real estate component is not shown in the 1970s as it is proprietary information. Sources: Private real estate associations (inter alia, Jones Lang LaSalle); national data; BIS estimates and calculations.

Denmark Norway

Sweden Finland

What do we know?

Large swings in asset prices figure prominently in many accounts of financial instability. Indeed, a boom and bust in asset prices is perhaps the most common thread running through narratives of financial crises. This is true for both industrial and emerging market countries alike. Typical examples in recent decades include Latin America in the late 1970s-early 1980s, the Nordic countries in the late 1980s, and East Asia in the mid to late 1990s. These experiences are of course not new. In many respects the descriptions of the Australian boom and bust of the 1880-1890s, for example, could be used with only limited editing to describe some of the more recent episodes of financial instability. 10 Likewise, while perhaps more controversial, the experience of the United States in the late 1920s-early 1930s also exhibits similar features. 11

Despite the importance of asset price developments, they have received relatively little attention in the recent empirical literature examining the determinants of banking system crises. To a large extent this reflects the lack of adequate cross-country data already mentioned. Formal cross-country econometric tests of the links between asset price cycles and financial stability are severely hampered, and at best limited to equity prices. 12

(^9) See e.g. Greenspan (1991), Bank of England Quarterly Bulletin (1991), Blundell-Wignall and Bullock (1993), Gizycki and Lowe (2000) and, for an overview, O'Brien and Browne (1992). For evidence of a credit crunch beyond the banking sector in the Unites States, specifically in the private placements market, see Carey et al (1993). (^10) For a discussion of the Australian banking crisis of 1893 see Fisher and Kent (1999).

(^11) See Persons (1930) for a detailed account of the rapid credit growth in the United States in the 1920s.

(^12) Hutchison and McDill (1999), for example, find that declining stock prices are a useful one-year-ahead indicator of future banking problems. Kaminsky and Reinhart (1999) discover richer dynamics, presenting evidence that equity prices generally fall in the 9 months preceding a crisis and rise strongly in the 9 months before that. Kaminsky and Reinhart do not, however, test for the predictive properties of the original increase and focus on the decline in equity prices. It is unclear from these studies whether the fall in equity prices contributes to the crisis, or simply reflects the market’s expectation that a crisis is more likely.

60

80

100

120

140

160

60

80

100

120

140

160

50

75

100

125

150

175

200

50

100

150

200

250

300

60

80

100

120

140

160

180

75

100

125

150

175

200

225

50

100

150

200

250

70 75 80 85 90 95 00 50

100

150

200

250

300

350

70 75 80 85 90 95 00

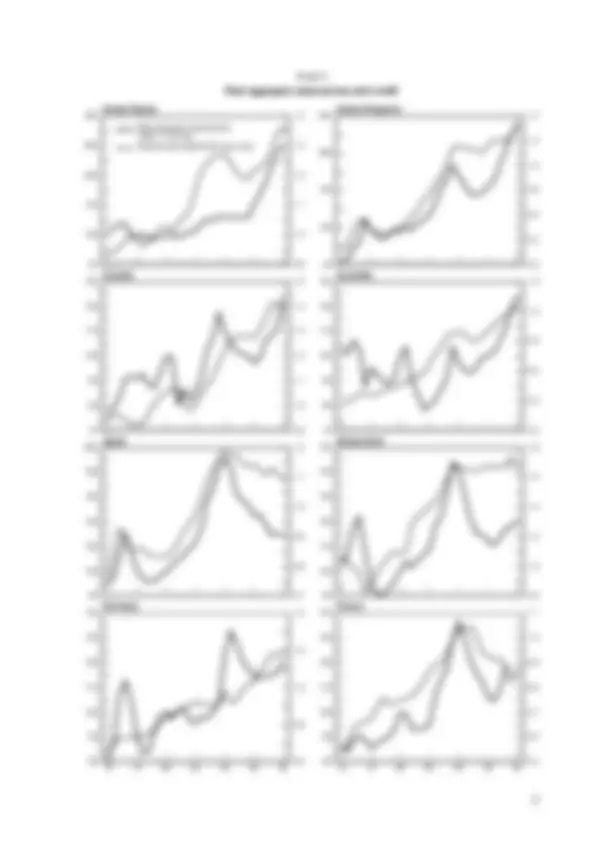

Real aggregate asset prices (1980 = 100; lhs) Total private credit/GDP (ratio; rhs)

Graph 3 (cont) Belgium Italy

Netherlands Spain

Denmark Norway

Sweden Finland

While asset prices have not generally been considered in these studies, their close cousin − credit − has been subject to considerable empirical investigation. One of the relatively few robust findings to emerge from the literature on leading indicators of banking crisis is that rapid domestic credit growth increases the likelihood of a problem.^13 Typical of the literature is Eichengreen and Arteta’s (2000) finding that a 1 percentage point increase in the rate of growth of domestic credit (evaluated at the mean rate of credit growth) increases the probability of banking crisis in the following year by 0. percent. Other studies have focused on credit growth lagged two years and find broadly similar effects, at least qualitatively.

Although these results tend to support the notion that booms in credit (and implicitly asset prices) increase the likelihood of financial problems, they provide little, if any, practical guidance about what constellation of outcomes materially increases the potential for instability. This reflects the design of the empirical work as well as the lack of data. Most studies do not take account of cumulative effects, or stocks, instead simply considering the effects of a single year of rapid credit growth, and posit a simple increasing relationship between credit growth in that year and the likelihood of financial problems. Moreover, the interactions between credit, asset prices and the real economy are typically ignored.

One consequence of this is that the existing literature provides relatively little insight into key questions that are of concern to both central banks and supervisory authorities. These include: (i) when should credit growth be judged as “too fast”? (ii) what is the cumulative effect of an extended period of strong credit growth?; and (iii) are lending booms more likely to end in problems if they occur simultaneously with other imbalances, either in the financial system or the real economy?

Beyond bubbles

From a practical perspective the issue of interactions between various imbalances is particularly important. Rapid credit growth, by itself , may pose little threat to the stability of the financial system. The same could be said for rapid increases in asset prices or an investment boom. Rather, the historical narratives suggest that it is the combination of events, in particular the simultaneous occurrence of rapid credit growth, rapid increases in asset prices and, in some cases, high levels of investment – rather than any one of these alone – that increases the likelihood of problems.

For policymakers, therefore, the more relevant issue is not whether a “bubble” exists in a given asset price, but rather what combination of events in the financial and real sectors exposes the financial system to a materially increased level of risk. While the bubble question is intrinsically interesting, it is extremely difficult to answer. Moreover, even if the authorities were confident in their judgement, serious political economy problems are likely if policy responses are explicitly conditioned on that judgement. Instead, a more constructive focus is likely to be on an overall assessment of the risks facing the financial system. Knowing the answer to the “bubble question” would obviously be helpful here, although it is by no means crucial.

A preliminary statistical analysis

Ideally, we would like to construct an accurate index of financial sector vulnerability that takes account of the interactions between all the relevant variables. In practice, this is extremely difficult (and perhaps even impossible) to do. Rather, in this paper our less ambitious goal is to undertake a preliminary investigation into the usefulness of credit, asset prices and investment as predictors of future problems in the financial system. Our intention is to be as parsimonious as possible and to explore how far a few key variables can take us. We are particularly interested in two questions. First, can useful indicators be constructed using only information available to the policymaker at the time that the policy decision is made? And second, can signals be made more accurate by jointly considering asset prices, credit and investment?

(^13) See, for example, Dermirguc-Kunt and Detragiache (1997, 1998), Gourinchas, Valdes and Landerretche (2001), Hardy and Pazarbasioglu (1999), Hutchinson and McDill (1999), Kaminsky (1999) and Kaminsky and Reinhart (2000). Bell and Pain (2000) and Eichengreen and Arteta (2000) provide useful overviews of the literature.

and even then do not go back sufficiently far in time to construct meaningful ex ante measures of the asset price gap for most of the years in the 1980s.

In determining the crisis dates we have used Bordo’s et al (2001) dating, rather than specifying the dates ourselves. 16 This has both benefits and costs. On the benefit’s side, these dates are representative of those used elsewhere in the literature. On the cost’s side, they exclude episodes characterised by strong financial headwinds, but not significant failures of banks. For example, the early 1990s is not recorded as a crisis episode for the United States, nor is it for the United Kingdom. 17 While these periods of financial headwinds may not fit the narrow definition of a “crisis”, they were certainty characterised by significant macroeconomic costs arising from developments in the financial system and arguably should be included as crisis episodes. In future work, we hope to extend our analysis to consider periods of “financial stress” and not just financial crises, since in practice the distinction between the two is often relatively small.

To start with, Table 1 reports our basic results for the indicators – i.e. the asset price, credit and investment gaps – taken individually , and using horizons of 1, 2 and 3 years. 18 For each indicator, the table shows a range of relevant threshold values and the associated noise to signal ratio for each of these values. 19,20^ The share of actual crises correctly signalled is also reported. For comparative purposes we also report results for a credit boom defined using just the annual rate of real credit growth.

A number of points emerge from this table.

(^16) Where the crisis episodes extend over multiple years we consider just the first year. In all there are 38 crisis episodes between 1970 and 1999 spread across 27 of the 34 countries. (^17) The only crisis for the United States is in 1984 and is associated with problems in the Savings and Loans institutions.

(^18) For the asset price indicator we introduce a lead of two years; i.e. when measuring whether the asset price gap exceeds a particular threshold we use the level of the equity price gap two years earlier. We do this for two reasons. First, previous studies have shown that equity markets provide a reasonable leading indicator of economic activity and financial problems, with the lead generally being around one to two years. Second, in many episodes a boom in property markets follows a boom in the equity market with a lag of a couple of years. In the absence of data on property prices, introducing a lead on the equity prices gap may allow equity prices to serve as a proxy (at least in some cases) for property prices. (^19) In all three cases an indicator is judged to successfully signal a crisis if it is “on” also in the year of the crisis. The justification for doing this is that we are using annual data and we cannot distinguish when in the year the crisis occurs and when in the year the indicator goes “on”. (Kaminsky and Reinhart, using monthly data, record a signal as good if a crisis occurs up to one year prior to the signal going on). From a policy perspective, one difficulty with this approach is that remedial action cannot be taken if the signal goes only on at the time that the crisis occurs. (^20) The noise to signal ratio is defined as the ratio of size of Type II errors (i.e. the percentage of non-crisis periods in which a

crisis is incorrectly signalled) to one minus the size of Type I errors (i.e. the percentage of crises that are not correctly predicted). Edison (2000) provides an easy to follow exposition. Where an indicator has been “on” prior to (or at the time of) the crisis and remains on after the beginning of the crisis for either 1 or 2 years we exclude the signals in the years after the crisis from the “noise” calculation (as they are not really false signals). (^21) Moreover, if we define the threshold for real credit growth in terms of the percentile of the distribution over the whole sample

(as do Kaminsky and Reinhart) the noise to signal ratio for a given share of crises predicted is even higher than when the threshold is defined in terms of an (arbitrarily high) absolute growth rate. This suggests that what is important is the absolute growth rate, not the growth rate relative to historical experience. In other words, if the growth rate in a country is generally moderate, the top percentile would be a poor indicator of strains.

Table 1: Performance of indicators A. Horizon = 1 year

Indicator * Asset price gap Credit gap Investment gap Real credit growth

threshold noise /signal predicted% threshold noise /signal predicted% threshold noise /signal predicted% threshold noise /signal predicted%

20 .56 53 3 .29 79 2 .57 58 7 .54 74 30 .44 50 4 .24 79 3 .54 55 8 .47 74 40 .32 50 5 .25 63 4 .50 50 9 .44 68 50 .29 45 6 .25 55 5 .52 42 10 .39 68 60 .29 34 7 .20 55 6 .61 32 11 .36 66 70 .30 24 8 .20 47 7 .55 29 12 .33 66 80 .27 21 9 .18 45 8 .54 26 13 .30 63 90 .43 11 10 .18 37 9 .44 26 14 .30 53

B. Horizon = 2 years

Indicator * Asset price gap Credit gap Investment gap Real credit growth

threshold noise /signal predicted% threshold noise /signal predicted% threshold noise /signal predicted% threshold noise /signal predicted%

20 .40 68 3 .27 79 2 .43 71 7 .43 87 30 .32 63 4 .21 79 3 .42 66 8 .38 84 40 .23 63 5 .20 71 4 .42 55 9 .36 79 50 .20 58 6 .19 63 5 .43 47 10 .31 79 60 .18 47 7 .15 63 6 .42 42 11 .29 74 70 .15 39 8 .16 53 7 .40 37 12 .27 74 80 .17 29 9 .14 50 8 .35 37 13 .25 71 90 .18 21 10 .14 39 9 .29 37 14 .22 66

C. Horizon = 3 years

Indicator * Asset price gap Credit gap Investment gap Real credit growth

threshold noise /signal predicted% threshold noise /signal predicted% threshold noise /signal predicted% threshold noise /signal predicted%

20 .37 71 3 .25 79 2 .37 79 7 .39 89 30 .28 68 4 .20 79 3 .36 74 8 .35 87 40 .19 68 5 .17 74 4 .40 55 9 .31 84 50 .16 66 6 .16 66 5 .41 47 10 .27 84 60 .13 55 7 .13 63 6 .37 45 11 .24 82 70 .12 45 8 .12 58 7 .33 42 12 .23 82 80 .13 .34 9 .10 55 8 .29 42 13 .20 79 90 .14 .26 10 .11 45 9 .23 .42 14 .18 74

*. The threshold values for the credit gap are defined in terms of the deviation in percentage points of the actual credit ratio from the trend ratio. For the other two gaps, the threshold values are expressed as percentage deviations from the trend.