Download 4 BASIC ACCOUNTING PROCEDURES LEDGER AND TRIAL ... and more Lecture notes Accounting in PDF only on Docsity!

CHAPTER - 4

BASIC ACCOUNTING PROCEDURES

LEDGER AND TRIAL BALANCE

In the Journal, each transaction is dealt with separately. Therefore, it is not possible to know at a glance, the net result of many transactions. So, in order to ascertain the net effect of all the transactions relating to a particular account are collected at one place in the Ledger. A Ledger is a book which contains all the accounts whether personal, real or nominal, which are first entered in journal or special purpose subsidiary books. The ledger that is normally used in a majority of business concern is a bound note book. This can be preserved for a long time. Its pages are consequently numbered. Each account in the ledger is opened preferably on a separate page.

The Advantages of ledger:

i. Complete information at a glance: All the transactions pertaining to an account are collected at one place in the ledger. By looking at the balance of that account, one can understand the collective effect of all such transactions at a glance. ii. Arithmetical Accuracy With the help of ledger balances, Trial balance can be prepared to know the arithmetical accuracy of accounts. iii. Result of Business Operations It facilitates the preparation of final accounts for ascertaining the operating result and the financial position of the business concern. iv. Accounting information The data supplied by various ledger accounts are summarized, analyzed and interpreted for obtaining various accounting information.

Format Name of Account Dr. Cr. Date Particulars J.F Amount Date Particulars J.F Amount

Year

Month

Date

To (Name of Credit Account in Journal)

Year Month Date

By (Name of Debit account in Journal)

Explanation: i. Each ledger account is divided into two parts. The left hand side is known as the debit side and the right hand side is known as the credit side. ii. The name of the account is mentioned in the top (middle) of the account. iii. The date of the transaction is recorded in the date column. iv. The word ‘To’ is used before the accounts which appear on the debit side of an account in the particulars column. Similarly, the word ‘By’ is used befo re the accounts which appear on the credit side of an account in the particulars column. v. The name of the other account which is affected by the transaction is written either in the debit side or credit side in the particulars column. vi. The page number of the Journal or Subsidiary Book from where that particular entry is transferred, is entered in the Journal Folio (J.F) column. vii. The amount pertaining to this account is entered in the amount column.

II. Procedure of posting for an Account which has been CREDITED in the journal entry. Step 1. Locate in the ledger the account to be credited and enter the date of the transaction in the date column on the credit side. Step 2. Record the name of the account debited in the Journal in the particulars column on the credit side as “By...... (Name of the account debited)” Step 3. Record the page number of the Journal in the J.F column on the credit side and in the Journal, write the page number of the ledger on which a particular account appears in the L.F. column. Step 4. Enter the relevant amount in the amount column on the credit side.

Illustration. From the following transactions prepare journal entries and post them into ledger. Date Particulars Amount 2015 Feb. 02 03 04 05 06 10 13 15 19 26 28 28 28

Business started with cash Purchased goods for cash Purchased goods from Adel Goods sold for cash Sold to Osman Cash deposited into Rajhi Bank Paid carriage Paid rent Paid for advertisement Commission received Machinery purchased Furniture purchased Cash withdrawn from Rajhi Bank for personal use Goods destroyed by fire

Solution : _Journal Entries in the book of______________________ for the month of _______

Date Particulars L.F. Amount-Dr. Amount-Cr.

Ledger

Cash Account Date Particulars J.F. Amount Date Particulars J. F .

Amount

2015 .Feb. Feb.

Feb.

To Capital a/c 80 , 000 2015.Feb. Feb. Feb.

By Purchase a/c By Rajhi Bank a/c

Capital Account Date Particulars J.F. Amount Date Particulars J.F. Amount 2015 Feb.28 2015 Feb.

Purchase Account Date Particulars J.F. Amount Date Particulars J.F. Amount 2015 Feb. 2015 Feb. 80 , 000

2015 Feb.

Adel’s Account Date Particulars J.F. Amount Date Particulars J.F. Amount 2015 Feb.28 2015 Feb.0 3

Sales Account Date Particulars J.F. Amount Date Particulars J.F. Amount

Osman’s Account Date Particulars J.F. Amount Date Particulars J.F. Amount

Rajhi Bank Account Date Particulars J.F. Amount Date Particulars J.F. Amount

Carriage Account Date Particulars J.F. Amount Date Particulars J.F. Amount

Posting the Opening Entry The opening entry is passed to open the books of accounts for the new financial year. The debit or credit balance of an account what we get at the end of the accounting period is known as closing balance of that account. This closing balance becomes the opening balance in the next accounting year. The procedure of posting an opening entry is same as in the case of an ordinary journal entry. An account which has a debit balance , the words ‘ To balance b/d ’ are recorded on the debit side in the particulars column. An account which has a credit balance , the words “ By balance b/d ” are recorded in the particulars co lumn on the credit side. In fact, opening entry is not actually posted but the accounts are merely incorporated in the ledger, if the ledger is a new one or old.

Illustration 2 Post the opening entry into the ledger of Fahad Co. as on 1st Feb. 2017, cash in hand SR. 10,000; Loan SR. 100,000.

Solution: In the Books of Fahad Cash Account Dr. Cr. Date Particulars J.F. Amount Date Particulars J.F. Amount 2017 Feb.01 10,

Loan Account Dr. Cr. Date Particulars J.F. Amount Date Particulars J.F. Amount 2017 Feb.

Balancing an Account Balance is the difference between the total debits and the total credits of an account. When posting is done, many accounts may have entries on their debit side as well as credit side. The net result of such debits and credits in an account is the balance. Balancing means the writing of the difference between the amount columns of the two sides in the lighter (smaller total) side, so that the grand totals of the two sides become equal.

Significance of balancing There are three possibilities while balancing an account during a given period. It may be a debit balance or a credit balance or a nil balance depending upon the debit total and the credit total.

Step 3 Total again both the amount columns, put the total on both the sides and draw a line above and a line below the totals. Step 4 Enter the date of the beginning of the next period in the date column and bring down the debit balance on the debit side along with the words “ To Balance b/d ” ( b/d means brought down) in the particulars column and the credit balance on the credit side along with the words “ By balance b/d ” in the particulars column.

Trial Balance

As so far you have learnt how to record and classify the transactions in the various accounts along with balancing thereof. The next step in the accounting process is to prepare a statement to check the arithmetical accuracy of the transactions recorded so for. This statement is called ‘ Trial Balance ’. Trial balance is a statement which shows debit balances and credit balances of all accounts in the ledger. Since, every debit should have a corresponding credit as per the rules of double entry system, the total of the debit balances and credit balances should tally (agree). In case, there is a difference, one has to check the correctness of the balances brought forward from the respective accounts. Trial balance can be prepared in any date provided accounts are balanced. Definition “ Trial balance is a statement, prepared with the debit and credit balances of ledger accounts to test the arithmetical accuracy of the books” – J.R. Batliboi.

Methods A trial balance can be prepared in the following methods. i. The Total Method: According to this method, the total amount of the debit side of the ledger accounts and the total amount of the credit side of the ledger accounts are recorded. ii. The Balance Method : In this method, only the balances of an account either debit or credit, as the case may be, are recorded against their respective accounts. The balance method is more widely used, as it supplies ready figures for preparing the final accounts.

Format Trial Balance of ABC Ltd. as on.................. Sl.No Name of Account L.F. Debit Balance Credit Balance

Total

Sundry Debtors and Sundry Creditors In the ledger there are many personal accounts, some of them may show debit balances, some others may show credit balances. If all the names are to be written in the trial balance it will be unduly long. Therefore, a list of names with the debit balances is prepared. This list is known as ‘ Sundry

Debtors ’ (Sundry means ‘ many’ ). Similarly, a list of names with the credit balances is

prepared. This list is known as ‘ Sundry Creditors ’.

Sl.No. Name of Account L.F. Debit Balance Credit Balance

1 2 3 4 5 6 7 8 Capital (Cr.) Drawings Sales (Cr.) Sales return (Return Inwards) Purchases Purchases return (Return Outwards) (Cr.) Expenses Incomes Carriage Inwards

Debit Balance: All assets (Tangible, Intangible, and Current &Fixed) All losses & Expenses

Credit Balance: All gains and Incomes

Personal Account may Debit or Credit Balance as case may be.

Illustration 3 Prepare a Trial Balance from the following items: Particulars Totals Capital Furniture & Fixture Land & Building Plant & Machinery Drawings Patents Stock Purchases Wages Salaries Sundry Debtors Sales Sales Returns Purchases Returns Loan from Ammar Rent, Rates & Taxes Bad Debts Sundry Creditors Discount received Trade Expenses Interest on Loan Insurance Traveling Expenses Cash in Hand Cash at Bank

The Solution is at the NEXT page

Illustration 4 From the following details prepare the trial balance as at 31 July 2009

Name of account Amount (SR) Bank 990 Capital introduced 2000 Motor vehicles 800 Motor expense 180 Purchase 250 A. Brown (trade payable) 60 Sales revenue 450 B.Green(trade receivable) 135 Purchases returns 50 Sales returns 75 Carriage outwards 20 Telephone and postage 65 Heat and light 45

Solution.

Trial Balance as at 31 July 2009 Name of account L.F. Amount (DR) Amount (CR) Bank Capital introduced Motor vehicles Motor expense Purchase A.Brown (trade payable) Sales revenue B.Green(trade receivable) Purchases returns Sales returns Carriage outwards Telephone and postage Heat and light Total

September2010. You are required to prepare a trial balance.

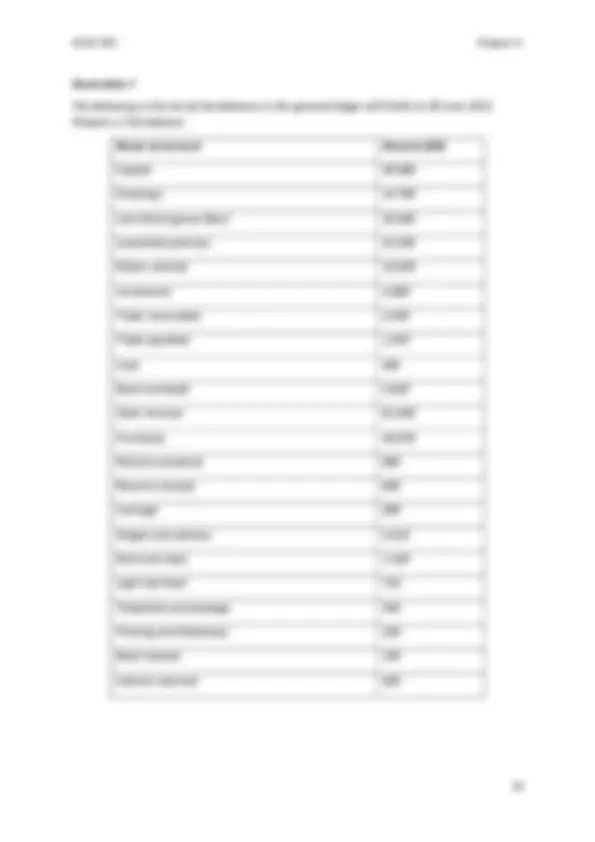

- Illustration

- The following is the list of the balances appearing in the general ledger of T. Wall at

- Capital 32 , Name of account Amount (SR)

- Drawings 5 ,

- Loan from M. Head 10 ,

- Cash

- Bank overdraft 1 ,

- Sales revenue 45 ,

- Purchases 29 ,

- Returns inwards 3 ,

- Returns outwards 2 ,

- Carriage inwards

- Carriage outwards

- Trade receivables 7 ,

- Trade payables 4 ,

- Land and buildings 26 ,

- Plant and machinery 13 ,

- Listed investments 4 ,

- Interest paid 1 ,

- Interest received

- Rent received

- Salaries 3 ,

- Repairs to buildings

- Plant hire charges

- Bank charges