ACC 405

Module 5 Project

Practice Problems and Solutions

Southern New Hampshire University

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

INSTANT PDF DOWNLOAD — ACC 405 Module 5 Project Solutions (2026) with accounting practice exercises, worked solutions, financial reporting tasks, and accounting coursework support. Includes advanced accounting applications, budgeting exercises, journal entries, balance sheet analysis, financial statement preparation, and real-world accounting scenarios designed to strengthen analytical skills and improve assignment and exam success. ACC 405 Module 5, ACC 405 project solutions, accounting practice problems PDF, accounting module 5 answers, ACC405 assignment help, financial accounting solutions, accounting exercises with answers, SNHU ACC 405, accounting project PDF, accounting homework solutions, accounting coursework help, accounting study guide 2026, journal entries practice, financial statement exercises, accounting practice questions, accounting concepts review, accounting solutions manual, accounting class assignment, bookkeeping exercises PDF, accounting project answers

Typology: Exams

1 / 20

This page cannot be seen from the preview

Don't miss anything!

ACC 405 Module 5 Practice Problems

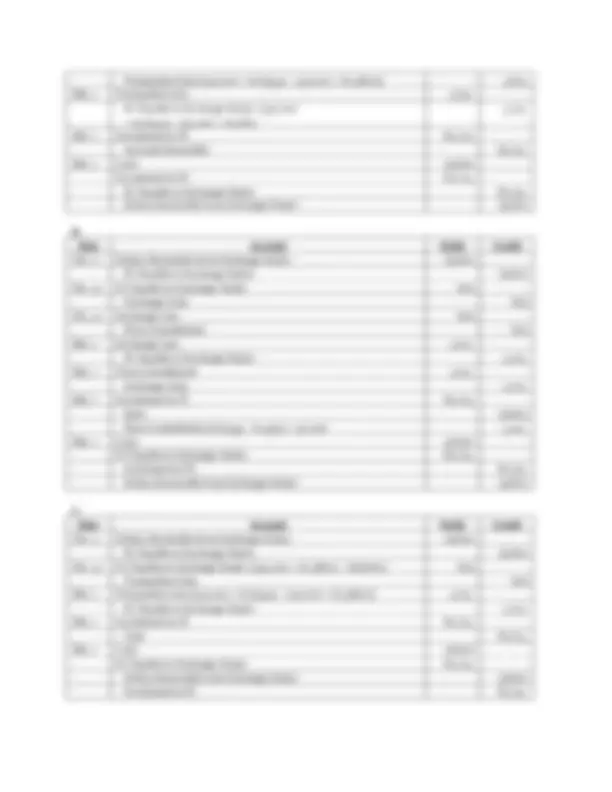

Problem 1. Selco, a U.S. company, imports and exports tools, shop equipment, and industrial construction supplies. The company uses a periodic inventory system. During April, the company entered the following transactions. All rate quotations are direct exchange rates.

April 3 – Purchased power tools from a wholesaler in Japan, on account, at an invoice cost of 1,600,000 yen. On this date the exchange rate for the yen was $0.0072. April 5 – Sold hand tools on credit that were manufactured in the U.S. to a retail outlet located in West Germany. The invoice price was $2,800. The exchange rate for euros was $1.25. April 9 – Sold electric drills on account to a retailer in New Zealand. The invoice price was 16, U.S. dollars and the exchange rate for the New Zealand dollar was $0.76. April 11 – Purchased drill bits on account from a manufacturer located in Belgium. The billing was for 801,282 euros. The exchange rate for euro was $1.26. April 16 – Paid 1,000,000 yen on account to the wholesaler for purchases made on April 3. The exchange rate on this date was $0.0067. April 18 – Settled the accounts payable with the Belgium manufacturer. The exchange rate was $1.28. April 22 – Received full payment from the New Zealand retailer. The exchange rate was $0.74. April 30 – Completed payment on the April 3 purchase. The exchange rate for yen was $0.0078.

Required: Prepare journal entries on the books of Selco to record the transactions listed above.

Date Account Debit Credit Apr. 3 Purchases 11, Accounts Payable (1,600,000 × $0.0072) 11, Apr. 5 Accounts Receivable 2, Sales 2, Apr. 9 Accounts Receivable 16, Sales 16, Apr. 11 Purchases 25, Accounts Payable (801,282 × $0.0312) 25, Apr. 16 Accounts Payable (1,000,000 × $0.0072) 7, Transaction Gain 500 Cash (1,000,000 × $0.0067) 6, Apr. 18 Accounts Payable 25, Transaction Loss 4, Cash (801,282 × $0.0368) 29, Apr. 22 Cash 16, Accounts Receivable 16, Apr. 30 Accounts Payable (600,000 × $0.0072) 4, Transaction Loss 360 Cash (600,000 × $0.0078) 4,

Problem 2. Crystal Exporting Co. is a U.S. wholesaler engaged in foreign trade. The following transactions are representative of its business dealings. The company uses a periodic inventory system and is on a calendar-year basis. All exchange rates are direct quotations.

Problem 3. Apple Company was incorporated in Delaware in 2012. On November 9, 2019, the controller of the company entered into a forward contract to sell 50,000 British pounds for $1.5920 on March 1, 2020. The following exchange rates were quoted on the indicated dates:

Date Spot Rate Forward Rate Nov. 2, 2019 $1.6021 1. Dec. 31, 2019 1.5820 1. Mar. 1, 2020 1.

Apple Company’s fiscal year-end is December 31.

Required: A. Assume that the forward contract was entered into as a hedge against an exposed foreign currency receivable balance in the amount of £50,000. Prepare the journal entries that would be made by Apple Company on: Nov. 2 – Record the sale of the goods on account for £50,000 and to record the forward contract. Dec. 31 – To adjust the accounts related to the exposed asset and forward contract at fiscal year-end. Mar. 1 – To adjust the accounts related to the exposed asset and forward contract and to record the settlement of the receivable and delivery of the pounds to the exchange dealer. B. Assume that the controller indicated on November 2 that the forward contract was acquired as a hedge of a future foreign currency transaction that is a commitment of Apple to sell inventory for £50,000 on March 1. Apple Company designates this hedge as a fair value hedge of an unrecognized firm commitment. Prepare the journal entries related to the forward contract and commitment to sell inventory that would be made by Apple Company on November 2, December 31, and March 1. C. Assume that the contract was entered into to speculate in future exchange rate fluctuations. Prepare the journal entries that would be made by Apple Company on November 2, December 31, and March 1. D. Compute the effect of the transactions in A., B., and C. on the net income for the fiscal years ended December 31, 2019 and December 31, 2020. Indicate how the balance sheet accounts related to the forward contract would be reported in the December 31, 2019 balance sheet.

A. Date Account Debit Credit Nov. 2 Accounts Receivable 80, Sales (50,000 × $1.6021) 80, Nov. 2 Dollars Receivable from Exchange Dealer (50,000 × $1.5920) 79, FC Payable to Exchange Dealer 79, Dec. 31 Transaction Loss 1, Accounts Receivable [(50,000 × $1.5920) – $80,105] 1, Dec. 31 FC Payable to Exchange Dealer 600 Transaction Gain [(50,000 × $1.58) – $79,600] 600 Mar. 1 Accounts Receivable 3,

C.

- Transaction Gain [(50,000 × $1.6543) – (50,000 × $1.5820)] 3,Feb. 25 Option to Sell Francs 3, Exchange Gain – Other Comprehensive Income 3, To adjust the option value to its current realizable value of $12,000: The value of the option [($0.60 exercise price – $0.57 spot rate) × 400,000 francs] of 12,000 less the carrying value of the option ($9,000) Feb. 25 Cash (400,000 × $0.60) 240, Option to Sell Francs 12, Payable to Option Trader (400,000 × $0.57) 228, To exercise the option and settle with the trader.

Problem 5. On October 1, 2019, Fairchange Corporation ordered some equipment from a supplier for 300,000 euros. Delivery and payment are to occur on November 15, 2019. The spot rates on October 1 and November 15, 2019, are $1.20 and $1.30, respectively.

Required: A. Assume that Fairchange entered into a forward contract on October 1, 2019, to hedge the firm commitment. The forward rates for euros for November 15 delivery were as follows:

October 1 $1. November 15 $1.

Furthermore, assume the equipment was purchased and paid for on November 15. Prepare all journal entries needed to record and settle the hedge and to record the purchase of the equipment.

B. If the forward contract was not acquired, record the journal entry to purchase the equipment.

A. Settlement date should be stated as 11/15/ Date Account Debit Credit Oct. 1 FC Receivable from Exchange Dealer (300,000 × $1.23) 369, Dollars Payable to Exchange Dealer 369, Nov. 15 FC Receivable from Exchange Dealer 21, Foreign Exchange Gain [300,000 × ($1.30 – $1.23)] 21, Nov. 15 Foreign Exchange Loss 21, Firm Commitment 21, Nov. 15 Investment in FC (300,000 × $1.30) 390, Dollars Payable to Exchange Dealer 369, FC Receivable from Exchange Dealer 390, Cash 369, Nov. 15 Firm Commitment 21, Equipment 369, Investment in FC 390,

B. Date Account Debit Credit Nov. 15 Equipment 390,

Cash 390,

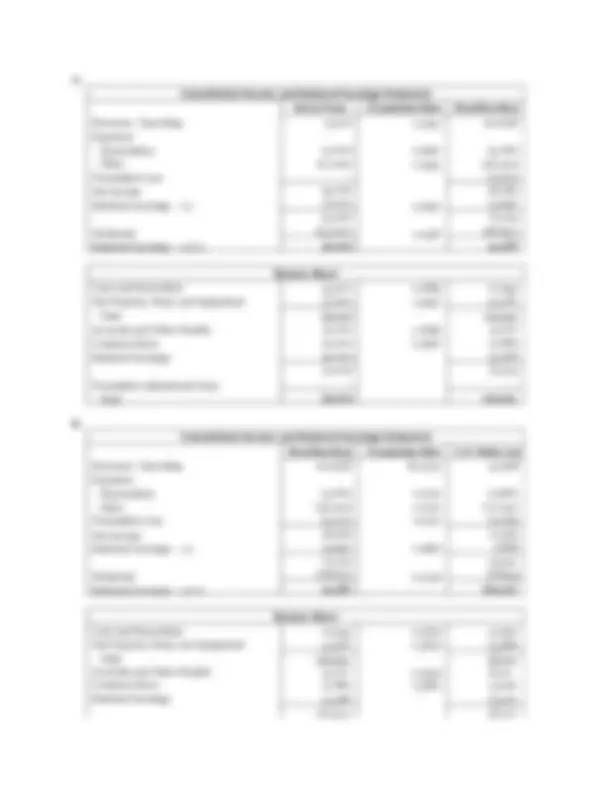

Problem 6. On January 1, 2014, Trenton Systems, a U.S.-based company, purchased a controlling interest in Grant Management Consultants, located in Zurich, Switzerland. The acquisition was treated as a purchase transaction. The 2014 financial statements stated in Swiss francs are below.

GRANT MANAGEMENT CONSULTANTS Comparative Balance Sheets January 1 and December 31, 2014

Cash and Receivables Net Property, Plant, and Equipment Total Accounts and Notes Payable Common Stock Retained Earnings Total

Jan. 1 Dec. 31 20,000 55, 40,000 37, 60,000 92, 30,000 32, 20,000 20, 10,000 40, 60,000 92,

Consolidated Income and Retained Earnings Statement for the Year Ended December 31, 2014 Revenues Operating Expenses (including Depreciation of 3,000 francs) Net Income Dividends Declared and Paid Increase in Retained Earnings

Direct exchange rates for Swiss franc are as follows:

Dollars per Swiss Franc January 1, 2014 $1. December 31, 2014 1. Average for 2014 1. Dividend declaration and payment date 1.

Required: A. Translate the end-of-year balance sheet and income statement of the foreign subsidiary using the current rate method of translation. B. Prepare a schedule to verify the translation adjustment.

A. Consolidated Income and Retained Earnings Statement

Revenues Operating Expenses Net Income Retained Earnings – 1/

Dividends

Swiss Franc Translation Rate U.S. Dollar ($) 75, (30,000)

Consolidated Income and Retained Earnings Statement

Revenues Operating Expenses: Depreciation Other Translation Loss Net Income Retained Earnings – 1/

Dividends Retained Earnings – 12/

Swiss Franc Translation Rate Brazilian Real 75,

(3,000) (27,000)

Balance Sheet Cash and Receivables Net Property, Plant, and Equipment Total Accounts and Notes Payable Common Stock Retained Earnings

Translation Adjustment (loss) Total

Consolidated Income and Retained Earnings Statement

Revenues Operating Expenses: Depreciation Other Translation Loss Net Income Retained Earnings – 1/

Dividends Retained Earnings – 12/

Brazilian Real Translation Rate U.S. Dollar ($) 100,

(4,182) (36,302) (2,271)

Balance Sheet Cash and Receivables 70,945 0.4630 32, Net Property, Plant, and Equipment 51,578^ 0.4630 23, Total 122,

Accounts and Notes Payable 41,277 19, Common Stock 27,880 0.4891 13, Retained Earnings 53,366 25, 122,523 58,

Translation Adjustment (loss) Total

Problem 8. Dorsey Corporation purchased 90% of common stock of Lansing Company on January 1,

LANSING COMPANY Consolidated Income and Retained Earnings Statement for the Year Ended December 31, 2014 Sales 2,900, Cost of Goods Sold (1,400,000) Depreciation Expense (300,000) Other Expenses (400,000) Net Income 800, Retained Earnings – 1/1 900,

Less: Dividends Declared and Paid Dec. 31

Retained Earnings – 12/31 1,375,

Balance Sheet December 31, 2014 Cash and Receivables 1,275, Merchandise Inventory 490, Property, Plant, and Equipment 3,450, Total 5,215, Current Liabilities 640, Long-Term Notes Payable 1,200, Capital Stock 2,000, Retained Earnings 1,375, Total 5,215,

Lansing Company was incorporated on January 1, 2006, at which time all the property, plant, and equipment was purchased. The long-term notes were issued to partially finance the purchase of the fixed assets. Direct exchange rates for the British pound are as follows:

January 1, 2006 $1. January 1, 2008 1. Average for last quarter 2018 1. January 1, 2019 1. December 31, 2019 1. Average for 2019 1. Average for Aug. – Dec. 2019 1.

Total 2,615,000 2,855, Short-Term Accounts and Notes Payable 295,000 210, Long-Term Notes 600,000 680, (600,000 issued 9/1/2006 and 80,000 issued 1/1/2019) Common Stock 800,000 800, Additional Paid-In Capital 200,000 200, Retained Earnings 720,000 965, Total 2,615,000^ 2,855,

Consolidated Income and Retained Earnings Statement for the Year Ended December 31, 2019 Revenues 3,225, Cost of Goods Sold: Beginning Inventory 600, Purchases 1,200, Cost of Goods Available for Sale 2,700, Less: Ending Inventory (500,000) Cost of Goods Sold 2,200, Gross Profit on Sales 1,025, Depreciation Expense 140, Other Expenses 540,000 680, Net Income 345, Retained Earnings – 1/1 720, Total 1,065, Less: Dividends Paid (100,000) Retained Earnings – 12/31 965,

The account balances are computed in conformity with U.S. generally accepted accounting standards. Other information is as follows:

Equipment – Purchased July 1, 2019 10,

Required: A. Translate the financial statements into dollars assuming that the local currency of the foreign subsidiary was identified as its functional currency. B. Prepare a schedule to verify the translation adjustment determined in requirement A. Describe how the translation adjustment would be reported in the financial statements.

A. Consolidated Income and Retained Earnings Statement

Revenues Cost of Goods Sold Depreciation Expense Other Expenses Net Income Retained Earnings – 1/

Less: Dividends Declared – 7/ Dividends Declared – 12/ Retained Earnings – 12/

New Zealand $ Translation Rate U.S. Dollar $ 3,225, 2,200, 140, 540,

Balance Sheet Cash and Receivables 880,000 0.7298 642, Inventories 500,000 0.7298 364, Land 400,000 0.7298 291, Building (net) 605,000 0.7298 441, Equipment (net): Purchased before 1/1 380,000 0.7298 277, Purchased 7/1 90,000 0.7298 65, Total 2,855,000 2,083, Short-Term Accounts and Notes 210,000 0.7298 153, Long-Term Notes 680,000 0.7298 496, Common Stock 800,000 0.7924 633, Additional Paid-In Capital 200,000 0.7924 158, Retained Earnings 965,000 755, Total 2,855,000^ 2,196, Cumulative Translation Adjustment – (113,381) Total 2,855,000^ 2,083,

B.

Exposed net asset position – 1/

New Zealand $ Translation Rate U.S. Dollar $ 1,720,000 $0.7924 1,362,

Schedule 1 – Translation of Cost of Goods Sold

Beginning Inventory Purchases

Less: Ending Inventory Cost of Goods Sold

New Zealand $ Translation Rate U.S. Dollar $ 600,000 0.7924* 475, 2,100,000 0.7480 1,570, 2,700,

Schedule 2 – Translation of Depreciation Expense Buildings 45,000 0.7924 35, Equipment on hand 1/1 85,000 0.7924 67, Equipment purchased 7/1 10,000 0.7412 7, Total 140,000 110, *Translation rate is the January 1, 2019 rate, the date the equity interest was acquired, rather than the $0.7480 rate in effect when the inventory was purchased.

B.

Exposed net monetary liability position – 1/ (295,000 + 600,000 – 500,000) Less: Increase in cash and receivables from sales Add: Decrease in monetary assets or increase in monetary liabilities: Purchases Other expenses Dividends 7/ Dividends 12/ Purchase of equipment – 7/ Net monetary liability position translation using rates in effect at date of each transaction Exposed net monetary liability position – 12/31 (210,

New Zealand $ Translation Rate U.S. Dollar $ 395,000 $0.7924 312,

(3,225,000) 0.7480 (2,412,300)

Problem 11. Jose, Jill, and Salil decided to engage in a real estate venture as a partnership. Jose invested $100,000 cash and Jill provided office equipment that is carried on her books at $82,000. The partners agree that the equipment has a fair value of $110,000. There is a $30,000 note payable remaining on the equipment to be assumed by the partnership. Although Salil has no physical assets to invest in the partnership, both Jose and Jill believe that his experience as a real estate appraiser is a valuable skill needed by the partnership and is a basis for granting him a capital interest in the partnership.

Required: Assuming that each partner is to receive an equal capital interest in the partnership, A. Record the partnership formation under the bonus method. B. Record the partnership formation under the goodwill method and assume a total goodwill of $90,000. C. Discuss the appropriations of using either the bonus or goodwill methods to record the formation of the partnership.

Bonus Method Cash 100, Equipment 110, Note Payable 30, Jose, Capital 60, Jill, Capital 60, Salil, Capital 60,

B. Goodwill Method Cash 100, Equipment 110, Goodwill 90, Note Payable 30, Jose, Capital 90, Jill, Capital 90, Salil, Capital 90,

C. Agreed Fair Values

Cash Equipment Total assets Note payable assumed by partnership Net assets invested

Invested by Jose Invested by Jill Invested by Salil $100,

Problem 12. Jones, Silva, and Thompson form a partnership and agree to allocate income equally after recognition of 10% interest on beginning capital balances and monthly salary allowances of $2,000 to Jones and $1,500 to Thompson. Capital balances on January 1 were as follows:

Jones $40, Silva 25, Thompson 30,

Calculate the net income (loss) allocation to each partner under each of the following independent situations:

Jones Silva Thompson Total

Problem 14. Disha, Brianna, and Pheobe are partners in a retail appliance store. The partnership was formed January 1, 2019, with each partner investing $45,000. They agreed that profits and losses are to be shared as follows:

Operating performance and other capital transactions were as follows:

Capital Transactions Disha Brian n

a Pheob e

Year-End Net Income (Loss) Investment Withdrawals Investment Withdrawals Investment Withdrawals

12/31/201 ($5,400) $15,000 $17,000 $15,000 $7,000 $6,000 $3, 9 12/31/202 27,000 0 17,000 0 7,000 6,000 3, 0 12/31/202 120,000 0 19,000 0 9,000 6,000 3, 1

Required: A. Prepare a schedule of changes in partners’ capital accounts for each of the three years. B. Prepare the journal entry to close the income summary account to the partners’ capital accounts at the end of each year.

A.

December 31, 2019 Beginning capital balances – 1/ Add: Investments

Less: Withdrawals Net loss allocation Capital balances – 12/

Disha Brianna Pheobe Total

December 31, 2020 Beginning capital balances – 1/1 $41,200 $51,200 $46,000 $138, Add: Investments 0 0 6,000 6, Net income allocation (40:30:30) 10,800 8,100 8,100 27,

Less: Withdrawals Capital balances – 12/

December 31, 2021 Beginning capital balances – 1/1 $35,000 $52,300 $56,900 $144, Add: Investments 0 0 6,000 6, Net income allocation: Salaries 42,000 30,000 18,000 90, Bonus* 8,889 8, Interest 3,500 5,230 5,690 14, Residual – Equally divided 2,230 2,231 2,230 6,

Less: Withdrawals

Capital balances – 12/31 $63,730 $89,650 $85,620 $239, *Bonus is calculated as follows: Bonus = 0.08 × (NI – B) B = 0.08 × ($120,000 – B) B = $9,600 – 0.08B 1.08B = $9, B = $8,

B. Closing Journal Entries December 31, 2019 Disha, Capital 1, Brianna, Capital 1, Pheobe, Capital 1, Income Summary 5, December 31, 2020 Income Summary 27, Disha, Capital 10, Brianna, Capital 8, Pheobe, Capital 8, December 31, 2021 Income Summary 120, Disha, Capital 47, Brianna, Capital 46, Pheobe, Capital 25,