1-1

Prepared by

Coby Harmon

University of California, Santa Barbara

Intermediate

Accounting

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Intermediate Accounting Notes - Financial Accounting - Chapter 1

Typology: Slides

1 / 51

This page cannot be seen from the preview

Don't miss anything!

1- 1

Prepared by Coby Harmon University of California, Santa Barbara

1- 2

1

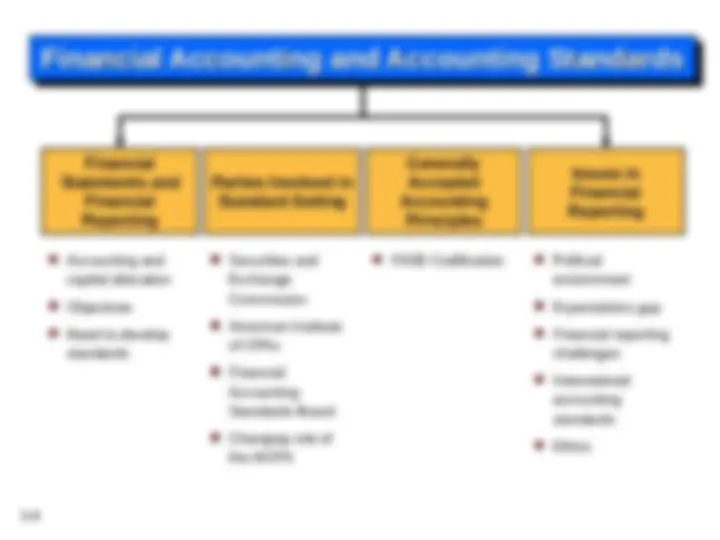

Financial Accounting and

Accounting Standards

Kieso, Weygandt, and Warfield

1- 4

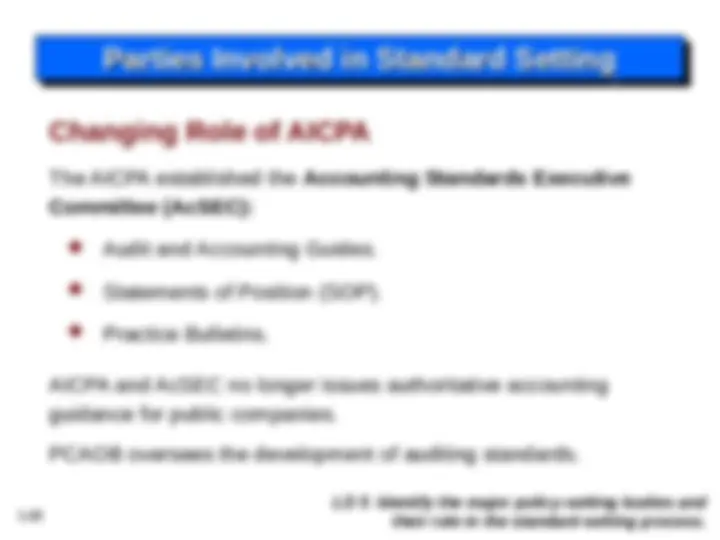

Securities and Exchange Commission American Institute of CPAs Financial Accounting Standards Board Changing role of the AICPA

Financial Statements and Financial Reporting

Parties Involved in Standard-Setting

Generally Accepted Accounting Principles

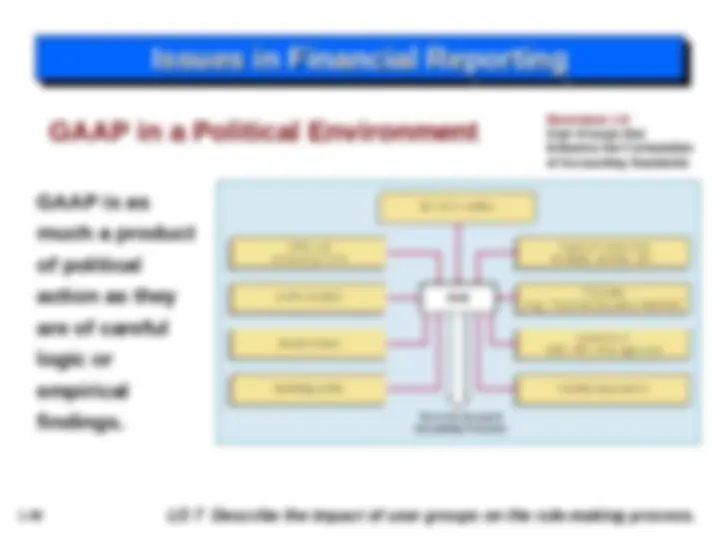

Issues in Financial Reporting

Accounting and capital allocation Objectives Need to develop standards

FASB Codification Political environment Expectations gap Financial reporting challenges International accounting standards Ethics

Financial Accounting and Accounting StandardsFinancial Accounting and Accounting StandardsFinancial Accounting and Accounting Standards Financial Accounting and Accounting Standards

1- 5

Financial Statements and Financial ReportingFinancial Statements and Financial ReportingFinancial Statements and Financial Reporting Financial Statements and Financial Reporting

Essential characteristics of accounting are:

LO 1 Identify the major financial statements and other means of financial reporting.

1- 7

Financial Statements and Financial ReportingFinancial Statements and Financial ReportingFinancial Statements and Financial Reporting Financial Statements and Financial Reporting

LO 1 Identify the major financial statements and other means of financial reporting.

Review Question

1- 8

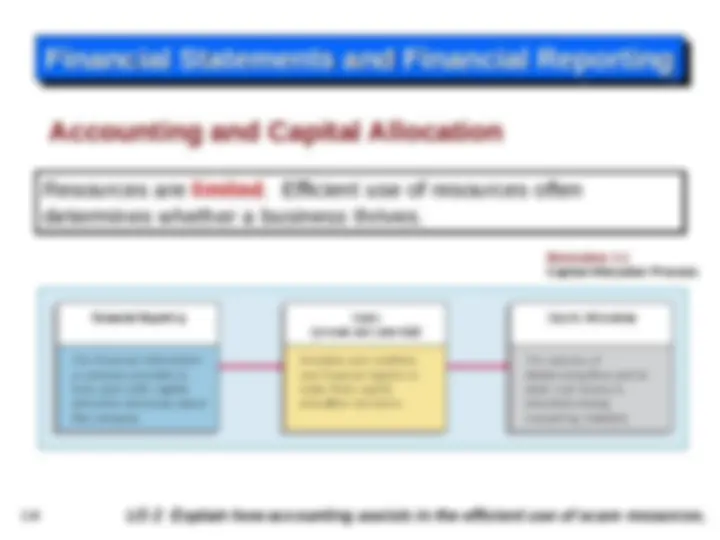

LO 2 Explain how accounting assists in the efficient use of scare resources.

Illustration 1- Capital Allocation Process

Accounting and Capital Allocation

Financial Statements and Financial ReportingFinancial Statements and Financial ReportingFinancial Statements and Financial Reporting Financial Statements and Financial Reporting

1- (^10) LO 3 Identify the objectives of financial reporting.

Objectives of Financial Reporting

Financial Statements and Financial ReportingFinancial Statements and Financial ReportingFinancial Statements and Financial Reporting Financial Statements and Financial Reporting

1- 11

Equity Investors and Creditors

Objective of Financial AccountingObjective of Financial AccountingObjective of Financial Accounting Objective of Financial Accounting

General-Purpose Financial Statements

LO 3 Identify the objectives of financial reporting.

1- 13

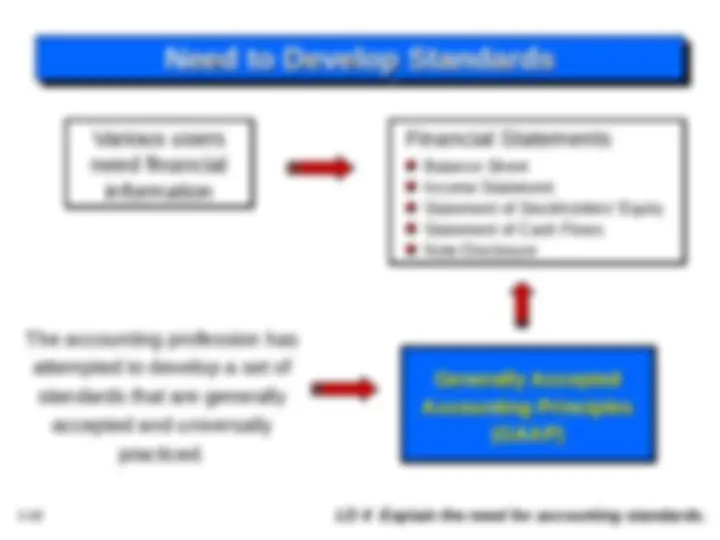

Need to Develop StandardsNeed to Develop StandardsNeed to Develop Standards Need to Develop Standards

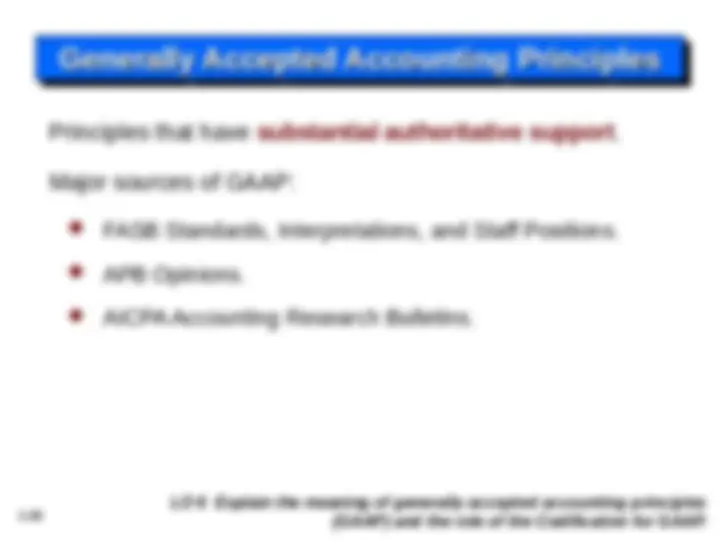

The accounting profession has attempted to develop a set of standards that are generally accepted and universally practiced.

Balance Sheet Income Statement Statement of Stockholders’ Equity Statement of Cash Flows Note Disclosure

Balance Sheet Income Statement Statement of Stockholders’ Equity Statement of Cash Flows Note Disclosure

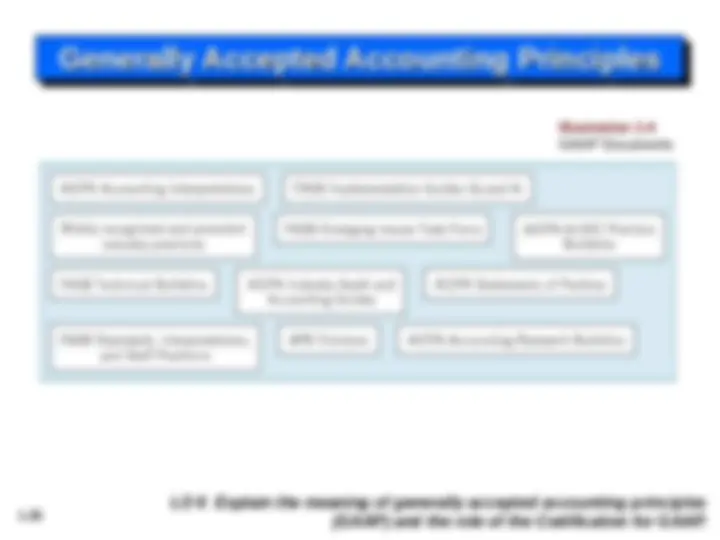

Generally Accepted Generally Accepted Accounting Principles Accounting Principles (GAAP) (GAAP)

Generally Accepted Generally Accepted Accounting Principles Accounting Principles (GAAP) (GAAP)

LO 4 Explain the need for accounting standards.

1- 14

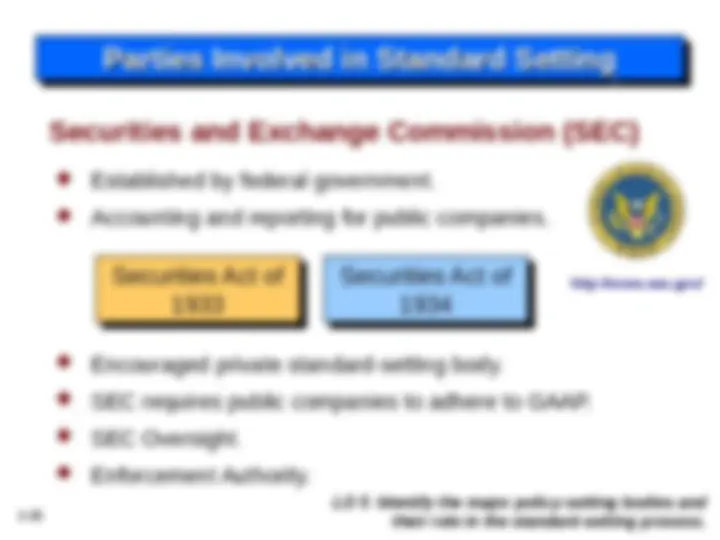

Parties Involved in Standard SettingParties Involved in Standard SettingParties Involved in Standard Setting Parties Involved in Standard Setting

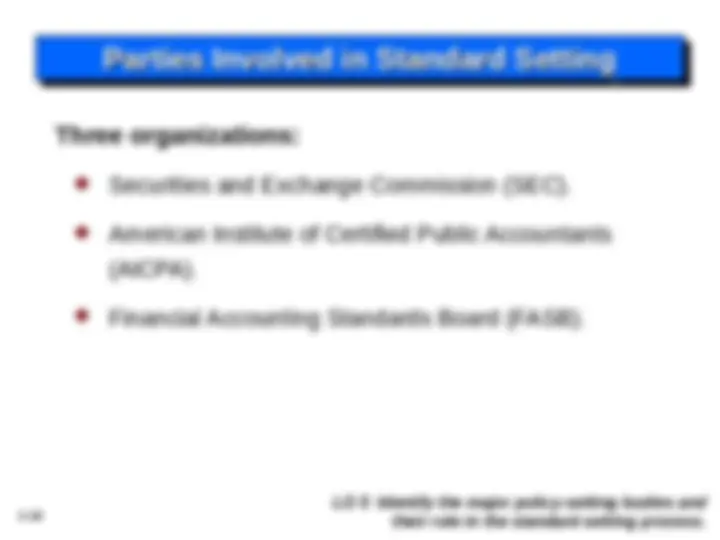

Three organizations:

(^) Securities and Exchange Commission (SEC).

(^) American Institute of Certified Public Accountants

(AICPA).

(^) Financial Accounting Standards Board (FASB).

LO 5 Identify the major policy-setting bodies and their role in the standard-setting process.

1- 16 LO 5

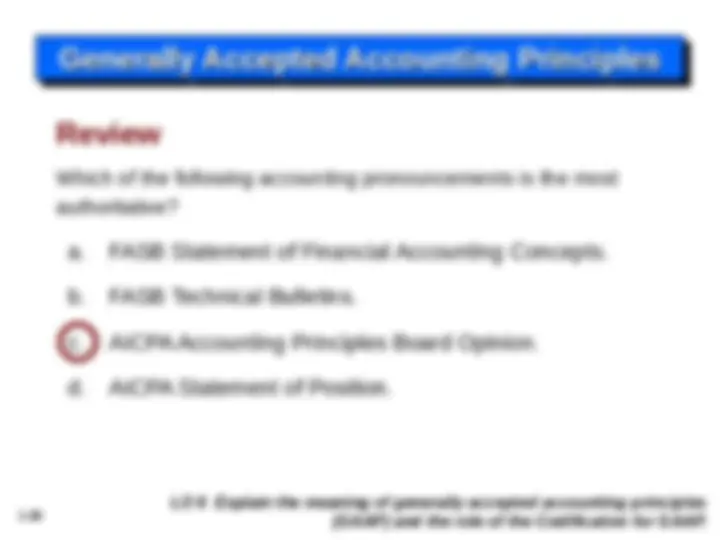

(^) 1939 to 1959 (^) Issued 51 Accounting Research Bulletins (ARBs) (^) Problem-by-problem approach failed

(^) 1959 to 1973 (^) Issued 31 Accounting Principle Board Opinions (APBOs) (^) Wheat Committee recommendations adopted in 1973

http://www.aicpa.org/

American Institute of CPAs (AICPA)

Parties Involved in Standard SettingParties Involved in Standard SettingParties Involved in Standard Setting Parties Involved in Standard Setting

1- 17

Wheat Committee’s recommendations resulted in creation of FASB.

Financial Accounting Foundation

Financial Accounting Foundation

(^) Selects members of the FASB. (^) Funds their activities. (^) Exercises general oversight.

Financial Accounting Standards Board

Financial Accounting Standards Board

Financial Accounting Standards Advisory Council

Financial Accounting Standards Advisory Council

(^) Mission to establish and improve standards of financial accounting and reporting.

(^) Consult on major policy issues.

LO 5

Financial Accounting Standards Board (FASB)

Parties Involved in Standard SettingParties Involved in Standard SettingParties Involved in Standard Setting Parties Involved in Standard Setting

1- 19

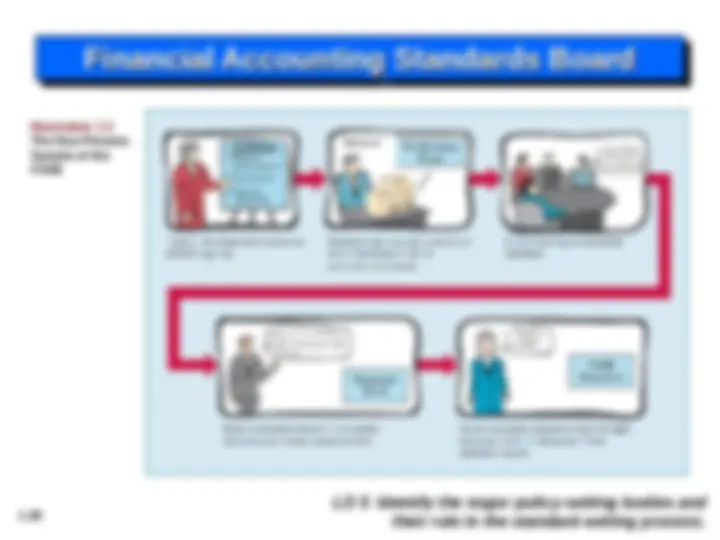

The first step taken in the establishment of a typical FASB statement is

Financial Accounting Standards BoardFinancial Accounting Standards BoardFinancial Accounting Standards Board Financial Accounting Standards Board

Review

LO 5 Identify the major policy-setting bodies and their role in the standard-setting process.

1- 20

Illustration 1- The Due Process System of the FASB

Financial Accounting Standards BoardFinancial Accounting Standards BoardFinancial Accounting Standards Board Financial Accounting Standards Board

LO 5 Identify the major policy-setting bodies and their role in the standard-setting process.