Download Accounting - Cost Accounting and more Study notes Accounting in PDF only on Docsity!

COST ACCOUNTING

Meaning : Cost Accounting is the classifying , recording

and appropriate allocation of expenditure for

the determination of the costs of products or

services, and for the presentation of suitably

arranged data for the purposes of control and guidance

of management.

Features

It is a process of accounting for costs

It records income and expenditure relating to production of

goods and services

It provides statistical data on the basis of which future

estimates are prepared and quotations are submitted

It is concerned with cost ascertainment, cost control and

cost reduction

It establishes budgets and standards so that actual cost

may be compared to find out deviations or variances

It involves the preparation of right information to the right

person at the right time so that it may be helpful to

management for planning, evaluation of performance,

control and decision making

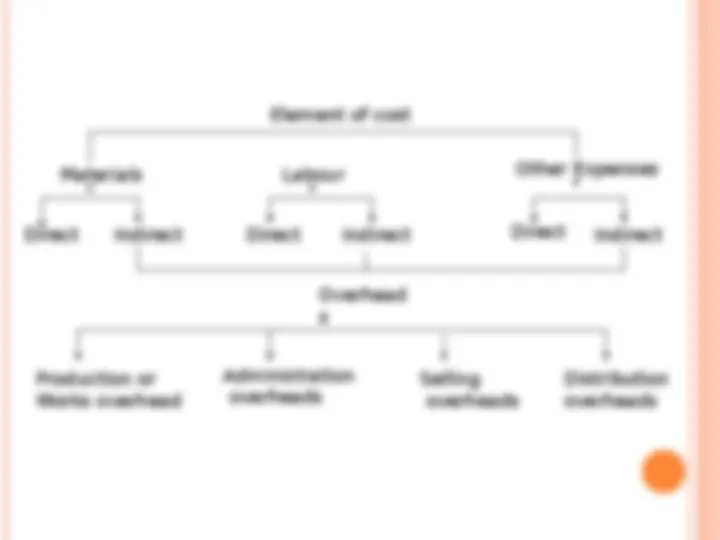

Element of cost Materials Labour Other Expenses Direct Indirect Direct Indirect Direct^ Indirect Overhead s Production or Works overhead Administration overheads Selling overheads Distribution overheads

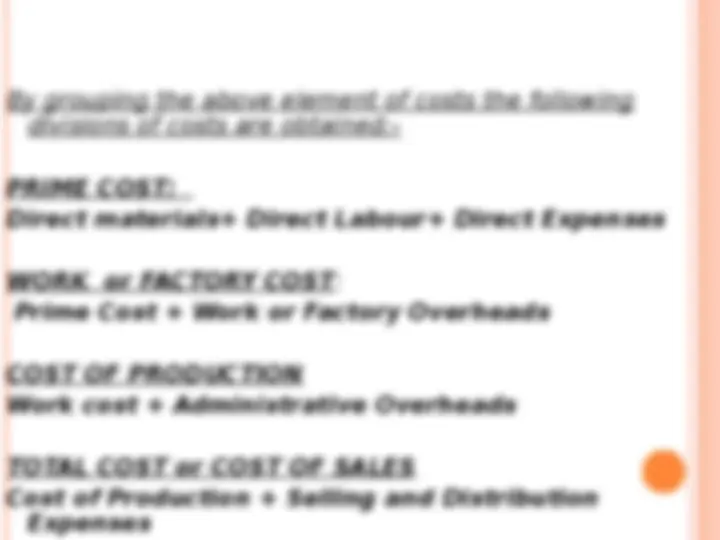

By grouping the above element of costs the following divisions of costs are obtained:- PRIME COST: Direct materials+ Direct Labour+ Direct Expenses WORK or FACTORY COST : Prime Cost + Work or Factory Overheads COST OF PRODUCTION Work cost + Administrative Overheads TOTAL COST or COST OF SALES Cost of Production + Selling and Distribution Expenses

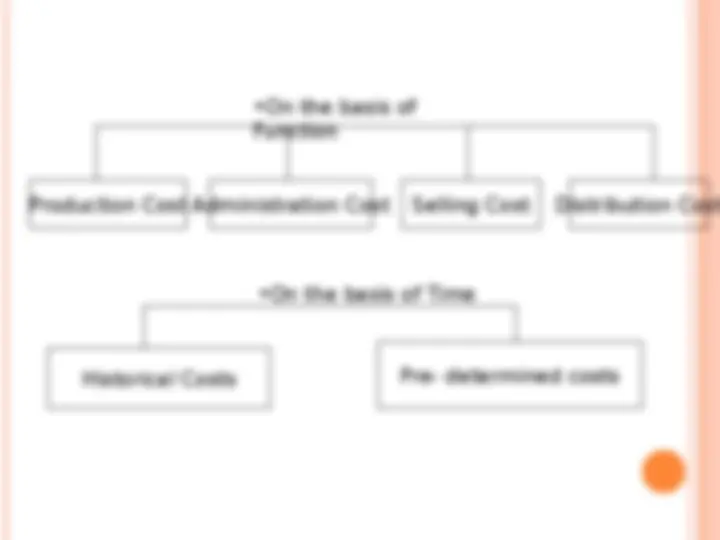

- (^) Classification on the basis of

Element

Material Cost Labour Cost

Expenses

- Classification on the basis of

Nature

Direct Cost (^) Indirect Cost

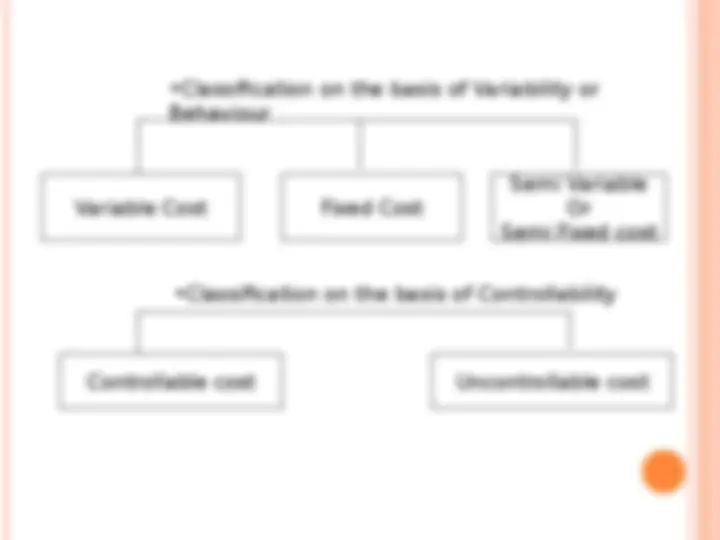

- Classification on the basis of Variability or

Behaviour

Variable Cost Fixed Cost

Semi Variable

Or

Semi Fixed cost

- Classification on the basis of Controllability

Controllable cost Uncontrollable cost

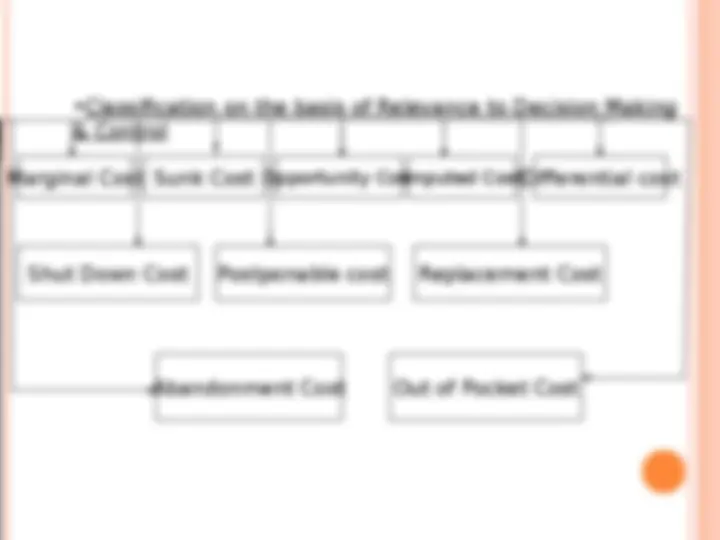

- Classification on the basis of Relevance to Decision Making

& Control

Marginal Cost Sunk Cost Opportunity CostImputed CostDifferential cost

Shut Down Cost Postponable cost Replacement Cost

Abandonment Cost Out of Pocket Cost

COST SHEET The calculation of cost of production at various stages can be shown by means of a statement called cost sheet Cost sheet is an analytical presentation of the cost of the product in the form of a statement and shows the various elements and components of cost

VALUATION OF INVENTORIES

The value of materials has a direct bearing on the

income of a concern, so it is necessary that a

method of pricing materials should be such that it

gives a realistic value of stocks. Different methods

can be used for the purpose of valuation of

inventories. The actual method to be adopted in a

manufacturing concern shall depend upon the

nature of materials and the nature of the

business itself.

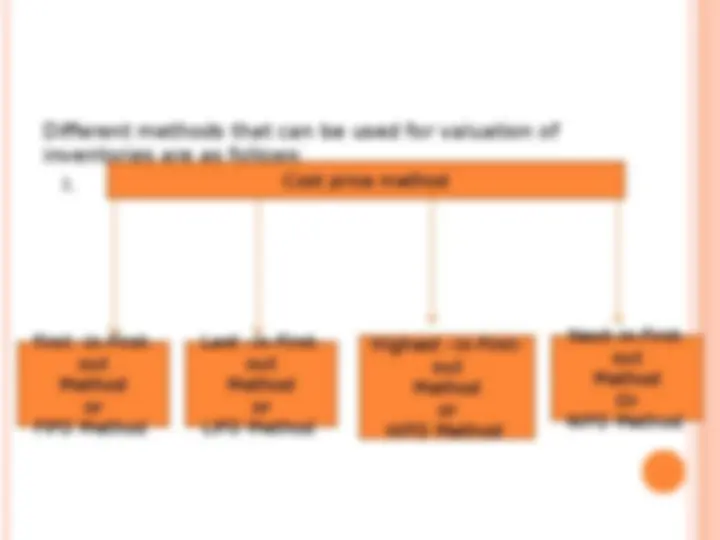

Different methods that can be used for valuation of

inventories are as follows:

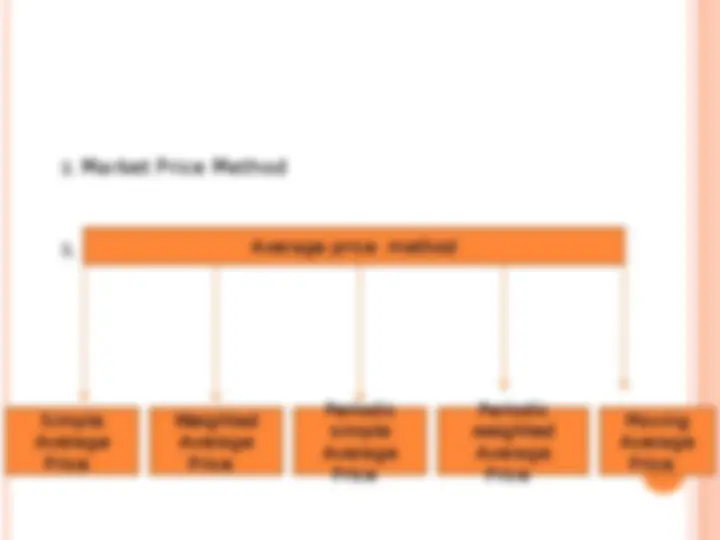

Cost price method First –in-First- out Method or FIFO Method Last –in-First- out Method or LIFO Method Highest –in-First- out Method or HIFO Method Next–in-First- out Method Or NIFO Method

4. Fixed Price Method or Standard Price Method

5. Inflated Price Method

6. Base Stock Method

Selection Of A Proper Method Of Valuation

The selection will be made by taking into account a number of

factors which

May be given as follows:

The nature of production – whether intermittent or continuous.

Volume/ Frequency of receipts of materials.

Variations and fluctuations in prices and their nature

Frequency of issue of material

Stock turnover rate.

Effect of pricing method on tax payable.

Clerical labour involved in the method.

Traceability of the issue to the particular lot or consignment.

Nature of the cost accounting system followed.