Bulacan Polytechnic College

Your Partner to Reach the World

FINANCIAL ACCOUNTING

AND REPORTING 1

FAR 113

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

We the sovereign people filipino

Typology: Lecture notes

1 / 17

This page cannot be seen from the preview

Don't miss anything!

Bulacan Polytechnic College

FAR 113

Bulacan Polytechnic College Your Partner to Reach the World

Information Sheet 6

Bulacan Polytechnic College

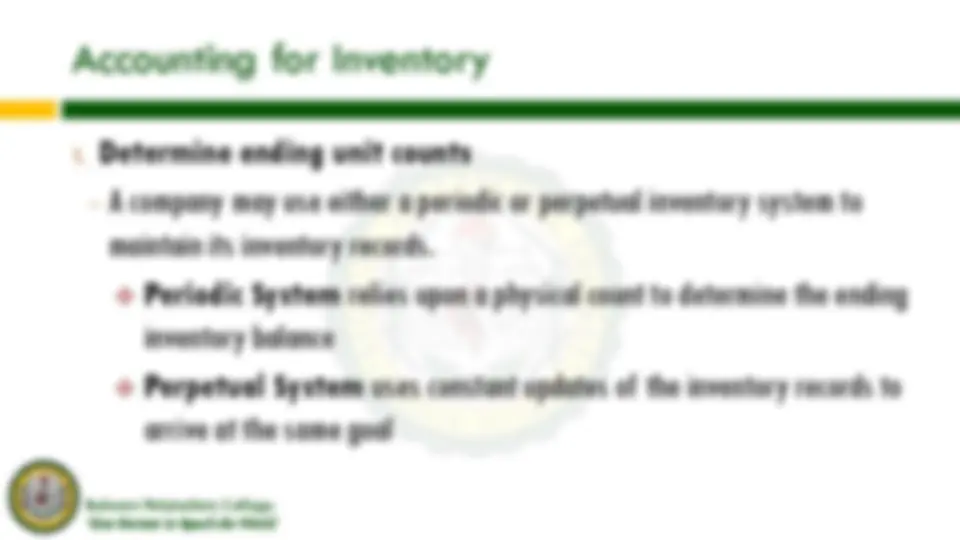

1. Determine ending unit counts − A company may use either a periodic or perpetual inventory system to maintain its inventory records. ❖ Periodic System relies upon a physical count to determine the ending inventory balance ❖ Perpetual System uses constant updates of the inventory records to arrive at the same goal

Bulacan Polytechnic College

➢ is easier to implement but is less robust than the perpetual system ➢ The Purchases account is not an expense or asset The account Inventory : − has only the ending balance from the previous accounting year − excludes the cost of purchases, purchases returns and allowances, etc. since these are recorded as separate accounts

Bulacan Polytechnic College

− A supplier may require that a customer first obtain an “RMA” or “Return Merchandise Authorization.” This indicates a willingness on the part of the supplier to accept the return. − Debit Memorandum may be prepared to indicate that the purchaser is to debit their Accounts Payable account; the corresponding credit is to Purchases Returns and Allowances

Bulacan Polytechnic College

When determining the amount of inventory owned at year-end, goods in transit must be considered in light of the F.O.B. (Freight on Board) terms.

Bulacan Polytechnic College

Sold items worth P5,000 on account (5 items) Accounts Receivables 5, Sales P5, Cost of Goods Sold P 4, Inventory P4, Customer returned 2 items from the previous transaction Sales Return and Allowances P2, Accounts Receivables P2, Inventory P1, Cost of Goods Sold P1,

Bulacan Polytechnic College

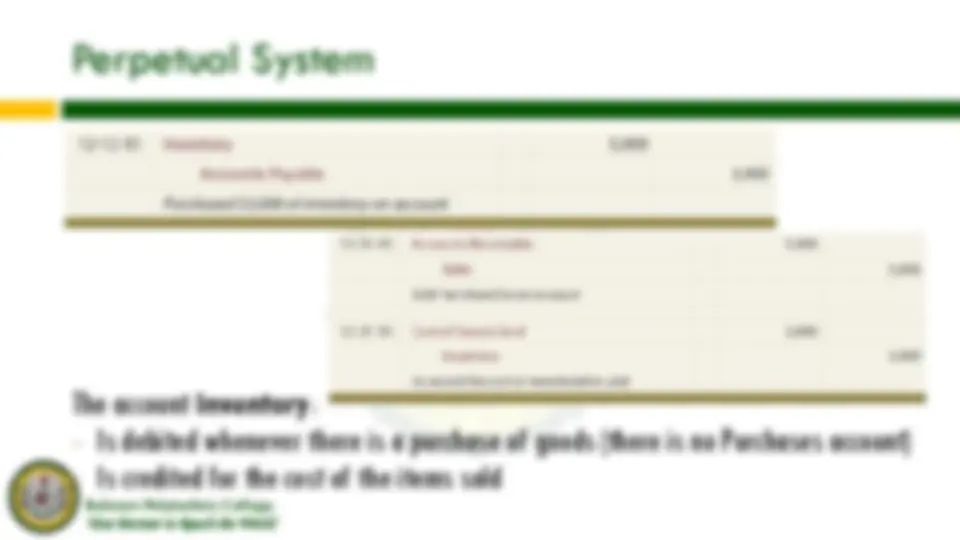

The account Inventory : − Has a continuously or perpetually changing balance because of the above entries − Requires a physical inventory to correct any errors in the Inventory account − Requires a cost flow assumption (FIFO, LIFO, average) With the perpetual inventory system, the cost of goods sold is readily available in the account Cost of Goods Sold.

Bulacan Polytechnic College

4. Estimate ending inventory − If it is not possible to conduct a physical count to arrive at the ending inventory balance, the gross profit method or the retail inventory method

5. Assign costs to inventory − assigning costs to ending inventory unit counts. − involves tracking tranches of inventory costs, involves FIFO, LIFO, or Weighted Average

Bulacan Polytechnic College

4. Allocate inventory to overhead − typical production facility has a large amount of overhead costs, which must be allocated to the units produced in a reporting period

Last-In, First-Out (LIFO) Calculations The oldest costs remain in inventory while recent costs are assigned to goods sold Beginning Inventory Net Purchases (P4,400) Goods Available for Sale 110 units P7, 50 units @P70/unit P3, 20 units @P71/unit P1, 10 units @P73/unit P 30 units @P75/unit P2, Assume that a physical count of inventory was conducted and confirmed that 20 units were actually on hand at the end of the accounting period. 20 units @P70/unit 110 units @P75/unit 30 units P2, 30 units @P70/unit P2, @P71/unit 20 units P1, 10 units P @73/unit Cost of Goods Available for Sale P7,900 (^) Cost of Goods Sold = P6, Ending Inventory P1, = =

Weighted Average Calculations Relies on the average unit cost Assume that a physical count of inventory was conducted and confirmed that 20 units were actually on hand at the end of the accounting period. Beginning Inventory (^) Net Purchases (P4,400) Goods Available for Sale 110 units P7, 50 units @P70/unit P3, 20 units @P71/unit P1, 10 units @P73/unit P 30 units @P75/unit P2, = Average Cost = 𝑪𝒐𝒔𝒕 𝒐𝒇 𝑮𝒐𝒐𝒅𝒔 𝑨𝒗𝒂𝒊𝒍𝒂𝒃𝒍𝒆 𝒇𝒐𝒓 𝑺𝒂𝒍𝒆 𝑻𝒐𝒕𝒂𝒍 𝑼𝒏𝒊𝒕𝒔 𝒇𝒐𝒓 𝑺𝒂𝒍𝒆 Average Cost = P7,900/ = P71. Cost of Goods Sold 90 x P71. = P6,463. Ending Inventory 20 x P71. = P1,436. Cost of Goods Available for Sale P7, =