Adaptive Algorithms for Tracking Volatility

Dinesh Krithivasan

EECS 659: Adaptive Signal Processing

D.Krithivasan (EECS 659) Algorithms for Tracking Volatility 1 / 23

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

A mcmc-based sampling method for a stochastic volatility (sv) model, which is used to estimate the volatility of financial assets. The sv model is studied in the context of the discrete sv model, which is a specific type of sv model. The document also discusses the use of gibbs sampling, a special case of monte carlo markov chain sampling, to sample from the posterior distribution of the model. The method is then applied to a filtering application and the results are presented.

Typology: Study notes

1 / 54

This page cannot be seen from the preview

Don't miss anything!

EECS 659: Adaptive Signal Processing

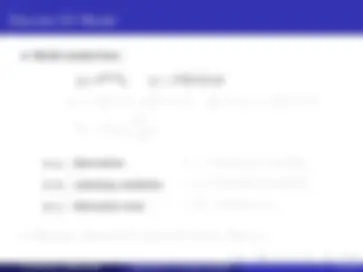

dSt St

σ

2

2

p

ht / 2

σ

2 η

yt - observations

ht - underlying volatilities

² t - observation noise

μ - Instantaneous volatility

φ - Persistence of volatility

σ

2 η - volatility of^ ht

2

ht / 2

σ

2 η

yt - observations

ht - underlying volatilities

² t - observation noise

μ - Instantaneous volatility

φ - Persistence of volatility

σ

2 η - volatility of^ ht

2

ht / 2

σ

2 η

yt - observations

ht - underlying volatilities

² t - observation noise

μ - Instantaneous volatility

φ - Persistence of volatility

σ

2 η - volatility of^ ht

2

ht / 2

σ

2 η

Marginalizing the joint density is hard.

Easy to sample from pX |Y and pY |X.

Pick y 0 from some distribution that has same support as pY (y ).

Pick x 0 from the distribution pX |Y (x | y 0 ).

For i = 1 ,... , N, pick yi from PY |X (y | xi− 1 ) and xi from PX |Y (x | yi ).

Marginalizing the joint density is hard.

Easy to sample from pX |Y and pY |X.

Pick y 0 from some distribution that has same support as pY (y ).

Pick x 0 from the distribution pX |Y (x | y 0 ).

For i = 1 ,... , N, pick yi from PY |X (y | xi− 1 ) and xi from PX |Y (x | yi ).

Marginalizing the joint density is hard.

Easy to sample from pX |Y and pY |X.

Pick y 0 from some distribution that has same support as pY (y ).

Pick x 0 from the distribution pX |Y (x | y 0 ).

For i = 1 ,... , N, pick yi from PY |X (y | xi− 1 ) and xi from PX |Y (x | yi ).