Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

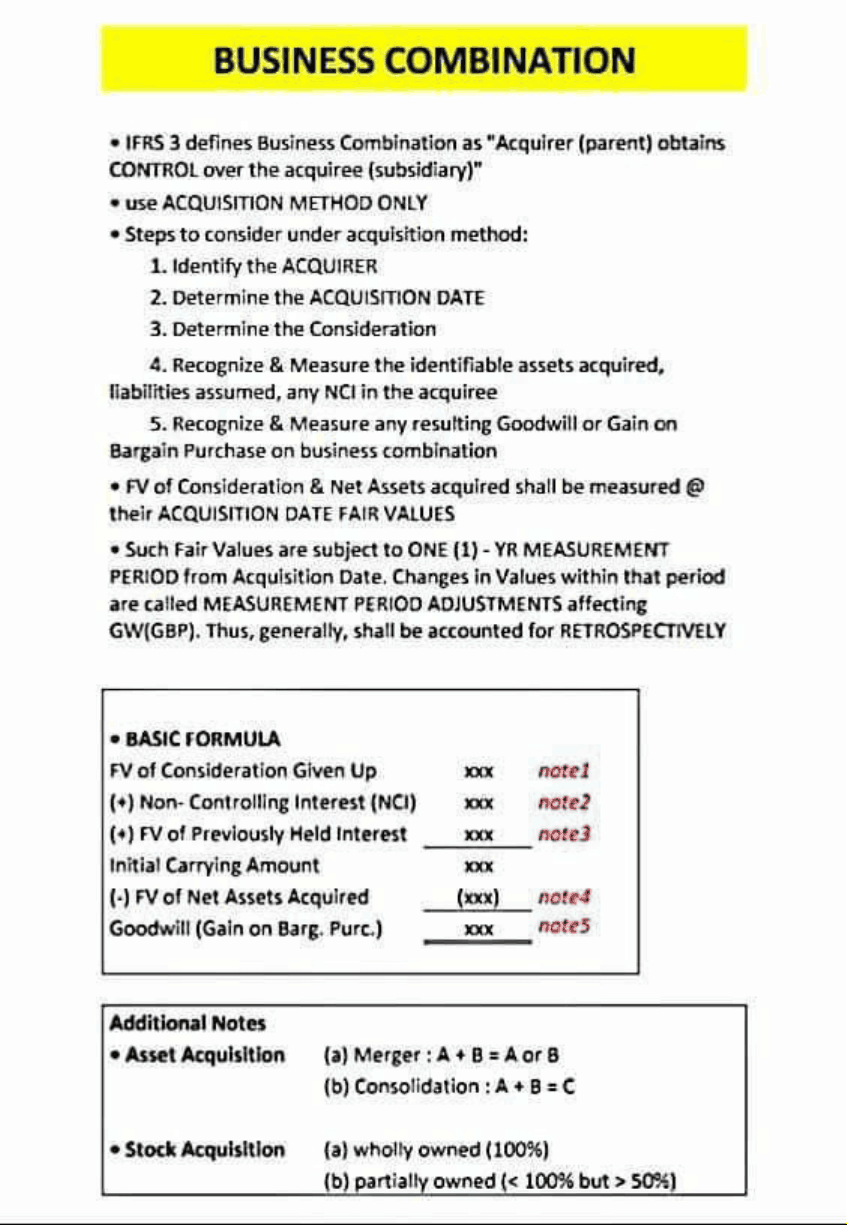

Advanced Financial Accounting & Reporting (AFAR) likely encompass advanced accounting topics. These may include consolidation of financial statements, international financial reporting standards (IFRS), complex financial instruments, accounting for mergers and acquisitions, fair value accounting, and financial statement analysis. Additionally, the notes may delve into regulatory requirements and ethical considerations in financial reporting.

Typology: Study notes

1 / 34

This page cannot be seen from the preview

Don't miss anything!