Download Adverse Selection - Banking - Lecture Slides and more Slides Banking and Finance in PDF only on Docsity!

Adverse Selection

What is Adverse Selection?

o Adverse selection is the problem created by asymmetric

information before the transaction occurs.

o It occurs when the potential borrowers who are the most

likely to produce an undesirable (adverse) outcome – the

bad credit risks – are the ones who most actively seek

out a loan and are thus most likely to be selected.

If used cars were securities…

- Investors often do not have sufficient information to determine which

firms have high or low risk.

- Investors will only be willing to pay a price for average quality firms’

securities.

- Good firms know their securities are under valued and will not sell

them.

- Bad firms know their securities are over priced and would love to sell.

- The only firms willing to sell will be the bad firms.

- Investors will not invest in firms.

- This scenario also goes for debt (bonds).

What this means?

- Marketable securities are not the primary source of financing for

businesses in any country in the world.

- Stocks are not the most important source of financing for American

businesses.

Tools to Help Solve Adverse Selection Problems

- Private Production and Sales of Information

- Government Regulation to Increase Information

- Financial Intermediation

- Collateral and Net Worth

Government Regulation to

Increase Information

- Because it is not efficient for private firms to produce information, the

government can.

- SEC – Securities and Exchange Commission – requires firms selling their

securities to have independent audits in which accounting firms certify that the

firm is adhering to standard accounting principles and disclosing accurate

information about sales, assets, and earnings.

- Problems : the government also would have to release negative information

about certain firms, which can cause political backlash.

- Bad firms may slant their information to make them look like good firms.

- There is a lot more to knowing the quality of a firm than statistics can provide.

Financial Intermediation

- Just as used car dealers help solve adverse selection problems in the

car market, financial intermediaries play a similar role in financial markets

- Financial Intermediaries, like banks, become experts in producing

information about firms, so it can sort out good credit risks from bad ones.

- Because the bank lends mostly to good firms, it is able to earn a higher

return on its loans than the interest it has to pay to its depositors. The

resulting profit that the bank earns gives it the incentive to engage in this

information production activity.

- Financial Intermediaries, because they hold a large portion of nontraded

loans, play a greater role in moving funds to corporations than security

markets do.

- Indirect finances are more important than direct finance.

Collateral and Net Worth

Collateral – property promised to

the lender if the borrower defaults

Net Worth (a.k.a. equity capital) –

the difference between a firm’s

assets and it’s liabilities

- Both Collateral and Net Worth offset the losses of the lender in the event of a default.

- Collateral leaves the lender compensation which can be sold to make up for the losses

on the loan.

- If a firm has a high net worth, then even if it engages in investments that cause it to

defaults on its debt payments, the lender can take title to the firm’s net worth, sell it off,

and use the proceeds to recoup some of the losses from the loan.

- Creditors have compensatory priority over shareholders in the event that a company

defaults.

Adverse Selection In Credit Card Market

- In order to gain empirical evidence of adverse selection, data was taken on results of large-scale randomized trials in preapproved credit card solicitations. This is meaningful, as over 5 billion solicitations were sent out in 2001, a substantial portion of credit card marketing.

- From this test, four basic conclusions can be drawn:

Adverse selection can be clearly seen from the start: respondents to mailed solicitations are those with characteristics of substantially worse credit risks than the average citizen.

Offers with inferior terms, such as higher introductory interest rates, yielded smaller customer pools. Those who remained were always those with worse credit-risk characteristics.

Predictably, customers who accept inferior offers also more likely to default.

Finally, those who accepted the solicitation prioritized cards with low introductory rates with less regard to long-term rates, showing a tendency towards overly optimistic views about future borrowing.

Stock Market Speculation

- Asymmetric information and adverse selection play a large

role in the survival of public firms, their funding, and their

current market value.

- Small firms ( Micro & Nano Cap firms < $300M value) heavily

rely on funding through the issuance of debt and equity

offerings.

- These firms are often considered “going concerns” as

investors and creditors have a difficult time valuing the firms

and are unsure of the exact credit risk/likelihood of survival

associated with each firm.

- This uncertainty creates significant volatility and doubt.

Ticker Symbol AEN: 110% Increase In 2 Weeks

Market Speculation Cont…

- High risks are associated with these firms because of an above

average default risk.

- Along with increased risk comes investors seeking high returns.

- These investors in-turn create a market for low-quality, unsecured

debt and debt instruments/insurance policies.

- One such debt/insurance instrument is called a Credit Default Swap

(CDS).

- A CDS is a contract where the buyer makes periodic payments to

the seller in exchange for the right to a payoff if there is a default or

material change in a firm’s credit standing.

- Eg: Buyer pays $100/mth in exchange for a $10,000 payment if a

company receives a downgrade from a Credit-rating agency or

defaults on bonds or loans.

Market Speculation Cont…

- The speculative aspect of the whole situation is when neither

party involved in trading the credit insurance actually owns

the assets/liabilities in question.

- Imagine: one person being able to insure your house, but

through someone else entirely not connected to your house;

so that if your house is destroyed, that person get paid your

house’s value.

- It’s making a bet on an outcome or event, which in the

financial industry causes extreme instability when a certain

series of events is triggered.

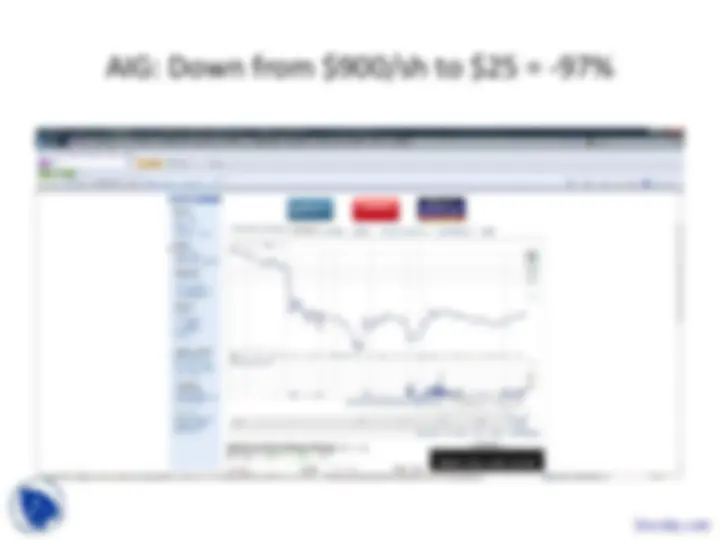

Real-Life Examples: #1-AIG

- As of June 2009, AIG had written $440 billion worth of swaps on corporate bonds and mortgage-backed securities. As the value of these insured- referenced entities fell, AIG had massive write-downs and additionally had to post more collateral. And when its ratings were downgraded that month, the company had to post even more collateral, which it didn’t have.

- These instruments are causing many of the massive write-downs at banks, investment banks and insurance companies. This means that the value of the hedge funds, the credit markets and the stock market had to adjust downward, rapidly and drastically.

- The financial structure of the U.S. was severely damaged by a domino- effect type forced liquidation by large firms and investors – all as a result of billions of dollars being invested without sufficient information.

AIG: Down from $900/sh to $25 = -97%