APPEALABLE

ORDERS

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

passed by the assessing officer under above relevant laws can prefer appeal within prescribed time period of 30 days before this appellate authority for redressal of grievance or otherwise. Commissioner Inland Revenue (Appeals) is a quasi-judicial authority and is meant for extending justice at first appellate stage by consulting all facts and merits of the case after hearing the appellant and the Revenue.

Typology: Slides

1 / 10

This page cannot be seen from the preview

Don't miss anything!

Whenever a dispute or difference of opinion is brought before the appellate authorities for decision, it is known as appeal. But the appeal can be made only against appealable orders.

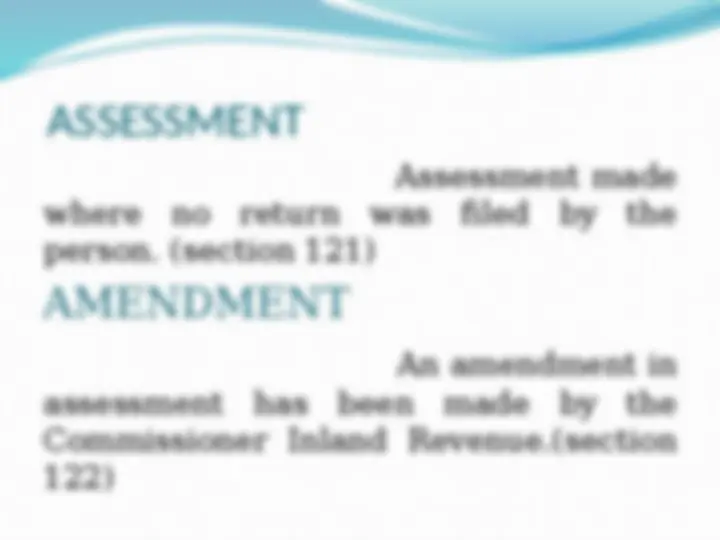

Assessment made where no return was filed by the person. (section 121)

An amendment in assessment has been made by the Commissioner Inland Revenue.(section

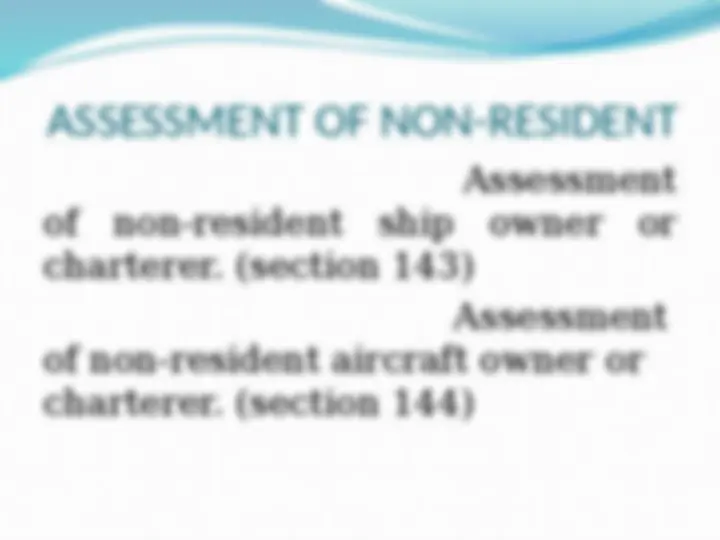

Assessment of non-resident ship owner or charterer. (section 143) Assessment of non-resident aircraft owner or charterer. (section 144)

Penalty imposed due to failure in furnishing a return or statement. (section 182)

Holding a person personally liable to pay an amount of tax collected or deducted but not deposited with the government. (section

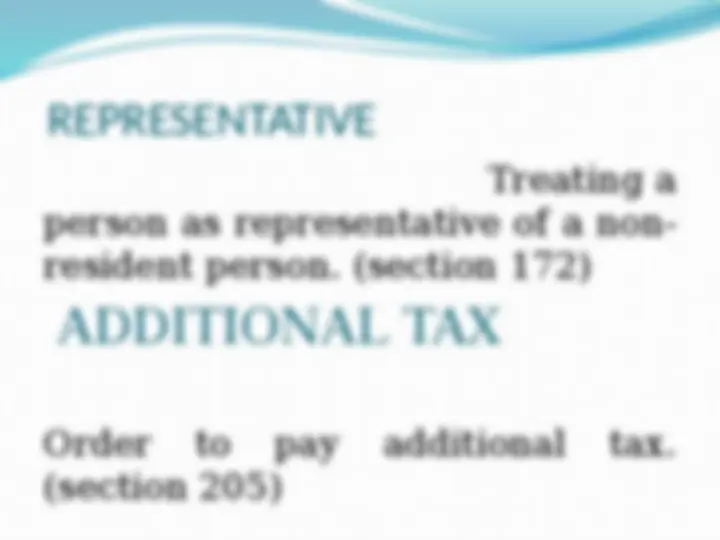

Treating a person as representative of a non- resident person. (section 172)

Order to pay additional tax. (section 205)