Download 2021 Small Biz Credit Survey: Firm Performance, Financing Needs, Satisfaction and more Exams Mechanical Systems Design in PDF only on Docsity!

Atlanta • Boston • Chicago • Cleveland • Dallas • Kansas City • Minneapolis

New York • Philadelphia • Richmond • St. Louis • San Francisco

F E D E R A L R E S E R V E B A N K S o f

SMALL

BUSINESS

CREDIT

SURVEY

2021 REPORT ON

EMPLOYER FIRMS

TABLE OF CONTENTS

I ACKNOWLEDGMENTS

II EXECUTIVE SUMMARY

1 PERFORMANCE & CHALLENGES

1 Revenue and Employment Change,

Prior 12 Months

2 Financial Condition

3 Effects of the Pandemic on Operations

4 Effects of the Pandemic on Sales

and Supply Chain

5 Financial Challenges, Prior 12 Months

6 Coping with Financial Challenges

and Use of Personal Funds

7 EMERGENCY FUNDING

7 Pandemic-Related Emergency

Funding Needs

8 PPP Application Outcomes and

Expected Loan Forgiveness

9 PPP Applications and Outcomes

10 PPP Funding and Employment Actions

11 LOOKING AHEAD

11 Performance Expectations, Next 12 Months

12 Expected Challenges Resulting From

Pandemic, Next 12 Months

14 Survival Expectations

15 Plans to Apply for More Emergency

Assistance in the Future

16 DEBT & FINANCING

16 Debt Outstanding

17 Financial Services Providers

18 Demand for Financing, Prior 12 Months

20 Nonapplicants

21 Financing Needs and Outcomes

22 Financing Received

24 FINANCING APPLICATIONS

24 Products Sought

25 Loan/Line of Credit/Cash Advance Sources

26 Loan/Line of Credit/Cash Advance Approval

28 Lender Satisfaction

29 DEMOGRAPHICS

33 METHODOLOGY

SMALL B USINESS CREDIT SURVEY | 2021 REPORT ON EMPLOYER FIRMS ii

5 The Small Business Credit Survey collects information from both employer and nonemployer firms. The 2020 survey yielded 4,531 responses from nonemployers; the findings for nonemployers will be explored in a separate report. Additionally, the survey yielded approximately 1,000 responses from permanently closed firms and new businesses that had not yet begun operations. 6 Johns Hopkins Coronavirus Resource Center, https://coronavirus.jhu.edu/data/new-cases. 7 In this summary, the years specified in year-over-year comparisons refer to the year in which the survey was fielded. Some survey questions pertain to the prior 12 months, which include the final months of the preceding year.

The Small Business Credit Survey (SBCS),

a collaboration of all 12 Federal Reserve

Banks, provides timely information about

small business conditions to policymakers,

service providers, and lenders. In 2020, the

survey reached more than 15,000 small

businesses,^5 gathering insights about the

COVID-19 pandemic’s impact on small

businesses, as well as business performance

and credit conditions.

The survey was fielded in September and

October 2020, approximately six months

after the onset of the pandemic. The timing

of the survey is important to the interpreta-

tion of the results. At the time of the survey,

the Paycheck Protection Program (PPP)

authorized by the CARES Act had recently

closed, and prospects for additional stimulus

funding were uncertain. Additionally, many

government-mandated business closures

had been lifted as the number of new

COVID-19 cases plateaued in advance of

a significant increase in cases by the

year’s end.^6

The 2020 survey findings highlight the

magnitude of the pandemic’s impact on

small businesses and the challenges they

anticipate as they navigate changes in the

business environment. The 2020 SBCS finds

that few firms avoided the negative impacts

of the pandemic. Furthermore, the findings

reveal disparities in experiences and out-

comes across firm and owner demographics,

including race and ethnicity, industry, and

firm size. While this report aggregates data

on all small employer firms, it includes some

details for select demographics. Future

publications will explore the impact of the

pandemic on different subsets of businesses.

SURVEY FINDINGS

The 2020 SBCS yielded 9,693 responses

from a nationwide convenience sample

of small employer firms with 1–499 full-

or part-time employees (hereafter “firms”)

across all 50 states and the District of

Columbia. This publication summarizes

data for firms that were currently operating

or temporarily closed at the time of

survey and does not include permanently

closed businesses.

Firms’ financial conditions declined sharply

between 2019 and 2020.^7 Firms owned by

people of color reported greater challenges.

Most firms reported declines in revenues

and employment in the 12 months prior

to the survey. Seventy-eight percent

of firms reported decreases in revenues,

and 46% reduced their workforce.

Fifty-seven percent of firms characterized

their financial condition as “fair” or “poor.”

This figure jumps to 79% for Asian-owned

firms and 77% for Black-owned firms.

The share of firms that experienced

financial challenges in the prior 12 months

rose from 66% to 80% between 2019 and

2020. In response to those challenges,

firms most commonly used personal funds

(62%) or cut staff hours/downsized

operations (55%).

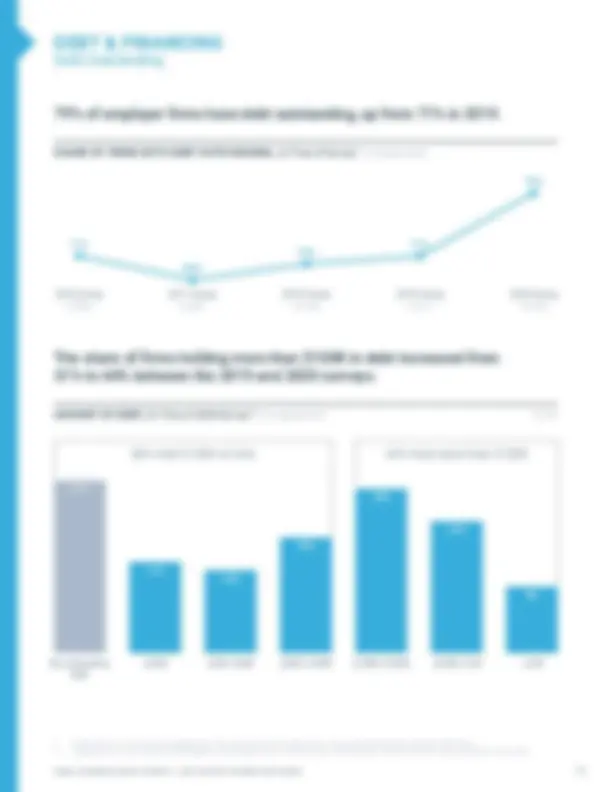

Seventy-nine percent of firms had debt

outstanding, an increase from 71% in

2019. The amount of debt firms hold also

increased; the share of firms with more

than $100,000 in debt rose from 31% in

2019 to 44% in 2020.

The COVID-19 pandemic has had

wide-reaching effects on small

business operations.

The vast majority of firms (95%)

reported that the pandemic impacted their

business. For example, 26% closed

temporarily, 56% reduced their operations,

and 48% modified their operations.

Of those that faced disruptions to

operations, firms most commonly cited

changes in demand (58%), government

mandates (55%), or the need to adapt

to health and safety guidelines (52%) as

reasons their businesses were affected.

Fifty-three percent of firms expected total

sales revenues for 2020 to be down by

more than 25% because of the pandemic.

More than 90% of firms sought emergency

funding to weather the financial impacts

of the pandemic.

Ninety-one percent of firms applied for

some type of emergency funding during

the pandemic. The PPP was the most

commonly used program; 82% of

employer firms applied. Seventy-seven

percent of PPP applicants received

all of the funding they sought.

Firms that sought PPP funds most

frequently submitted their applications

through small (48%) and large (43%)

banks. Of firms that applied through large

banks, 95% had an existing relationship

with their bank prior to applying for a PPP

loan. Eighty-three percent of small bank

applicants had an existing relationship.

EXECUTIVE SUMMARY

SMALL B USINESS CREDIT SURVEY | 2021 REPORT ON EMPLOYER FIRMS iii

Access to PPP funds bolstered firms’

ability to retain or rehire employees.

Forty-six percent of firms that received

all of the PPP funding they sought reduced

the number of employees on their payroll,

compared to 71% percent of firms that

received none of the PPP funding for

which they applied. In addition, PPP

recipients were more likely to rehire

employees they laid off.

Sixty-four percent of firms would apply

for additional government-provided

assistance if it were made available.

Of these firms, 39% expected they would

be unlikely to survive until sales return

to “normal” (that is, 2019 levels) without

further government assistance.

At the time of the survey, most firms

expected sales pressures and pandemic-

related challenges to persist.

Firms anticipate a challenging year

ahead. Firms were more likely to expect

a decrease in revenues in the next 12

months as opposed to an increase.

Furthermore, respondents were less

likely than in previous years to expect an

increase in employment. The net share

of firms expecting employment growth in

2020 was 14%, compared to 38% in 2019.

Eighty-eight percent of firms indicated

that sales had not yet returned to normal.

Of those firms, 30% projected it would

be unlikely that they could survive

until sales recover without additional

government assistance.

Thirty-seven percent of firms expect that

the most important challenge stemming

from the pandemic in the next 12 months

will be weak demand, followed by govern-

ment-mandated restrictions or closures

(26%) and credit availability (13%).

The most important anticipated challenge

differed by race and ethnicity of the owners.

For Black-owned firms, credit availability

was the top expected challenge, while

Asian-owned firms disproportionately

cited weak demand.

Applications for non-emergency financing

decreased from 2019 to 2020.

The share of firms that applied for

financing declined from 43% in 2019

to 37% in 2020.^8

Compared to 2019, firms were consider-

ably more likely to seek financing in order

to meet operating expenses (58% versus

43% in 2019) and less likely to seek funds

for expansion (38% versus 56% in 2019).

The share of applicant firms that received

all the financing they sought declined from

51% in 2019 to 37% in 2020.

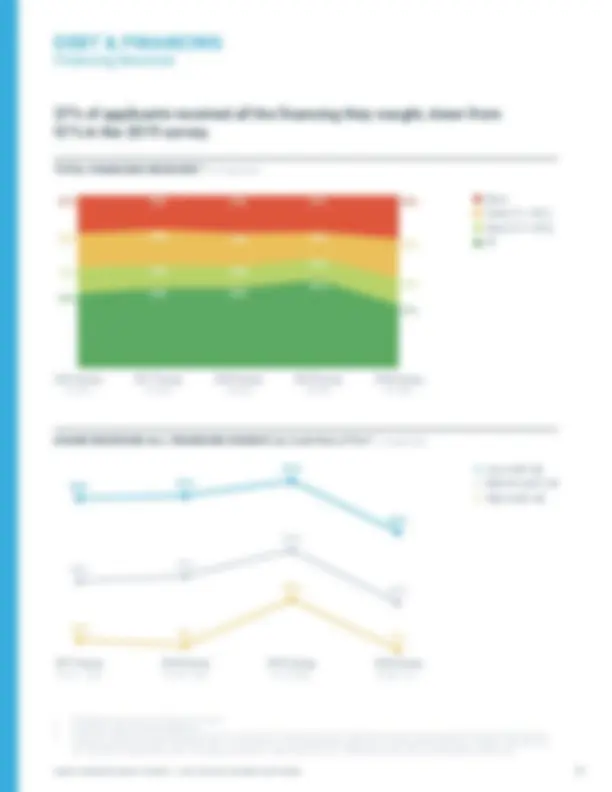

Approval rates on loans, lines of credit,

and cash advances declined in 2020.

The share of applicant firms that were

at least partially approved for loans, lines

of credit, and cash advances declined

from 83% in 2019 to 76% in 2020.

Following the start of the pandemic, firms

were less successful at obtaining loans,

lines of credits, and cash advances. Prior

to March 1, 2020, 81% of applicants were

approved for at least some of the funds

they sought. After March 1, only 70% were

at least partially approved.

Banks remain the most common source

of credit for small businesses; use of online

lenders declined.

Forty-two percent of firms that applied

for a loan, line of credit, or cash advance

sought this funding from a large bank,

similar to the share that applied at a large

bank in 2019 (40%). Forty-three percent

turned to a small bank, up from 36% in

2019. In contrast, the share of firms that

applied to an online lender fell from 33%

in 2019 to 20% in 2020.

Firms with lower credit scores turned to

online lenders (35%) and nonbank finance

companies (23%) much more often than

did their counterparts with higher credit

scores (11% and 11%, respectively).

Among applicant firms that were approved

for at least some financing, net satisfac-

tion was highest for credit unions (81%),

followed by small banks (74%) and large

banks (60%). Online lender applicants

were least satisfied, as net satisfaction

with online lenders declined from 37% in

2019 to 25% in 2020.

ABOUT THE SURVEY

The SBCS is an annual survey of firms with

fewer than 500 employees. These types of

firms represent 99.7% of all employer estab-

lishments in the United States.^9 Respondents

are asked to report information about their

business performance, financing needs

and choices, and borrowing experiences.

Responses to the SBCS provide insights on

the dynamics behind lending trends and

shed light on various segments of the small

business population. The SBCS is not a

random sample; results should be analyzed

with awareness of potential biases that are

associated with convenience samples. For

detailed information about the survey design

and weighting methodology, please consult

the Methodology section.

8 The share of firms that applied for financing in 2020 excludes firms that applied only for emergency funding, such as PPP. 9 US Census Bureau, 2018 County Business Patterns. EXECUTIVE SUMMARY (Continued)

PERFORMANCE & CHALLENGES Financial Condition 1 Percentages may not sum to 100 due to rounding. 2 The characteristics shown in darker bars are related to self-reported financial condition at a significance level of 0.05 using a logistic regression. For the demographics shown, the reference groups are Non-Hispanic White-owned firms, firms with 1-4 employees, and firms in the non-manufacturing goods production and associated services industry (54%, not shown). 3 Additional variables were tested for statistical significance, including credit risk, gender of owner(s), revenues, and age of firm. Along with the variables shown in the figure, the gender of the owner(s), self-reported credit risk of the firm, and the firm’s age are also related to financial condition at a significance level of 0.05. 4 Select industries shown. 57% of firms reported that their financial condition was fair or poor.

FINANCIAL CONDITION, At Time of Survey^1 (% of employer firms)

All employer

firms N=9,

Firms owned by people of color, smaller firms, and leisure and hospitality firms were in weaker financial condition.

SHARE OF FIRMS IN FAIR OR POOR FINANCIAL CONDITION, At Time of Survey 2,3^ (% of employer firms)

By number of employees

1–4 N=4, 415

5–49 N=4, 815

50–499 N= 434

By industry^4

Leisure and hospitality N=1,

Healthcare and

education N=1,

Retail N=1,

Manufacturing N=1,

Non-Hispanic Asian N= 663

Non-Hispanic Black

or African American N=1,

Hispanic N=

Non-Hispanic White N=6,

By race/ethnicity of owner(s)

Very good

Good

Fair

Poor

Excellent

PERFORMANCE & CHALLENGES Effects of the Pandemic on Operations 95% of employer firms reported that the pandemic affected their operations.

EFFECTS OF THE PANDEMIC ON BUSINESS OPERATIONS^1 (% of employer firms) N=9,

Reduced operations

Temporarily closed

Modified operations

Expanded operations

No significant impact

1 Respondents could select multiple options. For example, a firm may have temporarily closed, and then reopened with reduced operations. “Temporarily closed” includes firms that remained closed at the time of survey and firms that had closed for a time but have since reopened. 2 Respondents could select multiple options. 3 Response option “other” not shown in chart. See Appendix for more detail.

DRIVERS OF OPERATIONAL CHANGES DURING THE PANDEMIC 2,3^ N=8,

(% of employer firms that temporarily closed or reduced/modified operations)

Change in demand for

products/services

Government mandate

affecting my business

Needed to adapt to

health/safety guidelines

Government mandate

affecting clients’ businesses

Worker availability

Supply chain disruptions

Owner(s)’ personal/

family obligations

80% of employer firms experienced financial challenges in the prior 12 months, an increase of 14 percentage points from the 2019 survey. 1 Approximately the second half of the prior year through the second half of the surveyed year. 2 Respondents could select multiple options. 3 Approximately the second half of 2019 through the second half of 2020.

SHARE OF FIRMS WITH FINANCIAL CHALLENGES, Prior 12 Months^1 (% of employer firms)

PERFORMANCE & CHALLENGES Financial Challenges, Prior 12 Months

TYPES OF FINANCIAL CHALLENGES, Prior 12 Months2,^3 (% of employer firms) N=9,

Paying operating expenses

Making payments on debt

Paying rent

Purchasing inventory or

supplies to fulfill contracts

Credit availability

Other financial challenge

No financial challenges 20%

2017 Survey

N=8,

2018 Survey

N=6,

2019 Survey

N=5,

2020 Survey

N=9,

1 Respondents could select multiple options. 2 Approximately the second half of 2019 through the second half of 2020. 3 Response option “other” not shown in chart. See Appendix for more detail. 4 Data on personal finances were drawn from questions in the optional end-of-survey module (completed by approximately 80% of respondents). This subset of respondents is re-weighted to be reflective of the overall small firm population. 62% of firms used personal funds to address their financial challenges.

ACTIONS TAKEN TO ADDRESS FINANCIAL CHALLENGES, Prior 12 Months1,2^ N=7,

(% of employer firms reporting financial challenges)

80% of firms reported that pandemic-related business challenges impacted the owners’ personal finances.

EFFECTS OF THE FIRMS’ FINANCIAL CHALLENGES ON THE N=6,

PRIMARY OWNERS’ PERSONAL FINANCES 1,3,4^ (% of employer firms)

Did not draw a salary or reduced salary

Concerns about personal credit score or loss

of personal assets due to late payments

Paid business expenses with personal funds

Borrowed funds from spouse/

other family or friends

Borrowed against home or retirement account

Worked a second job or extra hours outside

of this business

No challenges or impact on personal finances

No action

Other action

38%

Made a late

payment or

did not pay

50%

Took out

debt

52%

Obtained funds

through grants,

crowdfunding,

donations, etc.

55%

Cut staff, hours,

and/or downsized

operations

62%

Used personal

funds

PERFORMANCE & CHALLENGES Coping with Financial Challenges and Use of Personal Funds

1 The Paycheck Protection Program (PPP) is administered through the US Small Business Administration. 2 The shares of firms that sought and obtained PPP funding that are shown in this report are higher than estimates from other sources. Much of the variance is likely attributed to the exclusion of nonemployer firm responses from this report, as nonemployers are less likely to have sought and obtained PPP funding. SBCS findings for nonemployers will be released in a separate publication. 3 Note that as a share of all employer firms in the SBCS sample (PPP applicants and nonapplicants), 78% received at least some PPP funding. EMERGENCY FUNDING PPP Application Outcomes and Expected Loan Forgiveness 96% of employer firms that applied for PPP loans reported that they received at least some funding.

PPP FUNDING RECEIVED, AS A SHARE OF AMOUNT SOUGHT 1,2,3^ N=7,

(% of PPP applicants)

SHARE OF PPP RECIPIENTS THAT EXPECT LOAN FORGIVENESS^1 N=7,

(% of PPP applicants at least partially approved)

All

Most

Some

None

Full forgiveness

Partial forgiveness

Unsure

Do not expect forgiveness

1 Respondents could select multiple options; respondents may have submitted more than one application. 2 Respondents were provided a list of large banks (those with at least $10B in total deposits) operating in their state. 3 “Online lenders,” also called fintech lenders, are nonbanks that lend online. Examples include: Lending Club, OnDeck, CAN Capital, Paypal Working Capital, Kabbage, etc. 4 “Finance company” includes nonbank lenders such as mortgage companies, equipment dealers, insurance companies, auto finance companies, etc. 5 Community development financial institutions (CDFIs) are financial institutions that provide credit and financial services to underserved markets and populations. CDFIs are certified by the CDFI Fund at the US Department of the Treasury. EMERGENCY FUNDING PPP Applications and Outcomes Small banks were the most common source for PPP loans among employer firms, and the source from which applicants were most successful in obtaining all the PPP funding they sought.

PPP APPLICATIONS AND OUTCOMES, By Source

Share of PPP applicants

that applied for PPP funding

at source^1

N=7,

Share of PPP applicants that

had an existing relationship

with the lender at which they

applied, by source

Share of PPP applicants that

received all of the PPP funding

they sought, by source

Small bank 48% 83% 78%

Large bank^2 43% 95% 70%

Online lender^3 9%

Credit union 80% 63%

Finance company^4 28% 41%

CDFI^5 26% 44%

N=3,

N=3,

N=

N=

N=3,

N=3,

N=

N=

N=

N=

N=

N=

LOOKING AHEAD Performance Expectations, Next 12 Months More firms were expecting a revenue decrease than a revenue increase in the next 12 months. 1 The index is the share reporting expected growth minus the share reporting a reduction. Due to rounding, the 2020 employment index is not equal to the difference between the shares shown for firms expecting an increase and firms expecting a decrease. 2 Expected change in approximately the second half of the surveyed year through the second half of the following year. 3 Questions were asked separately, thus the number of observations may differ slightly between questions. 4 Next 12 months is approximately the second half of 2020 through the second half of 2021.

EMPLOYER FIRM PERFORMANCE EXPECTATIONS, 2020 Survey (% of employer firms)

REVENUE CHANGE, N=9,

Next 12 Months^4

CHANGE IN EMPLOYMENT, N=9,

Next 12 Months^4

Will

increase

Will not

change

Will

decrease

Will

increase 31%

Will not

change

Will

decrease

EMPLOYER FIRM EXPECTATIONS INDEX, Next 12 Months1,^2 (% of employer firms)

Revenue growth

expectations

Employment growth

expectations

2016 Survey

N^3 =9,765–9,

2017 Survey

N^3 =7,736–8,

2018 Survey

N^3 =6,450–6,

2019 Survey

N^3 =5,024–4,

2020 Survey

N^3 =9,412–9,

LOOKING AHEAD Expected Challenges Resulting From Pandemic, Next 12 Months 95% of firms expected to face one or more pandemic-related challenges in the next 12 months. 1 Respondents could select multiple options. 2 Next 12 months is approximately the second half of 2020 through the second half of 2021. 3 Respondents who identified more than one anticipated challenge were asked which challenge they expected would be most important. This chart includes these responses as well as responses for firms with only one anticipated challenge.

Weak demand for

products/services

Supply chain disruptions

Government-mandated

restrictions or closures

Credit availability

Labor shortages

Owner(s)′ or employees′

personal/family obligations

Other

No significant challenges

CHALLENGES FIRMS EXPECT TO FACE AS A RESULT OF THE PANDEMIC, Next 12 Months1,2^ N=9,

(% of employer firms)

Of those anticipating pandemic-related challenges, 37% of firms identified weak demand as the most important challenge they expect to face.

SINGLE MOST IMPORTANT CHALLENGE FIRMS EXPECT TO FACE, Next 12 Months2,3^ N=9,

(% of employer firms expecting one or more pandemic-related challenges)

37% Weak demand for products/services 26% Government-mandated restrictions or closures 13% Credit availability 1 2 3

LOOKING AHEAD Survival Expectations 30% of the firms that reported sales were below normal at the time of the survey expect it is unlikely the business will survive without government assistance until sales recover. 1 Percentages may not sum to 100 due to rounding. 2 Data on sales recovery and firm survival expectations were drawn from questions in the optional end-of-survey module (completed by approximately 80% of respondents). This subset of respondents is re-weighted to be reflective of the overall small firm population. 3 At time of survey, September through October 2020.

EXPECTED TIMING OF SALES’ RETURN TO “NORMAL” (I.E., 2019 LEVELS) 1,2,3^ (% of employer firms) N=7,

LIKELIHOOD FIRMS WILL SURVIVE WITHOUT ADDITIONAL GOVERNMENT N=6,

ASSISTANCE UNTIL SALES RETURN TO NORMAL 1,2^ (% of employer firms for which sales had not yet returned to normal)

Sales are currently

at or above normal

By end of 2020 First half of 2021 Second half of 2021 2022 or later

Very

likely

Somewhat

likely

Neither likely

nor unlikely

Somewhat

unlikely

Very

unlikely

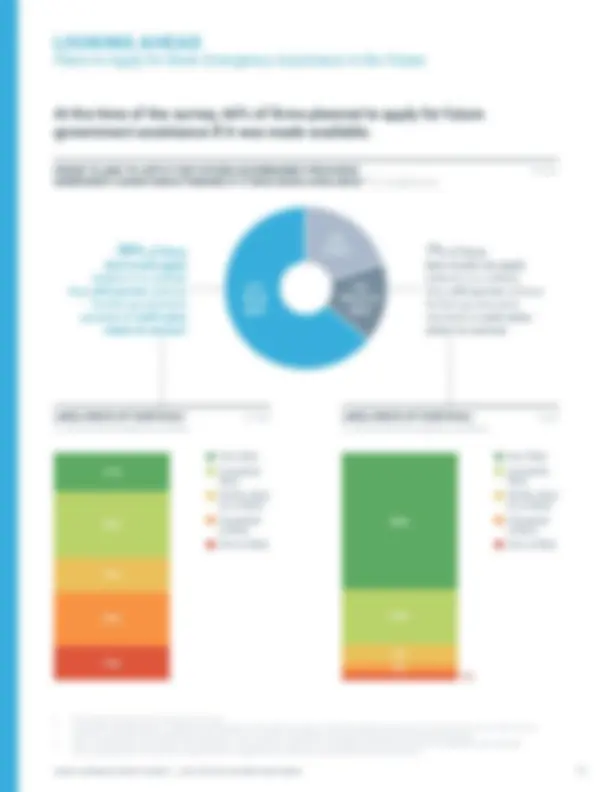

LOOKING AHEAD Plans to Apply for More Emergency Assistance in the Future At the time of the survey, 64% of firms planned to apply for future government assistance if it was made available.

FIRMS’ PLANS TO APPLY FOR FUTURE GOVERNMENT-PROVIDED N=9,

EMERGENCY ASSISTANCE FUNDING IF IT WAS MADE AVAILABLE 1,2^ (% of employer firms)

1 Percentages may not sum to 100 due to rounding. 2 The survey was administered in September and October of 2020, after the close of 2020 PPP funding and prior to the announcement of new PPP funding. Therefore, respondents were asked about their firms’ intent to apply for hypothetical, undefined future government-provided funding. 3 Data on sales recovery and firm survival expectations were drawn from questions in the optional end-of-survey module (completed by approximately 80% of respondents). This subset of respondents is re-weighted to be reflective of the overall small firm population.

Would

apply

Unsure

Would not

apply

7% of firms that would not apply believe it is unlikely they will survive without further government assistance until sales return to normal. 39% of firms that would apply believe it is unlikely they will survive without further government assistance until sales return to normal.

LIKELIHOOD OF SURVIVAL^3 N=4,

(% of firms that would apply for assistance)

LIKELIHOOD OF SURVIVAL^3 N=

(% of firms that would not apply for assistance)

Very likely

Somewhat

likely

Neither likely

nor unlikely

Somewhat

unlikely

Very unlikely

Very likely

Somewhat

likely

Neither likely

nor unlikely

Somewhat

unlikely

Very unlikely