GENERALCONFERENCEAUDITINGSERVICE

SANDIEGO,CALIFORNIA

JUNE20,2011

Assessing Audit Risk

Ann Gibson, PhD, CPA

Andrews University

1

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

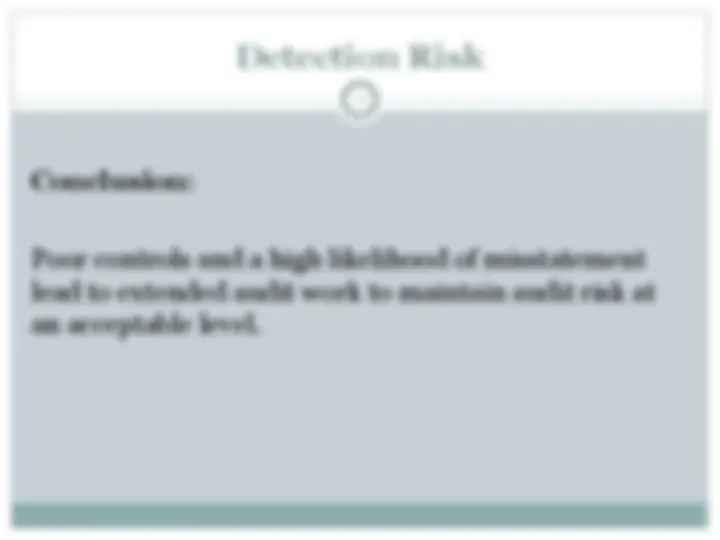

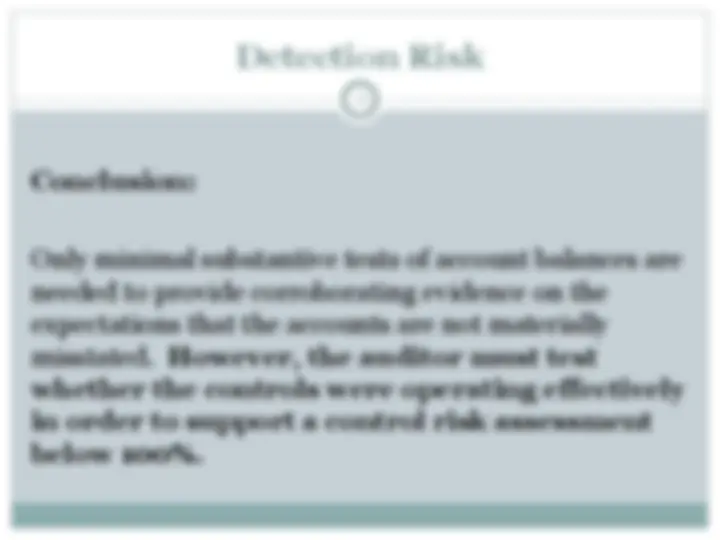

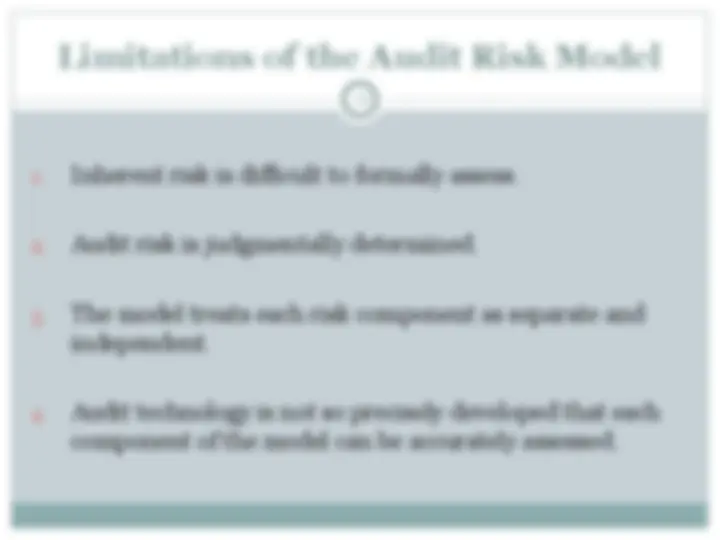

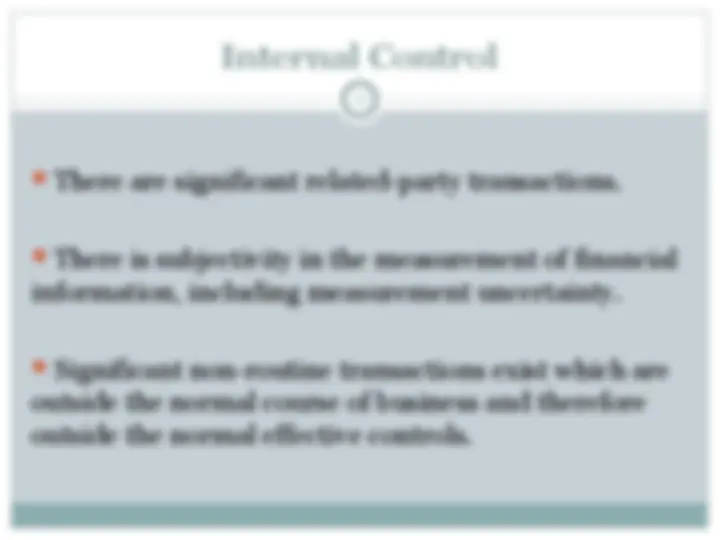

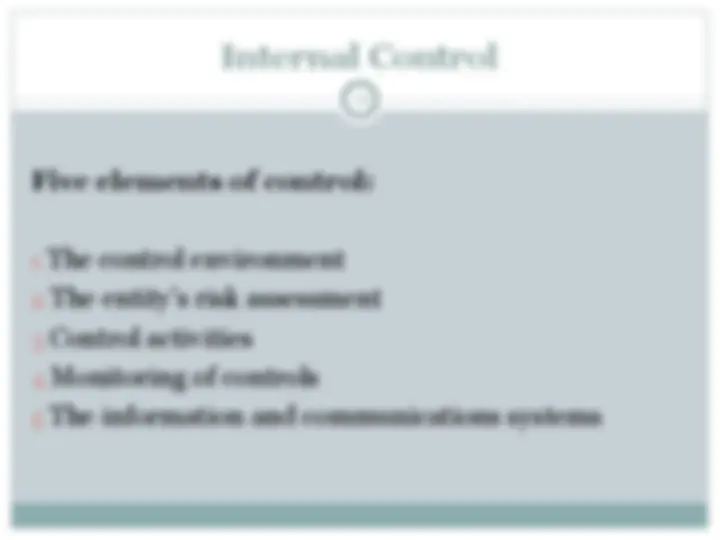

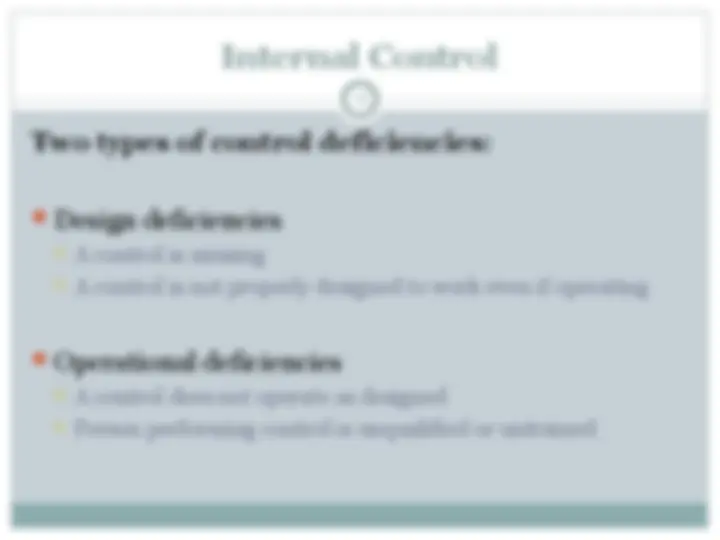

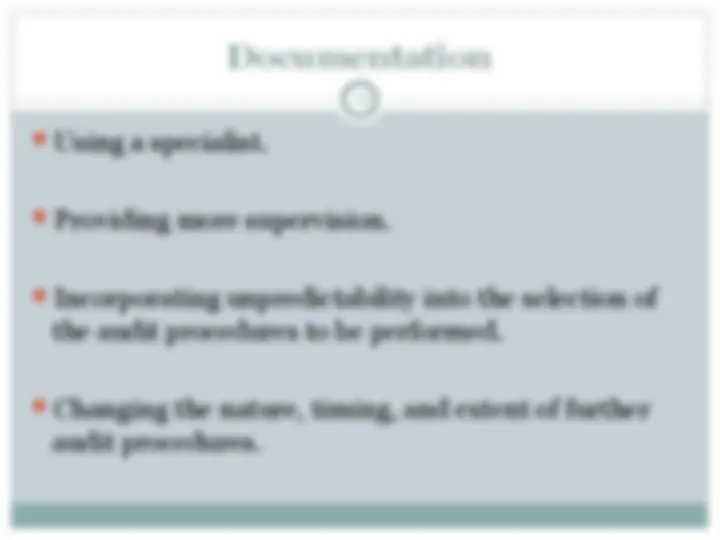

whether the controls were operating effectively in order to support a control risk assessment below 100%. 23. Page 24. Limitations of the Audit Risk Model. 1.

Typology: Lecture notes

1 / 46

This page cannot be seen from the preview

Don't miss anything!

GENERAL CONFERENCE AUDITING SERVICE SAN DIEGO, CALIFORNIA JUNE 20, 2011

Ann Gibson, PhD, CPA Andrews University 1

Risks associated with an audit: Business Risk Financial Reporting Risk Audit Risk 2

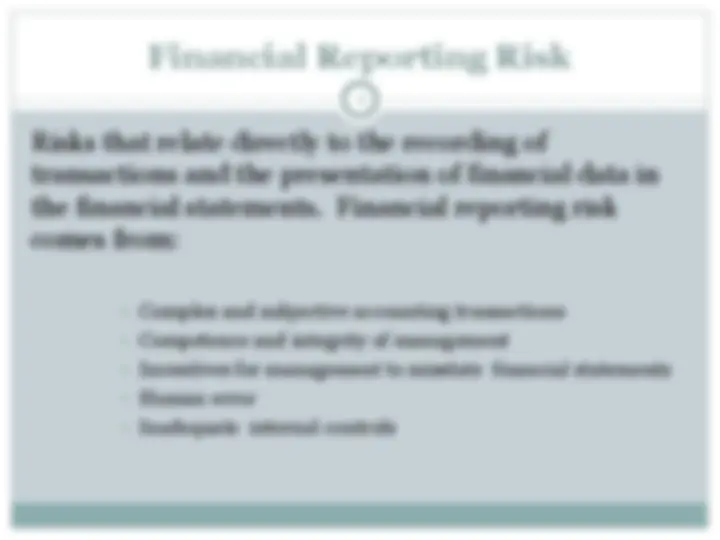

Financial Reporting Risk Risks that relate directly to the recording of transactions and the presentation of financial data in the financial statements. Financial reporting risk comes from:

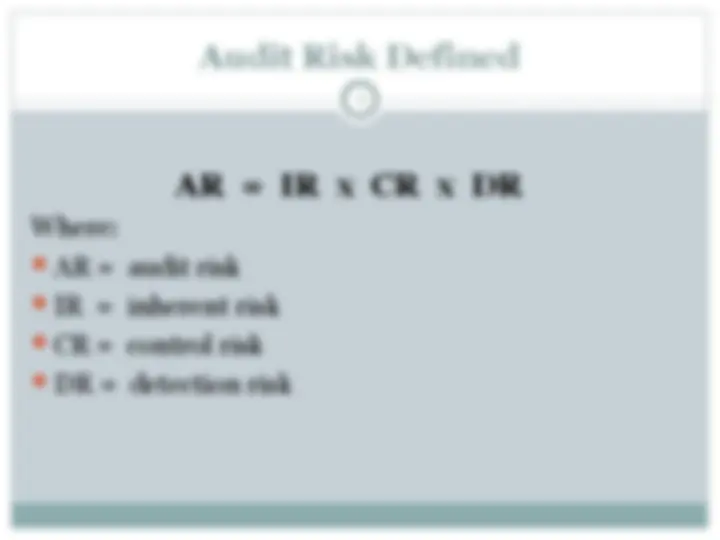

Audit Risk The risk that the auditor expresses an inappropriate audit opinion when the financial statements are materially misstated. 5

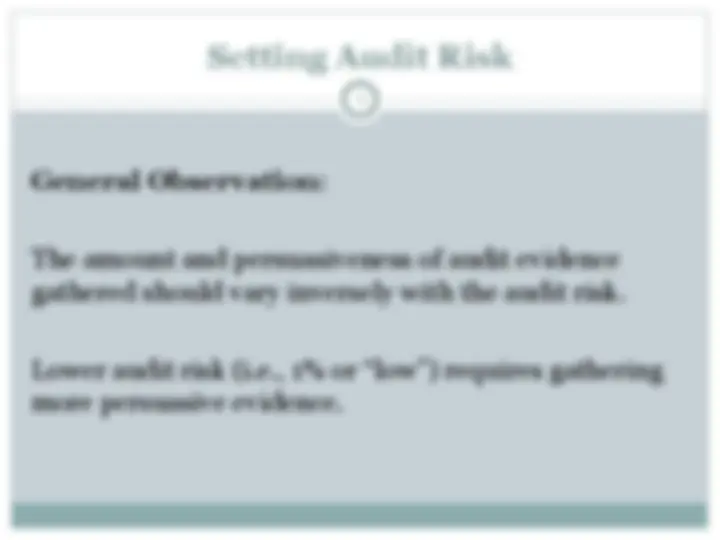

Setting Audit Risk May be set quantitatively: 1% or 5% May be set qualitatively: “high” “medium” “low” 7

Setting Audit Risk General Observation : The amount and persuasiveness of audit evidence gathered should vary inversely with the audit risk. Lower audit risk (i.e., 1% or “low”) requires gathering more persuasive evidence. 8

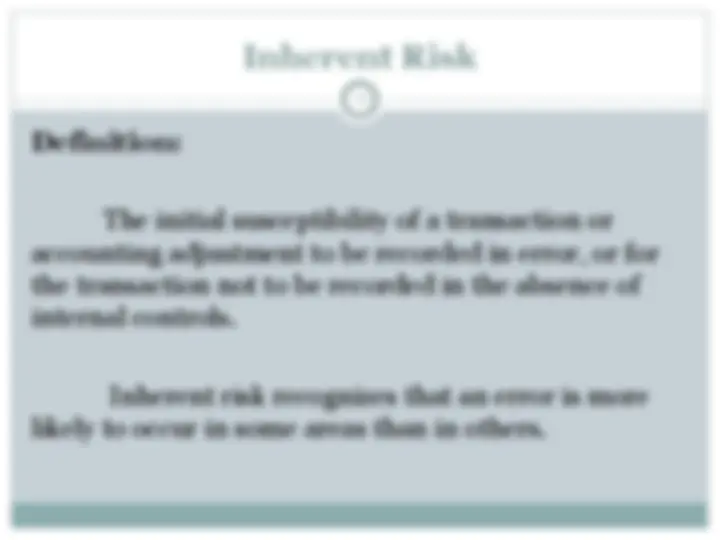

Inherent Risk Definition: The initial susceptibility of a transaction or accounting adjustment to be recorded in error, or for the transaction not to be recorded in the absence of internal controls. Inherent risk recognizes that an error is more likely to occur in some areas than in others. 10

11

Control Risk Definition: The risk that the client’s internal control system will fail to prevent or detect a misstatement. 13

Control Risk Auditor must evaluate the design of the control and determine whether it has been placed in operation. Is the control capable of effectively preventing a material misstatement? Of effectively detecting and correcting a material misstatement? Is the entity using the control? 14

Control Risk Second Standard of Fieldwork : The auditor must obtain a sufficient understanding of the entity and its environment, including its internal control , to assess the risk of material misstatement of the financial statements, whether due to error or fraud, and to design the nature, timing, and extent of further audit procedures. 16

Control Risk General Observation : The auditor should not rely too heavily on either the client’s internal controls nor on their audit procedures to detect errors or frauds in the financial statements. 17

Detection Risk The auditor can control/manage detection risk through: Careful audit planning. Effective audit procedures. Performing those procedures with due professional care. 19

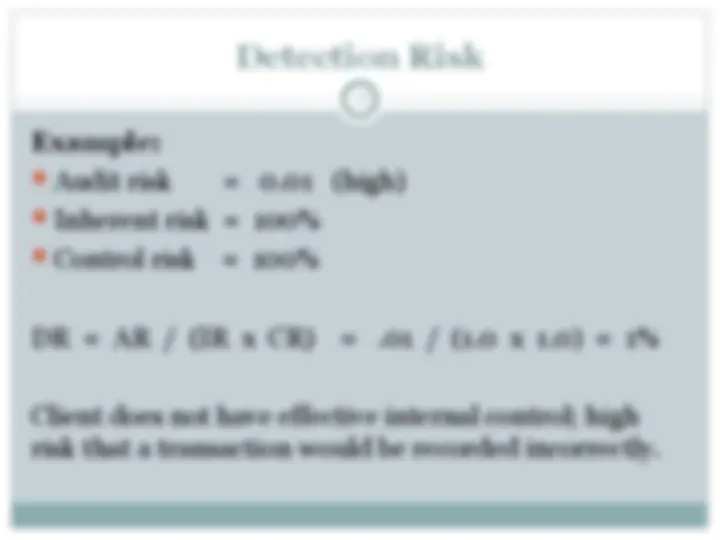

Detection Risk Example: Audit risk = 0.01 (high) Inherent risk = 100% Control risk = 100% DR = AR / (IR x CR) = .01 / (1.0 x 1.0) = 1% Client does not have effective internal control; high risk that a transaction would be recorded incorrectly. 20