Download Asymm info and more Lecture notes Microeconomics in PDF only on Docsity!

17.1 Quality, Uncertainty and the Market for Lemons 17.2 Market Signaling 17.3 Moral Hazard 17.4 The Principal–Agent Problem 17.5 Managerial Incentives in an Integrated Firm 17.6 Asymmetric Information in Labor Markets: Efficiency Wage Theory 17.7 Why Markets Fail

C H A P T E R 17

Prepared by: Fernando Quijano, Illustrator

Markets with

Asymmetric Information

CHAPTER OUTLINE

Quality Uncertainty and the Market

for Lemons

● asymmetric information Situation in which a buyer and a seller possess different information about a transaction. Used cars sell for much less than new cars because there is asymmetric information about their quality : The seller of a used car knows much more about the car than the prospective buyer does. As a result, the prospective buyer will always be suspicious of its quality—and with good reason. The implications of asymmetric information about product quality were first analyzed by George Akerlof and go far beyond the market for used cars. The markets for insurance, financial credit, and even employment are also characterized by asymmetric information about product quality.

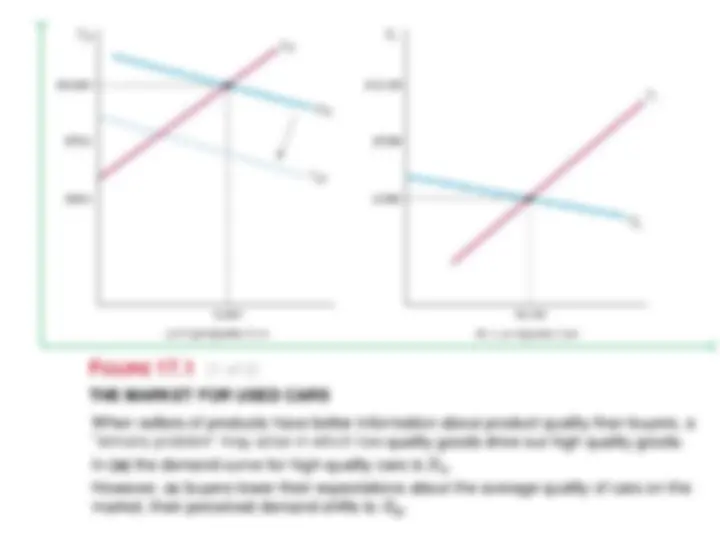

THE MARKET FOR USED CARS

FIGURE 17.1 (1 of 2)

When sellers of products have better information about product quality than buyers, a “lemons problem” may arise in which low-quality goods drive out high quality goods. In (a) the demand curve for high-quality cars is DH. However, as buyers lower their expectations about the average quality of cars on the market, their perceived demand shifts to DM.

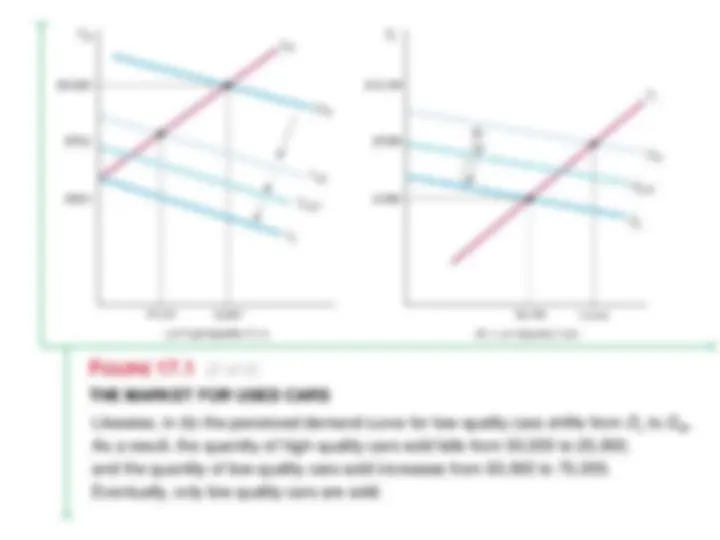

THE MARKET FOR USED CARS

FIGURE 17.1 (2 of 2)

Likewise, in (b) the perceived demand curve for low-quality cars shifts from DL to DM. As a result, the quantity of high-quality cars sold falls from 50,000 to 25,000, and the quantity of low-quality cars sold increases from 50,000 to 75,000. Eventually, only low quality cars are sold.

THE MARKET FOR INSURANCE

People who buy insurance know much more about their general health than any insurance company. As a result, adverse selection arises, much as it does in the market for used cars. Because unhealthy people are more likely to want insurance, the proportion of unhealthy people in the pool of insured people increases. This forces the price of insurance to rise, so that more healthy people, aware of their low risks, elect not to be insured. This further increases the proportion of unhealthy people among the insured, thus forcing the price of insurance up more. The process continues until most people who want to buy insurance are unhealthy. At that point, insurance becomes very expensive, or— in the extreme—insurance companies stop selling the insurance. One solution to the problem of adverse selection is to pool risks. For health insurance, the government might take on this role, as it does with the Medicare program. By providing insurance for all people over age 65, the government eliminates the problem of adverse selection. Likewise, insurance companies offer group health insurance policies at places of employment. By covering all workers in a firm, whether healthy or sick, the insurance company spreads risks and thereby reduces the likelihood that large numbers of high-risk individuals will purchase insurance.

THE MARKET FOR CREDIT

How can a credit card company or bank distinguish high-quality borrowers (who pay their debts) from low-quality borrowers (who don’t)? Clearly, borrowers have better information—i.e., they know more about whether they will pay than the lender does. Again, the lemons problem arises. Low-quality borrowers are more likely than high-quality borrowers to want credit, which forces the interest rate up, which increases the number of low-quality borrowers, which forces the interest rate up further, and so on. In fact, credit card companies and banks can , to some extent, use computerized credit histories, which they often share with one another, to distinguish low-quality from high-quality borrowers. Many people, however, think that computerized credit histories invade their privacy. Should companies be allowed to keep these credit histories and share them with other lenders? We can’t answer this question for you, but we can point out that credit Histories perform an important function: They eliminate, or at least greatly reduce, the problem of asymmetric information and adverse selection—a problem that might otherwise prevent credit markets from operating. Without these histories, even the creditworthy would find it extremely costly to borrow money.

17.2 Market Signaling

● market signaling Process by which sellers send signals to buyers conveying information about product quality. What characteristics can a firm examine to obtain information about people’s productivity before it hires them? Can potential employees convey information about their productivity? Dressing well for the job interview might convey some information, but even unproductive people can dress well. Dressing well is thus a weak signal —it doesn’t do much to distinguish high-productivity from low- productivity people. To be strong, a signal must be easier for high-productivity people to give than for low-productivity people to give, so that high-productivity people are more likely to give it. For example, education is a strong signal in labor markets. More productive people are more likely to attain high levels of education in order to signal their productivity to firms and thereby obtain better-paying jobs. Thus, firms are correct in considering education a signal of productivity.

A Simple Model of Job Market Signaling

Let’s assume that there are only low-productivity workers (Group I), whose average and marginal product is 1, and high-productivity workers (Group II), whose average and marginal product is 2. Workers will be employed by competitive firms whose products sell for $10,000, and who expect an average of 10 years’ work from each employee. We also assume that half the workers in the population are in Group I and the other half in Group II, so that the average productivity of all workers is 1.5. Note that the revenue expected to be generated from Group I workers is $100,000 ($10,000/year * 10 years) and from Group II workers is $200,000 ($20,000/year * 10 years). If firms could identify people by their productivity, they would offer them a wage equal to their marginal revenue product. Group I people would be paid $10, per year, Group II people $20,000. On the other hand, if firms could not identify productivity before they hired people, they would pay all workers an annual wage equal to the average productivity—$15,000. Group I people would then earn more ($15,000 instead of $10,000), at the expense of Group II people (who would earn $15,000 instead of $20,000).

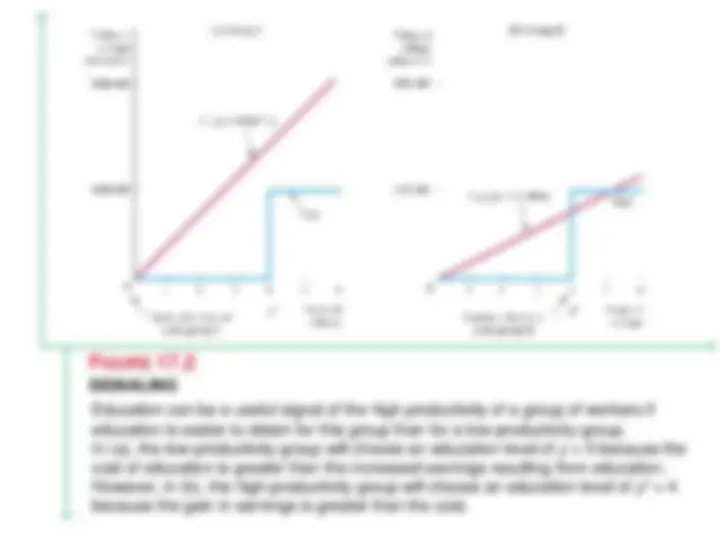

SIGNALING

FIGURE 17.

Education can be a useful signal of the high productivity of a group of workers if education is easier to obtain for this group than for a low-productivity group. In (a), the low-productivity group will choose an education level of y = 0 because the cost of education is greater than the increased earnings resulting from education. However, in (b), the high-productivity group will choose an education level of y * = 4 because the gain in earnings is greater than the cost.

COST – BENEFIT COMPARISON

People in each group make the following cost-benefit calculation: Obtain the education level y* if the benefit (i.e., the increase in earnings) is at least as large as the cost of this education. Therefore, Group I will obtain no education as long as $100, 000 < $40, 000 𝑦 ∗ or 𝑦 ∗

- 5 and Group II will obtain an education level y * as long as $100, 000 > $20, 000 𝑦 ∗ or 𝑦 ∗ < 5 These results give us an equilibrium as long as y * is between 2.5 and 5. When the firm interviews people who have four years of college, it correctly assumes their productivity is high, warranting a wage of $20,000. We therefore have an equilibrium. High-productivity people will obtain a college education to signal their productivity; firms will read this signal and offer them a high wage.

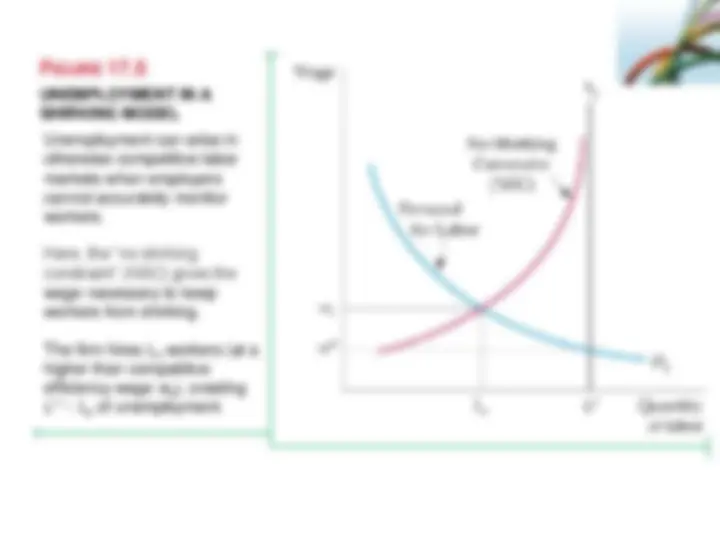

17.3 Moral Hazard

● moral hazard When a party whose actions are unobserved can affect the probability or magnitude of a payment associated with an event. The possibility that an individual’s behavior may change because she has insurance is an example of a problem known as moral hazard. The concept of moral hazard applies not only to problems of insurance, but also to problems of workers who perform below their capabilities when employers cannot monitor their behavior (“job shirking”). Moral hazard is a problem not only for insurance companies. It also alters the ability of markets to allocate resources efficiently.

THE EFFECTS OF MORAL HAZARD

FIGURE 17.

Moral hazard alters the ability of markets to allocate resources efficiently. D gives the demand for automobile driving. With no moral hazard, the marginal cost of transportation MC is $1. per mile; the driver drives 100 miles, which is the efficient amount. With moral hazard, the driver perceives the cost per mile to be MC = $1.00 and drives 140 miles.

The Principal–Agent Problem in Private Enterprises

Managers can often pursue their own objectives, rather than focusing on the objective of the stockholders, which is to maximize the value of the firm. One view is that managers are more concerned with rapid growth and larger market share, which provide more cash flow and in turn allows managers to enjoy more perks. Another view emphasizes the utility that managers get from their jobs, the power to control the corporation, the fringe benefits and other perks, and long job tenure. However, there are limitations to managers’ ability to deviate from the objectives of owners. First, stockholders can complain loudly when they feel that managers are behaving improperly. Second, a vigorous market for corporate control can develop unless managers pursue the goal of profit maximization. Third, there can be a highly developed market for managers. If managers who maximize profit are in great demand, they will earn high wages and so give other managers an incentive to pursue the same goal.

EXAMPLE 17.5 CEO SALARIES

CEO compensation has increased sharply over the past few decades. The average annual salary for production workers in the U.S. went from $18,187 in 1990 to $32,093 in 2009. But in constant dollar terms, the 2009 average salary was only $19,552 (in 1990 dollars), which represents only a 7.5% increase. At the same time, the average annual compensation for CEOs has grown from $2.9 million to $8.5 million, or about $5.2 million in 1990 dollars. In other words, while production workers have seen a 7.5% increase in their real wages over the past two decades, real CEO compensation has risen nearly 80%. Why? Have top managers become more productive, or are CEOs simply becoming more effective at extracting economic rents from their companies? The answer lies in the principal–agent problem, which is at the heart of CEO salary determination.