Download Asymmetric Information and more Lecture notes Economics in PDF only on Docsity!

PUBLIC FINANCE

ECON 453

E. Nketiah-Amponsah,

Department of Economics University of Ghana Legon Feb. 2026

symmetric Information and Market Failu

Learning Outcomes

- (^) At the end of this lecture, students should be able to ; - (^) Explain ‘Asymmetric Information’ and how pervasive

it is in the real world.

- (^) Understand and explain how asymmetric information

leads to market failure

- (^) Understand and explain how information asymmetry

leads to adverse selection

- (^) Understand and explain how information asymmetry

leads to moral hazard

- (^) Explain the principal-agent problem

- (^) appreciate the concept of supplier-induced demand

in healthcare by carefully articulating the import of

the Robert Evans model

Introduction

- AI occurs when one party in a transaction has superior or more information than the other market agents. It is potentially a ‘harmful’ situation because one party can take advantage of the other party’s lack of knowledge.

- For instance, the healthcare market is ripe with

problems of asymmetric information

- (^) Patients know their risks, insurance companies may not

- (^) Doctors understand the proper treatments, patients

may not

- AI results in market failure; a justification for policy intervention, e.g. compulsory car insurance and offering a menu of insurance contracts. In extreme situation this may lead to market failure where no exchange can take place

Pervasiveness of AI (Selected Markets)

- (^) Medical services : A Physician/doctor/health provider knows more about medical services than does the patient/client.

- (^) Insurance (Health ) : An insurance buyer knows more about his riskiness than does the insurance company. - (^) Asymmetric information occurs in (health) insurance markets when insurance attracts higher than average utilizers (adverse selection) than an actuarially fair premium would suggest

- (^) Used cars : The owner of a used car knows more about it (quality) than does a potential buyer.

- (^) Labour Market: Workers know their ability or reliability, but firms (employers) might not.

- (^) Market for loanable funds (Bank lending)

- (^) Car and Fire Insurance

The Problem

o (^) In the market for used cars

- (^) Sellers know the exact quality of the cars they sell

- (^) Buyers cannot distinguish good quality cars from bad ones (lemons)

- (^) Buyer beware cannot get your $/GHS back if you buy a bad car

- (^) If potential buyers only know the average quality of used cars, then market prices will tend to be lower than the true value of the top-quality cars.

- (^) Buyers offer average price: Owners of the top-quality cars will tend to withhold their cars from sale.

- (^) Due to a fall in perceived quality, demand shifts downward and equilibrium quantity decreases.

- (^) In a sense, the good cars are driven out of the market by the lemons (bad cars). Under what has become known as the Lemons Principle, the bad drives out the good until no market is left (market failure).

A Simple illustration

We assume that buyers know ;

50% of the cars for sale are good (plums)

50% are lemons (bad)

Assume, Good and Bad cars are worth GHS88,000 and

GHS66,000 respectively.

In this situation, what should a buyer offer for a car of

unknown type?

A risk neutral buyer will offer expected value of the car

Expected value here is the probability weighted average

value:

(1/2)(88,000) + (1/2)(66,000) = GHS 77,

- Thus if quality cannot be assessed, the buyer is willing to pay at most a price that reflects the average quality. However, sellers of good quality cars will not want to sells at the price for the average quality

- What will happen in the market for cars?

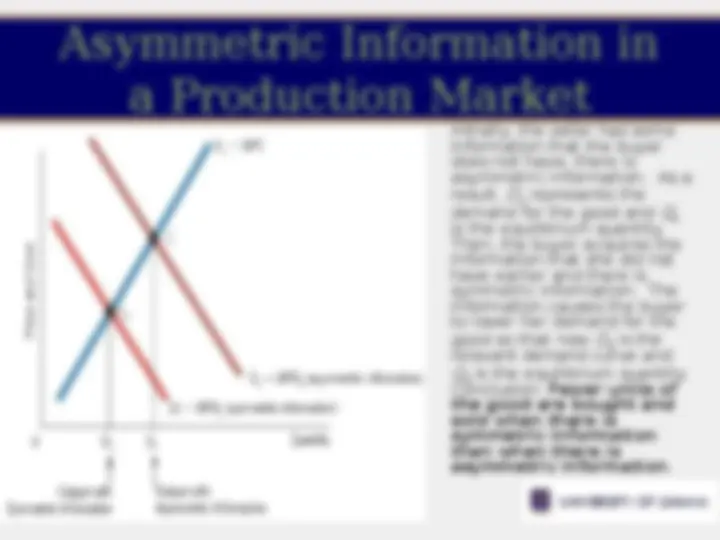

Asymmetric Information in

a Production Market

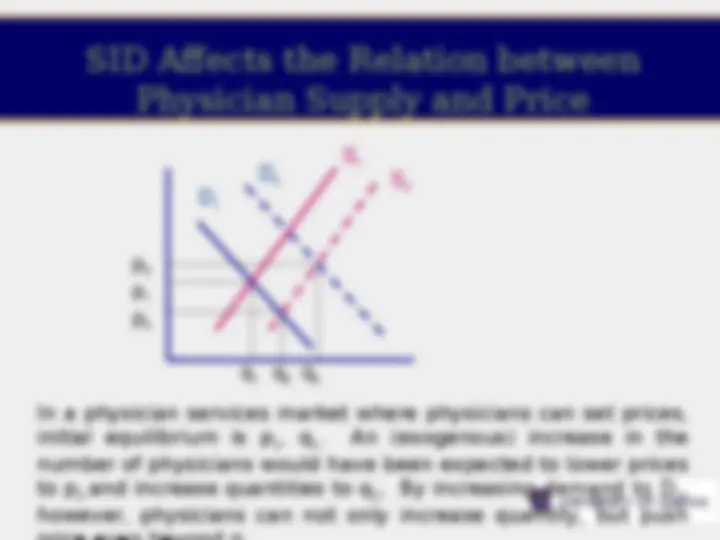

Initially, the seller has some information that the buyer does not have; there is asymmetric information. As a result, D 1 represents the demand for the good and Q 1 is the equilibrium quantity. Then, the buyer acquires the information that she did not have earlier and there is symmetric information. The information causes the buyer to lower her demand for the good so that now D 2 is the relevant demand curve and Q 2 is the equilibrium quantity. Conclusion: Fewer units of the good are bought and sold when there is symmetric information than when there is asymmetric information.

Asymmetric Information in

a Production Market

InitiInitally, the buyer (of the factor labor), or the firm, has some information that the seller (of the factor) does not have; there is asymmetric information. Consequently, S 1 is the relevant supply curve. W 1 is the equilibrium wage, and Q 1 is the equilibrium quantity of labor. Then, sellers acquire the information that they did not have earlier, and there is symmetric information. The information causes the sellers to reduce their supply of the factor so that now S 2 is the relevant supply curve, W 2 is the equilibrium wage, and Q 2 is the equilibrium quantity of labor. Conclusion: Fewer factor units are bought and sold and

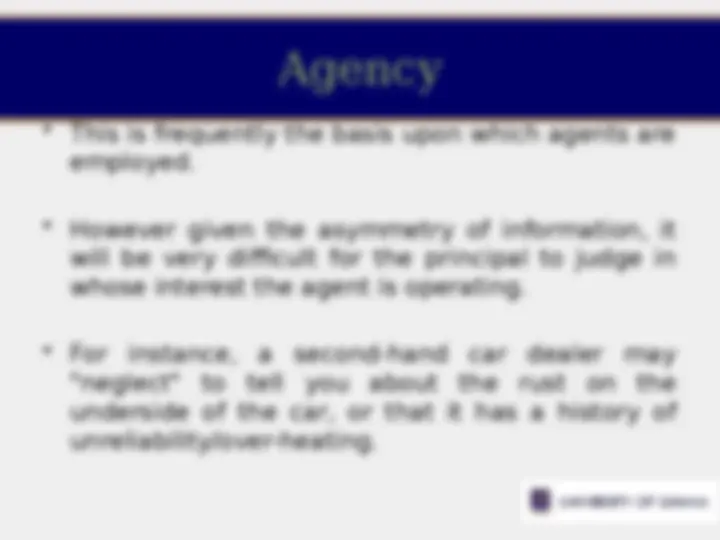

Agency

- (^) Asymmetric information lies at the heart of the

principal-agent problem.

- (^) The market ‘solution’ to imperfect information is the agency relationship

- (^) ‘Principal’ (patient) appoints ‘agent’ (health provider)

to advise them in making decision

- (^) Principal combines information with preferences to

make decision as if were perfectly informed

- (^) More usually agent combines information with

principal’s (expressed) preferences to make

decision (doctors make decisions for patients)

- (^) Agent is usually supplier, creating situation where one

actor is simultaneously both demander and supplier

in the market

Agency

- (^) This is frequently the basis upon which agents are employed.

- (^) However given the asymmetry of information, it will be very difficult for the principal to judge in whose interest the agent is operating.

- (^) For instance, a second-hand car dealer may "neglect" to tell you about the rust on the underside of the car, or that it has a history of unreliability/over-heating.

Robert Evan’s Model of

Inducement in the Health

• The model assumes that demand for inducement provides Care Market

disutility to the physician (then why engage in it?)

- (^) Let’s consider a world in which physicians maximize utility, and in which utility is a function of income I and hours of leisure L, we can add another term D to the utility function: U =U(I, L, D) where D is the amount of inducement engaged by the physician

- (^) In Evan’s model, D is characterized by increasing marginal disutility. If D has a negative effect on utility, why would physicians engage in it? - (^) A physician will be willing to induce demand as long as the amount of utility provided by the extra income exceeds the disutility associated with inducing demand. (See also McGuire and Pauly, 1991

Supplier induced demand in

the Health Care Market

- (^) Imperfect information on supply side leads to adverse selection

- (^) Imperfect information on demand side includes: - (^) current health state/diagnosis - (^) prognosis - (^) available interventions - (^) effectiveness/side-effects of interventions - (^) costs of interventions - (^) translating ‘effectiveness’ into ‘utility’

- (^) Supply side better informed about many of the above

Empirical Validity/Evidence

(^) Ikegami et al. (2020): Shows that when nearby hospitals acquire medical equipment such as MRI, inducement increases to the extent that patients patronizing the existing facility(ies) hitherto equipped with MRI end up demanding more health services than would have been needful. (^) Gruber et al. (1996) asserts that physicians in the USA compensated for their incomes losses following the reduction in fertility by recommending more (expensive) CS-sections. (^) Recent upsurge in caesarian deliveries in Ghana in the context of the Free Maternal Healthcare Policy/National Health Insurance Scheme??

- (^) Recent evidence suggests that CS delivery has increased from 13.5% in 2008 to 17.5% in 2014 (see GDHS 2008, 2014)

- (^) 11.2% points out of 13.5% and 14.2% points out of 17.5% of women who delivered by CS in 2008 and 2014 respectively had valid insurance cards.

- (^) NHIS significantly predicts and impacts CS delivery in Ghana (Amporfu, 2014; Awuku, 2017).

- (^) The changing mode of delivery for insured women is suggestive of SID

Empirical Validity/Evidence

(^) Ikegami et al. (2020): Shows that when nearby hospitals acquire medical equipment such as MRI, inducement increases to the extent that patients patronizing the existing facility(ies) hitherto equipped with MRI end up demanding more health services than would have been needful. (^) Gruber et al. (1996) asserts that physicians in the USA compensated for their incomes losses following the reduction in fertility by recommending more (expensive) CS-sections.

- (^) C-sections/100 births increased from 5.5% to 23.5% (240% increase (^) Dzampe & Takhashi (2022) find that an increase in competition— measured as a high doctor-to-population ratio at the district level— leads to an increase in the number of physician visits, suggesting physician-induced demand exists, and that effects are greater for large hospitals and public health providers