Download Estimating Beta: Overcoming the Regression Beta Problem and more Lecture notes Classical Physics in PDF only on Docsity!

Estimating Beta

The standard procedure for estimating betas is to regress stock returns (Rj) against market returns (Rm) - R (^) j = a + b Rm

- where a is the intercept and b is the slope of the regression.

The slope of the regression corresponds to the beta of the stock, and measures the riskiness of the stock.

This beta has three problems:

- It has high standard error

- It reflects the firm’s business mix over the period of the regression, not the current mix

- It reflects the firm’s average financial leverage over the period rather than the current leverage.

Beta Estimation: The Noise Problem

Solutions to the Regression Beta Problem

Modify the regression beta by

- changing the index used to estimate the beta

- adjusting the regression beta estimate, by bringing in information about the fundamentals of the company

Estimate the beta for the firm using

- the standard deviation in stock prices instead of a regression against an index

- accounting earnings or revenues, which are less noisy than market prices.

Estimate the beta for the firm from the bottom up without employing the regression technique. This will require

- understanding the business mix of the firm

- estimating the financial leverage of the firm

Use an alternative measure of market risk not based upon a regression.

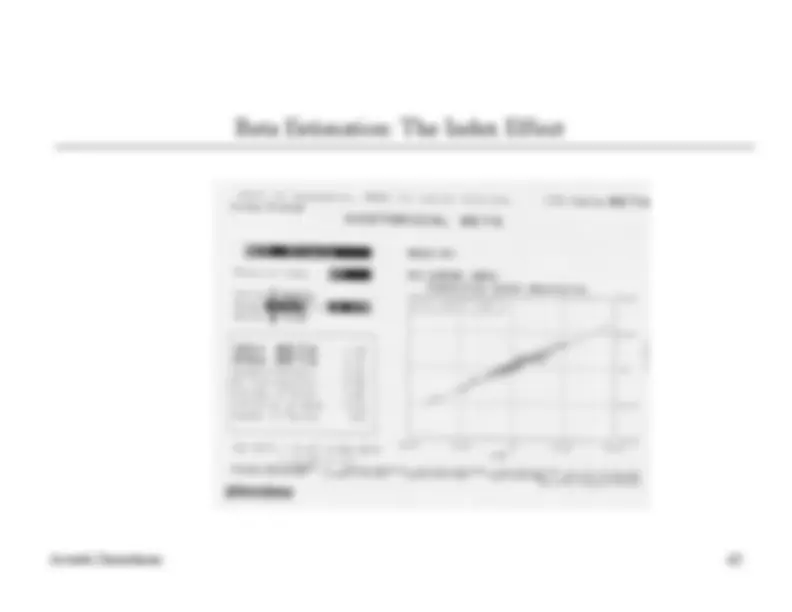

The Index Game…

Aracruz ADR vs S&P 500

S&P

-20 -10 0 10 20

Aracruz ADR

80 60 40 20 0

Aracruz vs Bovespa

BOVESPA

-50 -40 -30 -20 -10 0 10 20 30

Aracruz

1 40 1 20 1 00 80 60 40 20 0 -20-

A r a c r u z ADR = 2.80% + 1.00 S&P A r a c r u z = 2.62% + 0.22 Bovespa

In a perfect world… we would estimate the beta of a firm by

doing the following

Start with the beta of the business that the firm is in

Adjust the business beta for the operating leverage of the firm to arrive at the unlevered beta for the firm.

Use the financial leverage of the firm to estimate the equity beta for the firm Levered Beta = Unlevered Beta ( 1 + (1- tax rate) (Debt/Equity))

Adjusting for operating leverage…

Within any business, firms with lower fixed costs (as a percentage of total costs) should have lower unlevered betas. If you can compute fixed and variable costs for each firm in a sector, you can break down the unlevered beta into business and operating leverage components.

- Unlevered beta = Pure business beta * (1 + (Fixed costs/ Variable costs))

The biggest problem with doing this is informational. It is difficult to get information on fixed and variable costs for individual firms.

In practice, we tend to assume that the operating leverage of firms within a business are similar and use the same unlevered beta for every firm.

Bottom-up Betas

Step 1: Find the business or businesses that your firm operates in.

Step 2: Find publicly traded firms in each of these businesses and obtain their regression betas. Compute the simple average across these regression betas to arrive at an average beta for these publicly traded firms. Unlever this average beta using the average debt to equity ratio across the publicly traded firms in the sample. Unlevered beta for business = Average beta across publicly traded firms/ (1 + (1- t) (Average D/E ratio across firms))

If you can, adjust this beta for differences between your firm and the comparable firms on operating leverage and product characteristics.

Step 3: Estimate how much value your firm derives from each of the different businesses it is in.^ While revenues or operating income are often used as weights, it is better to try to estimate the value of each business.

Step 4: Compute a weighted average of the unlevered betas of the different businesses (from step 2) using the weights from step 3. Bottom-up Unlevered beta for your firm = Weighted average of the unlevered betas of the individual business

Step 5: Compute a levered beta (equity beta) for your firm, using the market debt to equity ratio for your firm. Levered bottom-up beta = Unlevered beta (1+ (1-t) (Debt/Equity))

If you expect the business mix of your firm to change over time, you can change the weights on a year-to-year basis.

If you expect your debt to equity ratio to change over time, the levered beta will change over time.

Possible Refinements

Why bottom-up betas?

The standard error in a bottom-up beta will be significantly lower than the standard error in a single regression beta. Roughly speaking, the standard error of a bottom-up beta estimate can be written as follows:

Std error of bottom-up beta =

The bottom-up beta can be adjusted to reflect changes in the firm’s business mix and financial leverage. Regression betas reflect the past.

You can estimate bottom-up betas even when you do not have historical stock prices. This is the case with initial public offerings, private businesses or divisions of companies.

€

Average Std Error across Betas Number of firms in sample

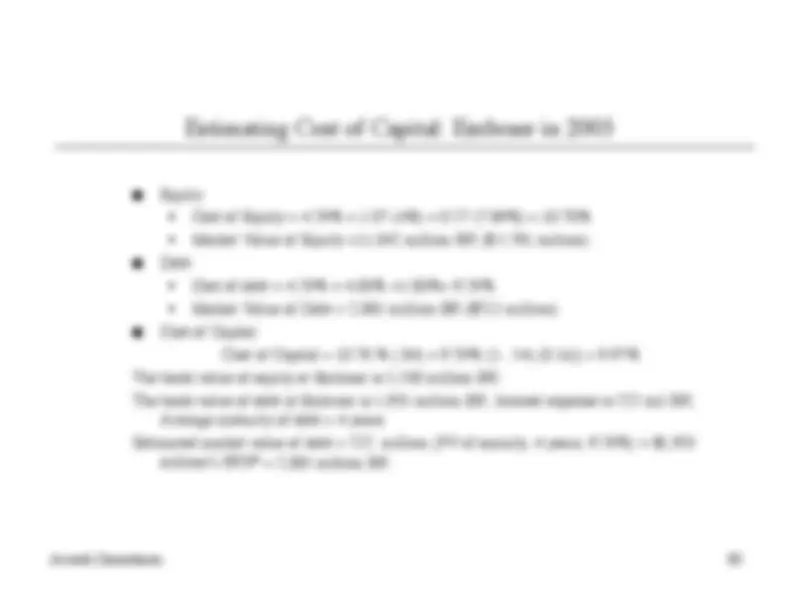

Embraer’s Bottom-up Beta

Business Unlevered Beta D/E Ratio Levered beta Aerospace 0.95 18.95% 1.

Levered Beta = Unlevered Beta ( 1 + (1- tax rate) (D/E Ratio) = 0.95 ( 1 + (1-.34) (.1895)) = 1.

Comparable Firms?

Can an unlevered beta estimated using U.S. and European aerospace companies be used to estimate the beta for a Brazilian aerospace company?

q Yes

q No

What concerns would you have in making this assumption?

The Cost of Equity: A Recap

Cost of Equity = Riskfree Rate + Beta * (Risk Premium)

Has to be in the same currency as cash flows, and defined in same terms (real or nominal) as the cash flows

Preferably, a bottom-up beta, based upon other firms in the business, and firmʼs own financial leverage

Historical Premium

- Mature Equity Market Premium: Average premium earned by stocks over T.Bonds in U.S.

- Country risk premium = Country Default Spread* ( σEquity/σCountry bond)

Implied Premium Based on how equity market is priced today and a simple valuation model

or

Estimating the Cost of Debt

The cost of debt is the rate at which you can borrow at currently, It will reflect not only your default risk but also the level of interest rates in the market.

The two most widely used approaches to estimating cost of debt are:

- Looking up the yield to maturity on a straight bond outstanding from the firm. The limitation of this approach is that very few firms have long term straight bonds that are liquid and widely traded

- Looking up the rating for the firm and estimating a default spread based upon the rating. While this approach is more robust, different bonds from the same firm can have different ratings. You have to use a median rating for the firm

When in trouble (either because you have no ratings or multiple ratings for a firm), estimate a synthetic rating for your firm and the cost of debt based upon that rating.

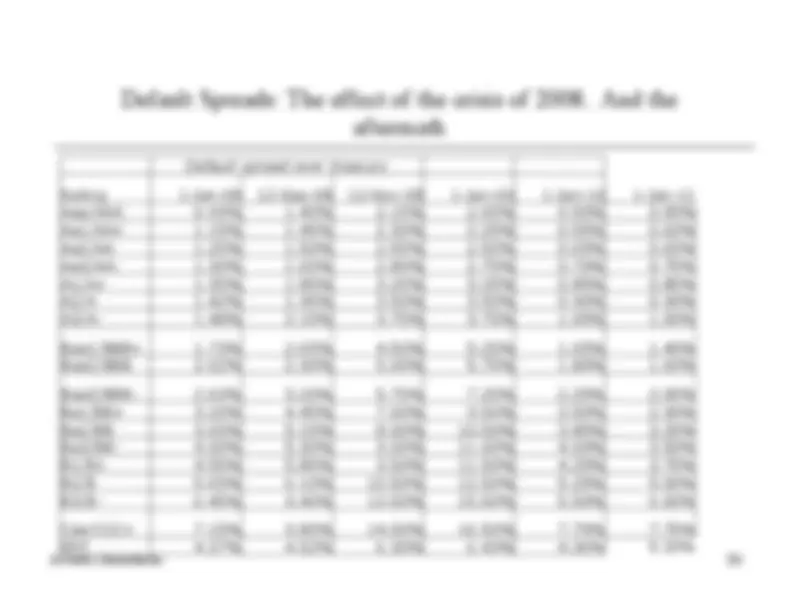

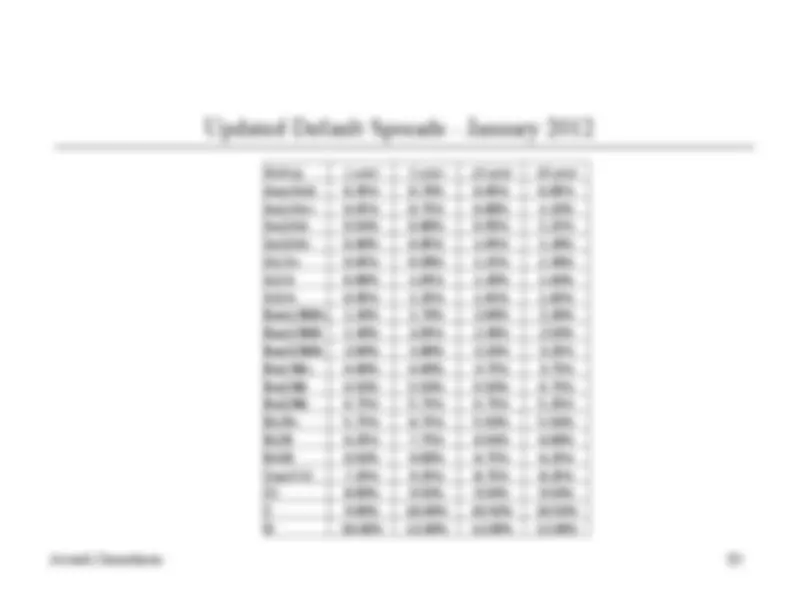

Interest Coverage Ratios, Ratings and Default Spreads: 2003

If Interest Coverage Ratio is Estimated Bond Rating Default Spread(2003) Default Spread(2004)

8.50 (>12.50) AAA 0.75% 0.35% 6.50 - 8.50 (9.5-12.5) AA 1.00% 0.50% 5.50 - 6.50 (7.5-9.5) A+ 1.50% 0.70%

4.25 - 5.50 (6-7.5) A 1.80% 0.85% 3.00 - 4.25 (4.5-6) A– 2.00% 1.00% 2.50 - 3.00 (4-4.5) BBB 2.25% 1.50% 2.25- 2.50 (3.5-4) BB+ 2.75% 2.00% 2.00 - 2.25 ((3-3.5) BB 3.50% 2.50% 1.75 - 2.00 (2.5-3) B+ 4.75% 3.25% 1.50 - 1.75 (2-2.5) B 6.50% 4.00% 1.25 - 1.50 (1.5-2) B – 8.00% 6.00% 0.80 - 1.25 (1.25-1.5) CCC 10.00% 8.00% 0.65 - 0.80 (0.8-1.25) CC 11.50% 10.00% 0.20 - 0.65 (0.5-0.8) C 12.70% 12.00% < 0.20 (<0.5) D 15.00% 20.00% The first number under interest coverage ratios is for larger market cap companies and the second in brackets is for smaller market cap companies. For Embraer , I used the interest coverage ratio table for smaller/riskier firms (the numbers in brackets) which yields a lower rating for the same interest coverage ratio.

Cost of Debt computations

Companies in countries with low bond ratings and high default risk might bear the burden of country default risk, especially if they are smaller or have all of their revenues within the country.

Larger companies that derive a significant portion of their revenues in global markets may be less exposed to country default risk. In other words, they may be able to borrow at a rate lower than the government.

The synthetic rating for Embraer is A-. Using the 2004 default spread of 1.00%, we estimate a cost of debt of 9.29% (using a riskfree rate of 4.29% and adding in two thirds of the country default spread of 6.01%): Cost of debt = Riskfree rate + 2/3(Brazil country default spread) + Company default spread =4.29% + 4.00%+ 1.00% = 9.29%