AUDIT EVIDENCE

Prepared by:

Siti Hajar Asmah bt Ali

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An in-depth understanding of audit evidence, its nature, appropriateness, and sufficiency. It covers various types of audit procedures such as inspection of records or documents, examination of physical assets, observation, inquiry, confirmation, scanning, computation, and re-performance. The document also discusses analytical procedures and their importance in identifying errors and anomalies.

Typology: Lecture notes

1 / 17

This page cannot be seen from the preview

Don't miss anything!

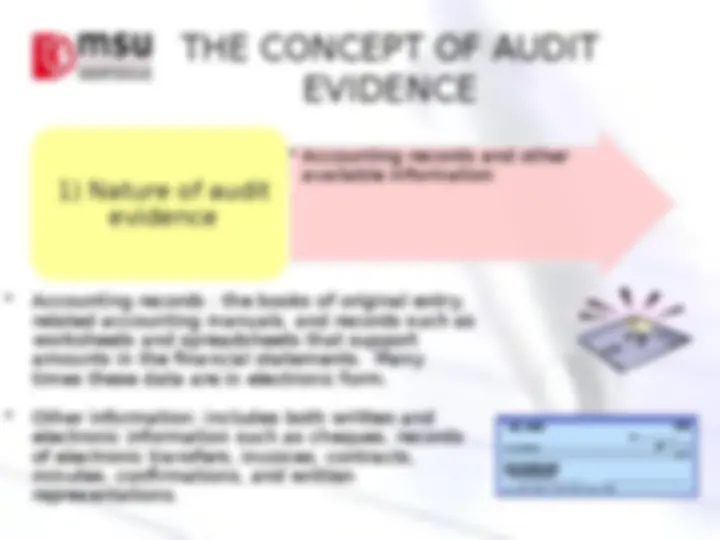

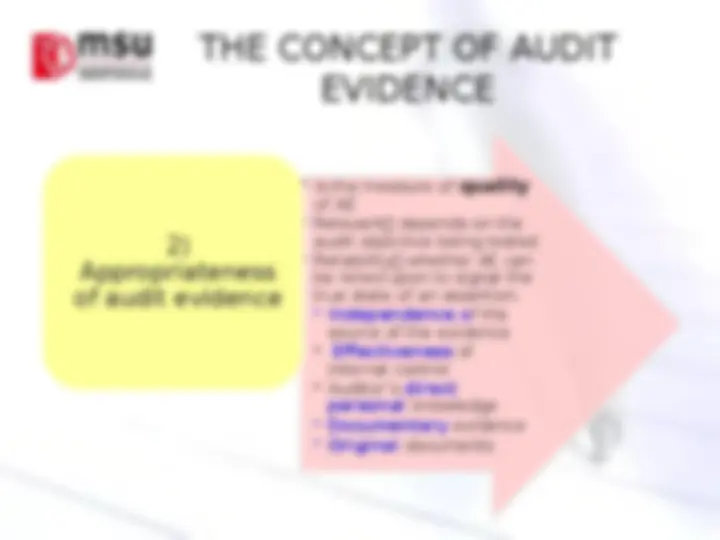

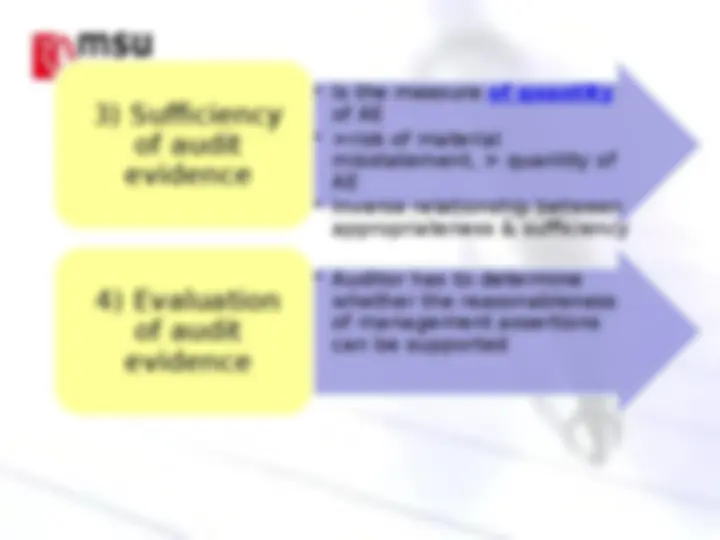

THE CONCEPT OF AUDIT EVIDENCE

AUDIT PROCEDURES Inspection of records or documents

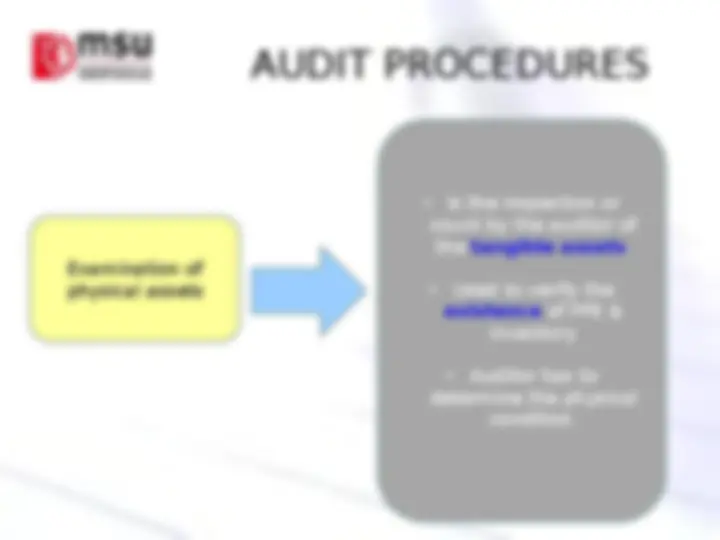

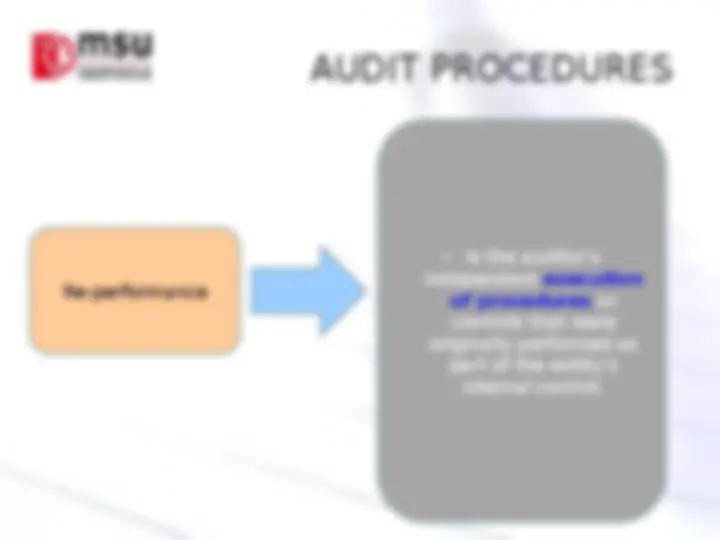

AUDIT PROCEDURES

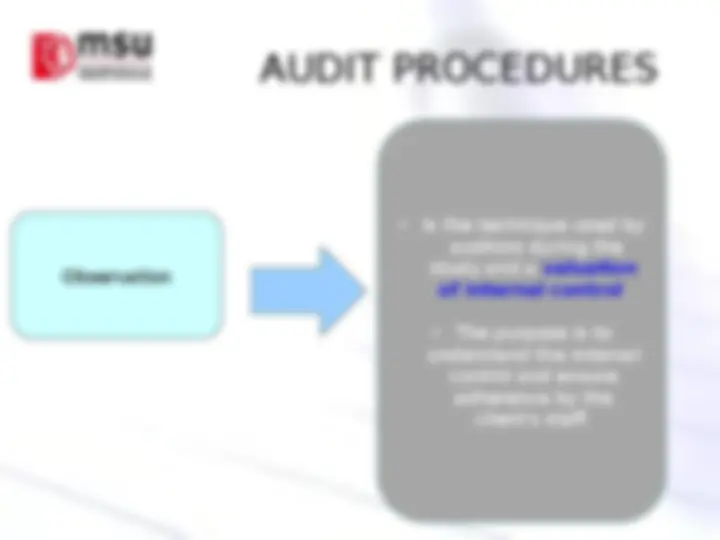

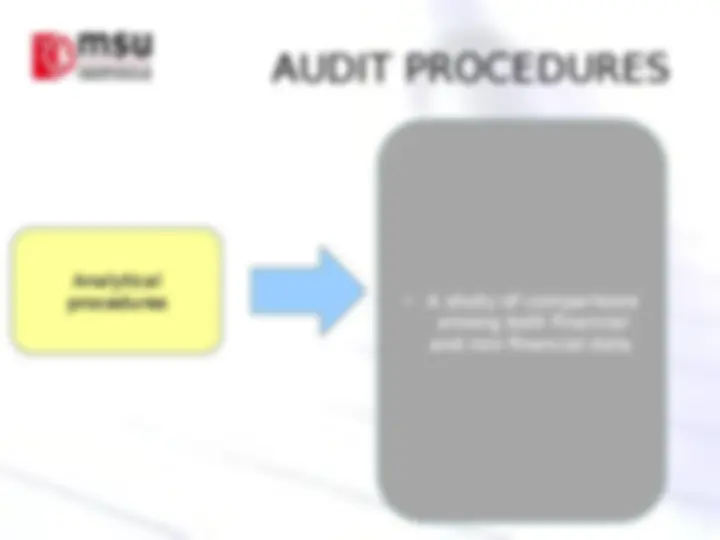

AUDIT PROCEDURES

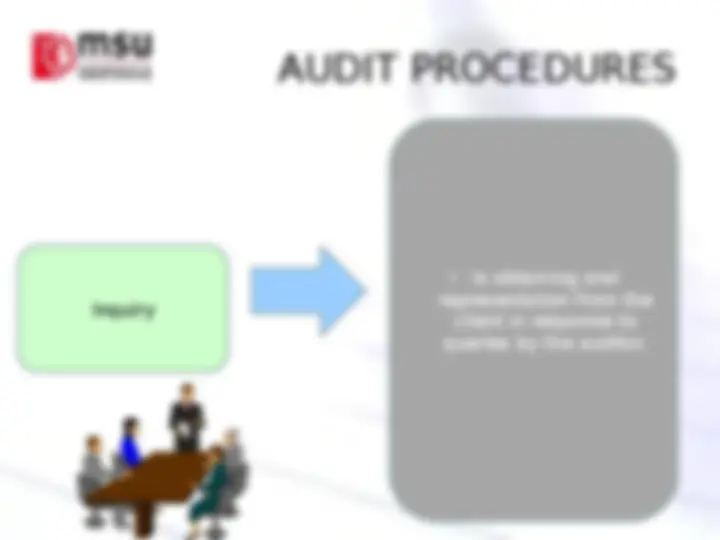

AUDIT PROCEDURES

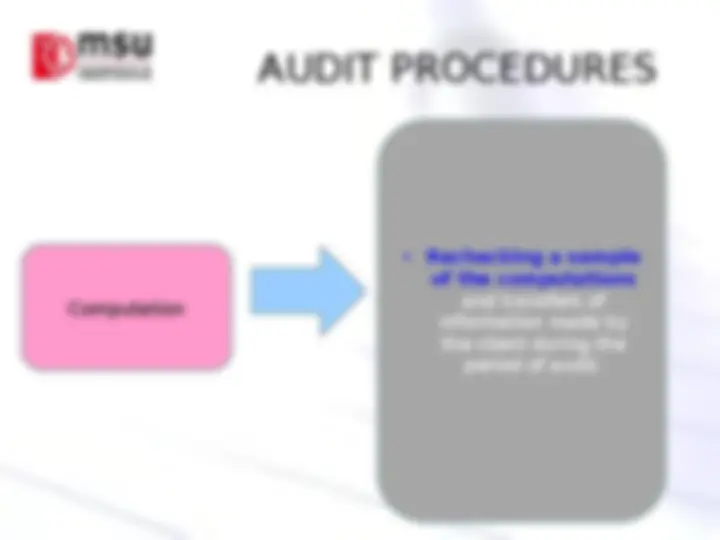

AUDIT PROCEDURES

AUDIT PROCEDURES

TYPES OF ANALYTICAL PROCEDURES