Download Bank reconciliation tutor and more Exercises Accounting in PDF only on Docsity!

Bank Reconciliation

Introduction to Bank

Reconciliation

A company's general ledger account Cash contains a record of the transactions (checks written,

receipts from customers, etc.) that involve its checking account. The bank also creates a record

of the company's checking account when it processes the company's checks, deposits, service

charges, and other items. Soon after each month ends the bank usually mails a bank statement to

the company. The bank statement lists the activity in the bank account during the recent month as

well as the balance in the bank account.

When the company receives its bank statement, the company should verify that the amounts on

the bank statement are consistent or compatible with the amounts in the company's Cash account

in its general ledger and vice versa. This process of confirming the amounts is referred to as

reconciling the bank statement, bank statement reconciliation, bank reconciliation, or doing a

"bank rec." The benefit of reconciling the bank statement is knowing that the amount of Cash

reported by the company (company's books) is consistent with the amount of cash shown in the

bank's records.

Because most companies write hundreds of checks each month and make many deposits,

reconciling the amounts on the company's books with the amounts on the bank statement can be

time consuming. The process is complicated because some items appear in the company's Cash

account in one month, but appear on the bank statement in a different month. For example,

checks written near the end of August are deducted immediately on the company's books, but

those checks will likely clear the bank account in early September. Sometimes the bank

decreases the company's bank account without informing the company of the amount. For

example, a bank service charge might be deducted on the bank statement on August 31, but the

company will not learn of the amount until the company receives the bank statement in early

September. From these two examples, you can understand why there will likely be a difference

in the balance on the bank statement vs. the balance in the Cash account on the company's

books. It is also possible (perhaps likely) that neither balance is the true balance. Both balances

may need adjustment in order to report the true amount of cash.

After you adjust the balance per bank to be the true balance and after you adjust the balance per

books to also be the same true balance, you have reconciled the bank statement. Most

accountants would simply say that you have done the bank reconciliation or the bank rec.

In addition to the following explanation of the bank reconciliation, we have developed a visual

tutorial, business forms, and exam questions to help you reinforce your understanding. They are

part of AccountingCoach PRO.

What is the purpose of Bank

Reconciliation?

A bank reconciliation is used to compare your records to those of your bank , to see if there are any differences between these two sets of records for your cash transactions. The ending balance of your version of the cash records is known as the book balance, while the bank's version is called the bank balance.

How often a Bank reconciliation

should be done:

Bank reconciliation statements are generally completed once a month.

However, if your business is very busy with a large number of transactions you

could ask your bank for an extra statement mid-month, or even weekly.

That way you can easily stay on top of the reconciliations and avoid feeling

rushed or stressed once a month.

If you have access to internet banking you do not have to wait for the bank to

send you a statement. Simply print a transaction listing for the dates you

require. Ensure there is an opening balance and a closing balance because

these are required to complete an accurate reconciliation.

There are no "rules" about how often to do a bank reconciliation statements. You

can do it daily if you wish. Then again, you could do it six monthly but only if

you have very few business transactions so that you don’t overload yourself

with too much work in one sitting!

Also important to note is that you should never reconcile a bank statement

to today's date , because today is not yet over and your closing balance might

change by the end of the day. The most up-to-date you can make a

reconciliation is to yesterday's date (meaning up to the day before you prepare

a reconciliation).

Bank Reconciliation Process

Step 1. Adjusting the Balance per Bank

Bank service charges are fees deducted from the bank statement for the bank's processing of the checking account activity (accepting deposits, posting checks, mailing the bank statement, etc.) Other types of bank service charges include the fee charged when a company overdraws its checking account and the bank fee for processing a stop payment order on a company's check. The bank might deduct these charges or fees on the bank statement without notifying the company. When that occurs the company usually learns of the amounts only after receiving its bank statement. Because the bank service charges have already been deducted on the bank statement, there is no adjustment to the balance per bank. However, the service charges will have to be entered as an adjustment to the company's books. The company's Cash account will need to be decreased by the amount of the service charges.

- Recall the helpful tip "put it where it isn't." A bank service charge is already listed on the bank statement, but it isn't on the company's books. Put it where it isn't: as an adjustment to the Cash account on the company's books.

An NSF check is a check that was not honored by the bank of the person or company writing the check because that account did not have a sufficient balance. As a result, the check is returned without being honored or paid. (NSF is the acronym for not sufficient funds. Often the bank describes the returned check as a return item. Others refer to the NSF check as a "rubber check" because the check "bounced" back from the bank on which it was written.) When the NSF check comes back to the bank in which it was deposited, the bank will decrease the checking account of the company that had deposited the check. The amount charged will be the amount of the check plus a bank fee. Because the NSF check and the related bank fee have already been deducted on the bank statement, there is no need to adjust the balance per the bank. However, if the company has not yet decreased its Cash account balance for the returned check and the bank fee, the company must decrease the balance per books in order to reconcile. Check printing charges occur when a company arranges for its bank to handle the reordering of its checks. The cost of the printed checks will automatically be deducted from the company's checking account. Because the check printing charges have already been deducted on the bank statement, there is no adjustment to the balance per bank. However, the check printing charges need to be an adjustment on the company's books. They will be a deduction to the company's Cash account.

- Recall the general rule, "put it where it isn't." A check printing charge is on the bank statement, but it isn't on the company's books. Put it where it isn't: as an adjustment to the Cash account on the company's books.

Interest earned will appear on the bank statement when a bank gives a company interest on its account balances. The amount is added to the checking account balance and is automatically on the bank statement. Hence there is no need to adjust the balance per the bank statement. However, the amount of interest earned will increase the balance in the company's Cash account on its books.

- Recall "put it where it isn't." Interest received from the bank is on the bank statement, but it isn't on the company's books. Put it where it isn't: as an adjustment to the Cash account on the company's books.

Notes Receivable are assets of a company. When notes come due, the company might ask its bank to collect the notes receivable. For this service the bank will charge a fee. The bank will increase the company's checking account for the amount it collected (principal and interest) and will decrease the account by the collection fee it charges. Since these amounts are already on the bank statement, the company must be certain that the amounts appear on the company's books in its Cash account.

- Recall the tip "put it where it isn't." The amounts collected by the bank and the bank's fees are on the bank statement, but they are not on the company's books. Put them where they aren't: as adjustments to the Cash account on the company's books.

Errors in the company's Cash account result from the company entering an incorrect amount, entering a transaction that does not belong in the account, or omitting a transaction that should be in the account. Since the company made these errors, the correction of the error will be either an increase or a decrease to the balance in the Cash account on the company's books.

Step 3. Comparing the Adjusted Balances

After adjusting the balance per bank (Step 1) and after adjusting the balance per books (Step 2), the two adjusted amounts should be equal. If they are not equal, you must repeat the process until the balances are identical. The balances should be the true, correct amount of cash as of the date of the bank reconciliation.

Step 4. Preparing Journal Entries

Journal entries must be prepared for the adjustments to the balance per books (Step 2). Adjustments to increase the cash balance will require a journal entry that debits Cash and credits another account. Adjustments to decrease the cash balance will require a credit to Cash and a debit to another account.

Items 1 through 10 above have been sorted into the following schedules labeled Step 1 and Step 2. The item number is shown in the far right column of each schedule.

Step 1 Amounts

Let's review the schedule for Step 1. In all likelihood the balance shown on the bank statement is not the true balance to be reported on the company's balance sheet. The bank reconciliation process is to list the items that will adjust the bank statement balance to become the true cash balance. As the schedule for Step 1 indicates, the amount of deposits in transit must be added to the bank statement's balance. Also, the amount of checks that have been written, but not yet appearing on a bank statement, must be subtracted from the bank statement's balance. Next any bank errors should be listed and should be reported to the bank for correction. (The company does not report deposits in transit and/or outstanding checks to the bank.)

Step 2 Amounts and Required Journal Entries

Step 2 begins with the balance in the company's Cash account found in its general ledger. The bank reconciliation process includes listing the items that will adjust the Cash account balance to become the true cash balance. We will review each item appearing in Step 2 and the related journal entry that is required. Remember that any adjustment to the company's Cash account requires a journal entry. Generally, the adjustments to the books are the result of items found on the bank statement but have not yet been entered in the company's Cash account.

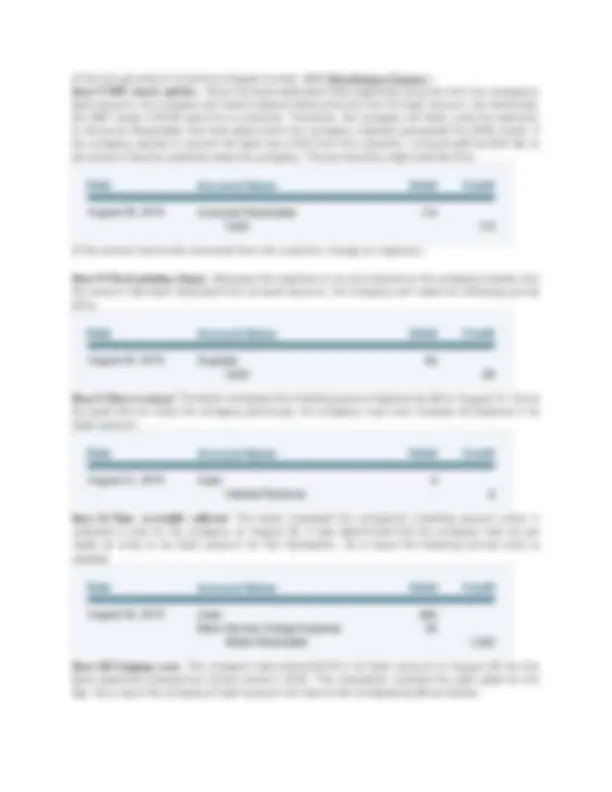

Item #2 Bank service charges. Since the bank deducted $35 from the company's checking account, but the company has not yet deducted this from its Cash account, the following journal entry needs to be made.

(If the annual amount of service charges is small, debit Miscellaneous Expense.) Item #3 NSF checks and fees. Since the bank deducted these legitimate amounts from the company's bank account, the company will need to deduct these amounts from its Cash account. As mentioned, the NSF check of $100 was from a customer. Therefore, the company will likely undo the reduction to Accounts Receivable that took place when the company originally processed the $100 check. If the company wishes to recover the bank fee of $10 from the customer, it should add the $10 fee to the amount that the customer owes the company. The journal entry might look like this:

(If the amount cannot be recovered from the customer, charge an expense.)

Item #4 Check printing charges. Because this expense is not yet entered on the company's books, but the amount has been deducted from its bank account, the company will make the following journal entry.

Item #5 Interest earned. The bank increased the checking account balance by $8 on August 31. Since the bank did not notify the company previously, the company must now increase the balance in its Cash account.

Item #6 Notes receivable collected. The bank increased the company's checking account when it collected a note for the company on August 29. It was determined that the company had not yet made an entry to its Cash account for this transaction. As a result the following journal entry is needed.

Item #10 Company error. The company had entered $145 in its Cash account on August 29, but the bank statement showed the correct amount: $154. The transaction involved the cash sales for the day. As a result the company's Cash account will have to be increased by $9 as follows:

BOOK

Balance

B. Deduct From BOOK Balance

C. Add To BANK Balance

D. Deduct From BANK Balance

Bank service charge. A. Add To BOOK Balance

B. Deduct From BOOK Balance

C. Add To BANK Balance

D. Deduct From BANK Balance

Interest credited to bank account.

A. Add (a) Add to book Balance

B. Deduct From book Balance

C. Add To BANK Balance

D. Deduct From BANK Balance

Interest charged to bank account. A. Add To BOOK Balance

B. Deduct From BOOK Balance

C. Add To BANK Balance

D. Deduct From BANK Balance

Deposit in transit.

Bank erred by posting another company's credit memo to your company's bank account. A. Add To BOOK Balance

B. Deduct From BOOK Balance

C. Add To BANK Balance

D. Deduct From BANK Balance

Fee charged by bank for returned check. A. Add To BOOK Balance

B. Deduct From BOOK Balance

C. Add To BANK Balance

D. Deduct From

BANK

Balance

A company wrote a check for $76 and it cleared the bank for $76. However, the company recorded the check in its Cash account as $67. How is the difference of $9 handled on the bank reconciliation? A. Add To BOOK Balance

B. Deduct From BOOK Balance

C. Add To BANK Balance

D. Deduct From BANK Balance

A company had a receipt of $989 and correctly prepared its bank deposit slip for $989. However, the company recorded the receipt in its Cash account as $998. How is the difference of $9 handled on the bank reconciliation?

A. Add To BOOK Balance

B. Deduct From BOOK Balance

BOOK

Balance

C. Add To BANK Balance

D. Deduct From BANK Balance

- A company's Cash account has a balance of $851 as of October 31. The bank statement for this account reports a balance of $1,430 as of October 31. There are outstanding checks totaling $840 and a deposit in transit of $60. The bank statement shows interest earned of $19, service charges of $30, a customer's returned check of $100, and a check printing fee of $90. The reconciled Cash balance that should be reported on the company’s balance sheet as of October 31 is $

.

Which of the following items will require a journal entry to the company's books? A. Bank Service Charge

B. (^) Deposit In Transit

C. Bank Error

Which of the following will NOT require a journal entry to the company's books?

A. Check Printing Charge

B. Outstanding Checks

C. Fee For NSF Check

A company recorded its check #2754 in its accounting records as $98. However, check #2754 was actually written for $89 and it cleared the bank as $89. What adjustment is needed to the Cash balance per books?

A. Decrease By $

B. Increase By $

C. None Needed

A company recorded its August 15 receipts on its books as $165. However, the receipts were actually $156. The deposit slip for the bank was prepared correctly as $156. What adjustment is needed to the Cash balance per books?

A. (^) Decrease By $

B. Increase By $

C. None Needed

Bank Reconciliation (Q&A)

What is an outstanding deposit?

An outstanding deposit refers to a company's receipts (cash, checks from customers, etc.) which have been recorded by the company, but the amount will appear on its bank statement at a later date. An outstanding deposit is also known as a deposit in transit.

To illustrate an outstanding deposit, let's assume that on October 31 a company received cash and checks from customers in the amount of $800. Clearly the company should report the $800 as part of its cash as of October 31. However, the company did not deposit the $800 into its bank account until after October

- Since the $800 is not on its bank statement as of October 31, the $800 is described as an outstanding deposit or deposit in transit as of October 31.

The $800 outstanding deposit is pertinent to the company's bank reconciliation as of October 31. When the company reconciles the bank statement, the outstanding deposit is an addition to the balance shown

Why does a company prepare a bank

reconciliation?

- To be certain that the amount of cash reported on the company's balance sheet (and the balance in its general ledger Cash account) is the correct amount. The additions and deductions on the bank statement are compared (or reconciled) with the items that are entered in the company's general ledger Cash account. Some differences, such as outstanding checks and deposits in transit, are noted as simply timing differences.

- Since most companies use double-entry accounting or bookkeeping, any omission or error in the company's general ledger Cash account also means that another general ledger account will have a corresponding omission or error. For example, if a company had wired money from its bank account for emergency computer maintenance services and had not recorded the credit to its Cash account, it is also omitting the debit to the account Computer Maintenance Expense. The bank reconciliation could prevent this company from issuing an incorrect balance sheet (incorrect Cash and incorrect Retained Earnings) and an incorrect income statement (expenses would be too low, net income would be too high).

- Performing a bank reconciliation results in improved internal control over the company's cash if done by someone other than the employee(s) handling and/or recording receipts and payments. Having another person reconciling the bank statement is known as the separation or segregation of duties and it should reduce the odds of dishonest acts involving the company's cash.

The bank reconciliation is also referred to as the bank statement reconciliation or as the bank rec.

How do I write off old outstanding

checks?

- Void the check and add the amount to your checkbook balance.

- Debit the general ledger Cash account for the amount, and credit the account that was originally debited.

- Remove the check from the bank reconciliation's list of outstanding checks.

Today, the answer is different for U.S. companies as states are now likely to have unclaimed property laws. For example, in my state a check issued to a vendor, but has not cleared the bank on which it is drawn, must be reported to the state after five years. In other words, you will now have to report a liability until the amount is remitted to your state.

Since you wrote the check and intended for it to be paid from the money in your checking, why not contact the payee as soon as the check is outstanding for 30 days? You may learn that the payee did not receive the check, had misplaced it, etc. Why not help your vendor the way you would want to be helped by your customers?

In short, communicate with the payees of your outstanding checks and eliminate the need for reporting and remitting to your state government many years after the original transactions.

In a bank reconciliation, what

happens to the outstanding checks of

the previous month?

The outstanding checks of the previous month will have either cleared the bank in the current month or will remain on the list of outstanding checks.

If an outstanding check of the previous month clears the bank (is paid by the bank) in the current month, you simply remove that check from the list of outstanding checks.

If an outstanding check of the previous month does not clear the bank in the current month, the check will remain on the list of outstanding checks until the month that it does clear the bank. In the bank reconciliation process, the total amount of the outstanding checks is deducted from the balance appearing on the bank statement. What is an unpresented check?

An unpresented check is a check written by a company and entered in its records, but the check

has not yet cleared the company's checking account. In other words, the check has not yet been

paid by the bank on which the check is drawn. An unpresented check is also known as an

outstanding check.

An unpresented check is listed on a bank reconciliation as a subtraction from the bank balance.

What does debit memo mean on a

bank statement?