Download basic corporate finance assignement and more Assignments Corporate Finance in PDF only on Docsity!

CIC 2001 BASIC CORPORATE FINANCE

SEMESTER 1 2020/

ASSIGNMENT 2

Tutorial slot: Thursday 1 pm - 3 pm

Lecturer: Dr. Koh Hsieng Yang Eric

Date Of Submission: 15 January 2021

Group 4 Members:

NAME MATRIC NO.

ANISHA SHARLENE BINTI ABD AVIS SUKURNY 17207178

HAZIQ FATHI BIN SAMSUL 17205502

LAVANYA LAKSMI A/P PERIASAMY U

KAVETHA A/P MAHALINGAM 17204928

NUR FATIN FATIHAH BINTI MUSTAZA 17203755

TABLE OF CONTENTS

NO. CONTENT PAGES

- Background of the Merger and Acquisition (M&A) exercise of the companies 1 -^4

- ● Target and acquirer company ● Type of industry (^4) - 6

- ● Purpose of the M&A exercise ● Type of M&A (^6)

- ● Mode of payment for the exercise ● Pricing paid by the acquirer to target company (^7)

- The chronology of the M&A process 8 - 9

- Performance of Acquirer and Target company: ● Market response ● Share price impact ● Financial performance

- Implication / Conclusion 18

- References

since the name of the larger company would now be substituted. In a single term, a business will buy by buying with cash or acquiring part of the stake to purchase a business. There is also an opportunity for a corporation to do their hardest to obtain all the properties of the other company for their own purposes. Mergers may be classified into many forms of mergers, distinguishable by just the arrangement between the merging entities. The category of merger will be referred to a horizontal merger, whereby two firms are in the same market as well as the finished product, where even the vertical merger between the seller and the business is linked, where the two companies supply the same type of goods and where the same client and team combine, where the two companies have little in common due to the type of industry. Mergers and acquisitions should be distinguished under certain scenarios and criteria for a depth study. For starters, a merger may only exist where a corporation wishes to combine as a separate entity with two other organizations of exactly the same size. An acquisition, though, applies to a big, economically powerful corporation that is able to purchase or buy through many legitimate deals to absorb a smaller firm. How the corporation tries to interact and consolidate into an impartial structure of managers, staff and customers may demonstrate the true difference. There are two forms of mergers of conglomerates. The merging between two corporations having little in general is a pure conglomerate, although blended conglomerate mergers. Next will be the mergers of the market extension, a corporate acquisition that takes place between businesses competing in the same goods but in different countries. The aim of this merger is to achieve greater market share and a wider base of consumers. Moreover, the fusion of product extension is the merging of two firms with the same business, but the items are only linked to one another. The aim of product extension mergers is to enable the merged businesses to obtain access to a broader variety of customers and to obtain greater benefit. Last but not least, as long as they could to accomplish their own ambitions and goals to build more successful companies than the past one, regardless of whether it is a merger or takeover. The success criteria can only be reached if the combined organisation is able to

fulfill those targets. The merger and takeover will profit a great deal from this step. Furthermore, a combined corporation is able to gain market supremacy, which would boost its profitability and sustain its economic survival. Another one, the merged group, will now be able to acquire innovative technologies that will allow them to be at the forefront of the market and obtain the benefit of opponents. Merger and acquisition would be the move for the business to develop into a significantly larger business that can thrive at a greater intensity of competition instead of the traditional order to expand. SapureCrest iPetroleum iBhd SapuraCrest iPetroleum iBhd iis iindeed imain ilocal isuppliers iof iinvolved ioil iand igas iindustry ifacilities, iand iit ihas ibeen ia idecent iroad ito ibe ithe ipioneering iplayer iin ithe iindustry ifor iMalaysia. iThe icompany iis ipursuing itwo imain ioperating idivisions, iPipeline iand iFacility iConstruction iand iOffshore iOil iand iGas iDrillingThe idivision iof iPipelines iand iInfrastructure iInstallation iis iactive iin ithe ideployment iof imarine ivessels iand iunderwater ipipelines, iwhich ihave iextended itheir iwings iregionally iand iglobally. iThe iOffshore iOil iand iGas iExploration idivision iis iactive iin ithe iexploration iof ioffshore ioil ifields iand ichartering irigs ifor ithe imining iof ioffshore ioil iwells. Kencana iPetroleum iBerhad Iniaddition, iKencana iPetroleum iGroup iis ithe ileading isupplier iof iadvanced ianalytics iand ifacilities iin iMalaysia ifor ithe ioil i& igas isector. iIt ihas ian iextended icomprehensive ioffering iof ifacilities ithat icovers ithe ibrand iimage iof idelivering iservices ifor iinfrastructure iand iproduction ias iwell ias ihook-up iand icommissioning, ionshore iconstruction, ioffshore imarine iand idrilling iactivities. iThey iare inow iextending itheir imarket iproposal iacross iour icore iskills, iknowledge iand imoney, ias iwell ias iventuring iinto ioil iand igas ifield igrowth iand iconsulting iwork. iIn iaddition, ithey iplan ito iexpand ito iprovide ia ihuge spectrum iof isubsea ifacilities ifor ithe ioil iand igas isector ibefore ijoining iit iinto imerger iby iparticipating iinto ithe iplanned ipurchase iof iAllied iMarine iand iEquipment iSdn iBhd i(AME). i

and changed their name into SapuraKencana Petroleum Berhad (SKPB). They have been 4th of biggest companies in the world by supplying oil and gas. However, they have renewed their SKPB name into Sapura Energy Berhad in 2017. SapuraCrest Petroleum Berhad was started on 3 March 1979 and was officially listed in the Second Board of Bursa Malaysia on 1992. SPCB operating in the petroleum industry majoring in transportation of oil and gas, construction of pipelines and equipment, marine services and operation of maintenance.In Malaysia, they are one of the largest company provides services of oil and gas. They were struggling to serve a best services to the customers based on their demands. They also made an investment with Crest Petroleum from UEM group under Sapura Telecommunication Bhd and joined with name Sapura group. Before the merger, Kencana Petroleum Berhad was named as Hin Loon Engineering (M) Sdn Bhd in 1982. It began as a resident contractor for a major fabrication yard by supplying manpower in Malaysia. By this Kencana HL and Kencana Bestwide two major subsidiaries in Kencana Petroleum, they successfully operated in excelled record for many years. They became the public listed company in December 2006 on the main market of Bursa Malaysia.They planned to expend and provide a wide range of sub-sea oil and gas facilities by entering into the proposed acquisition of Allied Marine and Equipment Sdn Bhd (AME) before entering into a merger. Furthermore, they can expand their core business into further propositions as it is also involved in engineering, procurement, construction and project management. Before the completing acquisition, the equity of SapuraCrest and Kencana was total is RM 1,619,576 million. However, after completion the merged their equity increase by RM 6,562,433 million. This proven that their merged of SapuraKencana Petroleum Berhad (SKPB) achieved success. Their vision is to be the best entrepreneur in the O & G industry and being great competitors in the global oil and gas company in the world. They become strong companies who has many expertise in the petroleum industry. PETRONAS also supported

both companies for their production capacity. The recapitalization granted by sub-contractors PETRONAS has refined competitiveness in the local industry because only giant contractors have permission for their huge asset capitalization. c) Purpose of M&A and identify the type of merger and acquisition The aim of merger and acquisition of SapuraKencana Petroleum Berhad (SPKB) is they want to create a full fledged integrated O&G services by supplying a powerful delivery capacity. By these two big companies, they become more powerful and become strong competitors in the competitive markets. They can produce good quality of O&G services as they have many expert professional workforce in the oil industry. This will lead to success for their company because two heads is better than one. With the power synergies, they can lead a role example to other companies. Furthermore, they aim to be an international brand despite getting high profits and expanding their supply of oil worldwide. According to the Chairman SapuraKencana Bhd, Datuk Hamzah Bakar, they want to strengthen their international track records and provide the best services as they can. They want to manage the complex task by using their expertise and grab any opportunity either in local or international projects in the future. Moreover, the merger and acquisition for SPKB is a share swap deal where the exchange of a target company share with acquiring company in amount of RM11.85 billion, are exercised to create the largest oil service.SapuraCrest and Kencana has been purchased by IKSB at RM 5.87 million and RM 5.98 million.It benefits in the earnings of sale due to low tax and long term capital gain rate. By merging both companies can reduce the risk and can lead in the Asian O&G. The merger of SapuraKencana Petroleum Berhad is horizontal integration. It means the two companies' processes are combined together at the same contribution on supplying

On 11 July 2011, Integral Key Sdn Bhd (IKSB) sent the offer letters to SapuraCrest Petroleum Bhd and Kencana Petroleum Bhd in order to notify them regarding the intention of IKSB to acquire their business for RM5.97 billion and RM 5.87 billion respectively. The reason for this acquisition is to merge the two companies to be the second-largest player in the country’s oil and gas service sector. Other than that, SapuraCrest specializes in terms of exploration and offshore installation. Meanwhile, Kencana Petroleum is recognized as one of the top fabricators in the world. Hence, if the merger of the two companies is successful, it will create an integrated O&G service provider with full capabilities to undertake marginal areas and improve the recovery of oil. Afterward, the major shareholder of both companies was approached by SPV in order to inform their intention as regards the merger. With this in mind, both major shareholders, Datuk Shahrial from Sapura Technology Bhd (which owns 40.1% of SapuraCrest) and Datuk Mokhzani from Khasera Baru Sdn Bhd (which owns 32.4% of Kencana) have indicated a strong interest in the merger. However, SPV must gain approval not just from the major shareholders, a 75% approval from both companies’ shareholders must be acquired. It is estimated that the whole process will be completed within six to eight months. On 15 December 2011, the planned merger between Kencana and SapuraCrest Petroleum Berhad was on track to be scheduled for 1Q 2012 pending regulatory approvals. Following the 99.8% approval vote of the shareholder of Kencana Petroleum Berhad. It is expected that by the end of February 2012, the merger will be completed. Eventually, after further discussion and agreement, SapuraCrest Sdn Bhd and Kencana Petroleum Sdn Bhd successfully merged to form SapuraKencana Petroleum Bhd on 17 May 2012. Therefore, SapuraKencana Petroleum Bhd was listed on the main market of Bursa Malaysia, initiating as the country's largest integrated oil and gas service provider. Nonetheless, SapuraKencana issued a total of 5,0004,366,196 shares at RM2 per share, which put them in the largest Malaysian companies by market capitalization in the top 30.

f) Analysis and evaluation of pre and post effect of the merger and acquisition exercise (i) Market response On May 17, 2012, SapuraKencana Petroleum Bhd, a merged company between SapuraCrest Petroleum Bhd and Kencana Petroleum Bhd, was classified on the Bursa Malaysia’s main board, creating a huge integrated oil and gas service provider by property in the world. SapuraKencana is said to be on a stable footing to land larger and more profitable oil and gas projects around through Malaysia, having turned itself into a filled with lots of engineering, procurement, production, installation and commissioning oil and gas service providers. SapuraKencana had a market capitalisation of RM2917 billion at the end of their combined year. The Star Online published 5 May 2012 announced that the chief executive officer of Areca Capital Sdn Bhd tells it is pleasant to have such a big acquiring firm soon be making its presence in Bursa Malaysia. Such large firms with greater market capitalization will draw international investors. On The Borneo Post on 18 May 2012, Datuk Hamzah Bakar, Chairman of SapuraKencana, stated, 'The O&G Industry is already looking for immediate service providers that can handle difficult operations. Our fresh, improved place, supported by a complete set of applications and a global platform proven record, puts us in a better position to develop our global reach while domestically exploiting opportunities. This doesn't really mean that, at the cost of all else, we are simply looking to raise revenues, but to continue to aspire to be an international company. To achieve this would mean that not only SapuraKencana, but Malaysia and Malaysia as a whole might create a good image globally. SapuraKencana would also have greater economic opportunities, technology and production understood exactly as a combined company, as SapuraKencana's partners would provide great support if necessary. SapuraKencana would be able to experience a greater degree of performance and quality with a broad collaboration base in entering new markets,

demand in their inventory, Kencana Petroleum had a good output in 2011. But SapuraCrest Petroleum's share price remained stable at RM0.71 in both 2010 and 2011 because of the unchanged demand. After those companies agreed to merge in 2012, SapuraKencana’s share price reached RM2.0 per share. The company's share price rose marginally to RM2.14 in 2013. Even though it’s not a dramatic raise but still the share price rose RM0.14 in one year. This shows SapuraKencana has a great result as the company has the potential to retain its productivity and improve its credibility to build more support from domestic and national investors and also customers after merging. Capital Asset Pricing Model (CAPM) The Capital Asset Pricing Model (CAPM) explains the relationship between systematic risk or known as a diversifiable risk with an expected return of a particular risk. The formula for CAPM is as follows: The CAPM formula is used to calculate the expected return of an investment. The expected return comprised three aspects as per the formula shown above. The risk free return (𝑅𝑓),beta (𝛽𝑖)and the risk premium (𝐸(𝑅𝑚) − 𝑅𝐹). The risk free rate of return is the rate investors expect from a completely risk free investment. On the other hand, the risk premium is also known as the non-diversifiable risk which will be obtained by deducting risk premium is also known from expected market return [𝐸(𝑅𝑚)]. Investors who prefer riskier investment would opt for an investment with a higher risk premium. The value of Beta (𝛽𝑖) is the measurement of non- diversifiable risk of a security or stock in a portfolio. In this merger and acquisition case, we will focus on the both companies which are SapuraCrest and Kencana point of view for CAPM analysis to see whether the companies

have profited or suffered losses from the merging. The CAPM figures before and after merging are as follows: Before Acquisition After Acquisition Rf of 2011 2.3% 2.3% Rm of 2011 - 2.98% - 2.98% Risk Premium (Rm-Rf) - 5.28% - 5.28% Beta 0.020 - 0. E(Ri) 2.3% + 0.020(-5.28%) =0.

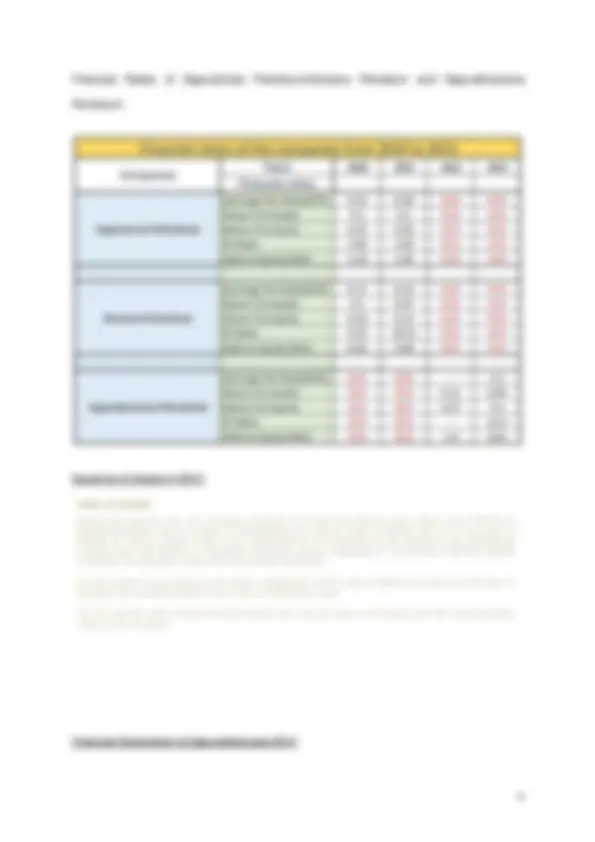

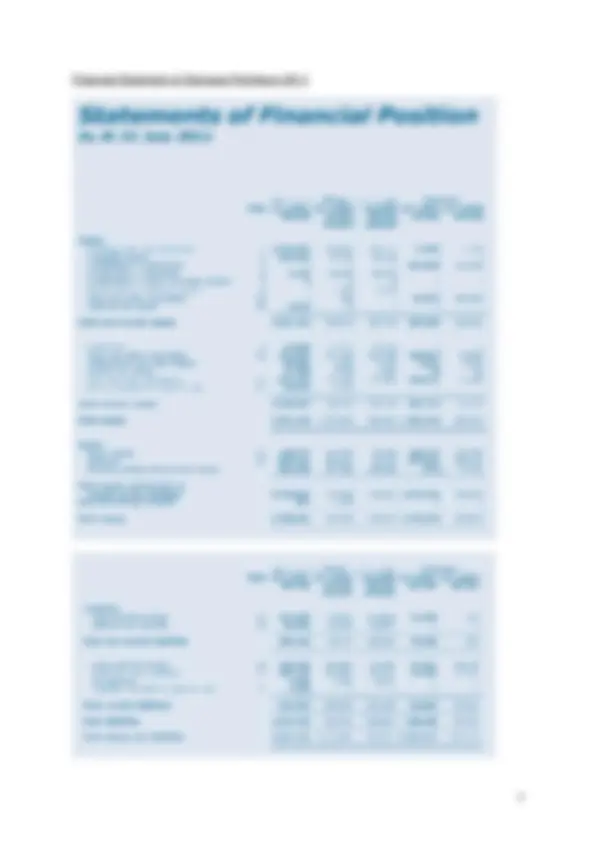

It is important to note that the risk free rate and premium rate are fixed in the computation of CAPM. On the other hand, the beta value acted as a variable. As shown in the table above, the beta value decreased from 0.020 to - 0.21 after the merging of both companies. After the merger the beta had a ngeative value which indicates that the stocks were not very sensitive the market, a beta of 1 means there is risk present and a beta of 0 means riskless. Therefore, the merging of both companies has diversified and significantly reduced their systematic risk of stocks. On the other hand the expected return value 𝐸(𝑅𝑖),value increased from 0.02 to 0.034. The negative beta post acquisition has caused the stocks to have an inverse relation with the market. In conclusion the Capital Asset Pricing Model stipulates that merging of these both companies has been more of a bargain than a loss seeing that the expected return increased. iii) Financial Performance The ratios below were derived from the values taken from the annual report of SapuraCrest Petroleum Bhd, Kencana Petroleum Bhd and SapuraKencana Bhd from the year 2010 to

- However, in 2012 after the merger SapuraKencana did not issue its annual report but the figures were taken from the annual report of 2013 that also reports the performance of previous year.

Graph 3 Return on Equity is another important profitability ratio as it shows how well the firm is generating earning growth through the investment. It is a ratio that allows the shareholders to know how much return the company can make with each ringgit the shareholders have invested. It is calculated by dividing net income over shareholder’s equity. Based on graph 3, both the individual firms have an ROE of 26% and 13% respectively in the year 2011. After the merger, the ROE has increased to 27% in 2012. However, out of expectations the ROE drops drastically to 10.47% in the following year. This can be due to decreasing gross profit margin where it can be caused by the dwindling number of sales. Besides, there can be also a limitation on the portions of earning from the acquiree company which had a negative impact on the profits as the adapting process to the acquisition accounting method for the merger can be still new. **Market Ratio

- Earnings Per Share**

Graph 1 Earnings per share is the firm’s annual profit per outstanding share where it is calculated by dividing net income over the number of outstanding shares. The higher the EPS the better it is as it indicates that the firm is profiting and has more profits to distribute to its shareholders. Based on Graph 1, after the merger took place in 2012, SapuraKencana did not issue any share capital. Hence, EPS in 2012 was not stated. While in the year 2013, we can see that the company earned RM0.1 per share which is slightly lower than both the individual firm’s in the year 2010 and 2011. This indicates that for every RM1 the investors invest, an amount of 10 sen is earned by the firm. Even though the EPS is relatively lower, it still indicates a good start as it is only a difference of RM0.03 and shows SapuraKencana can hit back the profit in the long run. 4) PE Ratio

Graph 5 Debt to equity is a leverage ratio which portrays what amount of debt and equity is being used to fund a firm’s assets which indicates the ratio of the firm’s total liabilities to its shareholder equity. Debt to equity ratio reflects the ability of shareholder equity to cover all outstanding debts if the firm faces an emergency or bankruptcy. A good debt to equity ratio will be about 1.5 or lower while a ratio which is higher than 2.0 is less preferable as it associates higher risk. Based on graph 5, the debt to equity ratio of Sapura and Kencana showed an increasing trend from 2010 to 2011 with the ratio of 1.56 and 0.88 respectively in the year

- After the merger in 2012, there is a slight increase in the ratio where it rose to 1.6 but however the following year it dropped to 1.25 which is a good sign to the merged firm. Thus, based on all the financial performance, we can see that SapuraKencana has performed quite well after the merger even though there were some downfall in certain areas of the ratios. This can be due to the new adaptations of the accounting method of both firms and it is to believed that SapuraKencana have actually performed well in the consequent years after the merger.

Implications / Conclusion In several modes of financial exchange, merger and acquisition can be viewed as a merging of firms. Our group has decided to concentrate on the 2012 merger among Kencana and SapuraCrest. SapuraCrest Petroleum Berhad is the petroleum corporation via its subsidiaries, which focuses on shipping and installation contractors. The Kencana Petroleum company is the supplier of integrated technologies and facilities for Malaysia's offshore oil and gas sector and drilling rigs. There are five types of mergers but both of them to be horizontal integration SapuraKencana Petroleum Bhd. The major oil and gas industries in Malaysia are both businesses. The company's name was changed to Sapura Energy Berhad. SapuraKencana Berhad has been able to widen market segments and achieve greater consumer access. The group knew it would be able to improve its core industries by fusion. Acquisition preparation will be the next important step. To have more data about each business enterprise, the two organizations communicate and start discussions. In spite of the industry reaction, since they would have greater access to foreign markets, SapuraKencana will now be able to attract increasingly large deals. Currently, they are evolving as a single young business with a vision for the O&G industry becoming a global superpower. The O&G Market is now searching for turnkey service suppliers that can handle complicated projects end to end. In this sector, they could grow further if they see the potential in this area. Pretty much across the board, both corporations seek to build synergies, indicating that with purchase and integration they would like to decrease the conflicting component and content or operation. In the new organisation where the firms run, they would merge them. In addition, by carrying out merger and acquisition, by acquiring over it or combining with yet another business, they may lower the amount of operating throughout their sector.

8. References