Download Business Plan Final Environmental Impact Statement and more Study notes Business English in PDF only on Docsity!

Business Plan Final Environmental Impact Statement

(DOE/EIS-0183)

Responsible Agency: U.S. Department of Energy, Bonneville Power Administration (BPA)

Title of Proposed Action: Business Plan

States and Provinces Involved: Arizona, California, Idaho, Montana, Nevada, New Mexico, Oregon,

Utah, Washington, Wyoming, and British Columbia

Abstract: BPA issued a Business Plan Draft Environmental Impact Statement (EIS) in June 1994 and a

Supplemental Draft EIS in February 1995. Since then, the business environment has continued to change,

and commenters have offered additional opinions and information which have been considered in the

preparation of this Final EIS (FEIS). The FEIS focuses on the analysis of relationships among BPA, the

utility market, and the affected environment.

To participate successfully in an increasingly competitive and dynamic electric utility environment and to

continue to meet specific public service obligations as a Federal agency, BPA needs adaptive policies to

guide its marketing efforts (including power and transmission products, energy services such as

conservation, and pricing mechanisms) and its administration of other statutory obligations such as its fish

and wildlife responsibilities. In selecting among alternative ways to meet this need, BPA will consider the

following purposes: achieve a set of Strategic Business Objectives; competitively market BPA’s power and

transmission products and services, both within the Pacific Northwest and outside the region, and assure

that BPA remains competitive; provide for equitable treatment of Columbia River Basin fish and wildlife in

relation to other purposes of the Federal Columbia River Power System; give energy conservation the

priority accorded it under the Northwest Power Act, and achieve BPA’s share of the conservation target

under the Council’s regional goal; establish rates that are easy to understand, easy to administer, stable,

and fair; recover BPA’s costs through rates; continue to meet statutory and treaty mandates and contractual

obligations; avoid adverse environmental impacts; and establish and maintain productive government-to-

government relationships with Indian Tribes.

The EIS discusses 19 specific issues and their effects over the range of Business Plan alternatives. The six

alternatives are: Status Quo (No Action), BPA Influence, Market-Driven (Proposed Action), Maximize

Financial Returns, Minimal BPA, and Short-Term Marketing. These alternatives may be varied by

replacing intrinsic elements with one or more policy modules responding to key issues (fish and wildlife

administration, rate design, Direct Service Industry service options, and conservation/renewable resources).

The alternatives and modules were tested for impacts on BPA’s marketing against two widely differing

“endpoint” scenarios for operation of the Columbia River system. The alternatives were compared in terms

of market responses, which include resource development, resource operations, transmission development

and operation, and consumer responses. These market responses were then used to estimate potential

environmental impacts.

Although the environmentally preferred alternatives can be identified—Status Quo and BPA Influence—

environmental differences among the alternatives appear to be relatively small. Other business aspects,

including loads and rates, showed greater variation among the alternatives. BPA’s ability to achieve the

purposes for action would be weakened under the environmentally preferred alternatives.

To request additional copies of the EIS, please contact:

For additional information on the EIS, please contact: Public Involvement Manager Charles Alton or Don Wolfe, Project Co-Managers P.O. Box 12999 P.O. Box 3621 Portland, OR 97212 Portland, OR 97208- Phone: (503) 230- Copies may also be obtained by calling BPA’s toll-free document request line: 1-800-622-4520. For information on DOE NEPA activities contact: Carol M. Borgstrom, Director, Office of NEPA Oversight, EH-25, U.S. Department of Energy, 1000 Independence Avenue, SW, Washington, DC, 20585. Phone: 1-800-472-2756.

Summary

BPA Business Plan Final EIS Summary • S-

Summary: Business Plan

Final Environmental Impact

Statement

The Business Plan Final Environmental Impact Statement (FEIS) seeks to address a need for business strategies and policies that will allow the Bonneville Power Administration (BPA) to participate fully in the rapidly changing energy market in the Pacific Northwest (PNW). The EIS explores the effects of 19 key issues in five broad categories (products and services, rates, energy resources, transmission, and fish and wildlife administration) and a range of different business directions (alternatives) responding to those issues. Policy modules permit construction of further variations on those alternatives. The set of alternatives is tested against two widely differing operations of the Columbia River system. Environmental impacts are identified, and the alternatives compared. Finally, the EIS describes possible response strategies (mitigations) that the agency might take for any alternative that does not allow BPA successfully to balance its costs and revenues. The proposed action is the Market-Driven alternative. The Summary contains section references so that the reader may locate the corresponding material in the FEIS.

Purpose of and Need for Action [Sections 1.1, 1.2]

The electric utility market is increasingly competitive and dynamic. To participate successfully in this market and to continue to meet specific public service obligations as a Federal agency, the Bonneville Power Administration (BPA) needs adaptive policies to guide its marketing efforts (including contracts for the sale of power and transmission products and services, and pricing mechanisms) and its administration of other obligations such as its energy conservation and fish and wildlife responsibilities. Four factors define and focus this need now: (1) Market Change. The electric energy industry is in a period of rapid business change that has increased competition and lowered the price of power from BPA competitors. The market is increasingly deregulated. Natural gas prices have fallen. Combustion turbines, an alternative technology for generating energy, have fallen in price and installed cost, and increased in performance efficiency. Wholesale marketers are aggressively pursuing BPA customers, even operating for a time at a loss to gain entrance to the PNW market. The price of power is correspondingly affected. (2) Obligations. BPA has mandated obligations beyond power marketing, such as fish and wildlife enhancement, support of energy efficiency, and environmental stewardship. Costs to carry out these missions have increased over time. In fulfilling these responsibilities, BPA must balance the interests of its ratepayers and its responsibility to the environment. BPA also shares in the Federal government’s trust responsibilities to Indian Tribes. (3) Cost/Revenue Balance. BPA must be able to balance its costs and revenues. With comparable power available at competitive prices, BPA can no longer meet increased costs by raising rates, without running the risk of losing customers.

S-2 • Summary Summary

(4) Lost Hydro Opportunity. More than three-quarters of BPA’s power is produced by generation at dams on the region’s rivers. A succession of dry years and changes in hydro system operations have seriously affected BPA’s ability to generate revenue. In times of average runoff, extra power can be produced and sold to help meet BPA’s revenue requirements. Dry years reduce opportunity for these extra revenues. Opportunity is also likely to be reduced under the latest proposals to change hydroelectric operations, as specified in the 1995 National Marine Fisheries Service (NMFS) Biological Opinion. BPA has been operating under policies that do not adequately account for the confluence of these factors and that therefore may prevent the agency from fulfilling all its missions. In selecting among the proposed and alternative ways to meet the need, BPA will consider the following purposes:

- Achieve a set of Strategic Business Objectives.

- Competitively market BPA's power and transmission products and services, both within the Pacific Northwest (PNW) and outside the region, and assure that BPA remains competitive.

- Provide for equitable treatment of Columbia River Basin fish and wildlife in relation to other purposes of the Federal Columbia River Power System.

- Give energy conservation the priority accorded it under the Northwest Power Act, and achieve BPA’s share of the conservation target under the Council’s regional goal.

- Establish rates that are easy to understand, easy to administer, stable, and fair.

- Recover BPA's costs through rates.

- Continue to meet statutory and treaty mandates and contractual obligations.

- Avoid adverse environmental impacts.

- Establish and maintain productive government-to-government relationships with Indian Tribes.

BPA’s Business Plan [Section 1.3]

The Business Plan FEIS addresses the environmental impacts of alternatives for BPA’s Business Plan, which will set policy direction for BPA’s pricing, power marketing, transmission, other necessary activities such as conservation and fish and wildlife administration activities. The Business Plan will be based on the BPA Strategic Marketing Plan (Marketing Plan) and Strategic Action Plans for major BPA functions. The EIS has identified numerous issues with the potential to affect market responses and subsequent environmental impact in two of these Strategic Action Plans (Marketing, Conservation and Production; and Transmission Services). Most issues are associated with power and resources, including product development, rates, generation resources, new power sales contracts, and conservation. A key issue for transmission system development is the level of transmission system reliability. The following Business Plan elements have the greatest potential to lead to environmental impacts through changes in energy resource development and operations and/or transmission development:

- the products and services BPA will offer;

- the resources, if any, BPA will acquire to supply those products and services; and

- the pricing principles BPA will apply to those products and services.

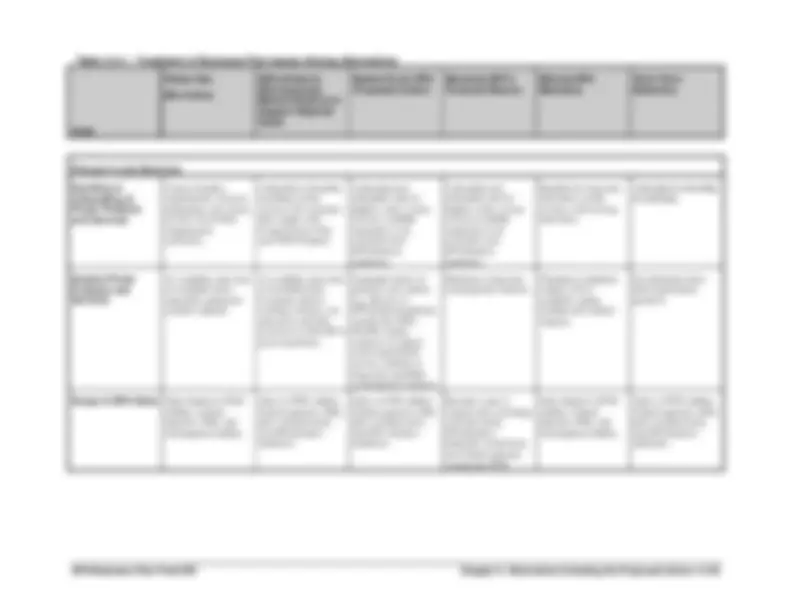

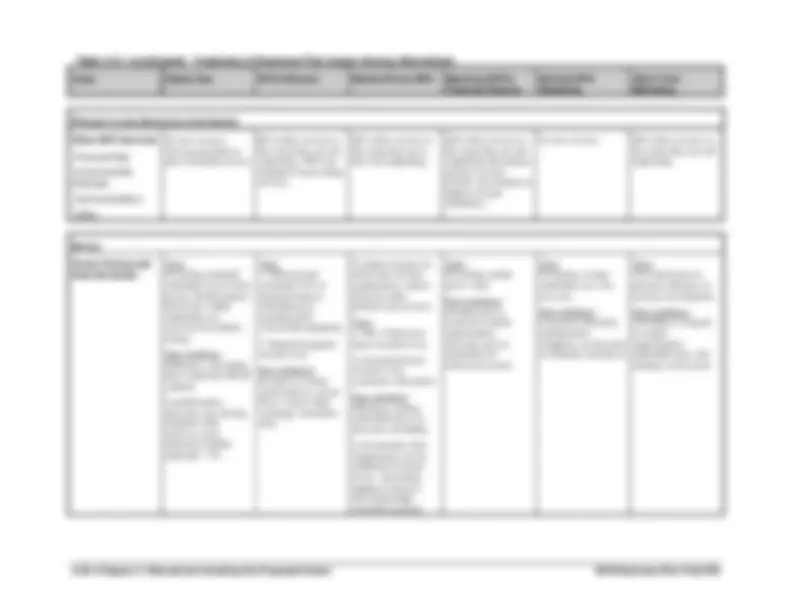

FIGURE S-

Framework for Environmental Impact Analysis

1994-1998 Biological Opinion (2d)

Detailed Fishery Operating Plan (DFOP)

Hydro Operations Scenarios

I S S U E S Products and Services Rates Energy Resources Transmission Fish & Wildlife Administration

A L T E R N A T I V E S Status Quo (No Action) BPA Influence Market Driven Ma ximize Financial Returns Minimal BPA Short-Term Marketing

Changes in:

- Resource mix

- Resource amount

- Operation of existing resources

- Transmission types . (^) 230-kV vs 500-kV . (^) BPA vs non-BPA

- Transmission system operations, maintenance, and replacement priorities

- Consumer behavior . (^) energy efficiency . (^) retail fuel switching . (^) reductions in use

Evaluate difference in impacts from changes in market responses due to how loads are met by BPA and others

M A R K E T R E S P O N S E

Resource Development Resource Operations Transmission Development/Operations Consumer Behavior

Modules: (Possib le variations) Fish & Wildlife Rates DSI Service Conservation/Renewables

BPA Response Strategies (To the extent needed when BPA’s costs exceed its maximum sustainable revenue level)

Air Land Water

E N V I R O N M E N T A L I M P A C T

FIGURE S-

Framework for Environmental Impact Analysis

1994-1998 Biological Opinion (2d)

Detailed Fishery Operating Plan (DFOP)

Hydro Operations Scenarios

I S S U E S Products and Services Rates Energy Resources Transmission Fish & Wildlife Administration

A L T E R N A T I V E S Status Quo (No Action) BPA Influence Market Driven Ma ximize Financial Returns Minimal BPA Short-Term Marketing

Changes in:

- Resource mix

- Resource amount

- Operation of existing resources

- Transmission types . (^) 230-kV vs 500-kV . (^) BPA vs non-BPA

- Transmission system operations, maintenance, and replacement priorities

- Consumer behavior . (^) energy efficiency . (^) retail fuel switching . (^) reductions in use

Evaluate difference in impacts from changes in market responses due to how loads are met by BPA and others

M A R K E T R E S P O N S E

Resource Development Resource Operations Transmission Development/Operations Consumer Behavior

Modules: (Possib le variations) Fish & Wildlife Rates DSI Service Conservation/Renewables

BPA Response Strategies (To the extent needed when BPA’s costs exceed its maximum sustainable revenue level)

Air Land Water

E N V I R O N M E N T A L I M P A C T

Air Land Water

E N V I R O N M E N T A L I M P A C T

S-4 • Summary Summary

BPA Business Plan Final EIS Summary • S-

Maximize BPA’s Financial Returns. Under this alternative, BPA would operate more like a private, for- profit business. It would focus on limiting costs and investing its money where it can get the best return, while continuing to fulfill the requirements of the Northwest Power Act and other organic statutes (except that rates would not be limited to recovering its costs). This alternative emphasizes obtaining the highest net revenue for marketable products and minimizing costs for activities that do not produce revenue. Minimal BPA Marketing. Under this alternative, BPA would not acquire new power resources or plan to serve customers’ load growth. Activities would focus on meeting revenue requirements through the long-term allocation of current Federal system capability, while continuing to fulfill other requirements of the Northwest Power Act. Short-Term Marketing. In this alternative, BPA would emphasize short-term (5 years or less) marketing of power and transmission products and services to be responsive to the market over 5 years or less, while continuing to fulfill the requirements of the Northwest Power Act.

Changes in Hydro Operations [Section 4.3.4]

This FEIS does not address decisions about how the Columbia River system is operated. That task falls to the System Operations Review (SOR), which runs concurrently with the Business Plan EIS process. BPA’s Business Plan alternatives would all occur within any hydro system operations constraints established by the SOR process. However, because it appears likely that current operations of the river system may change as a consequence of the SOR process, this FEIS has selected two SOR System Operating Strategies (SOSs) as “endpoints” for the potential range of impacts on business decisions.

- 1994-1998 Biological Opinion. This strategy represents river operations continued as at the time when the Draft SOR EIS was being developed (Summer 1994) to meet a variety of needs (e.g., fish and wildlife, flood control, irrigation, navigation, power, and recreation.). Under this SOS, power production would continue with little or no change to rates, availability of power, and so on. Of the likely SOR alternatives, this SOS would mean the least fish-related costs for power production.

- Detailed Fishery Operating Plan. The second SOS represents an operation to increase flow augmentation and spill, with the goal of assisting anadromous fish migration. Under this SOS, firm power production would lessen, and power to meet Northwest needs would have to be obtained by other means—building more generating sources and/or buying power from elsewhere. The increased power costs to BPA from power purchases to replace lost firm hydro capability would raise BPA’s total annual costs substantially.

Cumulative Market Responses and Environmental

Impacts of the Alternatives [Section 4.4]

Each set of proposed policies under the alternatives would cause BPA’s customers (or the retail consumers they serve) to react. These reactions, or market responses, would determine the possible environmental impacts of BPA’s actions within the region. Market responses can be sorted into four types:

- Resource development

- Resource operation

- Transmission development and operation

- Consumer behavior.

BPA Business Plan Final EIS Summary • S-

Response Strategies [Section 2.5]

Finally, if BPA’s costs rise above the amount of revenue it can generate, the agency will run the risk of not being able to meet all its obligations, including repayment of its debt to the U.S. Treasury. BPA would then have to undertake response strategies to try to rebalance the equation and to avoid political intervention in response to missed Treasury payments. Such response strategies would fall into three categories:

- Increasing revenues (possible actions ranging from raising firm power rates to increasing sales of new products and services to selling assets);

- Reducing spending (for instance, by reducing spending on conservation incentives, generation, operations and maintenance, and/or fish and wildlife enhancement); and/or

- Transferring program and financial responsibilities or increasing cost sharing for BPA programs. The EIS lists a number of representative options. Table S-1 shows the kinds of strategies and the alternatives to which they might apply.

Comparison of the Alternatives[Section 2.6; Chapter 4]

This section summarizes and compares key characteristics of the alternatives analyzed at length in the FEIS. The policy direction provided by each of the alternatives leads to different market responses by BPA and its customers. From the market responses of the three identified customer segments (utility firm requirements customers, DSIs, and surplus and nonfirm-power customers within and outside the Pacific Northwest), BPA can identify the likely environmental impacts of the alternatives. Each type of market response causes different environmental effects. Figure S-2 summarizes the key characteristics, including the expected environmental effects of each alternative. Note that the environmental impacts of all alternatives would be within a fairly narrow band, and several of the key impacts are virtually identical across alternatives. In addition, the costs of environmental externalities (in this case, the costs of air impacts not included in the direct costs of the action) would differ only slightly. Although environmentally preferable alternatives—Status Quo and BPA Influence—were identified, the distinctions among alternatives are small. Adoption of either of these alternatives would weaken BPA’s ability to achieve the purposes for action described above.

Comparison Under SOR 1994-1998 Biological Opinion Hydro

Operation

Status Quo. Under this alternative, BPA would offer to renew existing contracts with utilities and DSIs on terms comparable to those of current contracts. BPA would also renew existing rate designs, including the Variable Industrial Rate for DSIs. BPA would not respond to the availability of competitively priced alternatives to BPA power. BPA would lose load based on customers' expectations about BPA pricing, but would continue to acquire resources according to plans now in place. However, because of changes in the wholesale power market, BPA might terminate those resources that were no longer cost-effective. As a result, BPA would acquire more new generating and conservation resources than under all other alternatives, creating a substantial resource surplus as utility and DSI customers turn to other sources of competitively priced power. Overall, the region would acquire more resources than under any other alternative. BPA would use part of its surplus to exercise the “in-lieu” provisions of the Residential Exchange Program; that is, rather than nominally exchanging BPA power at the PF rate with power from investor-owned utilities (IOUs) at their average system cost in a purely accounting transaction, BPA would actually deliver power to serve a portion of the exchange load.

S-8 • Summary Summary

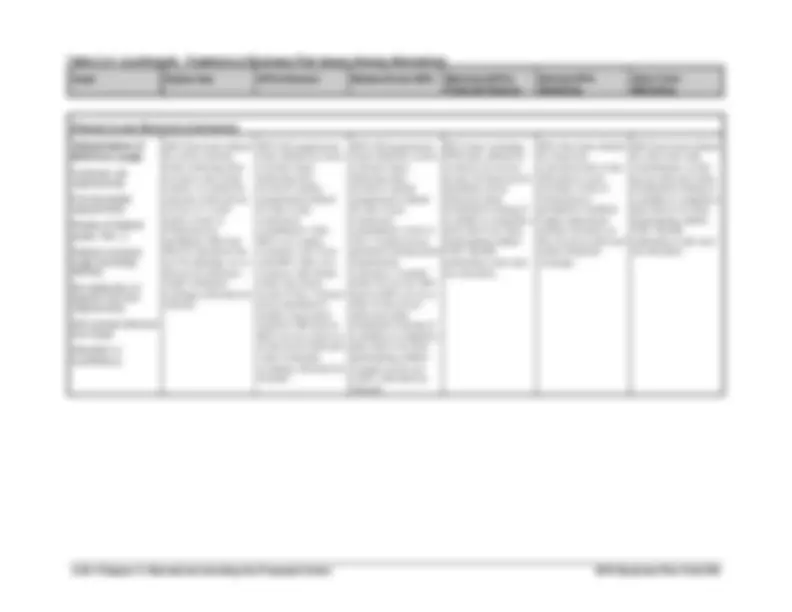

Table S-1: Applicability of Response Strategies to Alternatives

ALTERNATIVES

REPRESENTATIVE STRATEGIES Status Quo

BPA Infl.

Market- Driven

Max. Fin. Returns

Min. BPA

Short- Term Increase Revenues Raise firm power rates (^) —— —— Y (^) —— Y Y Raise transmission rates to cover other power system costs

N N N Y N N

Increase unbundled products & services revenues

N Y Y (^) —— N Y

Increase sales of new products & services N Y Y (^) —— N Y Implement a stranded investment charge (^) N Y N Y N N Increase seasonal storage Y Y Y Y Y Y Optimize hydro operations for net revenues (^) —— Y Y (^) —— N Y Increase extraregional sales revenues Y Y Y (^) —— N Y Increase joint venture revenues Y Y Y (^) —— N Y Sell assets N N N N Y N Decrease Spending Eliminate power purchases N N N N (^) —— N Reduce BPA spending on corporate overhead

Y (^) —— —— —— —— ——

Reduce WNP-1, -2, & -3 spending N Y Y Y Y Y Reduce conservation incentive spending (^) N N (^) —— —— —— N Reduce generation acquisition spending N Y Y (^) —— —— Y Reduce pollution prevention & abatement spending

N Y Y (^) —— —— Y

Reduce fish & wildlife spending N N N (^) —— —— N Reduce transmission construction spending N Y Y (^) —— —— Y Sell capacity ownership in new facilities Y Y Y Y (^) —— Y Reduce operations & maintenance spending

N Y Y (^) —— —— Y

Shift from revenue to debt financing (^) —— N N N (^) —— N Increase Treasury borrowing limits Y Y Y Y (^) —— N Lower probability of making Treasury payments

Y Y Y Y Y Y

Transfer Costs Seek 4(h)(10)(C) credit for fish & wildlife costs

Y Y Y Y Y Y

Increase cost sharing for BPA programs (^) N Y Y (^) —— —— Y Reallocate FBS costs & debt between power & non-power

—— —— —— —— —— ——

Secure appropriations for BPA’s costs N Y Y Y Y Y Transfer program & financial responsibility N N Y (^) —— —— Y

Y = Consistent with the concept of this alternative under current marketing environment. N = Inconsistent with the concept of this alternative under current marketing environment. -- = No change because it provides no mitigation value for the alternative even if consistent, or because all of the benefit of the response strategy has already been attained under this alternative.

S-10 • Summary Summary

Air quality emissions and water consumption would be associated primarily with the operation of existing coal plants, the DSIs, new and existing CTs, and fuel switching. This alternative would have slightly lower air quality impacts overall than other alternatives (except for BPA Influence), because the surplus resources would be used in part to displace higher-cost and higher-emission thermal resources such as coal plants. While this alternative shows more CT acquisitions than other alternatives, because CT emissions would be lower than coal, overall, emissions would be reduced. Land use impacts would result primarily from transmission development, which would be slightly higher in this alternative than under most others because BPA would continue its regional role of developing highly reliable transmission facilities based on regional one-utility planning. (See figure S-2.) Nonetheless, overall, land use impacts would be comparable to those of other alternatives, except BPA Influence. Regional employment growth under this and all other alternatives is likely to change little through 2002. The costs of environmental externalities would be slightly lower for Status Quo than for most other alternatives (excepting BPA Influence), because although more CTs would be developed regionally than under other alternatives, BPA’s hydro surplus would effectively displace older, more expensive thermal resources. Overall, it appears that Status Quo and BPA Influence alternatives (which have closely comparable levels of impacts) have the fewest environmental impacts, although environmental impacts would generally be similar among all alternatives. BPA Exercises Market Influence to Support Regional Goals. BPA would make the same program expenditures as under Status Quo. In addition to fully funding conservation, BPA would provide incentives for the development of additional renewable resources, maximize its own acquisition of renewable resources, and offer a “Green” Firm Power to customers who would prefer to buy power produced by renewable resources and who are willing to pay the higher cost of such resources. Because DSIs would be offered firm service in the spring only, about two-thirds of the DSI firm load would be served by other suppliers. BPA utility customers would be offered power at rates that varied with historical streamflow on the Columbia River system. Rates would be tiered: Tier 1 size would be based on a fixed percentage of Federal Base System firm capability, calculated on a monthly basis to reflect streamflows. The irrigation discount for farmers who use electricity for irrigation or drainage would be eliminated. BPA would reduce its resource acquisitions slightly compared with Status Quo, but would still have significant amounts of surplus firm power. Part of the surplus would be used to serve “in-lieu” loads of IOUs that participate in the Residential Exchange Program. Compared with Status Quo, regional resource development would be only slightly less, as would the regional impacts associated with new generation and transmission resource development. Existing CT operations would be about the same, but operations of newer CTs would be slightly lower. Overall, total environmental impacts would be comparable to those under Status Quo, and environmental externalities costs would be very slightly less. However, land use would be slightly higher than under other alternatives, because more renewable resources would be acquired, and renewable resources (wind and geothermal) are somewhat more land-intensive than other generating resources. Market-Driven BPA -Proposed Action. BPA would cut costs and, in the long term, would implement tiered rates, with the amount of power under each rate varying by season to reflect overall resource availability. The irrigation discount would be eliminated. DSIs would be offered firm service, but the amount of firm service would decline gradually over time. BPA would offer a “Green” Firm Power product to those utilities who desire it (but because this product covers its own costs, it would be revenue-neutral to BPA). In the long term, tiered rates would stimulate price-induced fuel-switching and conservation independent of BPA programs. Expected BPA prices would be lower due to reductions in costs of energy conservation, transmission system development, and BPA’s internal administrative activities. BPA would reduce its resource acquisitions and eliminate the surplus that exists under Status Quo. Less new CT construction and operation and increased operation of existing generation would result in increased impacts of existing thermal generation compared to the Status Quo or BPA Influence alternatives. The higher emissions levels of those older, less efficient thermal resources would result in higher levels of air emissions and water use from power generation under the Market-Driven alternative than under the Status Quo or BPA Influence alternatives. Environmental externality costs associated with air emissions of new and

BPA Business Plan Final EIS Summary • S-

existing thermal generation would be slightly higher than under Status Quo, again primarily because of higher amounts of existing thermal (especially coal) operation. Maximize BPA’s Financial Returns. BPA would cut costs and sell all firm power at just below market price, resulting in increased revenues. Expected BPA costs would be slightly lower due to reduced costs of conservation, generation, transmission system development, and administration compared to Status Quo. The PF rate would be capped at the maximum sustainable revenue point, and so might average slightly below the average Priority Firm Power (PF) rate in the Market-Driven alternative. Lower prices would retain and in some cases increase loads, eliminating any potential BPA firm surplus, and requiring increased power purchases to meet load. In this alternative, BPA would acquire fewer new resources than under the Status Quo, and the agency would rely more on power purchases to serve new load. Other utilities would also acquire fewer new resources, and, as a result, regional resource acquisition and associated land use, air, and water impacts would be less than under other alternatives. Land use associated with new transmission development would be slightly greater than under all other alternatives, in part because BPA would build intertie lines to capture new load where financially attractive, and would construct less transmission for regional needs. Other utilities would build regional transmission instead of BPA, but would do so at lower voltages (requiring more miles of transmission right-of-way to serve loads). Nonetheless, land use impacts would be comparable to those of other alternatives. Increased operations of existing thermal generation, both to continue serving regional loads and to replace energy conservation programs, would result in increased impacts of those generators compared to the Status Quo or BPA Influence alternatives. Because this alternative involves a high level of power purchases, it is likely that much of the thermal generation would occur outside the region (e.g., in the Pacific Southwest)). The primary influence on air quality impacts would be the high existing coal operations under this alternative, which are higher than all others. As a result, environmental externality estimates for air quality impacts of this alternative would be higher than under any other alternative except Minimal BPA. Minimal BPA Marketing. BPA would cut costs and eliminate all resource acquisitions recommended in the 1992 Resource Program, including conservation, that are not already under way. Without the added costs of new resource acquisitions and transmission construction, BPA’s rates would remain low, but the limited supply of BPA power would force customers to acquire resources elsewhere to serve their load growth. Expected BPA prices would be lower due to reductions in costs of resource acquisitions, transmission system development, and internal administration. Because BPA would sell all of its limited supply of firm power, there would be no BPA firm surplus. The rest of the region would develop resources at market prices to serve load growth (predominately CTs, but also some conservation). Existing and new thermal generation would operate more than under other alternatives, in part because the amount of energy conservation developed in the region would be lower than under any of the other alternatives. Existing less efficient and less clean thermal resources would be operated more often than under Status Quo, and, as load growth occurred, additional new thermal resources (probably CTs) would be added. Consequently, air quality impacts and water use would be higher than under other alternatives. Environmental externality estimates for air quality impacts of this alternative would be higher than under all other alternatives (but still be only about 13 percent higher than under Status Quo). Short-Term Marketing. BPA would cut costs and eliminate new resource acquisitions and new energy conservation programs, unless they would be cost-effective in 5 years or less. Without the added costs of new resource acquisitions and transmission construction, BPA’s rates would remain low, but limiting BPA power to short-term sales would cause some customers to obtain their own supplies. As a result, BPA would be left with a modest surplus, which it would use to serve “in-lieu” loads of IOUs that participate in the Residential Exchange Program. Expected BPA prices would be lower due to reductions in costs of conservation, transmission system development, and internal administration. The rest of the region, including generating publics, would develop resources at market prices to serve long-term firm needs. Under this alternative, BPA would acquire fewer conservation and generation resources than under Status Quo. The impacts on air and water from the operation of new and exiting resources would be higher than under Status Quo, primarily because of increased operation of existing, less clean and efficient thermal

BPA Business Plan Final EIS Summary • S-

that will tend to discourage customers from maintaining loads on BPA and cause them to look elsewhere for power. The three fish and wildlife modules are discussed below. Status Quo (FW-1). BPA would continue to fund fish and wildlife measures without systematically requiring demonstrated effectiveness. Continuing current fish and wildlife administrative policies (funding of virtually all program measures, unlimited expenditures, and little consideration of BPA’s other missions) would be most likely to keep fish and wildlife costs unstable and unpredictable. Customers would be likely to seek power supplies elsewhere, potentially increasing impacts from CTs and thermal generation. Under the worst case, BPA’s revenues could no longer support funding of all necessary fish and wildlife measures. BPA-Proposed Fish and Wildlife Reinvention (FW-2). BPA would work with other entities to set priorities for funding and to monitor results; establish multi-year, base-level funding agreements keyed to BPA maximum sustainable revenues; establish a gain-sharing trust for excess revenues; and use gain-sharing to fund additional activities. With consultation, monitoring of results, and additional controls, BPA customers could be more confident of future fish and wildlife costs. Environmental impacts would more closely resemble those under BPA’s resource acquisition choices. However, if monitoring showed poor results, more funding might be required, with results similar to those under FW-1. Lump-Sum Transfer (FW-3). BPA would transfer control for implementing fish and wildlife actions to fish/wildlife agencies and Tribes via trusts or lump-sum transfers. This module might require Federal legislation. Adjustments would be limited to review or renewal opportunities provided in the trust or transfer agreement. With funding priorities and monitoring assigned to other entities, cost stability would increase unless lack of results pressured BPA to increase funding levels despite prior funding agreements. BPA accountability would decrease.

S-14 • Summary Summary

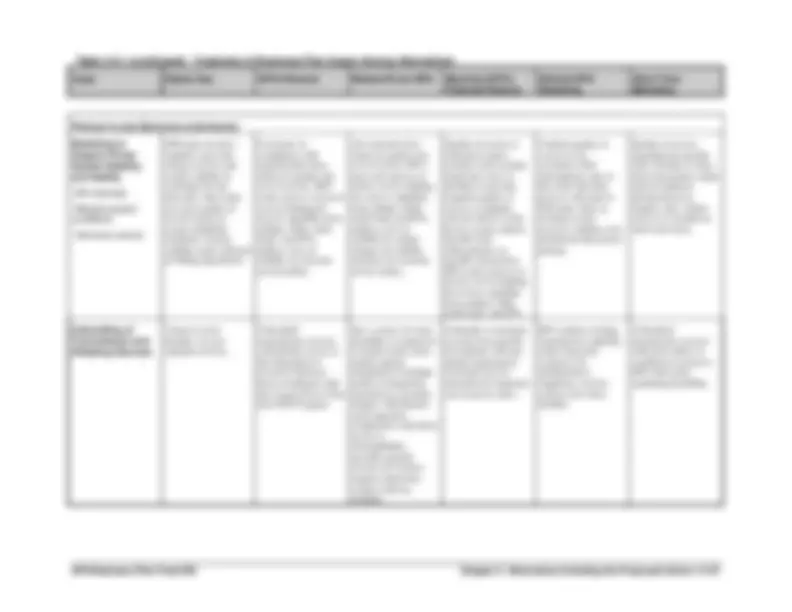

Table S-2: Analytical Modules in the Business Plan Final EIS

Alternatives

Module Description

1. Status Quo

2. BPA Influence

3. Market- Driven

4. Maximize Financial Returns

5. Minimal BPA

6. Short-Term Marketing

FW-1 Status Quo I V V V V V FW-2 BPA-Proposed Fish and Wildlife Reinvention

-- I I V V I

FW-3 Lump-Sum Transfer -- V V I I V

RD-1 Seasonal Rates - Three Periods -- V I V V V RD-2 Streamflow Seasonal Rates - Real Time

-- V V V V V

RD-3 Streamflow Seasonal Rates - Historical

-- I V V V V

RD-4 Eliminate Irrigation Discount -- I I I V I RD-5 Variable Industrial Rate I V V V V V RD-6 Load-Based Tier 1 --^ V^ I V^ --^ V RD-7 Resource-Based Tier 1 -- I V V -- V RD-8 Market-Based Tier 2 -- V V V -- I

DSI-1 Renew Existing Firm Contracts I V V V -- -- DSI-2 Firm Service in Spring Only -- I V V V V DSI-3 Declining Firm Service -- V I V I I DSI-4 No New Firm Power Sales Contracts

-- V V V V V

DSI-5 100-Percent Firm Service -- V V I -- V

CR-1 “Fully Funded” Conservation I I V V -- V CR-2 Renewables Incentives -- I V V -- V CR-3 Maximize Renewables Acquisition

-- I V V -- V

CR-4 “Green” Firm Power -- I I I -- V

I = Intrinsic V = Variable -- = Not Applicable Mutually exclusive: All FW modules; RD-1, -2, and -3; RD-6, -7, and -8; DSI-1 with -2 and -3; DSI-4 with all DSI modules.

Rate Design

Seasonal Rates - Three Periods (RD-1). BPA power rates for utility customers would have three seasonal periods of 3 to 5 months each, to achieve a closer seasonal linkage between BPA’s wholesale power rates and the market price of power. There would be a possible seasonal load loss from the generating publics during the high-rate periods; however, there would be slight overall load effects of implementing this module. BPA rates and market prices would be more closely matched, and costs would be shifted among various BPA customers. The primary environmental impacts would stem from utility and DSI decisions about whether and when to place load on BPA given the seasonal rates. During periods when they did not place load on BPA, these customers would likely rely on power purchases, probably supported by existing thermal generation or CTs. The extent to which customers place more load onto BPA in low-rate periods and less in high-rate periods would depend on the extent to which rates vary by period compared to the rates for alternative power supplies during those same periods. Streamflow Seasonal Rates - Real Time (RD-2). BPA power rates would change monthly, based on projected current-year streamflows. This would present BPA’s customers with substantial rate uncertainty.

S-16 • Summary Summary

Market-Based Tier 2 (RD-8). BPA would set the Tier 2 rate slightly below the price of long-term power or the cost of alternative resources that existing customers could purchase for use as an alternative to BPA power; Tier 1 might absorb Tier 2 costs. This module would help BPA to maintain competitive prices for Tier 2 sales even when Tier 2 costs were above the market price, by supporting Tier 2 sales with Tier 1 revenues. Conversely, Tier 2 sales at the market price could reduce Tier 1 rates if Tier 2 costs were below the market price. When the market price is falling, this module would add to uncertainty of Tier 1 prices and increase loss of BPA utility firm loads.

Direct Service Industries Services/Rates

Renew Existing DSI Power Sales Contracts (DSI-1). In 2001, DSIs would be offered new power sales contracts that incorporate the major elements of current contracts. This module is intrinsic to Status Quo, and is assumed to lead to reductions in DSI load because of the unresolved issues between the DSIs and BPA regarding certain provisions of the existing contracts. Substituting this module under BPA Influence would increase the DSI load served by BPA, and would consequently decrease BPA’s firm surplus. BPA revenues would increase because BPA would retain a larger portion of DSI firm load and because the DSI rate would be higher than the nonfirm rates at which the surplus would most likely be sold. Under Market-Driven and Maximize Financial Returns, BPA revenues would decrease with decreases in DSI load as DSIs would reduce their BPA loads in response to the terms of the contracts; there might be some additional costs to BPA because of the need for additional reserves. Implementation of this and other DSI modules would affect only whether increased load is served by BPA or other sources. If the latter, more CTs would likely be developed and operated, with corresponding effects on water, land use, and air quality (from emissions). However, at certain times of the year, BPA might have surplus which could be used to displace higher-cost thermal resources (e.g., coal). Use of newer and relatively cleaner CTs and displacement of older thermal/coal resources might be a net positive impact on air quality. Firm DSI Power in Spring Only (DSI-2). DSIs would be offered firm service for all contracted load during the spring flow augmentation period; for the remainder of the year, load would be 100-percent interruptible after a specified notice period. Implementation of this module under any applicable alternative would lead to a major shift of DSI firm load away from BPA, reducing BPA’s revenues. Rates would rise. Environmental impacts would be similar to those described under DSI-1, as loads shifted to other suppliers that might rely more on CTs, with attendant impacts on air quality and land use. Declining Firm Service (DSI-3). The amount of firm service offered to DSIs from Tier 1 power would decline over time to maintain availability of Federal firm power to public agency preference customers. This module is intrinsic to the Market-Driven BPA, Minimal BPA, and Short-Term Marketing alternatives, and helps retain DSI loads, at least in the short-term. BPA revenues would increase under BPA Influence, due to higher DSI loads, because this module would replace the “Firm DSI Power in Spring Only” module that is otherwise assumed for this alternative. Under the Maximize Financial Returns alternative, DSI loads would not change substantially. Environmental impacts of DSI loads’ moving away from BPA would be as described above for DSI-1. No New Firm DSI Power Sales Contracts (DSI-4). When their current contracts expire in 2001, DSIs would not be offered any long-term contracts for firm power; any power DSIs purchased from BPA would be nonfirm. If BPA gave up this load, the large amount of power suddenly available would drive down the price of power, further reducing BPA revenues. The agency would also have to replace the reserves provided by the DSIs. BPA would probably be unable to meet its financial obligations under these conditions. Environmental impacts would be similar to those described above for DSI-1, but greater, due to larger firm load losses. 100-Percent Firm Service (DSI-5). BPA would serve all four quartiles of the DSI load as firm (non- interruptible) load. Under the BPA Influence alternative, BPA revenues would increase under this module because the DSI firm load would be large compared to spring-only firm service. Overall, BPA rates to other customer classes would decrease with increased revenues from DSI sales. Under Market-Driven BPA, DSI loads would remain close to the level of DSI loads that BPA assumed in the early years of DSI service in this alternative, but would not decline over time. This module is intrinsic to the Maximize Financial Returns alternative, and would lead to BPA continuing to serve most of its current DSI load. Under Short-Term

BPA Business Plan Final EIS Summary • S-

Marketing, BPA’s DSI loads would increase somewhat. Environmental impacts would result from the fact that there would be less development of new generation and more operation of existing thermal resources when BPA serves more DSI load.

Conservation/Renewable Resources

“Fully Funded” Conservation (CR-1). BPA would fund conservation at total spending levels comparable to those under Status Quo. The annual increase in BPA costs would be $90 million or more per year. Under the Market-Driven, Maximize Financial Returns, and Short-Term Marketing alternatives , the increased PF rate due to these costs would lead to higher load loss among BPA preference and DSI customers. Increased conservation acquisition would likely reduce BPA’s and the region’s acquisition of CTs and/or cogeneration, consequently slightly reducing the associated land use, water, and air quality impacts. The magnitude of such positive impacts would depend on how much total conservation were acquired by BPA and other utilities. Renewable Resources Incentives (CR-2). BPA would offer price incentives or discounts to renewable resource proposals to stimulate development of the market transformation potential of renewable resources (especially wind/geothermal). Given the current market prices for power, it appears unlikely that this module would lead to substantial increases in the amount of renewable resources developed in the region; even with a 10 percent incentive, renewable resources are predicted to cost substantially more than the market price for power. Maximize Renewables Acquisitions (CR-3). BPA would acquire a significant portion of available commercial renewable resources, even at prices above the competitive price of non-renewable resources. These would tend to replace natural-gas-fired CTs or short-term power purchases in BPA’s resource portfolio. BPA would develop a firm surplus as a consequence. BPA’s revenue requirement would increase, leading to rate increases and revenue losses as load moves off BPA to be served by other sources. Environmental effects, as above, would depend on the incremental amount of renewable resources acquired under each alternative; generally, acquiring renewable resources instead of CTs at short-term power purchases would reduce air emissions and water use, but slightly increase land use impacts. “Green” Firm Power (CR-4). BPA would offer power from renewable resources at cost, including services comparable to those included in Tier 2 power. The amount of “Green” Firm Power that BPA would offer would depend on the willingness of a group of BPA customers to commit to purchase the output for the economic life of the resources. By developing this module, BPA would not need to acquire a similar amount of CTs and/or power purchases. However, “Green” Firm Power could help reduce the load BPA loses to other suppliers by offering customers a more environmentally benign resource pool, which some customers may want to acquire to serve load growth. This module would be revenue-neutral because BPA would acquire these resources only in an amount equal to the commitments made by its customers for “Green” Firm Power. Environmental impacts would change as described above as CTs are replaced with renewable resources.

Summary of Key Factors That May Limit Implementation

The projected outcomes of alternatives as described in the EIS assume that all the alternative approaches could be implemented and would be generally accepted. However, some factors may be beyond BPA’s control. Figure S-3 provides a “reality check” of the likelihood that the alternatives and associated environmental impacts would be realized.