Download Calculating - Asset Managment - Lecture Slides and more Slides Management Fundamentals in PDF only on Docsity!

Calculating the U.S. Dollar Equivalentof the Maturing AUD GovernmentBond when Covered

Assume:

A 1 year Australian Government Bond with a par value of1,000AUD (assume you purchased 100 of these at par)

Assume an annual coupon of 5.5% (payable at the end ofthe year)

Assume the following market maker bank quoted exchangerates:

AUD/USD spot

AUD/USD 1 year forward

Calculate the USD covered amount when the bondmatures:______________________

Answer: U.S. Dollar Equivalent of theMaturing AUD Government Bond

Amount of AUD to be received in 1 year frommaturing bonds: Par value = AUD1,000 x 100 = AUD100, Interest (5.5% coupon) = 100,000 x 0.055 = AUD5, Total received = AUD105,500 (to be sold forward)

Exchange rates:

AUD/USD spot

AUD/USD 1 year forward

USD covered amount (to be received in 1 year)= AUD105,500 x 0.9650 = USD101,807.

Calculating the Covered Return

Answer: Calculate the yield to maturity on the investment whencovered.

Note: Yield to Maturity is the internal rate of return (IRR), or thediscount rate that sets the present value of the future cashinflow to the price of the investment,

So given: AUD/USD spot 1.0005/1. AUD/USD 1 year forward 0.9650/0.

USD Purchase Price = AUD100,000 x 1.0009 = USD100,

USD Hedged Equivalent Cash Inflow in 1 year = AUD105,500 x0.9650 = USD101,807.

Solve for the IRR (k): -100,090 = 101,807.50/(1+k)

http://www.datadynamica.com/IRR.asp

k = 1.72% (Why is this different from the 5.5%)

Answer: Because AUD is selling at a 1 year forward discount.

Another Example of a CoveredReturn Assume the following:

A 1 year Japanese Government Bond with acoupon of 1%.

Par value of 100,000 yen and selling at par.

Exchange Rates:

USD/JPY spot:

1 year forward:

Calculate the covered return for a U.S.investor on the above JGB

Covered Interest Arbitrage

Covered interest “arbitrage” is a situation thatoccurs when a covered return offers a higherreturn than that in the investor’s home market. As an example assume: 1 year interest rate in U.S. is 4% 1 year interest rate in Australia is 7% AUD 1 year forward rate is quoted at a discount of 2%. In this case, a U.S. investor could invest inAustralia and Cover (sell Australian dollars forward) and earn acovered return of 5% (7% - 2%) which is 100 basispoints greater than the U.S. return This is covered interest arbitrage: earning more(when covering) than the rate at home.

Explanation for Covered InterestArbitrage Opportunities Covered interest arbitrage will exist whenever thequoted forward exchange rate is not pricedcorrectly. If the forward rate is priced correctly, coveredinterest arbitrage should not exist. Going back to our original example:

(1) Invest in a U.S. government bond and earn2.0%.

(2) Invest in an Australian government bond andearn 5.5%

If the AUD 1 year forward were quoted at adiscount of 3.5%, then the covered return (2%)and the home return (2%) would be equal.

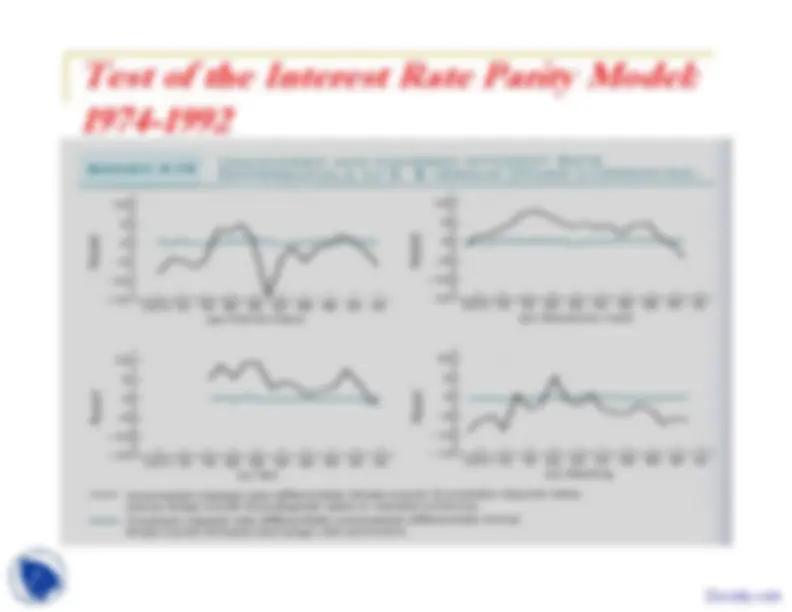

- Test of the Interest Rate Parity Model:1974-