© Correia, Flynn,

Uliana & Wormald

Further

Further

Issues in

Issues in

Capital

Capital

Budgeting

Budgeting

CHAPTER 9

CHAPTER 9

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

These are the slide from the new version of Drury.

Typology: Lecture notes

1 / 21

This page cannot be seen from the preview

Don't miss anything!

© Correia, Flynn, Uliana & Wormald

CHAPTER 9 CHAPTER 9

© Correia Flynn, Uliana, 2

© Correia Flynn, Uliana, 4

How do we choose between alternativesHow do we choose between alternatives with unequal economic lives?with unequal economic lives?

It may not be possible to compare NetIt may not be possible to compare Net Present Values.Present Values.

Need a universal measure to ensureNeed a universal measure to ensure comparability.comparability.

© Correia Flynn, Uliana, 5 (^) Projects with unequal livesProjects with unequal lives (^) Should we select Project Y with the higher NPV?Should we select Project Y with the higher NPV? (^) If there is an opportunity to reinvest in a similarIf there is an opportunity to reinvest in a similar project X in 3 years, then the NPV for Project Xproject X in 3 years, then the NPV for Project X will be:will be:

Project cash fows (Rm) 0 1 2 3 4 5 6 X -52 28 28 28 Y -80 25 25 25 25 25 25 NPV (X) 13. NPV (Y) 17. Project cash fows (Rm) 0 1 2 3 4 5 6 X (1) -52 28 28 28 X (2) -52 28 28 28 -52 28 28 -24 28 28 28 NPV (X) 21.

© Correia Flynn, Uliana, 7

We can convert capital costs into EquivalentWe can convert capital costs into Equivalent Annual costs.Annual costs. (^) Project X - 52m/2.3216 = 22.4mProject X - 52m/2.3216 = 22.4m (^) Project Y - 80m/3.8887 = 20.57mProject Y - 80m/3.8887 = 20.57m (^) If the annual cash flows were the same, Project YIf the annual cash flows were the same, Project Y would be selected as it minimises the annual costwould be selected as it minimises the annual cost of the investment.of the investment. (^) Further adjustments required for capital taxFurther adjustments required for capital tax allowances, which will reduce the real cost ofallowances, which will reduce the real cost of investments in fixed assets.investments in fixed assets.

© Correia Flynn, Uliana, 8

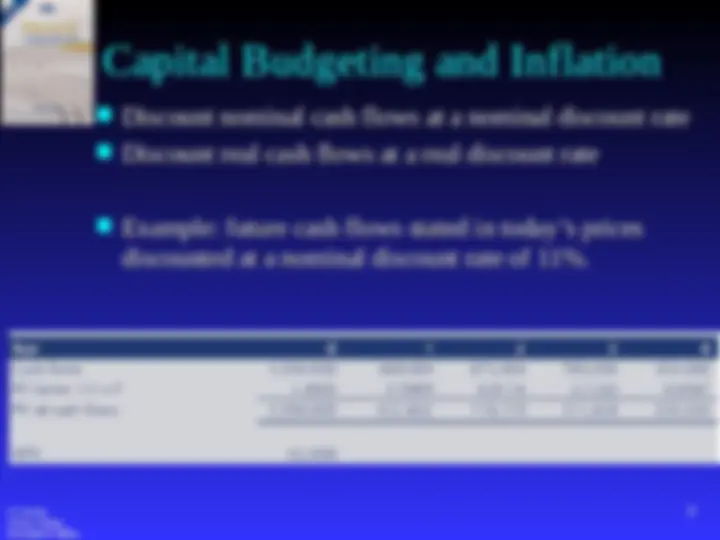

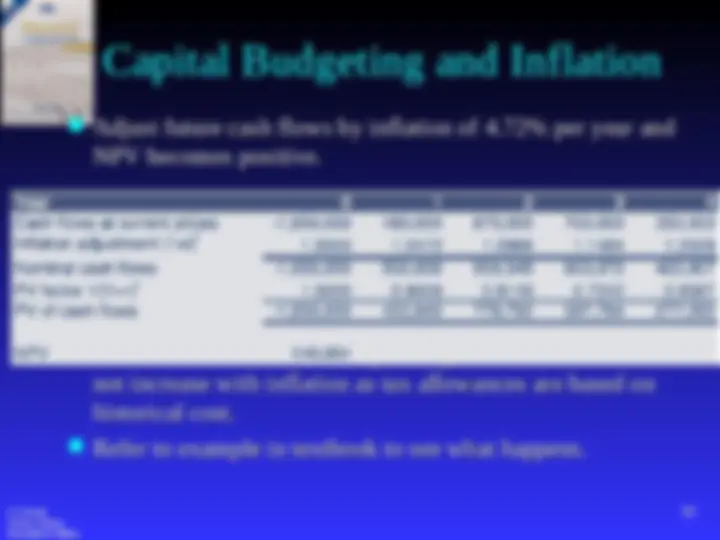

No adjustment for inflation may result inNo adjustment for inflation may result in material errors in capital budgeting decisions.material errors in capital budgeting decisions.

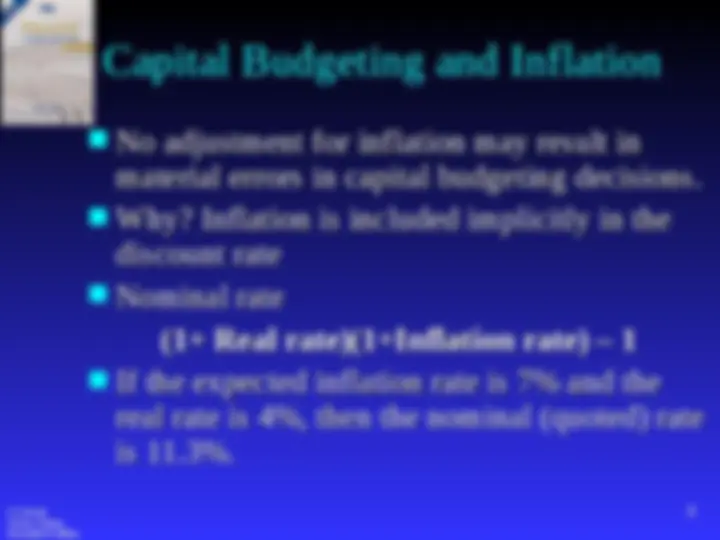

Why? Inflation is included implicitly in theWhy? Inflation is included implicitly in the discount ratediscount rate

Nominal rateNominal rate (1+ Real rate)(1+Inflation rate) – 1 (1+ Real rate)(1+Inflation rate) – 1

If the expected inflation rate is 7% and theIf the expected inflation rate is 7% and the real rate is 4%, then the nominal (quoted) ratereal rate is 4%, then the nominal (quoted) rate is 11.3%.is 11.3%.

© Correia Flynn, Uliana,

10

© Correia Flynn, Uliana,

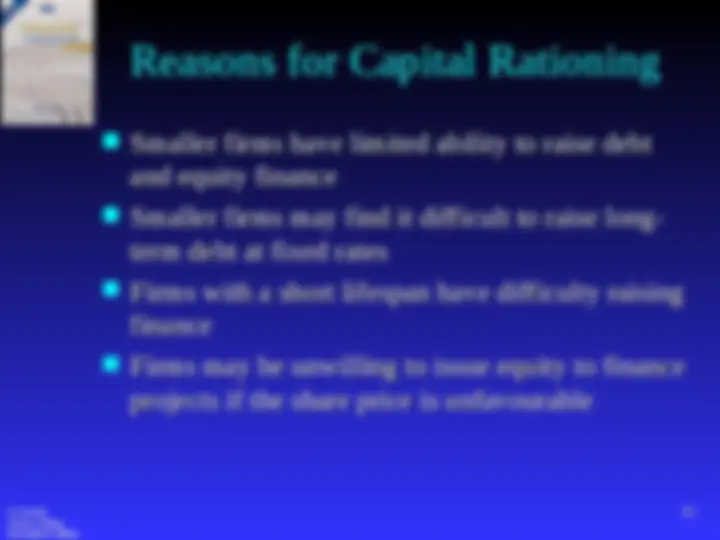

Used when a lack of capital prevents aUsed when a lack of capital prevents a company from selecting all positive NPVcompany from selecting all positive NPV projects.projects. 11

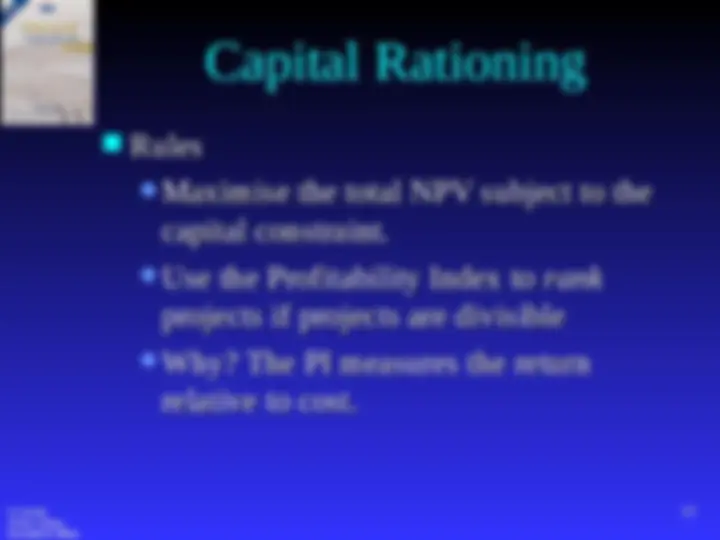

© Correia Flynn, Uliana, 13 Capital Rationing

RulesRules

Maximise the total NPV subject to theMaximise the total NPV subject to the capital constraint.capital constraint.

Use the Profitability Index toUse the Profitability Index to rankrank projects if projects are divisible projects if projects are divisible

Why? The PI measures the returnWhy? The PI measures the return relative to cost.relative to cost.

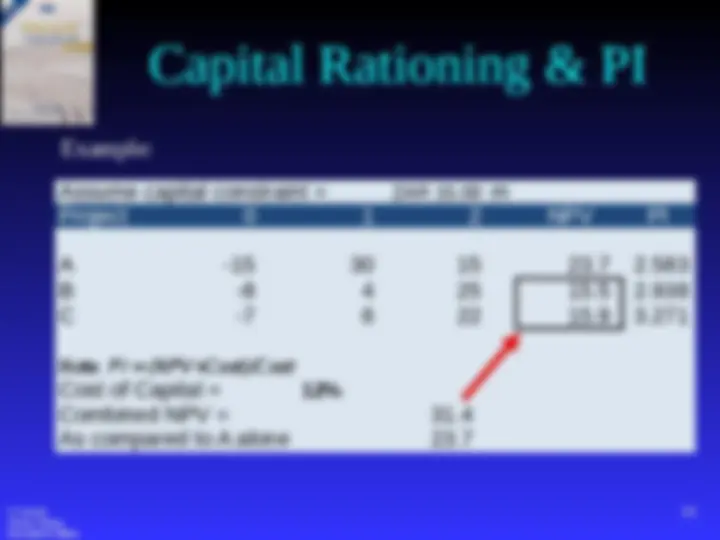

© Correia Flynn, Uliana, 14 Capital Rationing & PI

Assume capital constraint = ZAR 15. 00 m Project 0 1 2 NPV PI A -1 5 30 15 23.7 2. B -8 4 25 15.5 2. C -7 6 22 15.9 3.

Cost of Capital = 12% Combined NPV = 31. As compared to A alone 23.

© Correia Flynn, Uliana,

In order to manage capital rationing, firmsIn order to manage capital rationing, firms may set a hurdle rate that is higher than themay set a hurdle rate that is higher than the cost of capitalcost of capital

In figure 9.3, if we use a hurdle rate ofIn figure 9.3, if we use a hurdle rate of 20%, then only projects 1 and 2 would be20%, then only projects 1 and 2 would be acceptedaccepted

What the disadvantages with using a hurdleWhat the disadvantages with using a hurdle rate?rate? 16

© Correia Flynn, Uliana, 17 Assessed Tax Losses

Rm Rm

The tax loss should be set off against income from existing products. The effect on the new project is zero.

Year 1 2 Cash Flows 5.0 5. Tax - -1. 5 Tax -1. 5 5.0 2.

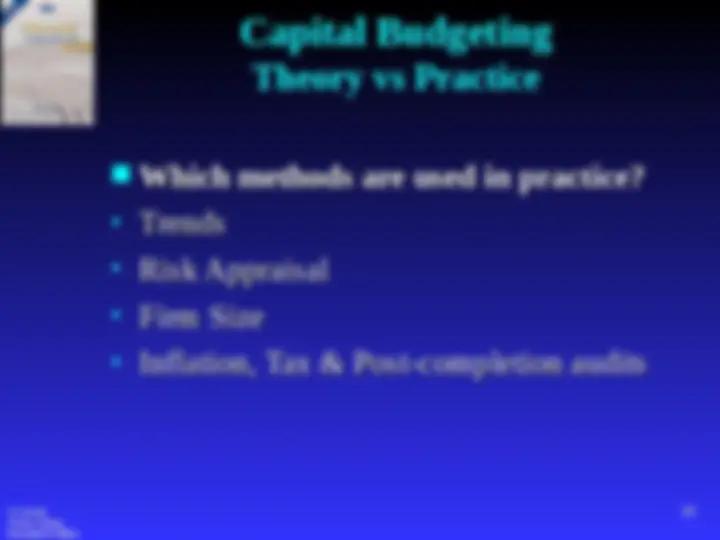

© Correia Flynn, Uliana, 19 Capital Budgeting Theory vs Practice

Which methods are used in practice?Which methods are used in practice?

TrendsTrends

Risk AppraisalRisk Appraisal

Firm SizeFirm Size

© Correia Flynn, Uliana,

20