Download Capital Budgeting Techniques: Investment Evaluation Criteria and more Summaries Finance in PDF only on Docsity!

CAPITAL BUDGETING UNDER CERTAINTY

Investment Evaluation Criteria A fundamental concept in investments is the time value of money. Firms are always confronted with opportunities to earn positive rates of return on their funds, either through investment in attractive projects or in interest bearing securities or deposits. Therefore, the timing of cash flows has important economies consequences, which financial managers explicitly recognize as the time value of money — the idea that there is a greater benefit to receiving a sum of money now, rather than an identical sum later.

Cash at a present time instead of that of a future date is preferred due to consideration of: 1.) Current cash has the potential to earn interest (Reward for money) 2.) Risk factors - Uncertainty of future cash flows. 3.) Inflation 4.) Macro-economic variables in future 5.) Availability of investment opportunities currently. 6.) Urgency of current consumption 7.)To take advantage of cash discounts.

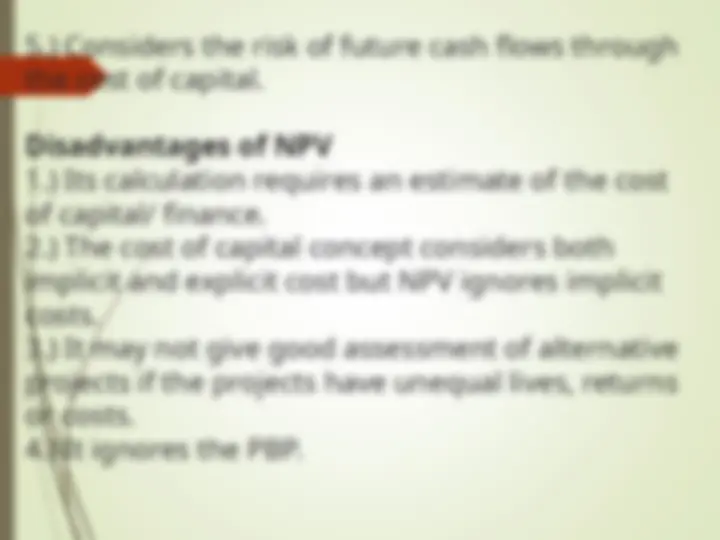

Difference between Discounted Cash Flows (DCF) & Non-Discounted Cash Flows (NDCF) 1.) DCFs have been adjusted to incorporate the time value of money, unlike NDCFs. 2.) DCFs are highly accurate as a result of consideration of time value of money unlike NDCFs that disregard of time value of money. 3.)When these two methods are used to evaluate an investment, the outcomes will be significantly different thus DCFs are preferably used in investment decisions due to the provision of financial reality check unlike the non-discounted techniques.

Capital Budgeting Techniques

1. Payback Period (PBP) The payback (PB) is one of the most popular and widely recognized traditional methods of evaluating investment proposals. Payback is the number of years required to recover the original cash outlay invested in a project. If the project generates constant annual cash inflows, the payback period can be computed by dividing cash outlay by the annual cash inflow. That is: PP = Initial Investment Cash flow per period

Illustration 2. Tujenge Limited invests Sh. 1,200,000 project XYZ that has an economic life span of 12 years with even expected annual returns of Ksh. 150,000. Determine the payback period of project XYZ. Illustration 2. Assume that a project requires an outlay of Ksh. 50,000 and yields annual cash inflow of Ksh. 12, for 7 years. Determine the payback period for the project. Illustration 2. Suppose that a project requires a cash outlay of Ksh. 20,000 and generates cash inflows of Ksh. 8,000, 7,000, 4,000 and 3,000 during the next 4 years. Determine the project’s payback

Advantages of Payback Period 1.) Simple to compute, use and understand. This has made it popular among executives especially traditional financial managers in ascertaining the viability of a venture. 2.) Provides a clue on the risk status of an investment. Ideal under high-risk investments because it will identify which venture will payback earlier to minimize risks with a venture. 3.) Aids in choosing mutually exclusive projects since it gives a clue as to which venture is viable if one considers the shortest PBP and the highest inflow of a venture.

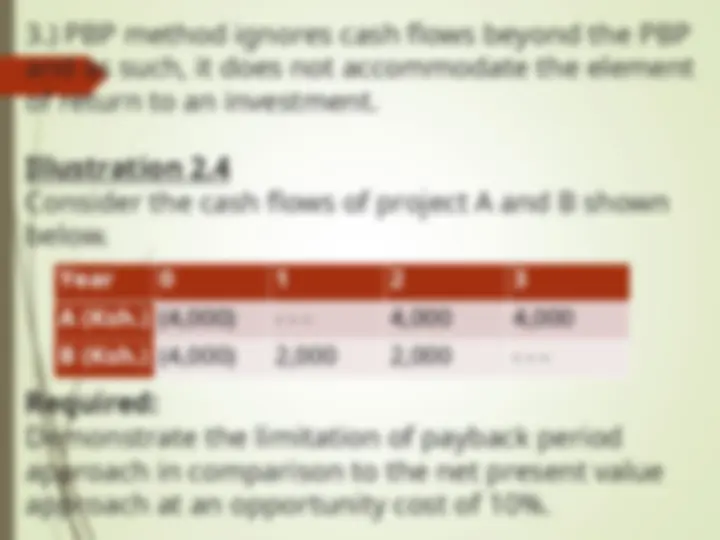

3.) PBP method ignores cash flows beyond the PBP and as such, it does not accommodate the element of return to an investment. Illustration 2. Consider the cash flows of project A and B shown below. Required: Demonstrate the limitation of payback period approach in comparison to the net present value approach at an opportunity cost of 10%. Year 0 1 2 3 A (Ksh.) (4,000) - - - 4,000 4, B (Ksh.) (4,000) 2,000 2,000 - - -

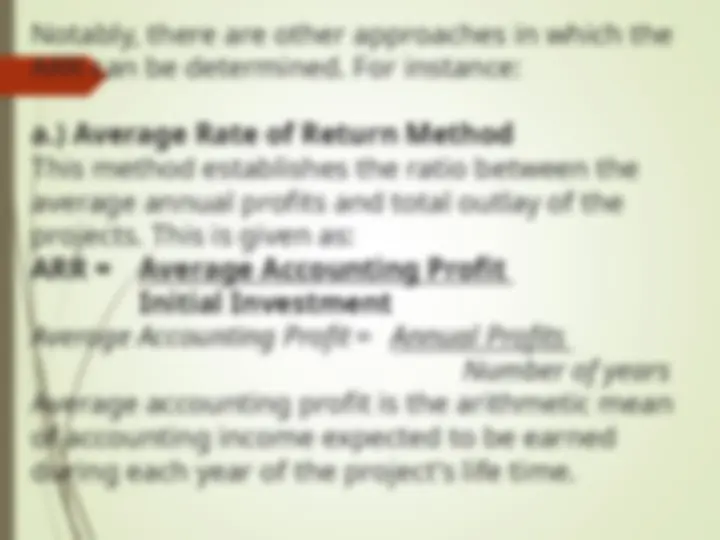

2. Accounting Rate of Return / Average Rate of Return (ARR) ARR can also be referred to as the Return on Investment (ROI). This measure uses accounting information, as revealed by financial statements, to measure the profitability of an investment. The accounting rate of return is the ratio of the average after tax profit divided by the average investment. The average investment would be equal to half of the original investment if it were depreciated constantly. Alternatively, it can be found out by dividing the total of the investment’s book values after depreciation by the life of the project.

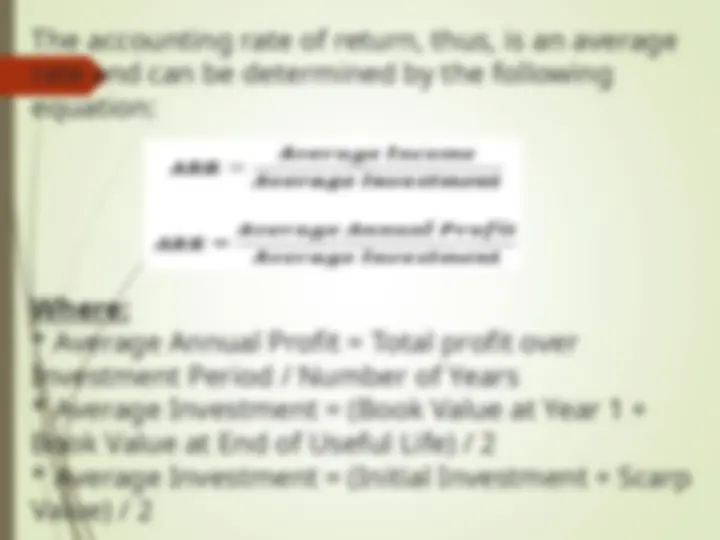

The accounting rate of return, thus, is an average rate and can be determined by the following equation: Where:

- Average Annual Profit = Total profit over Investment Period / Number of Years

- Average Investment = (Book Value at Year 1 + Book Value at End of Useful Life) / 2

- Average Investment = (Initial Investment + Scarp Value) / 2

b.) Earnings per unit of Money Invested This method establishes the ratio between the total net earnings and total investment. This is given as: ARR = Total Earnings Total Outlay Acceptance Rule for ARR As an accept-or-reject criterion, this method will accept all those projects whose ARR is higher than the minimum rate established by the management and reject those projects which have ARR less than the minimum rate.

Advantages of Accounting Rate of Return 1.) The ARR method is simple to understand and use. It does not involve complicated computations. 2.) Like payback period, this method of investment appraisal is easy to calculate. 3.) It recognizes the profitability factor of investment. The ARR rule incorporates the entire stream of income in calculating the project’s profitability. 4.) ARR can be readily calculated from the accounting data; unlike in the NPV and IRR methods, no adjustments are required to arrive at cash flows of the project.

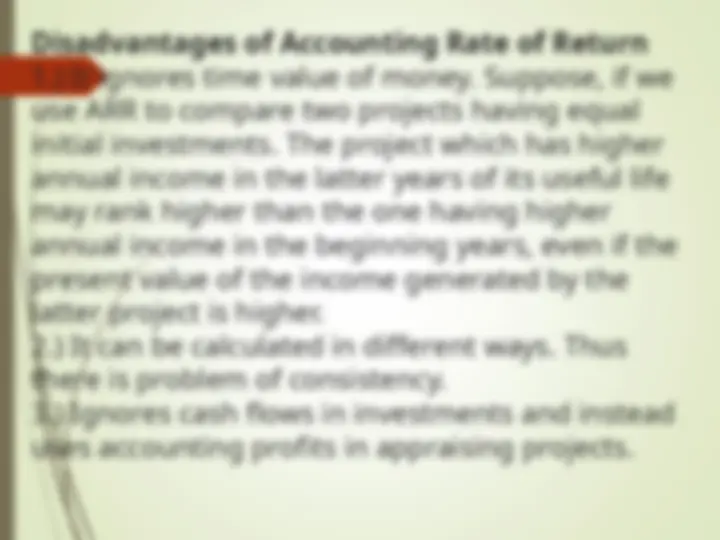

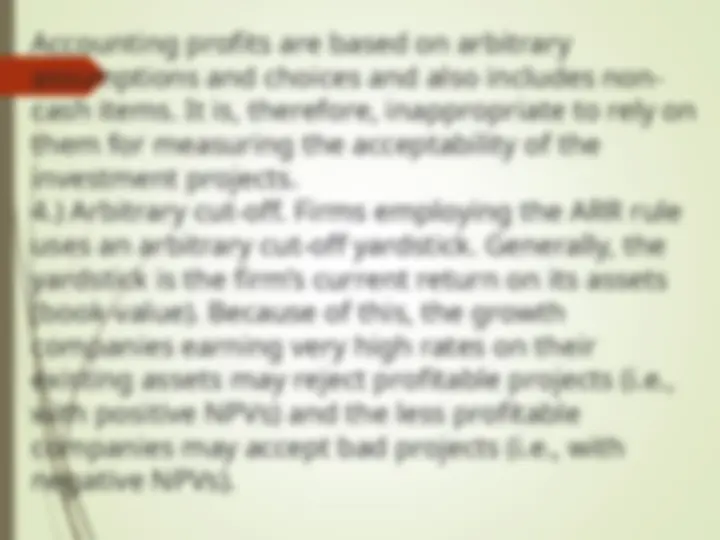

Accounting profits are based on arbitrary assumptions and choices and also includes non- cash items. It is, therefore, inappropriate to rely on them for measuring the acceptability of the investment projects. 4.) Arbitrary cut-off. Firms employing the ARR rule uses an arbitrary cut-off yardstick. Generally, the yardstick is the firm’s current return on its assets (book-value). Because of this, the growth companies earning very high rates on their existing assets may reject profitable projects (i.e., with positive NPVs) and the less profitable companies may accept bad projects (i.e., with negative NPVs).

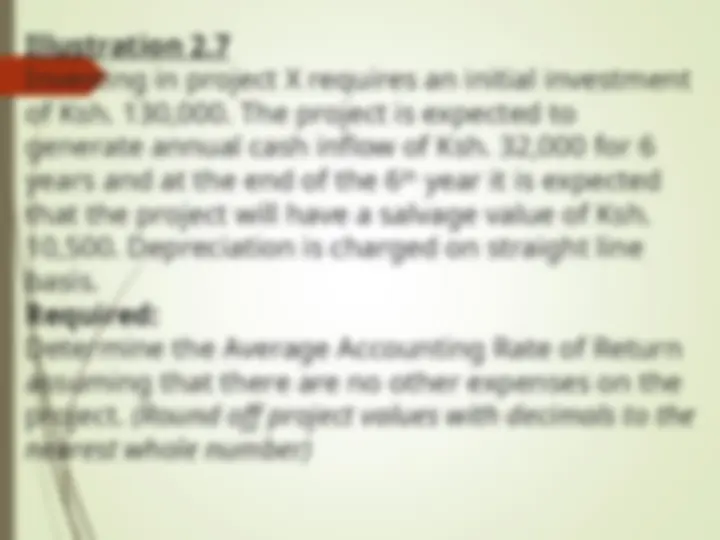

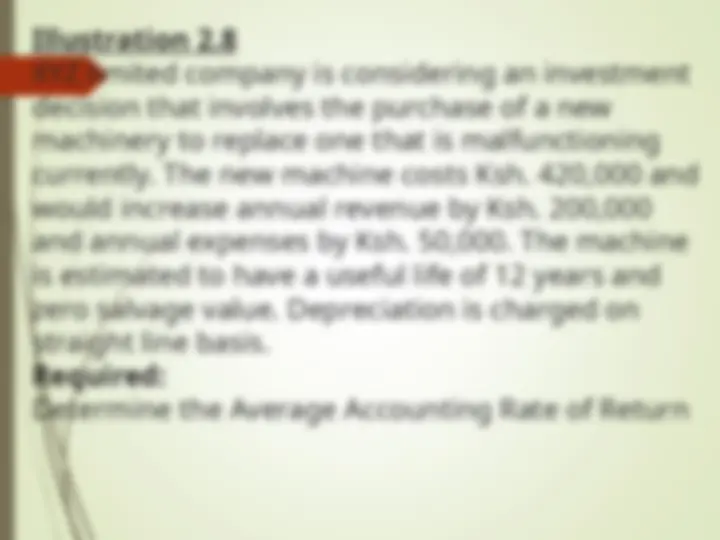

Illustration 2. A project will cost Ksh. 40,000. Its stream of earnings before depreciation, interest and taxes (EBDIT) during first year through five years is expected to be Ksh. 10,000, Ksh. 12,000, Ksh. 14,000, Ksh. 16,000 and Ksh. 20,000. Assumptions: i.) 50% tax rate ii.) Depreciation is an allowable expense that is determined on straight-line basis. Required: Determine the project’s ARR.