Download cash flow cheat sheet and more Cheat Sheet Accounting in PDF only on Docsity!

5-

The Statement of Cash Flows

Overview

You have finally arrived at the third of the “big three” required financial statements. The statement of cash flows is the newest of the three, having only been required since 1988. Although it usually isn’t given as much weight as the balance sheet or income statement, it can be a very useful statement for decision makers.

Like the other two statements, items are grouped according to categories. In the case of the statement of cash flows, the categories are referred to as activities: operating, investing, and financing.

There is one standard format for the investing and financing sections of the statement of cash flows. For the operating activities section, however, there are two possible methods: direct and indirect. Many people feel that the direct method is the better of the two methods. However, nearly all companies use the indirect method, so this method is the manner of the operating activities section that we will place our focus. In addition, the few companies that do use the direct method must perform a reconciliation, which essentially is the indirect method.

By analyzing a statement of cash flows, you can begin to understand where a company may be headed in the future or at what point in a company’s life cycle it is currently functioning. These pieces of information are sometimes easier to glean from a statement of cash flows than from a balance sheet or income statement (the latter two of which are prepared using the accrual method).

The statement of cash flows is the only one of the required financial statements not prepared on an accrual basis. It is prepared for a period of time, similar to the income statement and different from the balance sheet.

Learning Objectives

Refer to the Review of Learning Objectives at the end of the chapter. It is crucial that this section of the chapter is second nature to you before you attempt the homework, a quiz, or exam. This important piece of the chapter serves as your CliffsNotes or “cheat sheet” to the basic concepts and principles that must be mastered.

If after reading this section of the chapter you still don’t feel comfortable with all of the Learning Objectives covered, you will need to spend additional time and effort reviewing those concepts that you are struggling with.

The following “Tips, Hints, and Things to Remember” are organized according to the Learning Objectives (LOs) in the chapter and should be gone over after reading each of the LOs in the textbook.

5-2 O Chapter 5/The Statement of Cash Flows

Tips, Hints, and Things to Remember

LO1—Describe the circumstances in which the cash flow statement is a particularly

important companion of the income statement.

Why? In some instances, information on the income statement can be misleading in terms of how the company is actually doing and how they will perform in the future. Since some expenses are estimates, (like depreciation or provisions for future obligations) but don’t adversely affect cash, the company may be doing better in terms of current cash flow than the income statement indicates if these noncash expenses are very large.

The cash flow statement isn’t based on estimates and judgment calls like the income statement frequently is. It is based on the actual cash that came in or went out during the period. Hence, the statement of cash flows is an important financial statement that should be examined in conjunction with the other financial statements and should not be ignored or completely discounted.

LO2—Outline the structure of and information reported in the three main

categories of the cash flow statement: operating, investing, and financing.

How? Do you really need to memorize which of the three categories any possible transaction can fall under? Yes and no. Yes, you do need to know which of the three categories any given transaction falls under. No, you should not try memorizing a long list of transactions. Instead, rely on your knowledge of the balance sheet and income statement, information you hopefully have mastered from the prior two chapters, to make learning this chapter a piece of cake. With only a few exceptions, the following holds true:

Operating activities relate to those activities found on the income statement and in the current asset and current liability sections of the balance sheet. What are the exceptions? Just because cash (and equivalents) is a current asset doesn’t mean that a change in cash (and equivalents) indicates an operating activity has taken place. Cash (and equivalents) balances can change from any of the three types of activities so the change in the account balance of cash (and equivalents) should be ignored when computing the operating activities.

Another exception includes gains and losses on the income statement related to the sale of long- term assets. Yet another exception exists with respect to the balance sheet, and that is the paying off of long-term debt that has been reclassified as current for the period since it will be paid off soon. A recent reclassification of debt from long-term to current doesn’t change the type of activity from financing into operating.

Investing activities relate to those activities found in the long-term asset section of the balance sheet.

Financing activities relate to those activities found in the long-term liability and equity sections of the balance sheet.

5-4 O Chapter 5/The Statement of Cash Flows

If you are a visual learner, or like to put your knowledge on paper rather than risk it being jumbled in your head, then write out something like the following with the above accounts receivable information in mind:

Account Balance Change

Effect on Cash Flows Relative to Net Income Current – + Assets Current Liabilities

With only that one example, you can then fill in the rest of the table. Current asset increases go in the opposite direction as decreases, and current liabilities move in the exact opposite direction as current assets. Your completed table should then look like the following:

Account Balance Change

Effect on Cash Flows Relative to Net Income Current – + Assets + – Current – – Liabilities + +

Again, don’t try memorizing the table. Rather, know how to create it from any given example. A current asset decrease from one period to the next means that either more cash was collected (in the case of accounts receivable for instance) or cash wasn’t used as much (in the case of inventory declining for instance), so an increase in cash flow relative to net income results. The reverse is also true for assets (an increase will result in a decrease of cash flow relative to net income) and just the opposite happens in the case of current liabilities.

LO4—Prepare a complete statement of cash flows and provide the required

supplemental disclosures.

How? A statement of cash flows is not complete unless it reconciles the beginning and ending cash balance. Even if you aren’t asked to prepare a complete statement of cash flows, it is a good idea to reconcile your beginning and ending cash. Doing so allows you to check your work. Coming up with a change in cash on your statement of cash flows that equals your change in cash on your balance sheet will not guarantee that your statement of cash flows is correct (as you may have misclassified a financing activity as an investing activity for instance), but it will provide you with some confidence that you have at least captured every item and not made any errors in your calculations.

Chapter 5/The Statement of Cash Flows O 5- 5

LO5—Assess a firm’s financial strength by analyzing the relationships among cash

flows from operating, investing, and financing activities and by computing financial

ratios based on cash flow data.

Why? Exhibit 5-9 is very important to understand. Obviously, the magnitude of the numbers should also make a difference in your analysis. A company in position 6 who has –$10 in investing isn’t necessarily “growing rapidly.” Negative 10 dollars simply doesn’t mean much; wheras, –$ billion in investing certainly does.

Situations 2 and 4, assuming the numbers are significant, are the best situations to be in. A negative number in investing is actually a favorable sign. A company in situation 6 may be a company still in its start-up phase. Situations 5 and 7 are the worst positions to be in.

LO6—Demonstrate how the three primary financial statements tie together, or

articulate, in a unified framework.

LO7—Use knowledge of how the three primary financial statements tie together in

order to prepare a forecasted statement of cash flows.

How? When creating a forecasted, or pro-forma, statement of any type, start with the prior year’s statement as your “skeleton.” Then fill in the given items or items that aren’t changing. Finally, fill in the items that need to be solved for. You will have to create, or be given, a forecasted income statement and balance sheet before you can prepare a forecasted statement of cash flows.

For a forecasted income statement, be sure to adjust for variable costs and changes in the balance sheet numbers. In other words, if sales revenue goes up by 10 percent, COGS should also go up by 10 percent unless you are told otherwise. Other examples of items that are “tied” to the balance sheet include depreciation and interest expenses. If fixed assets go up, then depreciation should also usually go up. If debt goes up, then so should the interest expense (unless a lower interest rate is obtained on new debt while old debt is retired), etc.

The following section, featuring various multiple choice questions, exercises, and problems, along with solutions and approaches to arriving at the solutions, is intended to develop your problem- solving and critical-thinking abilities. While learning through trial and error can be effective for improving your quiz and exam scores, and it can be a more interesting way to study than merely re- reading a chapter, that is only a secondary objective in presenting this information in this format.

The main goal of the following section is to get you thinking, “How can I best approach this problem to arrive at the correct solution—even if I don’t know enough at this point to easily come up with the proper results?” There is not one simple approach that can be applied to all questions to arrive at the right answer. Think of the following approaches as possibilities, as tools that you can place in your problem-solving toolkit—a toolkit that should be consistently added to. Some of the tools have yet to even be created or thought of. Through practice, creative thinking, and an ever-expanding knowledge base, you will be the creator of the additional tools.

Chapter 5/The Statement of Cash Flows O 5- 7

MC5-4 (LO3) The following information was taken from the 2007 financial statements of Vaughn Corporation:

Accounts Receivable, January 1, 2007 $ 110, Accounts Receivable, December 31, 2007 150, Sales on account and cash sales 2,200,

No Accounts Receivable were written off or recovered (from previous write offs) during the year. What amount was collected from customers in 2007?

a. $2,160,

b. $2,200,

c. $2,240,

d. $2,350,

MC5-5 (LO3) Mays Company’s income statement for the year ended December 31, 2007, reported net income of $360,000. The financial statements also disclosed the following information:

Amortization $ 25,

Depreciation 60,

Increase in accounts receivable 140,

Increase in inventory 48,

Decrease in accounts payable 76,

Increase in salaries payable 28,

Dividends paid 120,

Purchase of equipment 150,

Increase in long-term note payable 300,

Net cash provided by operating activities for 2007 should be reported as

a. $89,000.

b. $209,000.

c. $239,000.

d. $329,000.

5-8 O Chapter 5/The Statement of Cash Flows

MC5-6 (LO3) In a statement of cash flows (indirect method), an increase in inventories with no change in the balance for accounts payable should

a. be presented in the investing activities section.

b. not be presented.

c. be presented as a deduction from net income.

d. be presented as an addition to net income.

MC5-7 (LO4) Supplemental disclosures required only when the statement of cash flows is prepared using the indirect method include

a. a schedule reconciling net income with net cash provided by (used in) operating activities.

b. amounts paid for interest and taxes.

c. amounts deducted for depreciation and amortization.

d. significant noncash investing and financing activities.

MC5-8 (LO4) Woods Company sold a computer for $50,000. The computer’s original cost was $250,000, and the accumulated depreciation at the date of sale was $175,000. The sale of the computer should appear on Woods’ annual statement of cash flows (indirect method) as

a. a reduction in cash flows from operating activities of $25,000 and an increase in cash flows from investing activities of $50,000.

b. only an increase in cash flows from operating activities of $50,000.

c. only an increase in cash flows from investing activities of $50,000.

d. an increase in cash flows from operating activities of $25,000 and an increase in cash flows from investing activities of $50,000.

MC5-9 (LO4) Pantheon Incorporated declared and paid cash dividends of $100,000 on their stock. Pantheon also received a cash dividend of $50,000 from a company they have heavily invested in. How would these dividends be presented in Pantheon’s statement of cash flows?

a. as a $150,000 reduction in cash flows from investing activities

b. as a $50,000 reduction in cash flows from financing activities

c. as a $100,000 reduction in cash flows from financing activities and a $50, increase in cash flows from investing activities

d. as a $100,000 reduction in cash flows from financing activities and a $50, increase in cash flows from operating activities

5-10 O Chapter 5/The Statement of Cash Flows

Matching

Matching 5-1 (LO1) Listed below are the terms and associated definitions from the chapter primarily for LO1 through LO4. Match the correct definition letter with each term number.

___ 1. articulation

___ 2. direct method

___ 3. financing activities

___ 4. indirect method

___ 5. investing activities

___ 6. noncash investing and financing activities

___ 7. operating activities

___ 8. pro forma cash flow statement

___ 9. statement of cash flows

a. approach to calculating and reporting cash flow from operating activities that reconciles net income with operating cash flow b. includes transactions and events that normally enter into the determination of net income, including interest and taxes c. primarily includes purchases and sales of noncurrent assets such as land, buildings, and nontrading financial instruments d. an example is the purchase of land by issuing stock e. forecast or projection of the amounts that will be in the cash flow statement in a future period f. one of the three primary financial statements, separated into operating, investing, and financing activities g. approach to calculating and reporting cash flow from operating activities that itemizes the major operating cash receipt and cash payment categories h. three primary financial statements are not isolated lists of numbers but are an integrated set of reports on a company’s financial health i. includes transactions and events whereby cash is obtained from or repaid to owners and creditors

Matching 5-2 (LO5) Listed below are the terms and associated definitions from the chapter for LO5. Match the correct definition letter with each term number.

___ 1. cash flow adequacy ratio

___ 2. cash flow-to-net income ratio

___ 3. cash times interest earned ratio

a. ratio used to analyze the cash flow relationship between cash from operations and reported net income b. cash from operations divided by expenditures for fixed asset additions and acquisitions of new businesses c. measure used to indicate a company’s interest-paying ability

5-

Problems

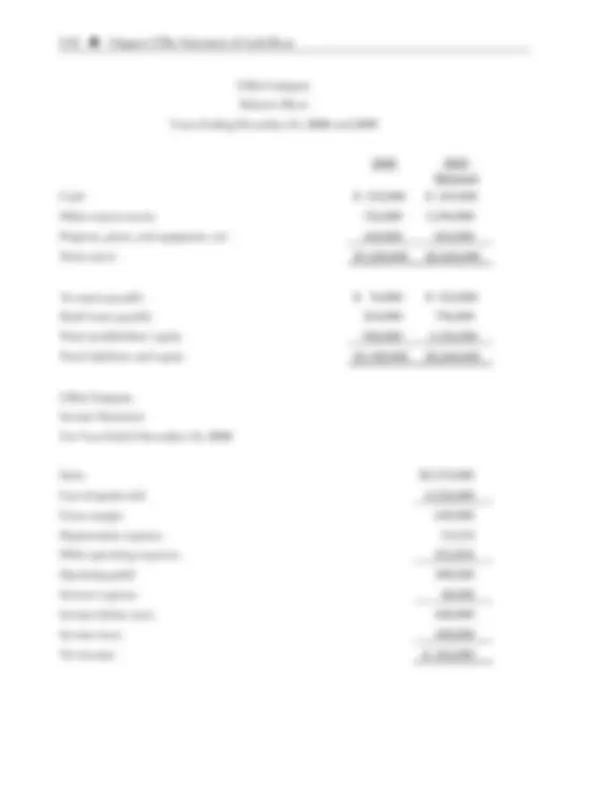

Problem 5-1 (LO3) Partial balance sheet data and additional information for Rasta Industries are given below:

Rasta Industries Partial Balance Sheet December 31, 2006 and 2005

Assets: 2006 2005

Cash $70,000 $20,

Accounts receivable 80,000 90,

Inventory 65,000 40,

Liabilities:

Accounts payable $95,000 $77,

Additional Information:

(a) Net income for 2006 was $55,000.

(b) Depreciation expense for 2006 was $28,000.

Prepare the operating activities section of the statement of cash flows, using the indirect method, for the year ending December 31, 2006.

Were there nonoperating activities during the year? How do you know?

Chapter 5/The Statement of Cash Flows O 5- 13

Problem 5-3 (LO5) The following pertains to the Lansford Company for the year ended December 31, 2007.

Depreciation expense $ 10,

Issuance of common stock 105,

Cash dividends paid 19,

Increase in inventory 43,

Decrease in accounts receivable 68,

Decrease in accounts payable 27,

Retirement (paying off) of long-term debt 120,

Net income 150,

Proceeds from sale of equipment ($12,000 loss) 63,

Purchase of equipment 84,

Cash and cash equivalents, beginning of year 200,

Prepare a statement of cash flows in good form using the indirect method. Calculate the cash flow to net income and cash flow adequacy ratios for the company.

How would you characterize Lansford Company based only on your completed statement of cash flows (healthy and growing/expanding, startup phase, cash cow, financially distressed, etc.)?

Problem 5-4 (LO7) Uffizi Company is preparing a forecast of its net income for the year 2009. In addition, Uffizi plans to construct a forecasted statement of cash flows for 2009. The balance sheet and income statement data for 2008 are presented below as well as a forecast of the balance sheet for 2009. Management expects sales in 2009 to rise to $6,000,000. In order to achieve this level of increase, management estimates that operating expenses (specifically sales commissions) will rise to $410,134.

Prepare a forecasted income statement and forecasted statement of cash flows (using the indirect method) for the year ended December 31, 2009, for Uffizi Company. Calculate the cash flow to net income and cash flow adequacy ratios.

5-14 O Chapter 5/The Statement of Cash Flows

Uffizi Company Balance Sheet Years Ending December 31, 2008 and 2009

(forecast)

Cash $ 132,000 $ 212,

Other current assets 756,000 1,196,

Property, plant, and equipment, net 440,000 852,

Total assets $1,328,000 $2,260,

Accounts payable $ 76,000 $ 112,

Bank loans payable 324,000 796,

Total stockholders’ equity 928,000 1,352,

Total liabilities and equity $1,328,000 $2,260,

Uffizi Company

Income Statement

For Year Ended December 31, 2008

Sales $3,172,

Cost of goods sold 2,532,

Gross margin 640,

Depreciation expense 14,

Other operating expenses 216,

Operating profit 408,

Interest expense 48,

Income before taxes 360,

Income taxes 108,

Net income $ 252,

5-16 O Chapter 5/The Statement of Cash Flows

$150,000 (550,000 – 400,000), but the cash receipts are $550,000. The gain of $150,000 shows up as part of net income. Assuming total net income is $800,000, part of the indirect statement of cash flows will look like the following:

Partial Statement of Cash Flows—Operating Activities

Cash flows from operating activities:

Net income $ 800, Adjustments:

- Gain on sale of plant assets (150,000)

In other words, our cash flow from operating activities without considering other items and after removing the nonoperating activity item of the gain on the sale of an investing activity is $650,000.

On the same statement, we will find the following in the investing activities section:

Partial Statement of Cash Flows—Investing Activities

Cash flows from investing activities:

Proceeds from the sale of plant assets $ 550,

Gains and cash receipts will only equal each other when the asset being sold has been fully depreciated. Therefore, say the question was worded to say the following:

“Cash receipts on the sale of a plant asset, without a book value, in the ordinary course of business should be presented in a statement of cash flows prepared using the indirect method as”

There would be two correct answers. Both choices a and d would be correct.

From this you can hopefully see how crucial it is to read every word in a question very carefully. Minor changes in wording can alter which answer is correct.

MC5-

Answer: d

Approach and explanation: Rather than attempt a question like this in your head or try to recall a memorized formula, your best bet may be to use T-accounts and actually “see” what happens to the accounts. First, sketch out something like this with some fake beginning balances:

Cash Taxes Payable Tax Expense Beginning Balances 11,000 2,

Chapter 5/The Statement of Cash Flows O 5- 17

Now let’s assume that taxes payable increased:

Cash Taxes Payable Tax Expense Beginning Balances 11,000 2, Tax Accrual?? Tax Payment?? Ending Balance 3,

Let’s also assume that we accrue taxes at a time other than when we pay them (leaving us with a missing debit to Taxes Payable as follows):

Cash Taxes Payable Tax Expense Beginning Balances 11,000 2, Tax Accrual 10,000 10, Tax Payment?? Ending Balance 3,

Finally, we can assume that no other items affected cash and fill in the blanks to make the correct answer apparent:

Cash Taxes Payable Tax Expense Beginning Balances 11,000 2, Tax Accrual 10,000 10, Tax Payment 9,000 9, Ending Balance 2,000 3,000 10,

Chapter 5/The Statement of Cash Flows O 5- 19

Next add your depreciation and amortization to net income. Subtract your increases in current assets. Add your increase in the only current liability that went up. And subtract your increase to the only current liability that went down.

If, at this point, you come up with an answer that is not one of the choices, do not circle the closest answer and call it good. You should come up with an exact answer that matches one of the choices (hopefully choice b !). Never just go with the next closest choice unless you have run out of time or it is a question that allows for minor rounding differences and you are only off by a dollar or so.

Instead, start from scratch and work the problem in a slightly different way to try and figure out where you went wrong the first time. You may have just added wrong or left off a number. Or you may have misclassified an item. In any case, keep working it, time permitting, until you come up with an exact match.

MC5-

Answer: c

Approach and explanation: Since inventory is a current asset (other than cash or a cash equivalent) you should know that it is not an investing or financing activity. Because the balance changed, you should know that it should be presented when the indirect method is being used. Hence, you can rule out choices a and b.

Now the question is, does an increase in inventories increase or decrease cash flows relative to net income? Here is a simple way to illustrate the answer assuming that a company had no transactions during the year except for the purchase of $1,000 of inventory with cash (or on credit that was subsequently paid off and hence no change in the Accounts Payable balance):

Cash basis: Cash flow = –$1,

Accrual basis: Net income = –0– (since COGS isn’t recognized until the inventory is sold)

Therefore, the statement of cash flows would look like this: Net Income 0 Adjustments:

- Increase in inventories (1,000) Net cash flow from operating activities (1,000)

5-20 O Chapter 5/The Statement of Cash Flows

Inventory balance changes may not be as intuitive to you as another account, like Accounts Receivable. Hence, you may want to use Accounts Receivable as your thought example and then just infer that since both Inventory and Accounts Receivable are current assets, they both move in the same direction (as subtractions for determining cash flow relative to net income when the balances increase).

MC5-

Answer: b

Approach and explanation: The key portion of this question is the fact that we are looking only for disclosures required when the indirect method is used. In other words, the disclosure is not needed when the direct method is used. According to FASB Statement No. 95 (step 6 in the textbook), amounts paid for interest and taxes must be disclosed. If the direct method is used, these items are already included in the operating activities section, so no supplemental disclosure is required. That is not the case if the indirect method is used, and that is why choice b is the correct one.

As far as the incorrect choices go...

Choice a would be correct if we changed the word indirect, in the question, to direct.

Amounts deducted for depreciation and amortization are already disclosed in statement using the indirect method, so they need not be included in any supplemental disclosure.

Significant noncash investing and financing activities are required supplemental disclosures regardless of which method (direct or indirect) is used.

MC5-

Answer: d

Approach and explanation: See the explanation for MC5-2 on page 5-15 for details on how to solve questions like this one.

MC5-

Answer: d

Approach and explanation: Dividends are a somewhat difficult item on the statement of cash flows because the treatment is different depending on whether the dividends are paid or received. Don’t net the dividends. Think of the inflow as showing up on the income statement and, hence, being an operating activity. Think of the outflow as being a reduction in Retained Earnings and, hence, a financing activity (given the discussion on pages 5-2 and 5-3). See, also, the explanation for MC5- on page 5-15.