Download Chapter 1 Government Bonds (JGBs) and more Schemes and Mind Maps Construction in PDF only on Docsity!

Chapter 1 Government Bonds (JGBs)

1 Primary Market for Government Bonds

Primary Market for Government Bonds

JGBs for financing fiscal expenditure are issued in various types, depending on their applicable

legal grounds and bond features. This section explains how JGBs are issued.

(1) JGBs by Legal Grounds of Issuance

JGBs can be divided into two main categories: General Bonds, and Fiscal Investment and

Loan Program Bonds (FILP Bonds). While the government mainly relies on tax revenue to

redeem General Bonds, the redemption and the interest payments on FILP Bonds are covered

by the collection of Fiscal Loan receivable. However, both General Bonds and FILP Bonds

are jointly issued as JGBs with the same interest rate and maturity. They are the same financial

instruments and are treated in the same manner on the market as well.

Fig.2-1 JGBs by Legal Grounds of Issuance

JGBs

General Bonds

Construction Bonds

Special Deficit-Financing Bonds

Reconstruction Bonds

Refunding Bonds

Fiscal Investment and Loan Program Bonds (FILP Bonds)

A. General Bonds

General Bonds consist of Construction Bonds, Special Deficit-Financing Bonds,

Reconstruction Bonds and Refunding Bonds. Construction Bonds and Special Deficit-

Financing Bonds are issued under the General Account and the revenue from their issuance is

reported as the government revenue of the General Account.

On the other hand, Reconstruction Bonds are issued under the Special Account for

Reconstruction from the Great East Japan Earthquake and Refunding Bonds under the Special

Account of Government Debt Consolidation Fund and the revenue from their issuance is

reported as the government revenue of each Special Account.

a. Construction Bonds

Article 4, paragraph (1) of the Public Finance Act prescribes that annual government

expenditure has to be covered in principle by annual government revenue generated from

other than government bonds or borrowings. But as an exception, a proviso of the Article

allows the government to raise money through bond issuance or borrowings for the purpose

of public works, capital subscription or lending. Bonds governed by this proviso of Article 4,

paragraph (1) are called Construction Bonds.

The Article prescribes that the government can issue Construction Bonds within the amount

approved by the Diet, and the ceiling amount is provided under the general provisions of the

General Account budget ( ☞ )

☞ When intending to get ap- proval for this ceiling amount, the government submits to the Diet a redemption plan that shows the redemption amount and the redemption periods for each fiscal year for reference.

Chapter 1 Government Bonds (JGBs)

Chapter 1 Government Bonds (JGBs)

1 Primary Market for Government Bonds

b. Special Deficit-Financing Bonds

When estimating a shortage of government revenue despite the issuance of Construction

Bonds, the government can issue government bonds based on a special act ( ☞① ) to raise

money for the purpose of other than public works and the like. These bonds are generally

called Special Deficit-Financing Bonds.

As is the case with Construction Bonds, the government can issue Special Deficit-Financing

Bonds within the amount approved by the Diet and the ceiling amount is provided under the

general provisions of the General Account budget ( ☞② ).

Special Deficit-Financing Bond issuance must be made on exceptional cases. Therefore, the

government has to minimize the issuance amount as much as possible within the amount

approved by the Diet, while taking into account the state of tax and other revenues ( ☞③ ).

c. Reconstruction Bonds

To recover from the Great East Japan Earthquake disasters, the government is supposed

to issue Reconstruction Bonds from FY2011 to FY2025 in accordance with the Act on

Special Measures concerning the securing of financial resources to execute measures

necessary for recovery from the Great East Japan Earthquake (Reconstruction Funding

Act). While necessary financial resources will be financed with revenues of Special Taxes

for Reconstruction, the government will issue Reconstruction Bonds as bridging finance

until these revenues are receivable to the government.

The government may issue these Reconstruction Bonds within the amount as approved

by the Diet. The ceiling amount is provided under the general provisions of the Special

Account budget from FY2012 onwards.

d. Refunding Bonds

As for General Bonds, Refunding Bonds are issued in order to raise funds for refunding

part of matured JGBs. Among General Bonds, as for Construction Bonds and Special

Deficit-Financing Bonds, the issuance amount of Refunding Bonds is determined basically

in accordance with the 60-year redemption rule. As for Reconstruction Bonds, Refunding

Bonds are issued depending on the amount of the revenue from Special Taxes for

Reconstruction and profit from sales of stocks in each year (☞ ).

Refunding Bonds are the JGBs issued through the Special Account for the Government

Debt Consolidation Fund (GDCF). Revenues from Refunding Bonds are directly posted to

the fund.

In the issuance of Refunding Bonds, the government is not required to seek the Diet

approval for the maximum issuance amount. This is because unlike in the case of bonds

issued to secure new revenue resources, such as Construction Bonds and Special Deficit-

Financing Bonds, issuing Refunding Bonds does not lead to an increase in the total amount

of outstanding debt.

(Reference) Front-loading issuance of Refunding Bonds

As massive bonds redemption at maturity is expected to continue, the government is

allowed to front-load the issuance of Refunding Bonds in order to mitigate the impact of

concentration of bonds redemption at maturity, to control substantial volatility of JGB market

issuance in each fiscal year and to enable flexible issuance of them in response to financial

☞② The government is also required to submit a redemp- tion plan to the Diet for refer- ence.

☞③ In this context, it is al- lowed to issue Special Deficit- Financing Bonds until the end of June in the next fiscal year. (deferred issuance in the ac- counting adjustment term)

☞① The “Act on Special Provisions concerning Is - suance of Public Bonds to Secure Financial Resources Required for Fiscal Manage- ment” allows Special Deficit- Financing Bonds to be issued for five years from FY2016 to FY2020.

☞ In line with tax revenues through the consumption tax increases in and after FY2014, Refunding Bonds are issued for Special Bonds for covering Public Pension Funding, which were issued in FY2012 and FY2013 as bridging finance until tax revenues are assured for the finance of increase of the Government’s contribution to the basic national pension, based on the special law for Special Deficit-Financing Bonds legislated in FY 2012.

Ref: Chapter 1 3 (1)

“Redemption System” (P77)

Chapter 1 Government Bonds (JGBs)

1 Primary Market for Government Bonds

Ref: “FILP Report”

☞① As with Construction Bonds and Special Deficit- Financing Bonds, the govern- ment is required to submit a redemption plan to the Diet for a reference.

☞②Also in the System of Na- tional Accounts (SNA), which is created by the United Na- tions for each country to create economic statistics based on a common standard, FILP Bonds are not classified as debt of the general government.

B. Fiscal Investment and Loan Program Bonds (FILP Bonds)

Along with the FY2001 reform of the FILP (Fiscal Investment and Loan Program), the

government started issuance of the Fiscal Investment and Loan Program Bonds (so-called

FILP Bonds) to raise funds for the investment of the Fiscal Loan Fund. As is the case

with other types of government bonds, FILP Bonds are issued based on the credit of the

government up to the amount approved by the Diet, and the ceiling amount is provided under

the general provisions of the Special Account Budget (Article 62, paragraph (2) of the Act on

Special Accounts ) ( ☞① ). Revenues from the FILP Bonds issuance are allotted to the annual

revenue for the Special Account for the Fiscal Investment and Loan Program (FILP Special

Account).

However, the FILP Bonds are different from Construction Bonds and Special Deficit-

Financing Bonds on one account. While future taxes will be used to redeem Construction

Bonds and Special Deficit-Financing Bonds, the redemption on the FILP Bonds are covered

by the collection of Fiscal Loan receivable. Therefore, when publishing outstanding debt, FILP

Bonds are treated differently from General Bonds (☞② ).

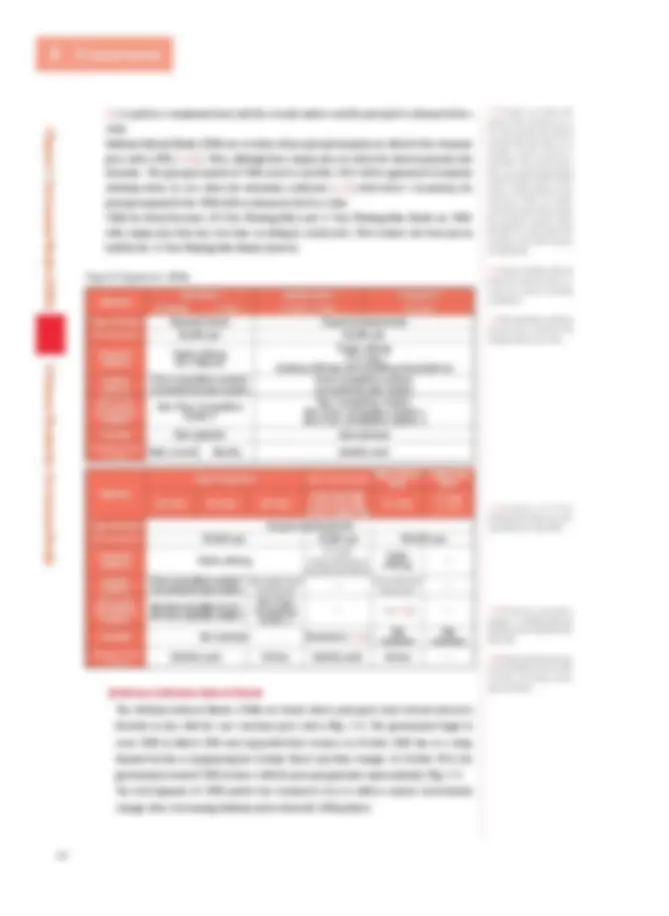

(2) Types of JGBs

Government bonds are the securities issued by the central government. The central government

pays the bondholders interests on the securities on a semiannual basis, except for short-term bonds

and redeems the principal amount at maturity (i.e., redemption). The JGBs planned to be issued in

FY2020 can be classified into six categories: short-term (6-Month and 1-Year Bonds); medium-

term (2-Year and 5-Year Bonds); long-term (10-Year Bonds); super long-term (20-Year, 30-Year

and 40-Year Bonds); Inflation-Indexed Bonds (10-Year Bonds); and JGBs for Retail Investors (3-

Year Fixed-Rate, 5-Year Fixed-Rate and 10-Year Floating-Rate Bonds).

The short-term JGBs are all discount bonds, which are accompanied by no interest payment

during their duration to maturity and redeemed at face value at maturity.

On the other hand, all medium-, long-, super long-term bonds and JGBs for Retail Investors (3-Year

Fixed-Rate, 5-Year Fixed-Rate) are the bonds with fixed-rate coupons. With fixed-rate coupon-

bearing bonds, the interest calculated by the coupon rate determined at the time of issuance (☞

Government affiliated financial

institutions

Incorporated administrative agencies

Local governments

Fiscal Loan Fund

Financial markets

Government affiliated financial

institutions

Incorporated administrative agencies

Local governments

Trust Fund Bureau Fund

Postal Savings (^) Refund

Deposit

Loan

FILP Bonds Loan

FILP agency bonds (non-FILP plan)

Redemption

Recovery

Refund

Deposit

<Before Reform> <After Reform>

Pension Reserves (Employee Pension/ National Pension)

Redemption Recovery

Note1: Prior to the reform, FILP funding came from the Trust Fund Bureau Fund (shown above) and also from Postal Life Insurance Funds, the Industrial Investment Special Account and Government-Guaranteed Bonds. Note2: Trust Fund Bureau Fund includes deposits from special account surplus reserves, other than those shown above.

Note1: After the reform, FILP includes loans to FILP Special Account (Investment Account), Government-Guaranteed Bonds; loans from Postal Savings and Postal Life Insurance to local governments. Since FY2007, there has been no loan from Postal Savings and Postal Life Insurance to local governments. Note2: Fiscal Loan Fund includes deposits from special account surplus reserves, other than those shown above.

Fig.2-2 Outline of FILP Reform

Chapter 1 Government Bonds (JGBs)

1 Primary Market for Government Bonds

①) is paid on a semiannual basis until the security matures and the principal is redeemed at face

value.

Inflation-Indexed Bonds (JGBi) are securities whose principal amounts are linked to the consumer

price index (CPI) (☞②). Thus, although their coupon rates are fixed, the interest payment also

fluctuates. The principal amount of JGBi issued in and after 2013 will be guaranteed at maturity

(deflation floor). In case where the indexation coefficient (☞③ ) falls below 1 at maturity, the

principal amount for the JGBi will be redeemed at the face value.

JGBs for Retail Investors (10-Year Floating-Rate) and 15-Year Floating-Rate Bonds are JGBs

with coupon rates that vary over time according to certain rules. New issuance has been put on

hold for the 15-Year Floating-Rate Bonds, however.

Fig.2-3 Types of JGBs

Maturity

Short-term Medium-term Long-term

6-Month 1-Year 2-Year, 5-Year 10-Year

Type of issue Discount bonds Coupon-bearing bonds

Min. face value unit 50,000 yen 50,000 yen

Issuance method

Public offering BOJ Rollover

Public offering OTC sales (making offerings and accepting subscriptions) Auction method

Price-competitive auction/ Conventional-style auction

Price-competitive auction/ Conventional-style auction Non-price Competitive Auction

Non-Price Competitive Auction I

Non-Competitive Auction Non-Price Competitive Auction I Non-Price Competitive Auction II

Transfer Not restricted Not restricted Frequency of issue (FY2020) Twice a month Monthly Monthly each

Maturity

Super long-term JGBs for Retail Investors

Inflation-Indexed Bonds

Floating-Rate Bonds

20-Year 30-Year 40-Year

3-Year Fixed-Rate, 5-Year Fixed-Rate, 10-Year Floating-Rate

10-Year

15-Year (☞④)

Type of issue Coupon-bearing bonds

Min. face value unit 50,000 yen 10,000 yen 100,000 yen

Issuance method Public offering

OTC sales (making offerings and accepting subscriptions)

Public offering ―

Auction method

Price-competitive auction/ Conventional-style auction

Yield-competitive auction/ Dutch-style auction ―

Price-competitive auction/ Dutch-style auction ―

Non-price Competitive Auction

Non-Price Competitive Auction I Non-Price Competitive Auction II

Non-Price Competitive Auction II

― ―( ☞⑤ ) ―

Transfer Not restricted Restricted ( ☞⑥ )

Not restricted

Not restricted Frequency of issue (FY2020)

Monthly each 6 times Monthly each 4 times ―

(Reference) Inflation-Indexed Bonds

The Inflation-Indexed Bonds (JGBi) are bonds whose principals (and relevant interests)

fluctuate in line with the core consumer price index (Fig. 2-4). The government began to

issue JGBi in March 2004 and suspended their issuance in October 2008 due to a sharp

demand decline accompanying the Lehman Shock and other changes. In October 2013, the

government resumed JGBi issuance with the principal guarantee upon maturity (Fig. 2-5).

The development of JGBi market has remained a key to address market environment

changes after overcoming deflation and to diversify JGB products.

☞① In the case where the period of time between an is- sue date and the first interest payment date falls short of six months, accrued interest is generated. The accrued inter- est is an amount representing interest for the period of time where a JGB purchaser does not hold a JGB (six months minus the period of time where the purchaser actually holds the JGB). It is paid by the JGB purchaser upon JGB issuance for adjustment.

☞② Japan’s Inflation-Indexed Bonds are indexed to the con- sumer price index (excluding perishables).

☞③The indexation coefficient measures how much the CPI changed after an issue date.

☞ ④ Issuance of 15-Year Floating-Rate Bonds has been suspended since May 2008.

☞⑤ Non-Price Competitive Auction Ⅱ of Inflation-Indexed Bonds has been suspended since May 2020.

☞⑥ JGBs for Retail Investors can be transferred only to retail investors (including certain trust custodians).

Chapter 1 Government Bonds (JGBs)

1 Primary Market for Government Bonds

submits a bidding price (or yield) and bidding amount in response to the issue terms (e.g.,

issuance amount, maturity, coupon rate ( ☞② )) presented by the MOF, and the issuance

price and amount will then be determined based on the bids.

In this type of auction, the issuing authority starts selling first to the highest price bidder

in descending order (or to the lowest yield bidder in ascending order) till the cumulative

total reaches the planned issuance amount. In Japan, the auction method varies by type of

security. One is the conventional (multiple price) method by which each winning bidder

purchases the security at one's bidding price; and the other is the Dutch-style (single price/

yield) method by which all winning bidders pay the lowest accepted bid price regardless of

their original bid prices (or yields) ( ☞③ ).

Non-competitive auction

Besides competitive auction, 2-Year, 5-Year and 10-Year Bonds are also issued through

non-competitive auction. This approach is to take into account small and medium market

participants who tend to submit a smaller bid than their larger counterparts. Biddings for

non-competitive auction are offered at the same time as for the price-competitive auction,

and the price offered equals to the weighted average accepted price of the price-competitive

auction. One can bid for either the price-competitive auction or for the non-price-

competitive auction.

The maximum issuance amount is 10% of the planned issuance amount. Each participant is

permitted to bid up to 1 billion yen ( ☞ ).

Non-Price Competitive Auction I & II

Non-Price Competitive Auction I is an auction in which biddings are offered at the same

time as for the price-competitive auction. The maximum issuance amount is set at 20% of

the total planned issuance amount and the price offered is equal to the weighted average

accepted price of the price-competitive auction. Only the JGB Market Special Participants

are eligible to bid in this auction. Each participant is allowed to bid up to the amount set

based on the result of its successful bids during the preceding two quarters. 40-year or JGBi

issues are not subject to Non-Price Competitive Auction I.

Non-Price Competitive Auction II is an auction carried out after the competitive auction

is finished. The price offered is equal to the weighted average accepted price in the price-

competitive auction or issuance price in Dutch-style competitive auction. Only the JGB

Market Special Participants are eligible to bid in this auction. Each participant is allowed

to bid up to the amount set based on the result of its bids during the preceding two quarters

( ☞① ). Inflation-Indexed Bonds (☞② ) and short-term JGB issues are not subject to Non-

Price Competitive Auction II.

b. Reopening rule

In March 2001, the immediate reopening rule was introduced for the purpose of the

enhancement of JGB liquidity, etc. The rule treats a new JGB issue as an addition to an

outstanding issue immediately from the issuance day, in principle, if the principal and

interest payment dates and the coupon rate for the new issue are the same as those for the

outstanding issue. 5-Year Bonds issues are subject to the rule ( ☞ ).

☞ The ceiling amount to bid is not applied to the Shinkin Central Bank, the Shinkumi Federation Bank, the Rokinren Bank and the Norinchukin Bank.

☞② Auction participants are designated according to Article 5, paragraph (2) of the Ordinance of the Ministry of Finance on Issuance, etc. of National Government Bonds. As of April 1, 2020, there were 233 auction participants.

☞③ The price-competitive conventional auction is used for all JGB issues excluding the 40-year issue subject to the yield-competitive Dutch auc- tion and the Inflation-Indexed Bonds subject to the price- competitive Dutch auction.

☞① Each participant is al^ - lowed to bid up to 10%* of one’s total successful bids in the competitive auction and Non-Price Competitive Auc- tion I. (*) The percentage was low- ered from 15% to 10% from an auction in January 2020.

☞② From May 2020, the MOF will not conduct Non- Price Competitive Auction (^) Ⅱ for Inflation-Indexed Bonds issues for the time being.

☞ As principal and interest payment dates for 2-Year Bonds differ from auction to auction, 2-Year Bonds are not effectively subjected to the re- opening rule (Ref: III Chapter 1 1(5) “Principal/Coupon Pay- ment Corresponding to Days of Issuance in FY2020”(P122)).

Chapter 1 Government Bonds (JGBs)

1 Primary Market for Government Bonds

From the viewpoint of securing market supply of each issue, 10, 20, 30 and 40-year issues

in FY2020 are subjected to the following rule, which is more advanced than the immediate

reopening rule.

The 10-Year Bonds will be integrated into four issues (integrating April, May and June

issues in 2020 into the April 2020 issue, July, August and September issues into the July

2020 issue, October, November and December issues into the October 2020 issue, and

January, February and March issues in 2021 into the January 2021 issue) unless interest

rates fluctuate wildly (the market yield on an auction day for a new issue deviates from the

coupon on the previous issue with the same maturity date by more than 30 basis points).

The reopening rule will also be used in principle to integrate 20-Year and 30-Year Bonds

each into four issues. The 40-Year Bonds (May, July, September, November, January and

March issues) will be integrated into one issue (May issue). In principle, JGBi issues (May,

August, November and February issues) will be integrated into one issue (May issue).

B. JGBs and sales system for Retail Investors

a. JGBs for Retail Investors

In March 2003, issuance was started on 10-Year Floating-Rate Bonds for Retail Investors

( ☞ ) in order to promote JGB holdings among individuals. Moreover, in order to respond

to retail investors various needs and to promote further sales, the government has been

improving product features by introducing 5-Year Fixed-Rate and 3-Year Fixed-Rate

Bonds.

Issuance of JGBs for Retail Investors rests on their handling and distribution by their

handling institutions comprised of securities companies, banks, and other financial

institutions as well as post offices (about 980 institutions). The handling institutions are

commissioned by the government to accept purchase applications and to sell JGBs to retail

investors. Handling institutions are paid a commission by the government corresponding to

the handled issuance amounts.

b. New Over-The-Counter (OTC) sales system for selling marketable JGBs

In addition to JGBs for Retail Investors, in October 2007 a new OTC sales system for

marketable JGBs was introduced in order to increase retail investors purchase opportunities

with regard to JGBs (2-Year, 5-Year, and 10-Year Bonds).

With regard to this new OTC sales system, it allows private financial institutions to engage

in subscription-based OTC sales of JGBs in a manner previously exclusive to post offices.

This development allows retail investors to purchase JGBs via financial institutions with

whom they are familiar, it also allows them to purchase JGBs in a manner that is essentially

ongoing. Depending on market yield conditions, however, the acceptance of subscriptions

may be suspended.

As with JGBs for Retail Investors, for the new OTC sales system, the government has

commissioned financial institutions (about 650 institutions) to conduct subscriptions and

sales of JGBs. Note that while these financial institutions are required to accept subscription

and sell JGBs at prices defined by the MOF within a defined period, they are not required to

purchase any unsold JGBs.

☞ JGBs for Retail Investors are designed not to lose prin- cipal. The minimum interest rate of 0.05% is set to prevent the rate from falling to zero or becoming negative.

Ref: Part I, 4 (1) “JGB

Holdings by Retail Inves-

tors” ( P29)

Chapter 1 Government Bonds (JGBs)

1 Primary Market for Government Bonds

C. Offering to the public sector (Bank of Japan Rollover)

In the Bank of Japan rollover, the BOJ underwrites Refunding Bonds instead of asking the

government to redeem part of JGBs that mature after being purchased by the central bank in

the market.

While Article 5 of the Public Finance Act prohibits the BOJ from underwriting government

bonds, the abovementioned BOJ rollover is an exception that is allowed up to an amount

authorized by the Diet under a proviso to the Article. Every fiscal year, the MOF requests

the BOJ rollover that the central bank accepts after confirming that the rollover will cause no

problem with monetary policy.

An increase in the BOJ rollover can reduce the amount of JGBs issued through usual auctions

in the market, allowing the MOF to level the effects of fluctuations in the annual JGB

redemption amount and fiscal demand on fluctuations in the amount of JGB market issuance

through usual auctions. Therefore, the MOF decides on the BOJ rollover request amount based

on the annual JGB Issuance Plan, etc.

Sales for Households

Bank of Japan Rollover

FILP Bonds

Public Offering

Non-price Competitive Auction II and others

Adjustment between fiscal years

JGB Issuance Amount Planned for FY

(12.0)

Financed in the market

(128.8) (8.0) (9.7)

40-year, 30-year, 20-year, 10-year, 5-year, 2-year, Treasury Discount Bills, 10-year Inflation- Indexed Bonds, Liquidity Enhancement Auctions

40-year, 30-year, 20-year, 10-year, 5-year, 2-year, 10-year Inflation-Indexed Bonds

(trillion yen)

Note: figures may not sum up to the total because of rounding.

Fig.2-8 JGB Issuance Amount by Methods of Issuance

Chapter 1 Government Bonds (JGBs)

1 Primary Market for Government Bonds

(4) JGB Market Special Participants Scheme

Amid expectations that JGB issuance in large volumes will continue, the JGB Market Special

Participants Scheme was introduced in Japan in October 2004 to promote the market s stable

absorption of JGBs and to maintain and enhance the liquidity of the JGB market.

This scheme is designed based on the so-called Primary Dealer System introduced in major European

countries and the U.S. To achieve the abovementioned purpose of the scheme, the MOF grants special

entitlements to certain auction participants who carry out responsibilities essential to debt management

policies, such as active participation in JGB auctions. The following is an outline of the scheme.

A. Responsibilities of JGB Market Special Participants

Bidding responsibility:

In every auction, the Special Participants shall bid for an adequate amount (at least 5% of

the planned issue amount) at reasonable prices.

Purchasing responsibility:

The Special Participants shall purchase and underwrite at least a specified share of the

planned total issue amount (0.5% for short-term zone; and 1% for other zones) in each

of the super long-term, long-term, medium-term and short-term zones in auctions for the

preceding two quarters.

Responsibility in the secondary market:

The Special Participants shall provide sufficient liquidity to the JGB secondary market.

Provision of Information:

The Special Participants shall provide information on JGB markets and related transactions

to the MOF.

B. Entitlements of JGB Market Special Participants

Entitlement to participate in the Meeting of JGB Market Special Participants:

The Special Participants may participate in the Meeting of JGB Market Special Participants

to exchange opinions with the MOF.

Entitlement to participate in Non-Price-Competitive Auctions & :

The Special Participants may participate in Non-Price Competitive Auction I held

concurrently with a normal competitive auction and in Non-Price Competitive Auction

II held after a normal competitive auction. These auctions enable Special Participants

to obtain JGBs at the weighted average accepted price in a competitive auction (or at

the issuance price in a Dutch-style auction) up to the maximum amount preset for each

Participant on the basis of the amount of past successful bids (Non-Price Competitive

Auction I) and past bids as a whole (Non-Price Competitive Auction II).

Entitlement to participate in Liquidity Enhancement Auctions:

The Special Participants may participate in Liquidity Enhancement Auctions that are

designed to maintain and enhance the liquidity of the JGB market.

Entitlement to participate in Auctions for Buy-backs:

The Special Participants may participate in Auctions for Buy-backs.

Entitlement to apply for separating and integrating STRIPS Bonds:

The Special Participants may apply for the separation and integration of STRIPS Bonds.

Chapter 1 Government Bonds (JGBs)

1 Primary Market for Government Bonds

(5) Government Bond Administration

A. Items the Bank of Japan handles

The government does not directly undertake the government bond-related administrative

tasks, such as issuance and redemption, but entrusts the BOJ with most of those tasks based

on Article 1, paragraph (2) of the Act on National Government Bonds. Those administrative

tasks entrusted to the BOJ are as follows ( ☞ ).

Issuance: The BOJ accepts bids from bidders in auctions, notifies amounts of bids accepted,

collects payments, issues the securities, and receives and handles revenues.

Redemption/interest payment: The BOJ pays principal and interests on JGBs, and receives

and handles funds to be used for redemption, and makes their disbursement.

B. The Bank of Japan government bond network system

The Bank of Japan operates the Bank of Japan Financial Network System (BOJ-NET) JGB

Services ( ☞① ) to efficiently and safely implement JGB issuance, redemption and other

administrative tasks as explained above and the settlement of JGB transactions with its

customer financial institutions.

Banks, securities companies, money market brokers, insurance companies, etc. participate

in the BOJ-NET JGB Services that implement JGB issuance, redemption and other

administrative tasks online.

Under the Act on Book-Entry Transfer of Corporate Bonds and Shares, at present, JGBs

traded between financial institutions are paperless. JGB transfers are done in the form of

transfers on accounts managed by the transfer institution (the Bank of Japan) ( ☞② ).

The BOJ-NET JGB Services allow the following procedures to be completed online:

Notification of offering (from the BOJ to auction participants)

Bidding (from bidders to the BOJ)

Counting the number of bidding and reporting to the MOF on total bidding

Notification of accepted/allocated bids (from the BOJ to bidders)

Issuance and payment (from the BOJ to purchasers / from purchasers to the BOJ)

☞① The BOJ-NET includes the BOJ-NET current account system as a fund settlement system and the BOJ-NET JGB Services as a JGB settlement system.

☞ The BOJ provides these government bond related ser- vices through its head office and branches, and through agent financial institutions.

☞② JGBs for this mecha^ - nism are called Book-entry transfer JGBs, representing those whose ownership is determined by descriptions or records in book-entry accounts as provided by the “Act on Book-Entry Transfer of Corpo- rate Bonds and Shares.” (JGB certificates are not issued.)

Chapter 1 Government Bonds (JGBs)

1 Primary Market for Government Bonds

C. Auction procedures for public offering auction

(Media) (Bank of Japan) (Qualified auction participants)

Market

Market trends and investors’ demand research

About 3 months

before auction

About 1 week

before auction

Till the day

before auction

Day of Auction

Determination of coupon rate (Note 1)

Release of the auction information

Instruction

Determination of successful bids

Auction announcement

Bid closing

(Ministry of Finance)

Determination of issue date and amount

Determination of auction date

Release of the auction result

Notification of the successful bids

Bidders

Determination of successful bids

Release of the auction result

Bid closing

Bidding

Auction announcement

Notification of the successful bids

Bidders

Bidding

(Note 2)

Press release

Press release

Press release

Press release

Press release

Non-Price Competitive Auction II

Note1: Treasury Discount Bills are discount bonds and have no coupon rates. Note2: Successful bids in a Liquidity Enhancement Auction are notified at 14:30. Note3: Time in parenthesis refers to the time for Treasury Discount Bills. Note4: Non-Price Competitive Auction II is not conducted for Inflation-Indexed Bonds and Treasury Discount Bills.

Fig.2-9 Auction Procedures for Public Offering Auction

Chapter 1 Government Bonds (JGBs)

1 Primary Market for Government Bonds

The development of the Inflation-Indexed Bonds (JGBi) market is a key issue for JGB Management Policy to

address market environment changes after overcoming deflation and promote the diversification of JGBs (Reference

This column introduces the major trend of the JGBi market and the MOF s relevant responses since FY2019.

(Reference 1) See Chapter 1 1(2) (Reference) Inflation-Indexed Bonds (P42) for an outline of Inflation-Indexed Bonds.

August-September 2019 Trend

Break-even inflation rates (BEIs), which followed a downtrend from the middle of 2018, weakened as nominal

bond yields plunged due to investors risk-off attitude that grew in response to the escalation of U.S.-China trade

disputes in August 2019 (Figs. c5-1 and c5-2 ). In Japan, particularly, the BEI remained below 0.1% as the yield

on JGBi failed to follow the nominal bond yield.

At the Meeting of JGB Market Special Participants under such situation in September 2019, many market

participant surged the MOF to increase the amount of Buy-backs, while maintaining the current amount of issuance

to improve the supply-demand balance for JGBi. Based on such opinion, the MOF switched from a 20 billion yen

bimonthly Buy-back (every even-numbered month) to a 20 billion yen monthly Buy-back for JGBi in the October-

December 2019 quarter.

The BOJ s outright JGBi purchase size (Reference 2) was also raised from 25 billion yen to 30 billion yen in

November.

(Reference 2) The BOJ conducts an outright JGBi purchase twice a month (See Monthly Schedule of Outright Purchases

of Japanese Government Bonds (Competitive Auction Method) released at every month-end on the BOJ Website).

❷ February-March 2020 Trend

After increased JGBi Buy-backs were implemented in the October-December quarter of 2019, Japan s BEI was

stabilized at around 0.2% around the turn of the year. As European and U.S. BEIs declined substantially in response

to the global novel coronavirus (COVID-19) outbreak expansion and crude oil price crashes from February 2020,

however, Japans BEI fell steeply, slipping far below 0% in mid-March, with JGBi prices dropping below par (Figs.

c5-1 and c5-2 ). As JGBi are guaranteed to be redeemed at par even in the event of deflation, their prices slip

below par indicated that the JGBi market was not working sufficiently.

At the Meeting of JGB Market Special Participants under such situation in March 2020, many market participants

stated that as inflation-indexed government bonds were globally sold, with their supply-demand balance

deteriorating, it would be desirable to cut or cancel JGBi issues, or substantially increase JGBi Buy-backs in the

April-June quarter. Based on such opinion, the MOF took the following measures:

The May issue size was cut to 300 billion yen from 400 billion yen planned in the FY2020 JGB Issuance Plan.

The monthly Buy-back size in the April-June quarter was increased to 50 billion yen from 20 billion yen.

An additional Buy-back worth 300 billion yen was conducted in March through the price-spread-competitive

(multi-price) auction method with a limit of bidding spread with the standard price.

Non-price competitive auction II was cancelled for the time being.

Column 5 Inflation-Indexed Bonds Trend

April-May 2020 Trend

These measures led JGBi prices to stop falling but the prices remained below par. As the key crude oil futures price plunged

into negative territory temporarily due to rapidly falling crude oil demand amid economic stagnation under the expanding

COVID-19 outbreak, a breakdown at a meeting of oil-producing countries on production cuts and potential oil storage capacity

shortages, the external environment for inflation-indexed government bonds deteriorated globally, with European and U.S. BEIs

entering a downtrend again. Japan s BEI then remained weak at around minus 0.2% (Figs. c5-1 and c5-2 ).

At the Meeting of JGB Market Special Participants under such situation in late April 2020, market participants stated that as the supply-

demand balance for inflation-indexed government bonds had substantially deteriorated due to their global selling associated with

investors risk-off attitude under the expanding COVID-19 outbreak, declining market liquidity and weak crude oil prices, the planned

auction for a 300 billion yen JGBi issue in May could lead supply to far exceed demand. Based on such opinion, the MOF cut the May

JGBi issue size to 200 billion yen from 300 billion yen as set in March (with the Buy-back size kept unchanged). As market participants

warned that any cut in the JGBi issue size could lead the future continuity of JGBi to be doubted, the MOF noted that the JGBi issue

size cut responding to current market conditions was designed to secure the future stable issuance of JGBi.

After the auction for the May JGBi issue, the BEI turned positive.

Fig. c5-2 BEI Trend

Fig. c5-1 Country-by-Country BEI and Crude Oil Price Trends

Chapter 1 Government Bonds (JGBs)

1 Primary Market for Government Bonds

Government Debt Issuances Growing Due to the Novel Coronavirus Expansion

As the Novel Coronavirus (COVID-19) expansion has exerted huge impacts on the world economy, foreign

countries have come up with economic assistance packages. Subsequently, they have been forced to raise more

funds by changing government bond issuance plans and increasing government bond issuances substantially from

the previous year.

In Japan, the first supplementary budget for FY2020 was enacted in April 2020 and the second one in June 2020,

leading the planned FY2020 JGB issuance amount to increase by 99.8 trillion yen from the initially planned level (as

of June 2020).

The U.S., Germany and France rapidly increased discount bond issuances from March or April 2020, indicating

that they were exploiting discount bonds to quickly raise funds (Fig. c6-3). Bond issuances increased mainly in

the 7-year for the U.S., in the 1- to 7-year zone for the U.K. and in the 7- to 15-year zone for Germany (Fig. c6-4).

The U.K. nearly quadrupled the frequency of April-July government bond auctions from the initially planned level,

while Germany introduced 7- and 15-year government bonds. Foreign countries have thus used various devices to

expand government bond issuances.

Fig.c6-2 Announcement Time of Issuance Amount and Auction Date in Japan and Foreign Countries

Japan U.S. U.K. Germany France

In previous fiscal year

Quarterly basis * Auction date of each month is announced 3 months before.

Approximately one week before

Note 1: As for issuance lots per auction announced in the previous fiscal year, the fixed amounts are announced one week before in Japan and again every quarter in Germany. Note 2: Planned quarterly amounts financed from the market. Note 3: Scheduled auction date is announced again every quarter. (Source) Relevant countries’ debt management authorities

Scheduled auction date (*3)

Scheduled auction date (*3)

Planned auction amount (*1)

Total issuance amount

Total issuance amount

Total issuance amount

Total issuance amount

Total issuance amount (*2)

Issues Issues

Issues

Issues

Issues

Planned auction amount Planned auction amount

Planned auction amount

Planned auction amount

Planned auction amount

Scheduled auction date

Scheduled auction date

Scheduled auction date

Scheduled auction date

Planned auction amount (*1)

Scheduled auction date

Planned auction amout

Chapter 1 Government Bonds (JGBs)

1 Primary Market for Government Bonds

0

200

400

600

800

1,

1,

1,

1,

Oct Nov Dec Jan Feb Mar Apr May Jun Jul

Discount bond issuance amount (year-on-year change) Coupon-bearing bond issuance amount (year-on-year change)

(Unit: billion dollar)

2019

0

10

20

30

40

50

60

70

Oct Nov Dec Jan Feb Mar Apr May Jun Jul

Discount bond issuance amount (year-on-year change) Coupon-bearing bond issuance amount (year-on-year change)

No discount bond issuance plan from May has been released

2019 2020

(Unit: billion pound)

0

10

20

30

40

Oct Nov Dec Jan Feb Mar Apr May Jun

Discount bond issuance amount (year-on-year change) Coupon-bearing bond issuance amount (year-on-year change)

(Unit: billion euro)

2019 2020

0

5

10

15

Oct Nov Dec Jan Feb Mar Apr

Discount bond issuance amount (year-on-year change) Coupon-bearing bond issuance amount (year-on-year change)

2019 2020

(Unit: billion euro)

(2) (2) (*2)

No discount bond issuance plan from May has been released

【U.S.】 【U.K.】

【Germany】 【France】

2020

【U.S.】 (billion dollar)^ 【U.K.】 (billion pound) Changes 2-year 18.0 Issuance amount Frequency of auc�ons^ Issuance amount Frequency of auc�ons^ Issuance amount^ of aucFrequency�ons 3-year 18.0 1 ~5-year^ 3.25- 5-year 18.0 5 ~7-year 3-3. 7-year 27.0 7 ~year15- 3.3 1 17.6 4 13 7 ~year15- 2.75-3. 10-year 15.0 (^15) year~30- 2-2. 20-year 54.0 Over 30-year 1.75-2. 30-year 9.0 10-year orless 1.25-1. 8.0 Over 10-year 1-1. 1.0 9.5 3 58.5 17 180.0 49 168.0 (billion pounds) Issuance results for Apr.-June 2019

Issuance results for July-Sept. 2019

Issuance results for Oct.-Dec. 2019

Issuance results for Jan.-Mar. 2020

Issuance results for Apr.-June 2019

Issuance results for July-Sept. 2019

Issuance results for Oct.-Dec. 2019

Issuance results for Jan.-Mar. 2020

Issuance results for Apr. 2020 ▲ 229.1 126.0 39.9 240.6 2,673.0 ▲ 5.5 33.2 4.7 ▲ 24.4 12.

Issuance plans for May-July 2020

Coupon-bearing bonds 120.0 138.0 Issuance amount perauc�on 114.0 132.0 Coupon-bearing bonds 1 ~7 - year 3.

Issuance results for May-July 2019

Issuance plans for May-July 2020 Issuance results for April 2019^ Issuance results for April 2020

123.0 141. 96.0 123.

1 23.0 6 20

10 0.0 54. 51.0 60.0 Infla�on- Indexed Bonds

0.5 (^) - 2.0 1

90.0 (^) Over 15-year 2.3^1 15.8^6

Floa�ng Rate^6 Bonds 56.0^ 64. Infla�on-Indexed Bonds 40.0^ 41.0^ Total Total 675.0 843.

Discount Bonds Discount Bonds

【Germany】 (billion euro) 【France】 (billion euro) Ini�al issuance plan for April-June 2020

Revised issuance plan for April-June 2020 Changes^

Ini�al issuance plan for FY

Revised issuance plan for FY2020 Changes 2-year 13.0 15.0 2.0 (^) InCoupon-bearing bondsfla�on-Indexed Bonds 205.0 245.0 40. 5-year (^) 9.0 12.0 3.0 Discount Bonds (^) 10.0 64.1 54. 7-year 0.0 10.0 10. 10-year 14.0 17.0 3. 15-year 0.0 5.0 5. 30-year 3.5 3.0 ▲ 0. Subtotal 39.5 62.0 22. 3-month 2.0 12.0 10. 5-month 4.5 12.0 7. 6-month 9.0 12.0 3. 9-month 0.0 12.0 12. 11-month (^) 0.0 12.0 12. 12-month 0.0 12.0 12. Subtotal 15.5 72.0 56. 55.0 134.0 79.

Coupon-bearing bonds

Discount Bonds

Total Infla�on- Indexed Bonds (No revision from “6-8 billion euros a year” as published in the ini�al issuance plan)

Note 1: As of April-end 2020 (Some data include published data in May 2020 for the U.S. alone). Note 2: Components may not add up to the total because of rounding. Note 3: The data of discount bonds in the U.S., U.K., France are net issuance amount. The others are gross issuance amount. The U.S.’s Aplil-June discount bond issuance amount is es�mated by MOF. Note 4: Data for the U.K. are calculated on a revenue basis while data for the other countries are calculated on a nominal value basis. Note 5: Infla�on-Indexed Bonds worth 500 million pounds out of April 2019 issuances and coupon-bearing bonds worth about 3. billion pounds out of April 2020 issuances in the U.K. were subjected to gilt tenders that differ from ordinary auc�ons (reopening exis�ng bonds to supplement ordinary compe��ve auc�ons). Note 6: Germany’s May-June coupon-bearing bond issuance amount includes unpublished syndica�on issues (a 15-year issue and a 30-year issue) that are es�mated as the same as those planned for the latest month. (Sources) Relevant countries’ debt management authori�es

Issuance results for Apr.-June 2020

Note 1: Coupon-bearing bond include Inflation-Indexed Bonds, floating-rate bonds (for the U.S. alone) and Green Bonds (for France alone). Note 2: As of April 2020. Data represent results for October 2019 to April 2020 and plans for May-July 2020 for countries where plans are made available. Note 3: No discount bond issuance plans for May-July 2020 have been released in the U.S. and the U.K. As the U.K. has released only a total coupon- bearing bond issuance amount for the May-July 2020 period, the MOF has estimated monthly amounts. Note 4: Germany’s May-June coupon-bearing bond issuance amount includes unpublished syndication issues (a 15-year issue and a 30-year issue) that are estimated as the same as those planned for the latest month. Its monthly inflation-indexed bond issuance amount for the period is estimated at 580 million euros based on the planned annual issuance amount at 6-8 billion euros. (Sources) Websites of these countries’ respective government debt management authorities

【U.S.】 (billion dollar) 【U.K.】 Changes 2-year 18.0 Issuance amount Frequency of auc�ons Issuance amount Frequency of auc�ons Issuance amo 3-year 18. 5-year 18. 7-year 27. 7 ~15- year 3.3 1 17.6 4 10-year 15. 20-year 54. 30-year 9.

1.0 9.5 3 58.5 17 168.0 (billion p Issuance results for Apr.-June 2019

Issuance results for July-Sept. 2019

Issuance results for Oct.-Dec. 2019

Issuance results for Jan.-Mar. 2020

Issuance results for Apr.-June 2019

Issuance results for July-Sept. 2019

Issuance results for Oct.-Dec. 2019

Issuance results for Jan.-Mar. 2020

Issuance resu Apr. 202 ▲ 229.1 126.0 39.9 240.6 2,673.0 ▲ 5.5 33.2 4.7 ▲ 24.

Iss

Coupon-bearing bonds

120.0 138. 114.0 132.0 Coupon-bearing bonds 1 ~7 - year

Issuance results for May-July 2019

Issuance plans for May-July 2020 Issuance results for April 2019^ Issuance results for April 2020

123.0 141. 96.0 123.

1 23.0 6

0.0 54. 51.0 60.0 Infla�on- Indexed Bonds

0.5 - 2.0 1

90.0 (^) Over 15-year 2.3^1 15.8^6

Floa�ng Rate Bonds 56.0^ 64. Infla�on-Indexed Bonds 40.0^ 41.0^ Total Total 675.0 843.

Discount Bonds Discount Bonds

【Germany】 (billion euro) 【France】 (billion euro) Ini�al issuance plan for April-June 2020

Revised issuance plan for April-June 2020 Changes Ini�al issuance plan for FY

Revised issuance plan for FY Changes 2-year 13.0 15.0 2.0 (^) InCoupon-bearing bondsfla�on-Indexed Bonds 205.0 245.0 40. 5-year 9.0 12.0 3.0 Discount Bonds 10.0 64.1 54. 7-year (^) 0.0 10.0 10. 10-year 14.0 17.0 3. 15-year 0.0 5.0 5. 30-year 3.5 3.0 ▲ 0. Subtotal 39.5 62.0 22. 3-month 2.0 12.0 10. 5-month 4.5 12.0 7. 6-month (^) 9.0 12.0 3. 9-month 0.0 12.0 12. 11-month 0.0 12.0 12. 12-month 0.0 12.0 12. Subtotal 15.5 72.0 56. 55.0 134.0 79.

Coupon-bearing bonds

Discount Bonds

Total Infla�on- Indexed Bonds

(No revision from “6-8 billion euros a year” as published in the ini�al issuance plan)

Note 1: As of April-end 2020 (Some data include published data in May 2020 for the U.S. alone). Note 2: Components may not add up to the total because of rounding. Note 3: The data of discount bonds in the U.S., U.K., France are net issuance amount. The others are gross issuance amount. The U.S.’s Aplil-June discount bond issuance amount is es�mated by MOF. Note 4: Data for the U.K. are calculated on a revenue basis while data for the other countries are calculated on a nominal value basis. Note 5: Infla�on-Indexed Bonds worth 500 million pounds out of April 2019 issuances and coupon-bearing bonds worth about 3. billion pounds out of April 2020 issuances in the U.K. were subjected to gilt tenders that differ from ordinary auc�ons (reopening exis�ng bonds to supplement ordinary compe��ve auc�ons). Note 6: Germany’s May-June coupon-bearing bond issuance amount includes unpublished syndica�on issues (a 15-year issue and a 30-year issue) that are es�mated as the same as those planned for the latest month. (Sources) Relevant countries’ debt management authori�es

Issuance results for Apr.-June 2020

【U.S.】 (billion dollar) 【U.K.】

Changes

2-year 18.0 Issuance amount Frequency of auc�ons Issuance amount Frequency of auc�on

3-year 18.

5-year 18.

7-year 27. 7 ~15- year 3.3 1 17.

10-year 15.

20-year 54.

30-year 9.

1.0 9.5 3 58.5 1

Issuance results for Apr.-June 2019

Issuance results for July-Sept. 2019

Issuance results for Oct.-Dec. 2019

Issuance results for Jan.-Mar. 2020

Issuance results for Apr.-June 2019

Issuance results for July-Sept. 2019

Issuance results for Oct.-Dec. 2019

Issuance results fo Jan.-Mar. 2020 ▲ 229.1 126.0 39.9 240.6 2,673.0 ▲ 5.5 33.2 4.7 ▲ 24.

Coupon-bearing bonds

114.0 132.0 Coupon-bearing bonds 1 ~7 - year

Issuance results for May-July 2019

Issuance plans for May-July 2020 Issuance results for April 2019 Issuance results for April 2020

1 23.

51.0 60.0 Infla�on- Indexed Bonds

0.5 - 2.

90.0 (^) Over 15-year 2.3 1 15.

Floa�ng Rate Bonds 56.0^ 64. Infla�on-Indexed Bonds 40.0^ 41.0^ Total Total 675.0 843.

Discount Bonds Discount Bonds

【Germany】 (billion euro) 【France】 (billion euro) Ini�al issuance plan for April-June 2020

Revised issuance plan for April-June 2020 Changes Ini�al issuance plan for FY

Revised issuance plan for FY Changes

2-year (^) 13.0 15.0 2.0 (^) InCoupon-bearing bondsfla�on-Indexed Bonds 205.0 245.0 40.

5-year 9.0 12.0 3.0 Discount Bonds 10.0 64.1 54.

7-year 0.0 10.0 10.

10-year 14.0 17.0 3.

15-year (^) 0.0 5.0 5.

30-year 3.5 3.0 ▲ 0.

Subtotal 39.5 62.0 22.

3-month (^) 2.0 12.0 10.

5-month 4.5 12.0 7.

6-month 9.0 12.0 3.

9-month 0.0 12.0 12.

11-month (^) 0.0 12.0 12.

12-month 0.0 12.0 12.

Subtotal 15.5 72.0 56.

55.0 134.0 79.

Coupon-bearing bonds

Discount Bonds

Total Infla�on- Indexed Bonds

(No revision from “6-8 billion euros a year” as published in the ini�al issuance plan)

Note 1: As of April-end 2020 (Some data include published data in May

2020 for the U.S. alone).

Note 2: Components may not add up to the total because of rounding.

Note 3: The data of discount bonds in the U.S., U.K., France are net

issuance amount. The others are gross issuance amount. The U.S.’s

Aplil-June discount bond issuance amount is es�mated by MOF.

Note 4: Data for the U.K. are calculated on a revenue basis while data for

the other countries are calculated on a nominal value basis.

Note 5: Infla�on-Indexed Bonds worth 500 million pounds out of April

2019 issuances and coupon-bearing bonds worth about 3.

billion pounds out of April 2020 issuances in the U.K. were

subjected to gilt tenders that differ from ordinary auc�ons

(reopening exis�ng bonds to supplement ordinary compe��ve

auc�ons).

Note 6: Germany’s May-June coupon-bearing bond issuance amount

includes unpublished syndica�on issues (a 15-year issue and a

30-year issue) that are es�mated as the same as those planned

for the latest month.

(Sources) Relevant countries’ debt management authori�es

Issuance results for Apr.-June 2020

Fig.c6-3 Government Bond Issuance Changes Accompanying COVID-19 Expansion in Foreign

Countries (Trends of Year-on-Year Changes)

Fig.c6-4 Government Bond Issuance Changes Accompanying COVID-19 Expansion in Foreign

Countries (Trends by Maturity and Issue)

Chapter 1 Government Bonds (JGBs)

1 Primary Market for Government Bonds