Download Bond Interest and Amortization Problems and more Study notes Accounting in PDF only on Docsity!

CHAPTER 15

Long-Term Liabilities

ASSIGNMENT CLASSIFICATION TABLE

Study Objectives Questions

Brief Exercises Exercises

A Problems

B Problems

*1. Explain why bonds are issued.

1, 2, 3, 4, 5

1 1, 2

*2. Prepare the entries for the issuance of bonds and interest expense.

6, 7, 8 2, 3, 4 3, 4, 5, 6, 7, 8

1A, 2A, 5A, 6A, 9A

1B, 2B, 5B, 6B, 9B

*3. Describe the entries when bonds are redeemed or converted.

9, 10 5 5, 6, 8, 9, 18, 19

1A, 2A, 9A 1B, 2B, 9B

*4. Describe the accounting for long-term notes payable.

11 6 10, 11 3A 3B

*5. Contrast the accounting for operating and capital leases.

12, 13, 14 7 12 4A 4B

- Identify the methods for the presentation and analysis of long-term liabilities.

15 8 13, 14 1A, 2A, 7A, 8A

1B, 2B, 7B, 8B

*7. Compute the market price of a bond.

18 9 15

*8. Apply the effective-interest method of amortizing bond discount and bond premium.

16, 17 10 16, 17 5A, 6A 5B, 6B

*9. Apply the straight-line method of amortizing bond discount and bond premium.

19, 20 11, 12 18, 19 7A, 8A, 9A 7B, 8B, 9B

Note: All asterisked Questions, Exercises, and Problems relate to material contained in the appendixto the chapter.

ASSIGNMENT CHARACTERISTICS TABLE

Problem Number Description

Difficulty Level

Time Allotted (min.)

1A Prepare entries to record issuance of bonds, interest accrual, and bond redemption.

Moderate 20–

2A Prepare entries to record issuance of bonds, interest accrual, and bond redemption.

Moderate 15–

3A Prepare installment payments schedule and journal entries for a mortgage note payable.

Moderate 20–

4A Analyze three different lease situations and prepare journal entries.

Moderate 20–

5A Prepare entries to record issuance of bonds, payment of interest, and amortization of bond premium using effective-interest method.

Moderate 30–

6A Prepare entries to record issuance of bonds, payment of interest, and amortization of discount using effective- interest method. In addition, answer questions.

Moderate 30–

*7A Prepare entries to record issuance of bonds, interest accrual, and straight-line amortization for two years.

Simple 30–

*8A Prepare entries to record issuance of bonds, interest, and straight-line amortization of bond premium and discount.

Simple 30–

*9A Prepare entries to record interest payments, straight-line premium amortization, and redemption of bonds.

Moderate 30–

1B Prepare entries to record issuance of bonds, interest accrual, and bond redemption.

Moderate 20–

2B Prepare entries to record issuance of bonds, interest accrual, and bond redemption.

Moderate 15–

3B Prepare installment payments schedule and journal entries for a mortgage note payable.

Moderate 20–

4B Analyze three different lease situations and prepare journal entries.

Moderate 20–

5B Prepare entries to record issuance of bonds, payment of interest, and amortization of bond discount using effective-interest method.

Moderate 30–

BLOOM’S TAXONOMY TABLE

15-

Study Objective^ Correlation Chart between Bloom’s Taxonomy, Study Objectives and End-of-Chapter Exercises and Problems

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

Explain why bonds are issued.

Q15-

Q15-3Q15-2Q15-

E15-1Q15-

BE15-

E15-

of bonds and interest expense.Prepare the entries for the issuance

Q15-8Q15-

E15-5E15-4E15-3BE15-4BE15-3BE15-2Q15-

P15-6AP15-5AP15-2AP15-1AE15-8E15-7E15-

P15-9BP15-6BP15-5BP15-2BP15-1BP15-9A

redeemed or converted.Describe the entries when bonds are

Q15-

E15-6E15-5BE15-5Q15-

P15-2BP15-1BP15-9BP15-9A

E15-19E15-18P15-2AP15-1A

notes payable.Describe the accounting for long-term

E15-8BE15-6Q15-

E15-11E15-10E15-

P15-3BP15-3A

and capital leases.Contrast the accounting for operating

Q15-13Q15-

E15-12BE15-7Q15-

P15-4BP15-4A

long-term liabilities.presentation and analysis ofIdentify the methods for the

Q15-

P15-1AE15-14E15-13BE15-

P15-1BP15-8AP15-7AP15-2A

P15-8BP15-7BP15-2B

*7. Compute the market price of a bond.

Q15-

BE15-

E15-

*8. bond premium.of amortizing bond discount and^ Apply the effective-interest method

Q15-17Q15-

E15-17E15-16BE15-

P15-5BP15-6AP15-5A

P15-6B

*9. premium.amortizing bond discount and bond^ Apply the straight-line method of

Q15-

E15-18BE15-12BE15-11Q15-

P15-9AP15-8AP15-7AE15-

P15-9BP15-8BP15-7B

Broadening Your Perspective

Exploring the WebCommunication

Comp. Analysis

OrganizationAcross theDecision MakingFinancial Reporting

Ethics CaseAll About You

ANSWERS TO QUESTIONS

- (a) Long-term liabilities are obligations that are expected to be paid after one year. Examples include bonds, long-term notes, and lease obligations. (b) Bonds are a form of interest-bearing notes payable used by corporations, universities, and governmental agencies.

- (a) The major advantages are: (1) Stockholder control is not affected—bondholders do not have voting rights, so current stockholders retain full control of the company. (2) Tax savings result—bond interest is deductible for tax purposes; dividends on stock are not. (3) Earnings per share may be higher—although bond interest expense will reduce net income, earnings per share on common stock will often be higher under bond financing because no additional shares of common stock are issued. (b) The major disadvantages in using bonds are that interest must be paid on a periodic basis and the principal (face value) of the bonds must be paid at maturity.

- (a) Secured bonds have specific assets of the issuer pledged as collateral. In contrast, unse- cured bonds are issued against the general credit of the borrower. These bonds are called debenture bonds. (b) Term bonds mature at a single specified future date. In contrast, serial bonds mature in installments. (c) Registered bonds are issued in the name of the owner. In contrast, bearer (coupon) bonds are issued to bearer and are unregistered. Holders of bearer bonds must send in coupons to receive interest payments. (d) Convertible bonds may be converted into common stock at the bondholders’ option. In contrast, callable bonds are subject to call and retirement at a stated dollar amount prior to maturity at the option of the issuer.

- (a) Face value is the amount of principal due at the maturity date. (Face value is also called par value.) (b) The contractual interest rate is the rate used to determine the amount of cash interest the borrower pays and the investor receives. This rate is also called the stated interest rate because it is the rate stated on the bonds. (c) A bond indenture is a legal document that sets forth the terms of the bond issue. (d) A bond certificate is a legal document that indicates the name of the issuer, the face value of the bonds, and such other data as the contractual interest rate and maturity date of the bonds.

- The two major obligations incurred by a company when bonds are issued are the interest payments due on a periodic basis and the principal which must be paid at maturity.

- Less than. Investors are required to pay more than the face value; therefore, the market interest rate is less than the contractual rate.

- $28,000. $800,000 X 7% X 1/2 year = $28,000.

- $860,000. The balance of the Bonds Payable account minus the balance of the Discount on Bonds Payable account (or plus the balance of the Premium on Bonds Payable account) equals the carrying value of the bonds.

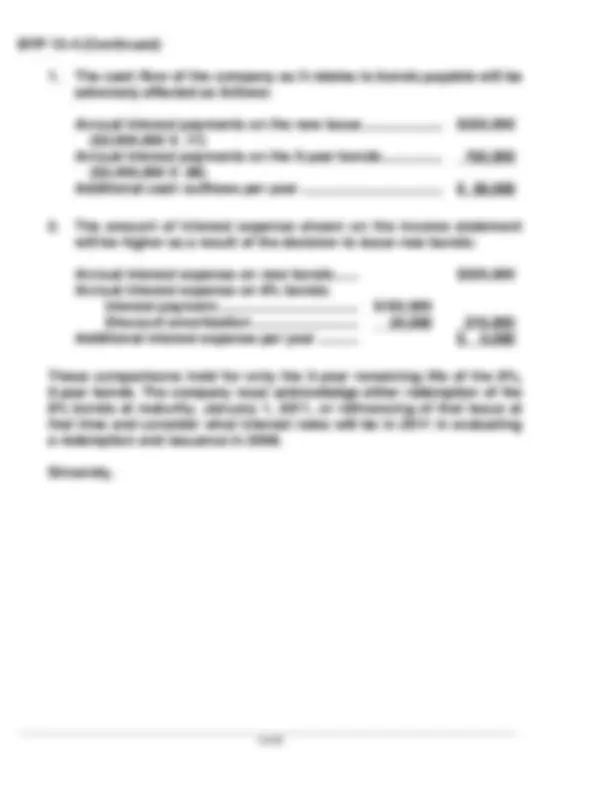

Questions Chapter 15 (Continued)

*18. No, Tina is not right. The market price of any bond is a function of three factors: (1) The dollar amounts to be received by the investor (interest and principal), (2) The length of time until the amounts are received (interest payment dates and maturity date), and (3) The market interest rate.

*19. The straight-line method results in the same amortized amount being assigned to Interest Expense each interest period. This amount is determined by dividing the total bond discount or premium by the number of interest periods the bonds will be outstanding.

*20. $28,000. Interest expense is the interest to be paid in cash less the premium amortization for the year. Cash to be paid equals 8% X $400,000 or $32,000. Total premium equals 5% of $400, or $20,000. Since this is to be amortized over 5 years (the life of the bonds) in equal amounts, the amortization amount is $20,000 ÷ 5 = $4,000. Thus, $32,000 – $4,000 or $28,000 equals interest expense for 2008.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 15-

Issue Stock Issue Bond Income before interest and taxes Interest ($2,000,000 X 8%) Income before income taxes Income tax expense (30%) Net income (a)

Outstanding shares (b) Earnings per share (a) ÷ (b)

Net income is higher if stock is used. However, earnings per share is lower than earnings per share if bonds are used because of the additional shares of stock that are outstanding.

BRIEF EXERCISE 15-

(a) Jan. 1 Cash ......................................................... 3,000, Bonds Payable ............................. 3,000, (3,000 X $1,000)

(b) July 1 Bond Interest Expense....................... 120, Cash................................................. 120, ($3,000,000 X 8% X 1/2)

(c) Dec. 31 Bond Interest Expense....................... 120, Bond Interest Payable ............... 120, ($3,000,000 X 8% X 1/2)

BRIEF EXERCISE 15-

Semiannual Interest Period

(A)

Cash Payment

(B)

Interest Expense (D) X 5%

(C)

Reduction of Principal (A) – (B)

(D)

Principal Balance (D) – (C) Issue Date 1 $48,145 $30,000 $18,

Dec. 31 Cash........................................................................ 600, Mortgage Notes Payable ......................... 600,

June 30 Interest Expense................................................. 30, Mortgage Notes Payable.................................. 18, Cash ............................................................... 48,

BRIEF EXERCISE 15-

- Rent Expense ................................................................... 80, Cash............................................................................ 80,

- Leased Asset—Building ............................................... 700, Lease Liability ......................................................... 700,

BRIEF EXERCISE 15-

Long-term liabilities Bonds payable, due 2010 ............................................. $500, Less: Discount on bonds payable............................ 45,000 $455, Notes payable, due 2013............................................... 80, Lease liability.................................................................... 70, Total long-term liabilities..................................... $605,

*BRIEF EXERCISE 15-

(b) i = 10% ? $10,

Discount rate from Table 15 A-1 is .46651 (8 periods at 10%). Present value of $10,000 to be received in 8 periods discounted at 10% is therefore $4,665. ($10,000 X .46651).

(b) i = 8%

? $20,000 $20,000 $20,000 $20,000 $20,000 $20,

Discount rate from Table 15 A-2 is 4.62288 (6 periods at 8%). Present value of 6 payments of $20,000 each discounted at 8% is therefore $92,457.60 ($20,000 X 4.62288).

*BRIEF EXERCISE 15-

(a) Interest Expense ............................................................. 46, Discount on Bonds Payable............................... 1, Cash ........................................................................... 45,

(b) Interest expense is greater than interest paid because the bonds sold at a discount which must be amortized over the life of the bonds. The bonds sold at a discount because investors demanded a market interest rate higher than the contractual interest rate.

(c) Interest expense increases each period because the bond carrying value increases each period. As the market interest rate is applied to this bond carrying amount, interest expense will increase.

SOLUTIONS TO EXERCISES

EXERCISE 15-

- True.

- True.

- False. When seeking long-term financing, an advantage of issuing bonds over issuing common stock is that tax savings result.

- True.

- False. Unsecured bonds are also known as debenture bonds.

- False. Bonds that mature in installments are called serial bonds.

- True.

- True.

- True.

- True.

EXERCISE 15-

Plan One Issue Stock

Plan Two Issue Bonds Income before interest and taxes Interest ($2,700,000 X 10%) Income before taxes Income tax expense (30%) Net income Outstanding shares Earnings per share

EXERCISE 15-

(a) Jan. 1 Cash ................................................................. 500, Bonds Payable..................................... 500,

(b) July 1 Bond Interest Expense .............................. 25, Cash ($500,000 X 10% X 1/2)........... 25,

(c) Dec. 31 Bond Interest Expense .............................. 25, Bond Interest Payable....................... 25,

(b)

*($500,000 X .08 X 6/12)

EXERCISE 15-

(a) Jan. 1 Bond Interest Payable................................ 72, Cash ........................................................ 72,

(b) Jan 1 Bonds Payable ............................................. 600, Loss on Bond Redemption ...................... 24, Cash ($600,000 X 1.04)...................... 624,

(c) July 1 Bond Interest Expense .............................. 45, Cash ($1,000,000 X 9% X 1/2).......... 45,

EXERCISE 15-

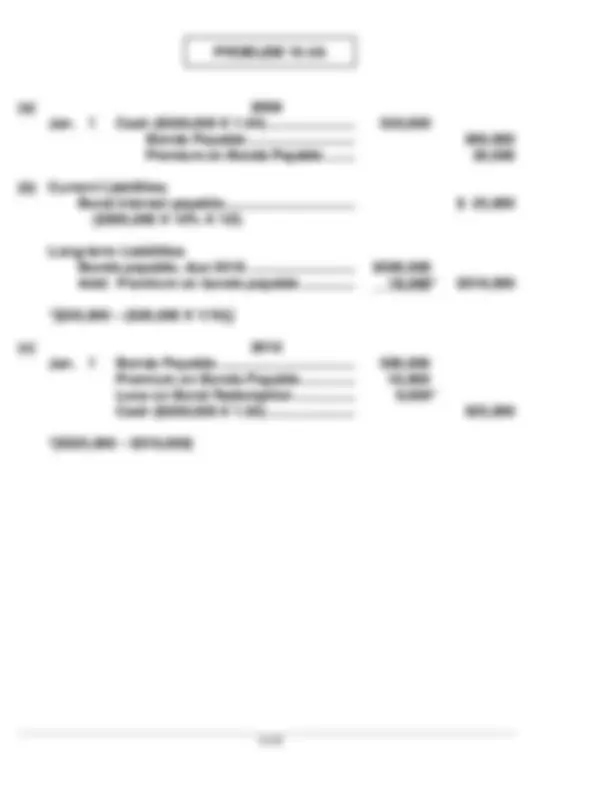

- June 30 Bonds Payable ............................................ 130, Loss on Bond Redemption ..................... 15, ($132,600 – $117,500) Discount on Bonds Payable .......... 12, ($130,000 – $117,500) Cash ($130,000 X 102%).................. 132,

- June 30 Bonds Payable ............................................ 150, Premium on Bonds Payable................... 1, Gain on Bond Redemption............. 4, ($151,000 – $147,000) Cash ($150,000 X 98%) .................... 147,

- Dec. 31 Bonds Payable ............................................ 20, Common Stock .................................. 3, ($5 X 20* X 30) Paid-in Capital in Excess of Par Value ......................................... 17,

*($20,000 ÷ $1,000)

Note: As per the textbook, the market value of the stock is ignored in the conversion.

EXERCISE 15-11 (Continued)

(b) Current: $17, [$20,000 – ($283,680 X 8% X 6/12)] + [$20,000 – ($275,027 X 8% X 6/12)]

Long-term: $266,028 [($300,000 – $8,000 – $8,320) – $17,652]

EXERCISE 15-

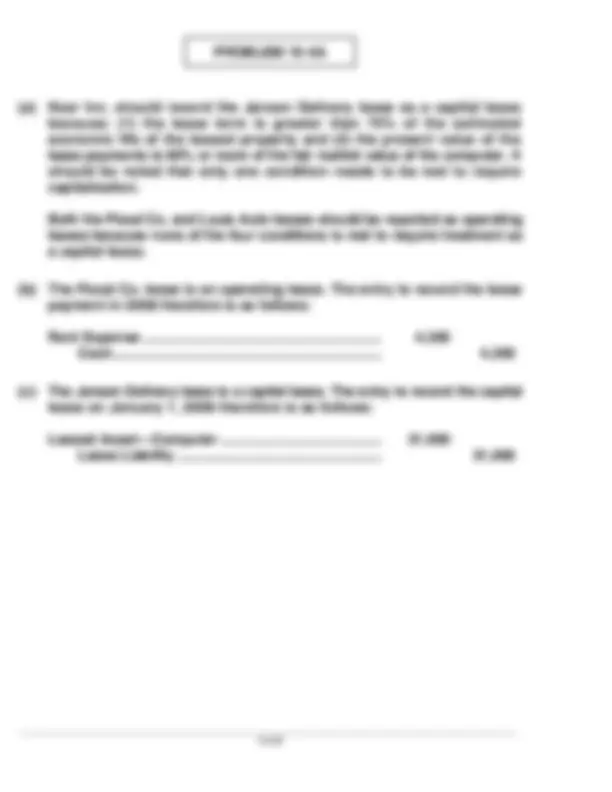

(a) Car Rental Expense .................................... 500 Cash ........................................................ 500

(b) Jan. 1 Leased Equipment ...................................... 74, Lease Liability...................................... 74,

EXERCISE 15-

Long-term liabilities Bonds payable, due 2013 ..................................... $180, Add: Premium on bonds payable..................... 32,000 $212, Lease liability ........................................................... 89, Total long-term liabilities............................. $301,

EXERCISE 15-

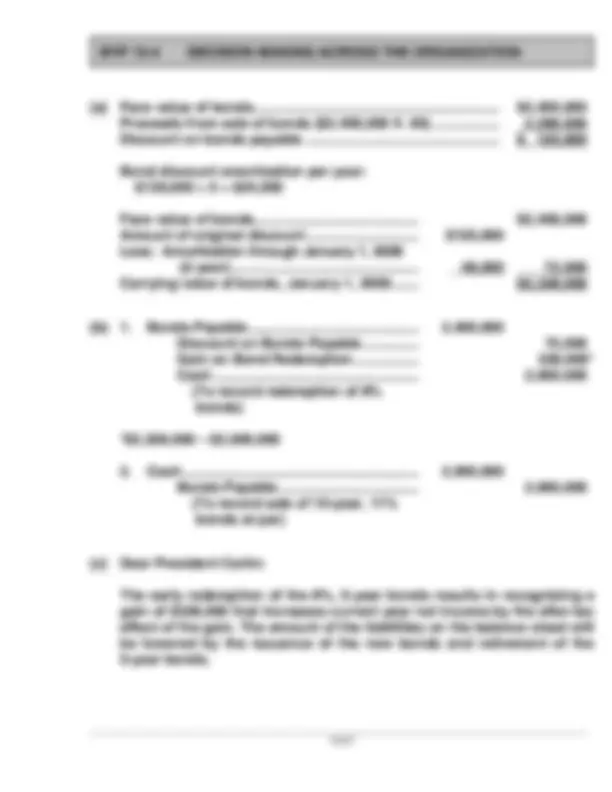

(a) Total assets ....................................................................... $1,000, Less: Total liabilities ..................................................... 620, Total stockholders’ equity ............................................ $ 380,

Total liabilities $620, (b) Debt to total assets ratio = Total assets

Net income + Income tax expense + Interest expense (c) Times interest earned ratio = Interest expense

$150,000 + $100,000 + $7,

$7, = 36.7 times

($562,613 X 5%)

- BRIEF EXERCISE 15-

- (a) Jan. 1 Cash ($2,000,000 X .97)....................... 1,940, - Discount on Bonds Payable 60, - Bonds Payable.............................. 2,000,

- (b) Jan. 1 Cash ($2,000,000 X 1.04) 2,080, - Bonds Payable.............................. 2,000, - Premium on Bonds Payable....... 80,

- BRIEF EXERCISE 15-

- Jan. 1 Cash (1,000 X $1,000) 1,000, - Bonds Payable.............................. 1,000,

- July 1 Cash ($800,000 X 1.02)........................ 816, - Bonds Payable.............................. 800, - Premium on Bonds Payable....... 16,

- Sept. 1 Cash ($200,000 X .98) 196,

- Discount on Bonds Payable 4,

- Bonds Payable.............................. 200,

- BRIEF EXERCISE 15-

- Bonds Payable.................................................................... 1,000,

- Loss on Bond Redemption............................................. 70,

- Discount on Bonds Payable.................................. 60,

- Cash ($1,000,000 X 101%) 1,010,

- *BRIEF EXERCISE 15-

- (a) Jan. 1 Cash (.96 X $5,000,000) 4,800, - Discount on Bonds Payable.............. 200, - Bonds Payable 5,000,

- (b) July 1 Bond Interest Expense 235, - Discount on Bonds Payable........ 10, - Cash.................................................. 225,

- *BRIEF EXERCISE 15- ($5,000,000 X 9% X 1/2)

- (a) Cash (1.02 X $3,000,000)......................................... 3,060, - Bonds Payable 3,000, - Premium on Bonds Payable 60,

- (b) Bond Interest Expense............................................ 144,

- Premium on Bonds Payable 6,

- Cash ($3,000,000 X 10% X 1/2) 150, ($60,000 ÷ 10)

- EXERCISE 15-

- (a) Jan. 1 Cash 300, - Bonds Payable 300,

- (b) July 1 Bond Interest Expense............................... 12, - Cash ($300,000 X 8% X 1/2).............. 12,

- (c) Dec. 31 Bond Interest Expense............................... 12, - Bond Interest Payable 12,

- EXERCISE 15-

- (a)

- Jan. 1 Cash 400, - Bonds Payable 400,

- July 1 Bond Interest Expense 18, - Cash ($400,000 X 9% X 1/2) 18,

- Dec. 31 Bond Interest Expense 18, (c) - Bond Interest Payable...................... 18,

- (d)

- Jan. 1 Bonds Payable 400, - Cash 400,

- EXERCISE 15- - At

- (a) (1) Cash 1,000, - Bonds Payable............................................. 1,000, - At

- (2) Cash 980, - Discount on Bonds Payable 20, - Bonds Payable............................................. 1,000, - At

- (3) Cash 1,030, - Bonds Payable............................................. 1,000, - Premium on Bonds Payable.................... 30,

- (b) Bonds Payable 1,000, Retirement of bonds at maturity - Cash 1,000, - Retirement of bonds before maturity at

- (c) Bonds Payable 1,000, - Premium on Bonds Payable 9, - Cash 980, - Gain on Bond Redemption 29,

- (d) Bonds Payable 1,000, Conversion of bonds into common stock - Common Stock............................................ 300, - Paid-in Capital in Excess of Par Value 700,

- EXERCISE 15-

- (a) (1) Cash............................................................................ 485, - Discount on Bonds Payable............................... 15, - Bonds Payable 500,

- (2) Semiannual interest payments $200,

- Plus: Bond discount 15, ($20,000* X 10)

- Total cost of borrowing........................................ $215,

- Principal at maturity.............................................. $500, OR

- Semiannual interest payments 200,

- Cash to be paid to bondholders........................ 700, ($20,000 X 10)

- Cash received from bondholders 485,

- Total cost of borrowing........................................ $215,

- (b) (1) Cash............................................................................ 525, - Bonds Payable 500, - Premium on Bonds Payable 25,

- (2) Semiannual interest payments $200,

- Less: Bond Premium 25, ($20,000 X 10)

- Total cost of borrowing........................................ $175,

- Principal at maturity.............................................. $500, OR

- Semiannual interest payments 200,

- Cash to be paid to bondholders........................ 700, ($20,000 X 10)

- Cash received from bondholders 525,

- Total cost of borrowing........................................ $175,

- *EXERCISE 15-

- Present value of principal ($200,000 X .61391) $122,

- Present value of interest ($8,000 X 7.72173) 61,

- Market price of bonds............................................................. $184,

- *EXERCISE 15-

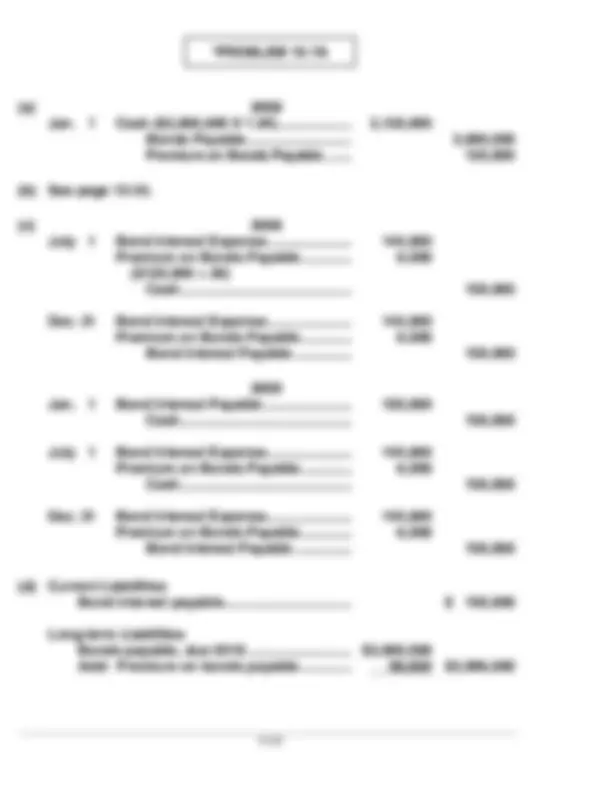

- (a) Jan. 1 Cash 562,

- Discount on Bonds Payable.................... 37,

- (b) July 1 Bond Interest Expense.............................. 28, - Discount on Bonds Payable........... 1, - Cash ($600,000 X 9% X 1/2)............. 27,

- (c) Dec. 31 Bond Interest Expense.............................. 28, - Discount on Bonds Payable........... 1, [($562,613 + $1,131) X 5%] - Bond Interest Payable 27,