Chapter 4

More Interest Formulas

1

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

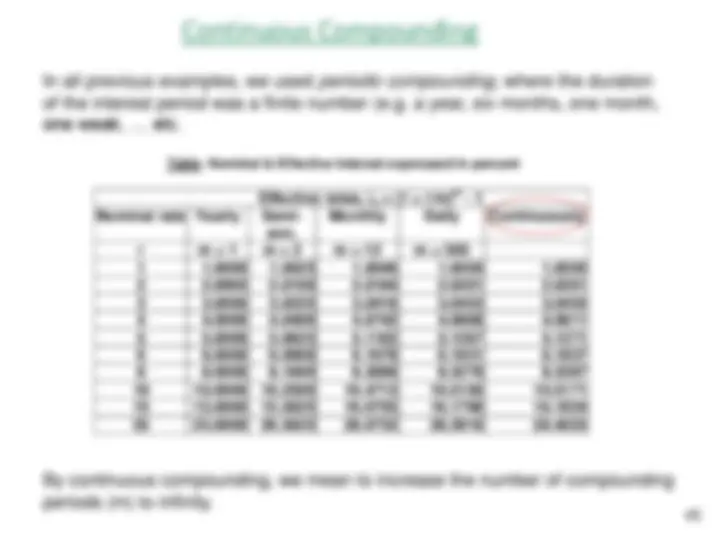

Formulas and examples for calculating Uniform Series Compound Amount, Present Worth, Capital Recovery and Sinking Fund Factors. It covers the relationships between compound interest factors and derivation of geometric gradient formula.

Typology: Slides

1 / 50

This page cannot be seen from the preview

Don't miss anything!

Uniform Series Compound Interest Formulas

Many payments are based on a uniform

payment series.

e.g. automobile loans, house payments, and

many other loans.

Amount A is invested at the end of each year for

four years A A A A

F

F = A(1+i)

3

2

F = A(1+i)

n-

n- + ….. + A( 1+i)

2

Multiply by (1+i)

(1+i)F = A(1+i)

n +A(1+i)

n-

3 +A(1+i)

2 +A(1+i)

…( 2)

Subtract eqn (1) from eqn (2) n

4

(1+i)F – F = A(1+i)

n

- A

i F = A[(1 + i )

n

- 1 ]

i

i F A

n

, %,

Where A(F/A, i%, n) is called uniform series

compound amount factor

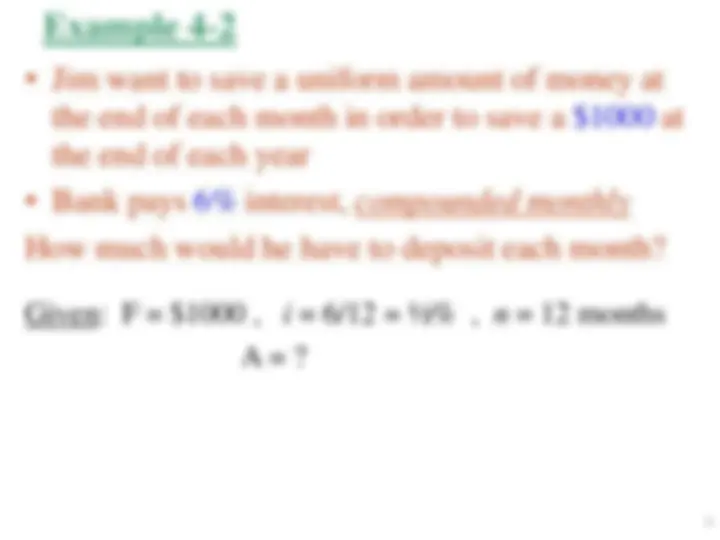

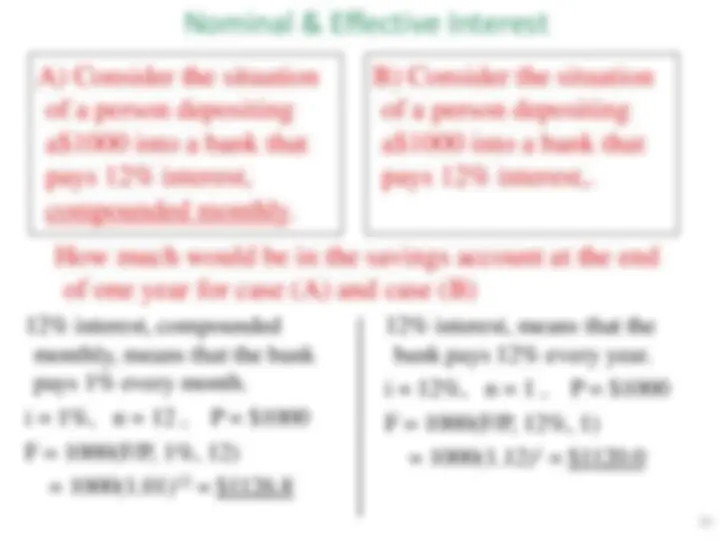

A man deposits $500 in a credit union at the end of

each year for 5 years. The credit union pays 5%

interest, compounded annually.

At the end of 5 years, immediately after the fifth

deposit, how much does the man have in his

account?

A = $500 , i = 5% , n = 5

A A A A

F

A

0 1 2 3 4 5 A A A A A

0 1 2 3 4 5

F

Man’s point of view Credit Union point of view

i

i A F n , %, 1 1

P A P i n i

i i A P n

n

10

A A^ A^ A^ A^ A^ A^ A

P

(^1) n

n

i

i A P i

Where P(A/P, i%, n) is called uniform series capital

recovery factor

Also, we can solve for P in terms of A

A P A i n i i

i P A n

n

, %, 1

Where A(P/A, i%, n) is called uniform series

present worth factor

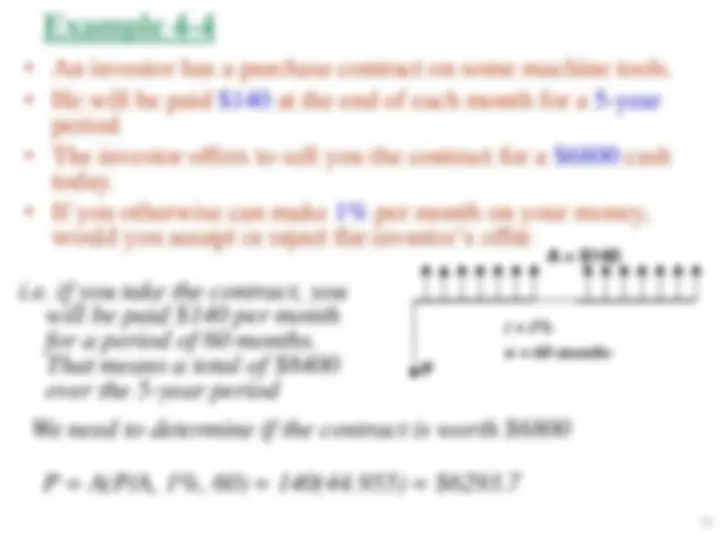

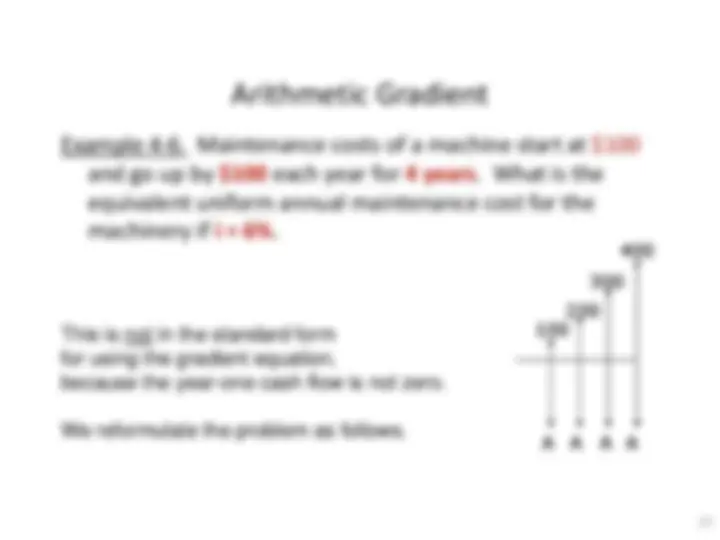

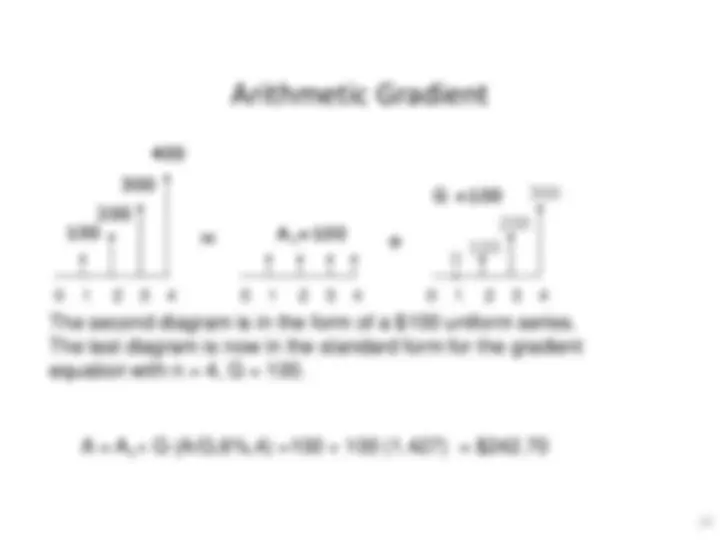

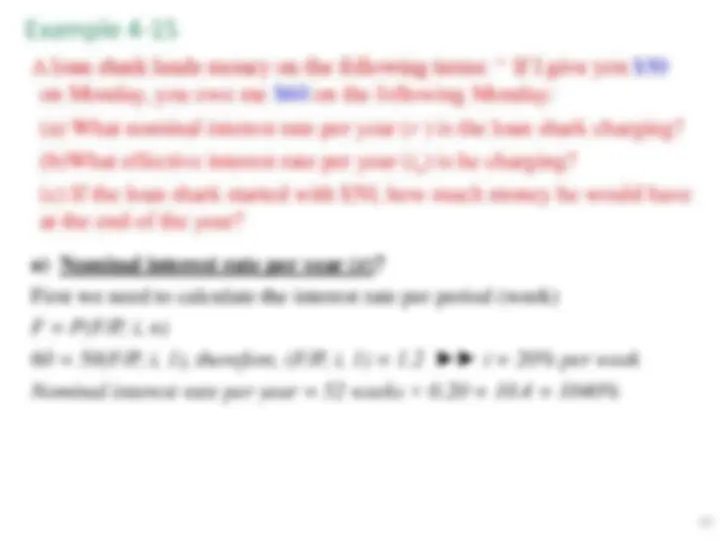

Example 4-

P

A = $

i = 1% n = 60 months

i.e. if you take the contract, you

will be paid $140 per month for a period of 60 months. That means a total of $ over the 5-year period

We need to determine if the contract is worth $

P = A(P/A, 1%, 60) = 140(44.955) = $6293.

… Example 4-

$140 per month, we will receive less than the 1% per month interest (which is the interest that we can otherwise make). Therefore the offer should be rejected.

equivalent to $6293.7. Therefore if we pay $6800 for a benefit of $140 per month, we will lose money

per month if invested at the given interest rate of 1%, which means that investing the $6800 in the purchase contract will be a loss when compared to investing it in in the other investment opportunity (which gives a 1% interest rate)

Therefore, Reject the offer.

100

F

100 100

20

P

30 20

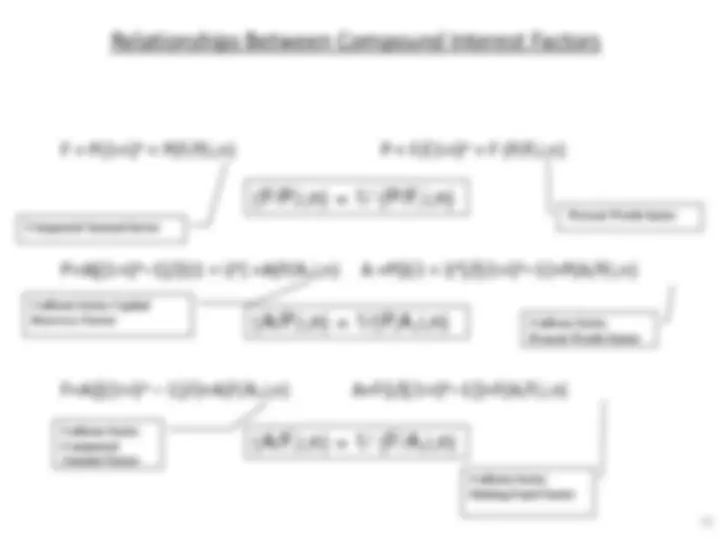

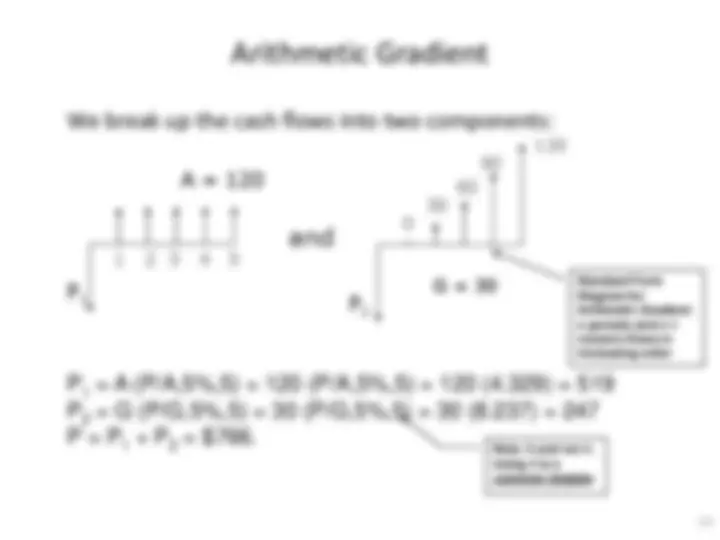

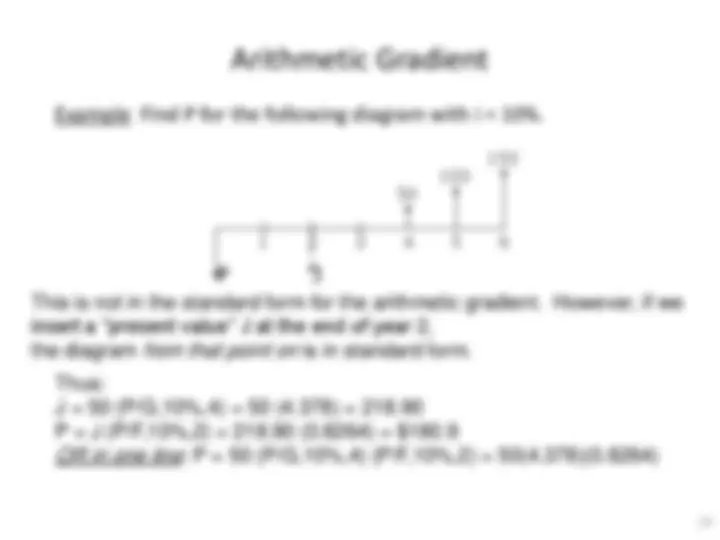

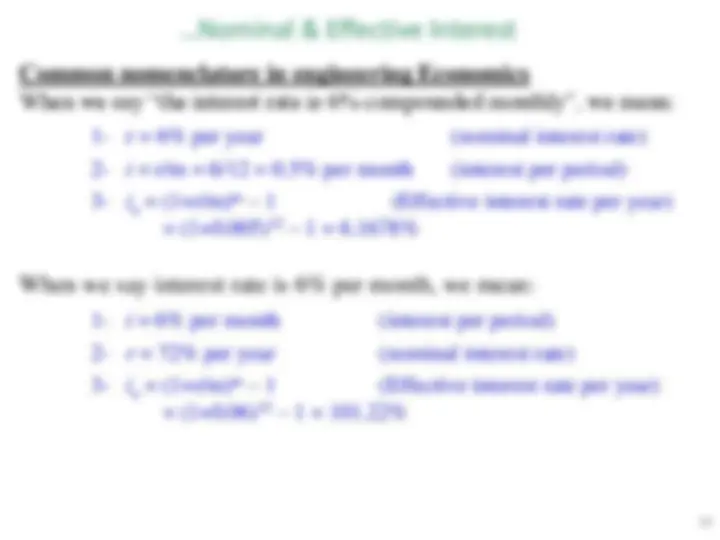

Relationships Between Compound Interest Factors

How?

P = A(1+ i)-1^ + A(1+ i)-2^ + ……+ A( 1 + i)-n

P = A[(1+ i)-1^ + (1+ i)-2^ +……+ ( 1+ i)-n^ ]

P = A[(P/F,i,1)+(P/F,i,2)+...+(P/F,i,n)]

since P = A(P/A, i, n)

We conclude that (P/A, i, n) = (P/F,i,1)+(P/F,i,2)+...+(P/F,i,n)

n

J

P A i n P F i J 1

( / , , ) ( / , , )

n

J

P A i n P F i J 1

( / , , ) ( / , , )

(^0 1 2 3) n

A A A A …..

P

For Example:

(P/A, 5%, 4) = (P/F, 5%, 1) + (P/F, 5%, 2) + (P/F, 5%, 3) + (P/F, 5%, 4)

Relationships Between Compound Interest Factors

1 1

( / ,, ) 1 ( / ,, )

n J

F Ain F Pi J

1

1

( / , , ) 1 ( / , , )

n

J

F A i n F P i J

0 1 2 3 n

A

F

A A A …..

F = A + A(1+ i) + A(1+ i)^2 + ……+ A( 1+ i)n-

F = A[ 1 + (1+ i) + (1+ i)^2 + ... + (1+ i)n-1^ ]

F = A[ 1 + (F/P,i,1) + (F/P,i,2) + ... + (F/P,i,n-1)]

since F = A(F/A,i,n)

We conclude that (F/A,i,n) = 1 + (F/P,i,1) + (F/P,i,2) + ... + (F/P,i,n-1)