Download Internal Control & Managing Cash and more Lecture notes Principles of Accounting in PDF only on Docsity!

Chapter 5 Internal Control & Managing Cash

Internal Control Characteristics of an effective internal control system include:

- (^) Competent, reliable, and ethical personnel

- (^) Assignment of responsibilities

- (^) Proper authorisation

- (^) Separation of duties Objective 3: The Bank Account as a Control Device Documents used to control a bank account include:

- (^) signature card

- (^) deposit slip

- (^) cheque

- (^) bank statement

- (^) Bank fees

- (^) Interest earned or paid on account

- (^) Dishonoured cheques, also known as Non-sufficient funds (NSF) cheques and bounced cheques. Steps in the Reconciliation Process

- (^) Step 1: Refer to the prior month’s bank reconciliation for any outstanding items (O/S deposits and cheques)

- (^) Step 2: Compare cash receipts journal amounts to the deposits on the bank statement (these will be credits on the bank statement)

- (^) Step 3: Check for ‘direct’ deposits on the bank statement that are not on the cash receipts journal

- (^) Step 4: Compare cash payments journal amounts to withdrawal amounts on the bank statement (these will be debits on the bank statement)

- (^) Step 5: Check for ‘direct’ withdrawals from the bank statement not recorded in the business’s cash payments

- (^) Step 6: Adjust for any errors made by the bank or by the business

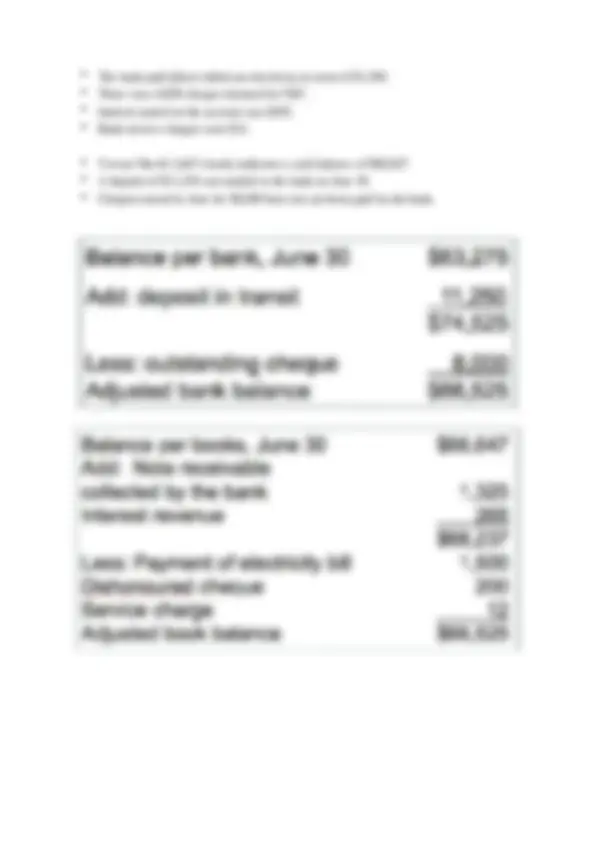

- (^) Step 7: Prepare the bank reconciliation Bank rec E.G./

- (^) At the beginning of July, Vervaci Bar & Grill received the June’s bank statement.

- (^) It indicated the following:

- (^) The bank balance was $63,275;

- (^) The bank had collected a note receivable from one of Vervaci’s customers in the amount of $1,325.

- (^) The bank paid (direct debit) an electricity account of $1,500.

- (^) There was a $200 cheque returned for NSF.

- (^) Interest earned on the account was $265.

- (^) Bank service charges were $12.

- (^) Vervaci Bar & Grill’s books indicates a cash balance of $66,647.

- (^) A deposit of $11,250 was mailed to the bank on June 30.

- (^) Cheques issued in June for $8,000 have not yet been paid by the bank.

Cash Short and Over Objective 4: Petty Cash Fund

- (^) On June 15, Donayella Vervaci decided to establish a $250 petty cash fund at the Vervaci Bar and Grill.

- (^) What is the entry?

- (^) Petty Cash is an Asset Account Cash in Draw/Tin + $ Sum of dockets = Petty Cash Fund e.g. ▪ (^) On June 20, she purchased supplies in the amount of $. ▪ (^) Bonatella also spent $20 for delivery charges and

lOMoARcPSD| Accounts Receivable – Valuation ▪ (^) Not all AR owing will be collected ▪ (^) Those not collected are a business expense ▪ (^) Uncollected AR amount = bad debt ▪ (^) AR are reported on the Balance Sheet at “Net Realisable Value” (NRV) ▪ (^) therefore need to estimate future bad debts in current period (to match current revenues with current expenses )…known as ‘ doubtful debts’ Accounting for Bad Debts

- Allowance method (matching principle)

- Direct write off method The Allowance Method

lOMoARcPSD| ▪ (^) Firms with significant credit sales will use the allowance method to measure bad debts ▪ (^) This makes an estimate of what debts will go bad based on experience ▪ (^) This is recorded in a contra account related to accounts receivable ▪ (^) Allowance for doubtful debts Two ways of allowance method

- Percentage of Sales

- Ageing of Accounts Receivable

lOMoARcPSD| Writing Off Bad Debts