Variable Costing and

Segment Reporting: Tools

for Management

CHAPTER 6

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

The content is very in depth and thorough.

Typology: Lecture notes

1 / 45

This page cannot be seen from the preview

Don't miss anything!

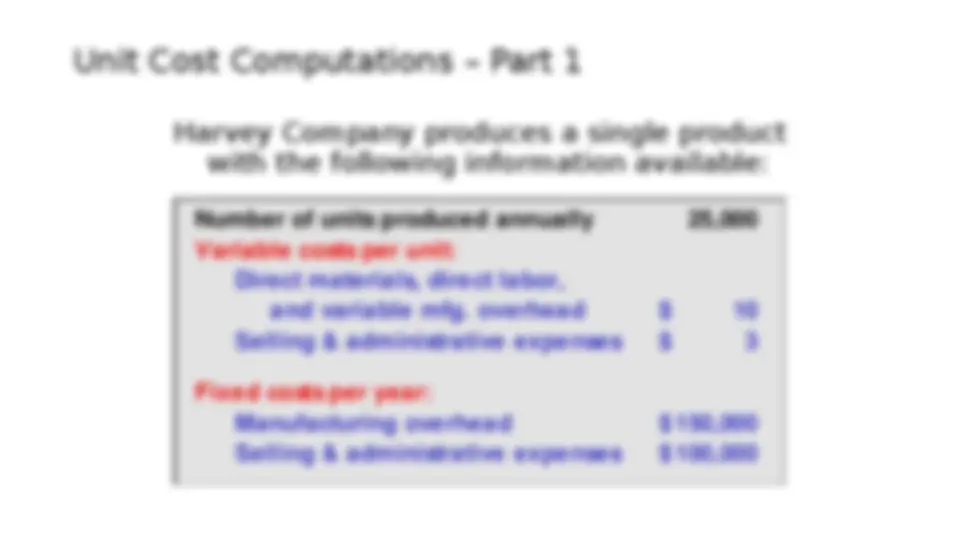

Harvey Company produces a single product with the following information available:

Unit Cost Computations – Part 1

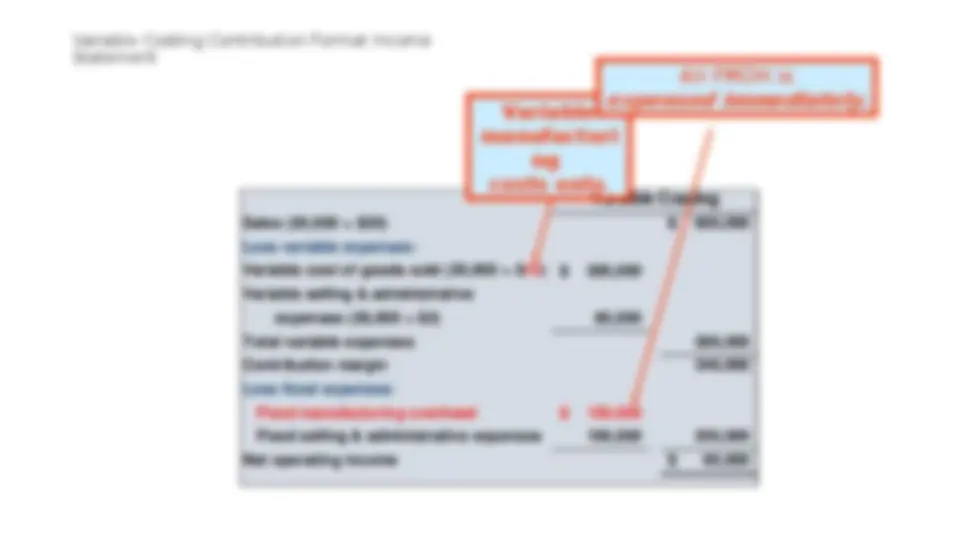

Let’s assume the following additional information for Harvey Company. ▫20,000 units were sold during the year at a price of $30 each. ▫There is no beginning inventory. Now, let’s compute net operating income using both absorption and variable costing. Variable and Absorption Costing Income Statements

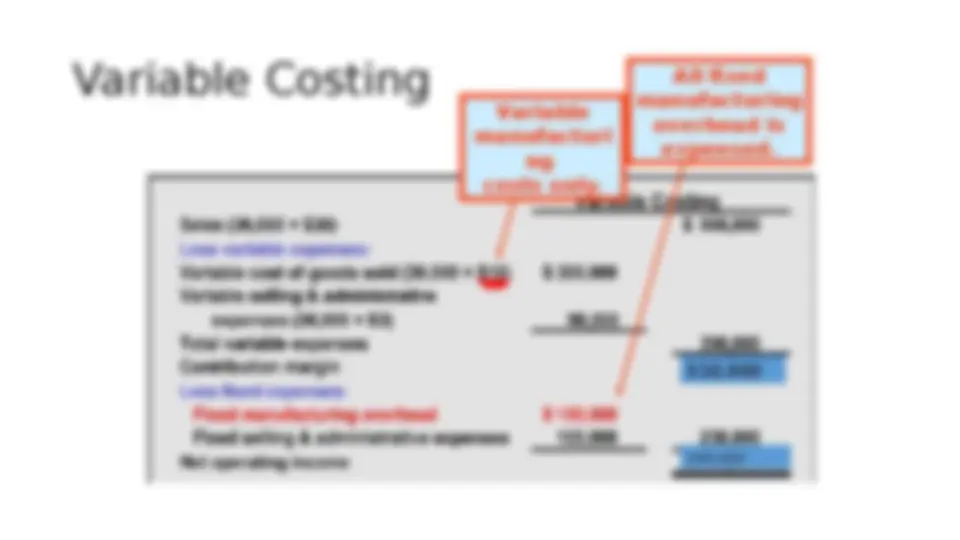

Variable Costing Sales (20,000 × $30) $ 600, Less variable expenses: Variable cost of goods sold (20,000 × $ 10 ) (^) $ 200, Variable selling & administrative expenses (20,000 × $3) 60, Total variable expenses 260, Contribution margin 340, Less fixed expenses: Fixed manufacturing overhead $ 150, Fixed selling & administrative expenses 100,000 250, Net operating income $ 90, Variable manufacturi ng costs only. All FMOH is expensed immediately. Variable Costing Contribution Format Income Statement

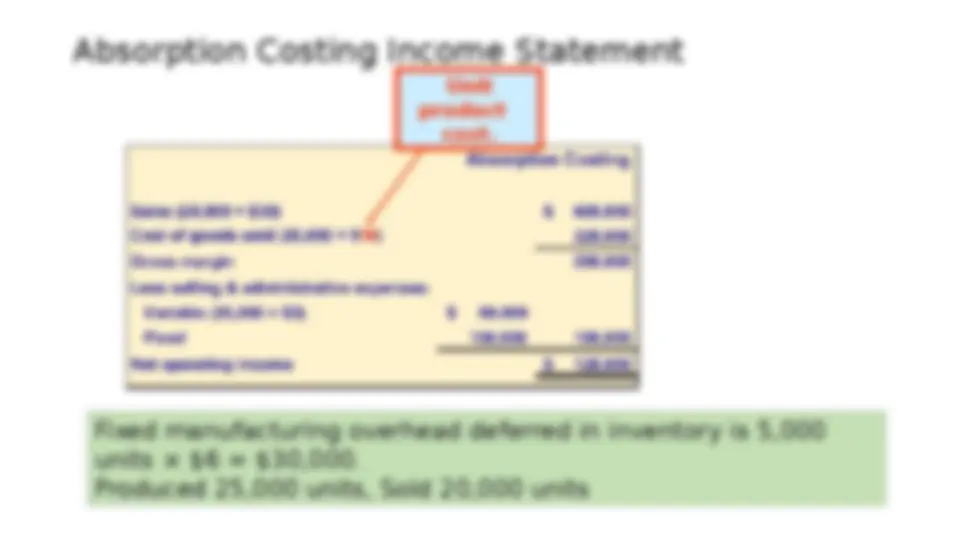

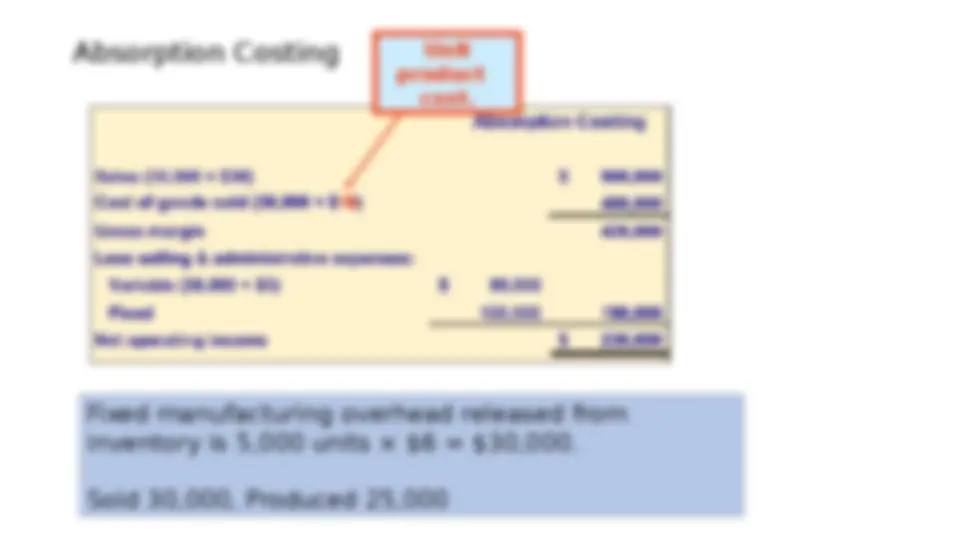

Variable costing net operating income $ 90, Add: Fixed mfg. overhead costs deferred in inventory (5,000 units × $6 per unit) 30, Absorption costing net operating income $ 120,

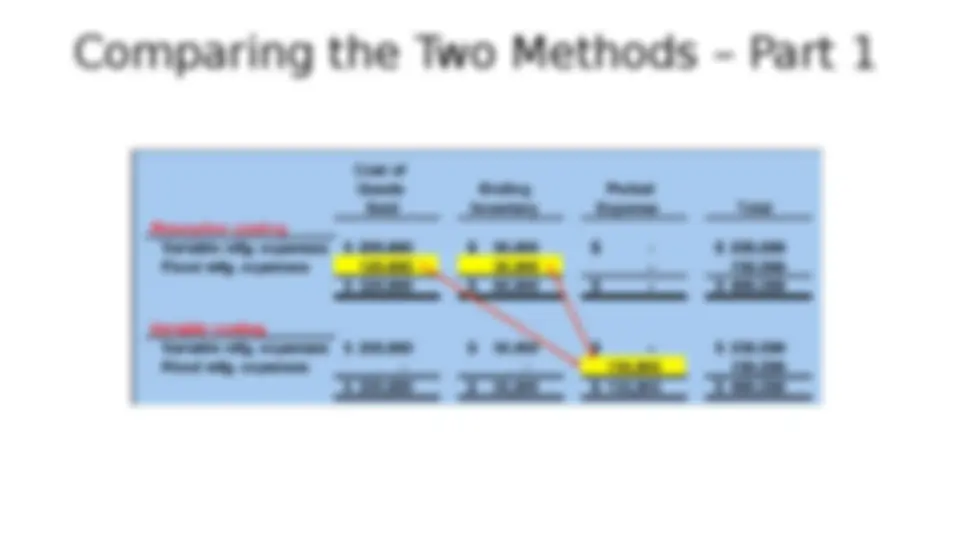

We can reconcile the difference between absorption and variable income as follows: Comparing the Two Methods – Part 2

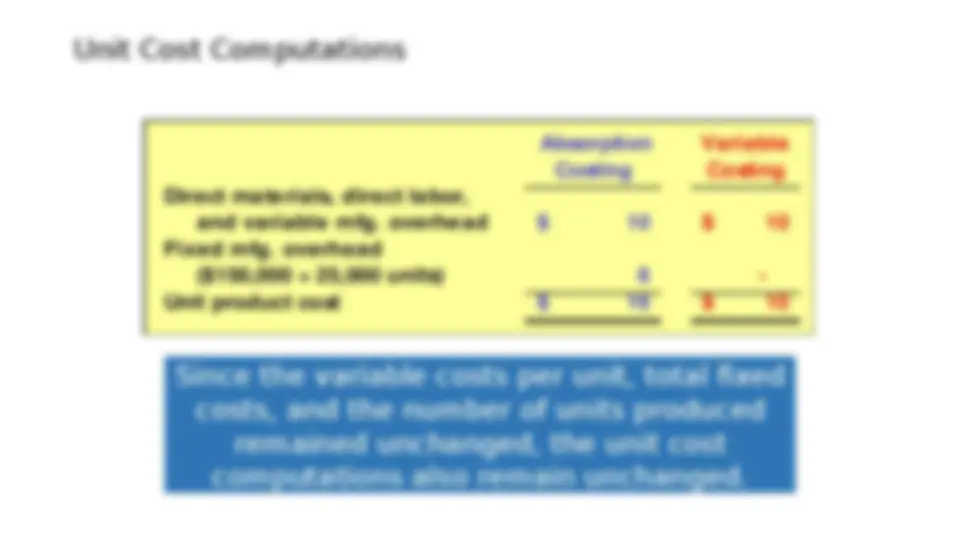

Unit Cost Computations Since the variable costs per unit, total fixed costs, and the number of units produced remained unchanged, the unit cost computations also remain unchanged. Absorption Costing Variable Costing Direct materials, direct labor, and variable mfg. overhead $ 10 $ 10 Fixed mfg. overhead ($150,000 ÷ 25,000 units) 6 - Unit product cost $ 16 $ 10

Variable manufacturi ng costs only. All fixed manufacturing overhead is expensed. 510, 260,

Reconciling the Difference – Part 1

Costing Method 1st Period 2nd Period Total Absorption $ 120,000 $ 230,000 $350, Variable 90,000 260,000 350, Reconciling the Difference – Part 2

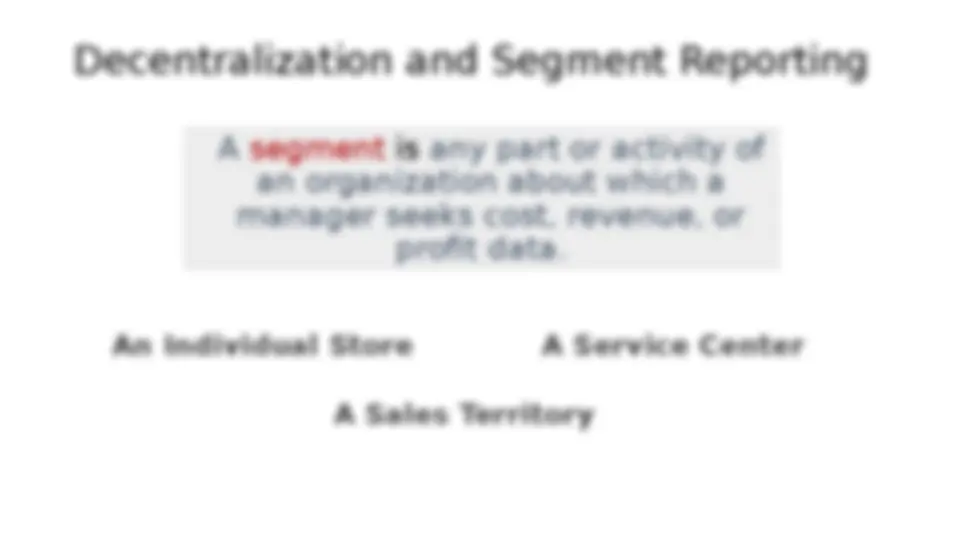

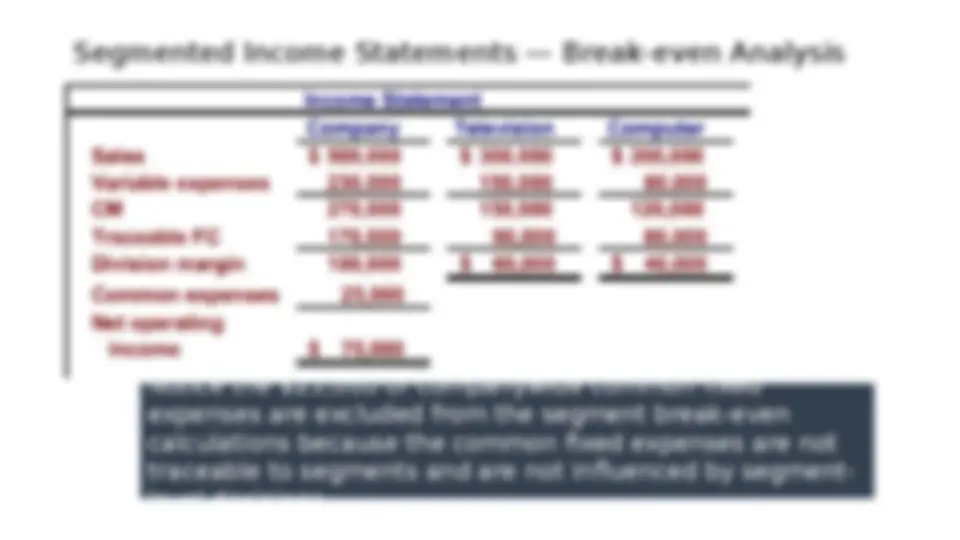

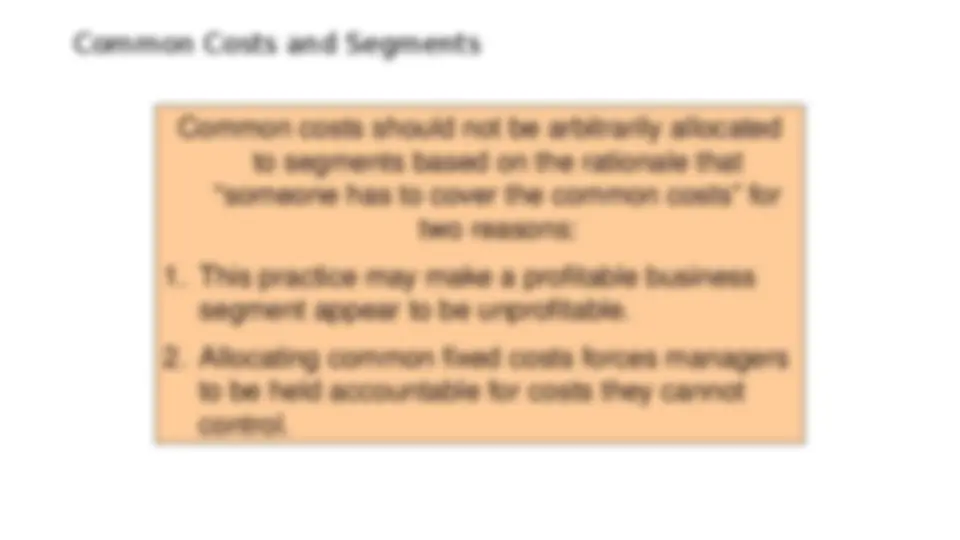

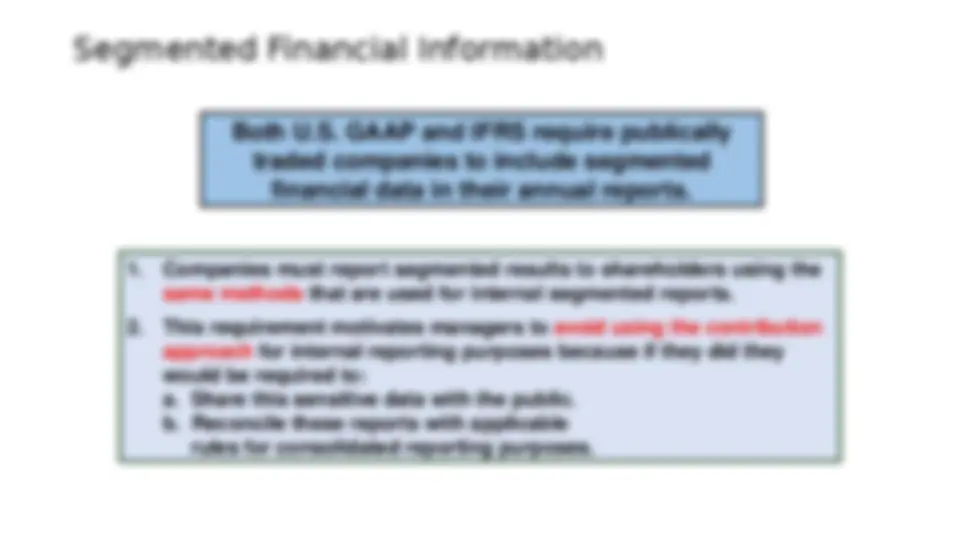

Decentralization and Segment Reporting A segment is any part or activity of an organization about which a manager seeks cost, revenue, or profit data. An Individual Store A Sales Territory A Service Center