Chapter 6:

Chapter 6:

THE MASTER BUDGET

H 13

1

H

orn

g

ren

13

e

E

T

R

BUDG

E

MASTE

R

W

OF THE

V

ERVIE

W

O

V

2

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

The concept of master budgeting, its benefits, and the steps involved in its preparation. It also introduces the concept of responsibility accounting and the different types of responsibility centers in an organization. exercises and quiz questions.

Typology: Assignments

1 / 11

This page cannot be seen from the preview

Don't miss anything!

H 13

1

Horngren 13e

3

Learning Objective 1: Describe the master budget... The master budget is the initial budget prepared before the start of a period andg p p p explain its benefits... benefits include planning, coordination, and control

Well-managed companies usually follow an annual budget cycle including the following steps:

Learning Objective 3: Prepare the operating budget... the budgeted income statement and its supporting schedules... such as costpp g of goods sold and nonmanufacturing costs [EXERCISE]

7

Learning Objective 3: Prepare the operating budget... the budgeted income statement and its supporting schedules... such as costpp g of goods sold and nonmanufacturing costs [SOLUTION]

Learning Objective 4: Use computer-based financial planning models in sensitivity analysis... for example, understand they y p , effects of changes in selling prices and direct material pries on budgeted income [EXERCISE][EXERCISE]

9

Learning Objective 4: Use computer-based financial planning models in sensitivity analysis... for example, understand they y p , effects of changes in selling prices and direct material pries on budgeted income [SOLUTION][SOLUTION]

Learning Objective 6: Describe responsibility centers... a part of an organization that a manager is accountable for andg g responsibility accounting... measurement of plans and actual results that a manager is accountable for A responsibility center is a part segment or subunit of an organization whoseA responsibility center is a part, segment, or subunit of an organization whose manager is responsible for a specified set of activities. Responsibility accounting measures the plans, budgets, actions, and results of each responsibility center. Four types of responsibility centers are: 1.1. Cost center, in which the manager is responsible for costs only. The accountingCost center, in which the manager is responsible for costs only. The accounting department would be accounted for as a cost center.

13

manager is responsible for. Any costs over which the manager lacks control should not be a part of his evaluation.

Learning Objective 7: Explain how controllability relates to responsibility accounting... managers cannot control all of the costsg g that they are accountable for; responsibility accounting focuses on obtaining information, not fixing blame Controllability is the degree of influence that a specific manager has over costs revenues or relatedControllability is the degree of influence that a specific manager has over costs, revenues, or related items for which he or she is responsible.

A controllable cost is any cost that is primarily subject to the influence of a given responsibility center manager for a given periodmanager for a given period.

This controllability can be difficult to pinpoint for two reasons:

Key Point: Someone cannot be held responsible for that which they cannot control. Control must be equal to the responsibility givenequal to the responsibility given.

Learning Objective 8: Recognize the human aspects of budgeting... to engage subordinate managers in the budgeting processg g g p A budget is usually more effective if the lower-level managers have input into the budget process. Through this process of participatory budgeting , the manager obtains “ownership” in the budget and is more likely to achieve budgetary success.

Managers frequently play games with budgets and build in budgetary slack. This is the practice of underestimating revenues, overestimating costs, or overestimating time in order to make the budget targets more easily achievable.

In budgeting in multinational companies three adjustments must be made:

15

Appendix: The Cash Budget [EXERCISE]

Required:Required:

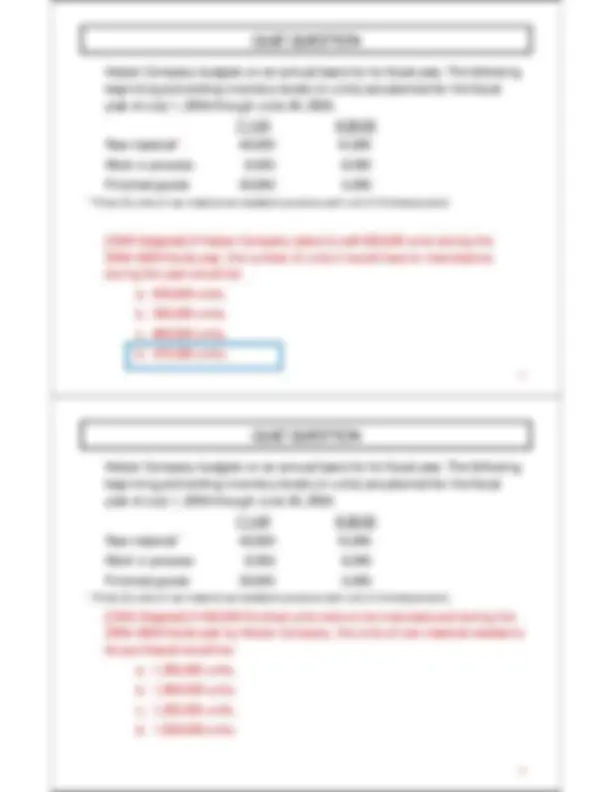

Hester Company budgets on an annual basis for its fiscal year. The following beginning and ending inventory levels (in units) are planned for the fiscal year of July 1 2004 through June 30 2005year of July 1, 2004 through June 30, 2005. 7-1-04 6-30- Raw material 1 40,000, 10,000, Work in process 8,000 8, Finished goods 30,000 5, (^11) ThThree (3) units of raw material are needed to produce each unit of finished product. (3) i f i l d d d h i f fi i h d d

[CMA Adapted] If Hester Company plans to sell 500,000 units during the[CMA Adapted] If Hester Company plans to sell 500,000 units during the 2004–2005 fiscal year, the number of units it would have to manufacture during the year would be: aa. 505,000 units. 505 000 units b. 500,000 units. c. 480,000 units.c 80,000 u ts d. 475,000 units. 19

Hester Company budgets on an annual basis for its fiscal year. The following beginning and ending inventory levels (in units) are planned for the fiscal year of July 1 2004 through June 30 2005year of July 1, 2004 through June 30, 2005. 7-1-04 6-30- Raw material 1 40,000, 10,000, Work in process 8,000 8, Finished goods 30,000 5, (^11) ThThree (3) units of raw material are needed to produce each unit of finished product. (3) i f i l d d d h i f fi i h d d

[CMA Adapted] If 450,000 finished units were to be manufactured during the 2004–2005 fiscal year by Hester Company, the units of raw material needed to be purchased would be: a. 1,350,000 units. bb. 1,360,000 units. 1 360 000 units c. 1,320,000 units. d. 1,330,000 units.d ,330,000 u ts

Hester Company budgets on an annual basis for its fiscal year. The following beginning and ending inventory levels (in units) are planned for the fiscal year of July 1 2004 through June 30 2005year of July 1, 2004 through June 30, 2005. 7-1-04 6-30- Raw material 1 40,000, 10,000, Work in process 8,000 8, Finished goods 30,000 5, (^11) ThThree (3) units of raw material are needed to produce each unit of finished product. (3) i f i l d d d h i f fi i h d d

[CMA Adapted] If 450,000 finished units were to be manufactured during the 2004–2005 fiscal year by Hester Company, the units of raw material needed to be purchased would be: a. 1,350,000 units. bb. 1,360,000 units. 1 360 000 units c. 1,320,000 units. d. 1,330,000 units.d ,330,000 u ts