CLASSIFICATION OF COST

Dr. RAVI JAIN (Visiting)

Faculty of Management,

Subject: Business Environment (MBA CSM 2nd Sem)

SoS in CSM, Jiwaji University, Gwalior

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

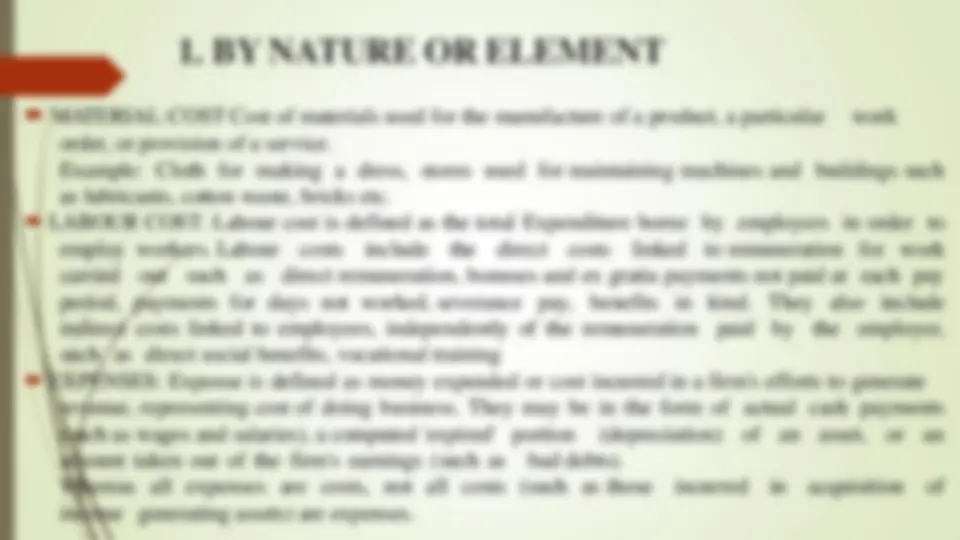

Classification of Costs on The Basis of Their ... EXPENSES: Expense is defined as money expended or cost incurred in a firm's efforts to generate.

Typology: Lecture notes

1 / 12

This page cannot be seen from the preview

Don't miss anything!

Classification of Costs on The Basis of Their

Common Characteristics are:

By Nature or Elements

By Functions

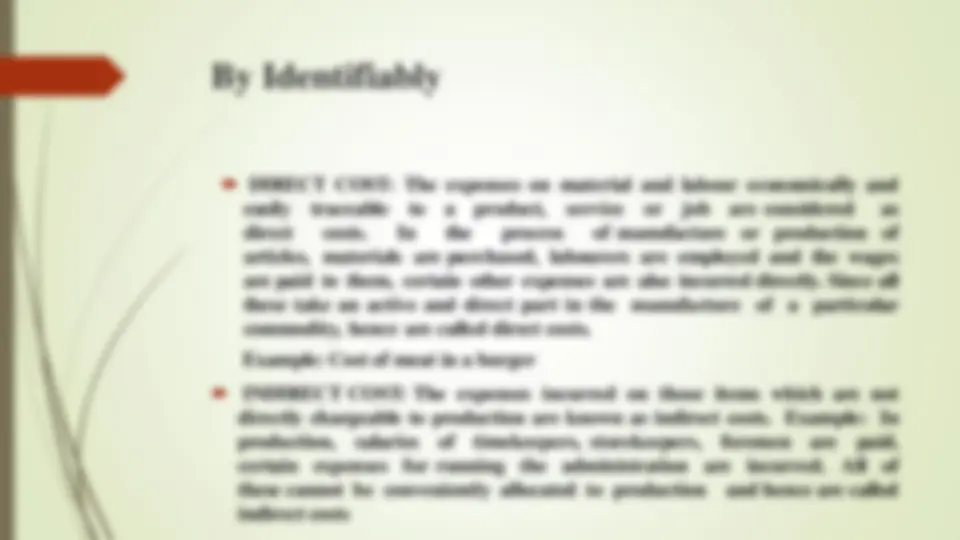

By Identifiably

By Variability

By Controllability

By Normality

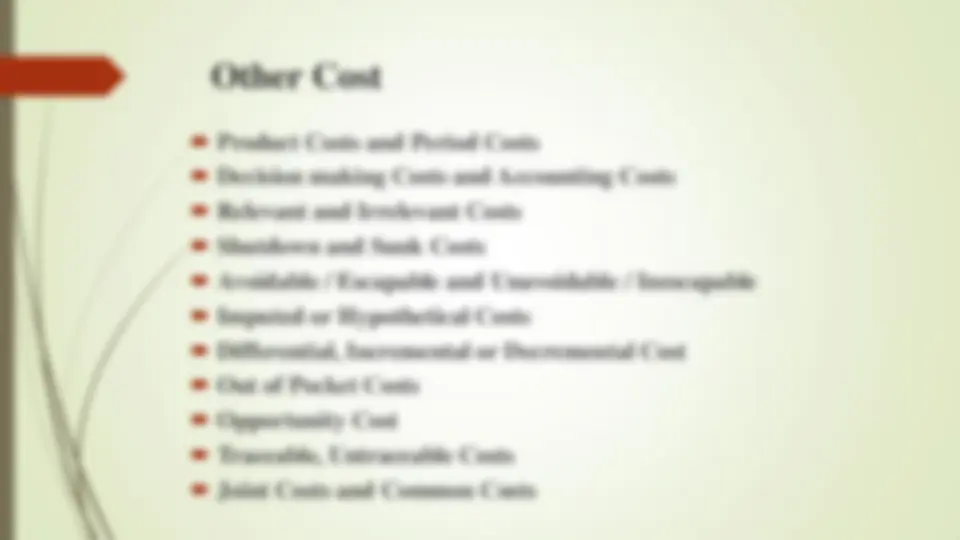

Other Costs

By Functions

By Identifiably

DIRECT COST: The expenses on material and labour economically and

easily traceable to a product, service or job are considered as

direct costs. In the process of manufacture or production of

articles, materials are purchased, labourers are employed and the wages

are paid to them, certain other expenses are also incurred directly. Since all

these take an active and direct part in the manufacture of a particular

commodity, hence are called direct costs.

Example: Cost of meat in a burger

INDIRECT COST: The expenses incurred on those items which are not

directly chargeable to production are known as indirect costs. Example: In

production, salaries of timekeepers, storekeepers, foremen are paid,

certain expenses for running the administration are incurred. All of

these cannot be conveniently allocated to production and hence are called

indirect costs

By Controllability

CONTROLLABLE COSTS: These are the costs which can be

influenced by the action of a specified member of an

undertaking. A business organization is usually divided into a

number of responsibility centres and each centre is headed by an

executive. The executive can thus control the costs incurred in that

particular responsibility centre.

UNCONTROLLABLE COSTS: Costs which cannot be

influenced by the action of a specified member of an undertaking.

Example: Expenditure incurred by the tool room is controllable

by the foreman in charge of that section but the share of the tool

room expenditure which is apportioned to a machine shop is not to

be controlled by the machine shop foreman.

By Normality

NORMAL COSTS: It is the cost which is normally incurred at a

given level of output under the conditions in which that level of

output is normally attained.

ABNORMAL COST: It is the cost which is not normally incurred

at a given level of output in the conditions in which that level of

output is normally attained. This is charged to Costing P&L A/c

IMPUTED OR HYPOTHETICAL COSTS: These are costs which do not involve any cash outlay. They are not included in cost accounts but are important for taking into consideration while making management decisions.

Examples: Interest on internally generated funds, salaries of the proprietor or partner of a partnership firm, rented value of company‟s own property etc. When two projects require unequal outlays of cash, the management must take into consideration interest on capital for judging the relative profitability of the projects though the company may use internally generated funds for the purpose.

DIFFERENTIAL COSTS: The difference in total costs between two alternatives is termed as „differential costs‟. In case the choice of an alternative results in increase in total costs, such increase in costs is known as „incremental costs.‟ In case the choice results in decrease in total costs, such decrease in total costs is termed as „decremental costs‟. While assessing the profitability of a proposed change the incremental costs are matched with incremental revenue and vice versa. The proposed change is taken only when it is profitable.

OUT-OF-POCKET COST: This means the present or future cash expenditure regarding a certain decision which varies depending upon the nature of decision made.

Example: A company has its own trucks for transporting raw materials and finished products from one place to another. It seeks to replace these trucks by employment of public carrier of goods. In making this decision of course , the depreciation of the trucks is not to be considered, but the management must take into account the present expenditure on fuel, salary to drivers and maintenance. Such costs are termed as out- of-pocket expenses.

OPPORTUNITY COST: This cost refers to the advantage, in measurable terms, which has been foregone on account of not using the facilities in the manner originally planned.

Example: If an owned building is proposed to be utilized for housing a new project plant, the likely revenue which the building could fetch if rented out is the opportunity cost which should be taken into account while evaluating the profitability of the

TRACEABLE OR UNTRACEABLE COSTS: Costs which can be easily identified with a department, process or product are termed as traceable costs. Example: the cost of direct material, direct labour etc. Costs which cannot be so identified are termed as untraceable or common costs.

In other words common costs are costs incurred collectively for a number of cost centres and are to be suitably apportioned for determining the cost of individual cost centres. Example: overheads incurred for a factory as a whole etc.

JOINT COSTS: These are a sort of common costs. When two or more products are produced out of one and the same material or process, the costs of such material or process are called joint costs.

Example: When cotton seeds and cotton fibre are produced from the same raw materials, the cost incurred till split off or separation point will be joint costs.

COMMON COSTS: Common costs are those which are incurred for more than one product, job, territory or any other specific costing unit. They are not capable of being identified with individual product, and are therefore apportioned on a suitable basis.

Example: Rent, lighting and supervision costs are common costs to all departments located in the factory.