GOVERNMENT

ACCOUNTING

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

The process, objectives, and responsibilities of government accounting. It covers the analysis, recording, classification, summarization, and communication of transactions involving government funds and property. The document emphasizes the importance of sources and utilization of government funds, accountability, and liability over government funds and property. It also discusses the role of various entities, such as COA, DBM, BTr, and government agencies, in government accounting.

Typology: Lecture notes

1 / 31

This page cannot be seen from the preview

Don't miss anything!

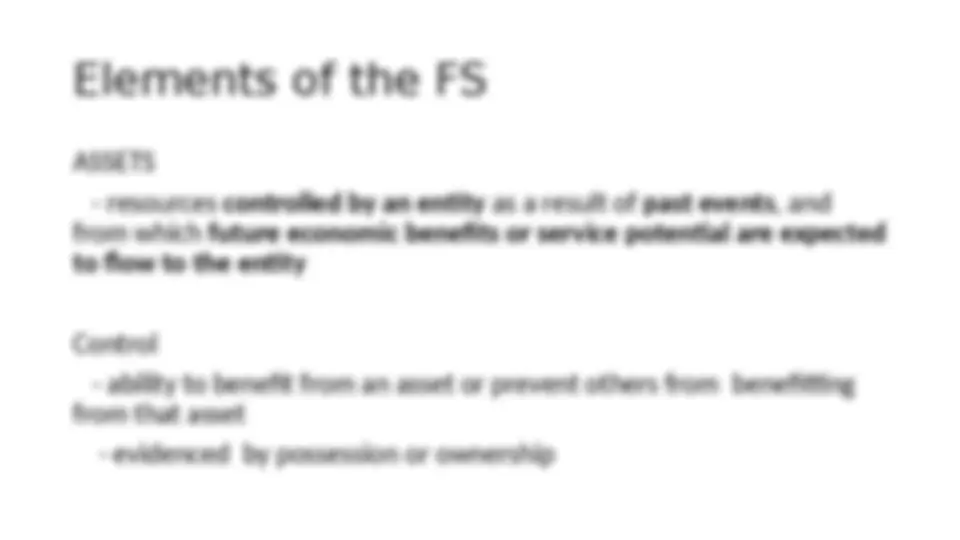

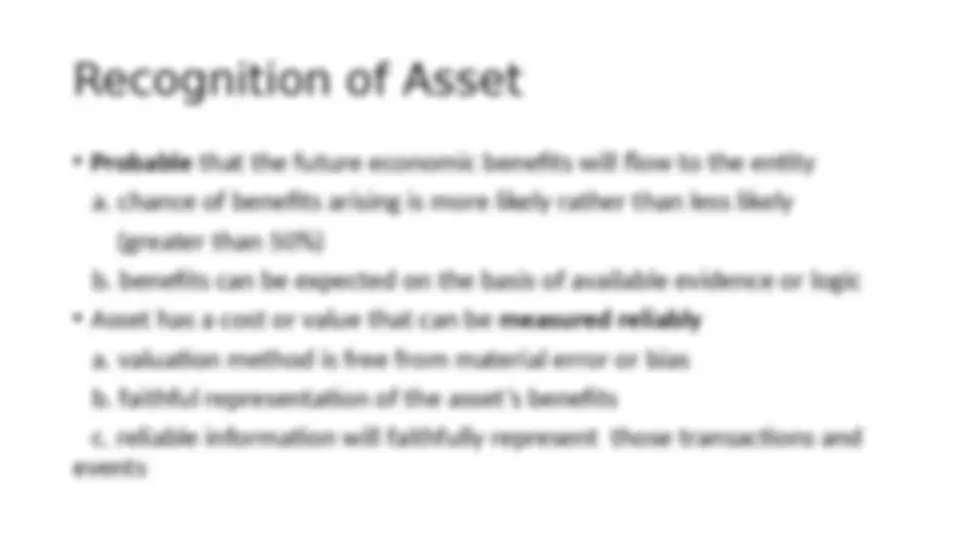

The Process of analyzing, recording, classifying, summarizing and communicating all transactions involving the receipt and disposition of government fund and property and interpreting the results thereof (Section 109 of PD 1445)