The Conceptual Framework and

Objectives of Financial Reporting

docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

In this course topics like Accounting Process, Balance Sheet and Owners’ Interests, Cash Flows, Conceptual Framework, Control of Cash, Expense Recognition, Income Statement, Inventory, Recognition, Recognition and Measurement are covered. This lecture includes: Conceptual Framework, Financial Reporting, Allocation of Resources, Evaluation of Past Performance, Expectations of Future Performance, Enterprise Principle, Investors, Role of Accounting, Sources of Gaap, Accounting Procedure

Typology: Slides

1 / 38

This page cannot be seen from the preview

Don't miss anything!

The Conceptual Framework and Objectives of Financial Reporting

Accounting

Information

Investors

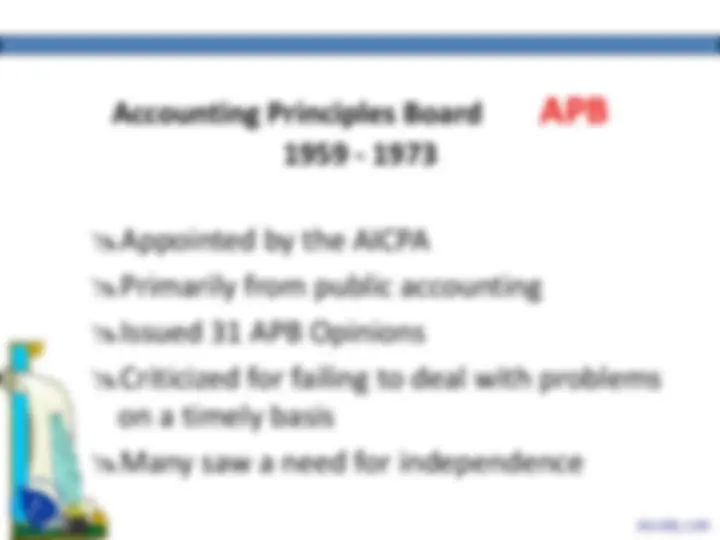

Committee on Accounting Procedure CAP

1939 - 1959

First private body concerned with writing accounting rules Issued 51 Accounting Research Bulletins Members were practicing CPAs An “ad hoc” approach

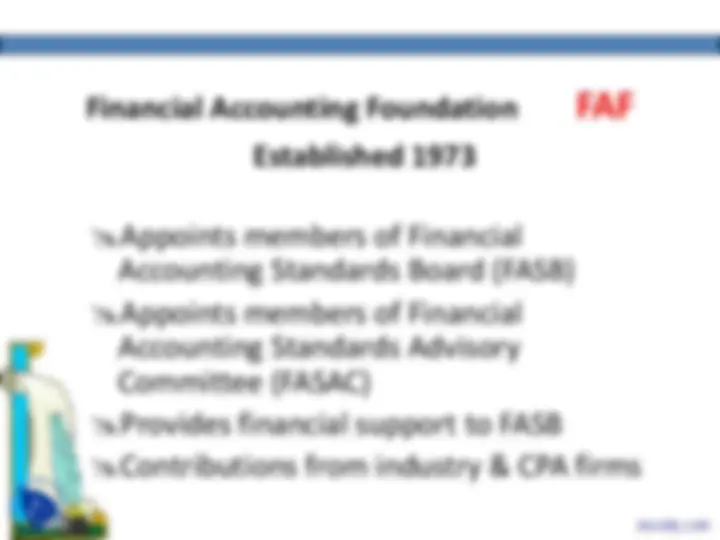

Financial Accounting Foundation FAF

Established 1973

Appoints members of Financial Accounting Standards Board (FASB) Appoints members of Financial Accounting Standards Advisory Committee (FASAC) Provides financial support to FASB Contributions from industry & CPA firms

Financial Accounting Standards Board FASB Established 1973

7 members

Members are full time, well paid

Responsible only to FAF

Passage of standards requires 5 out of 7 votes

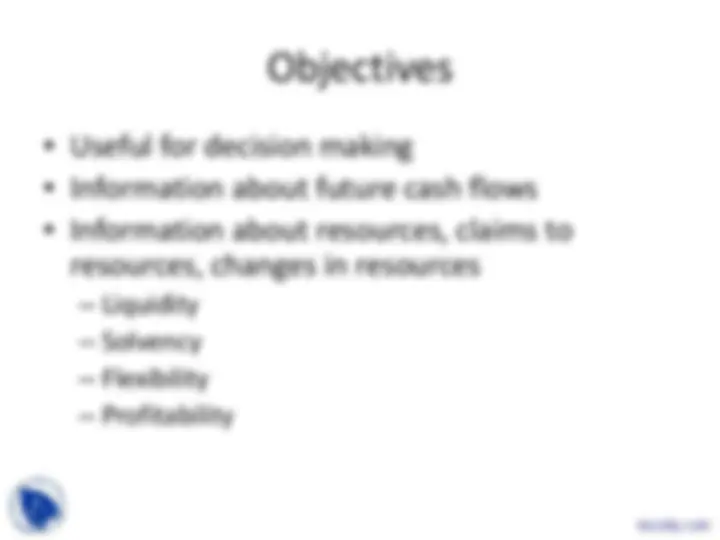

Statements of Financial Accounting Concepts (SFACs)

Purpose:

Establish the objectives and concepts to be used by the FASB in developing standards for financial reporting

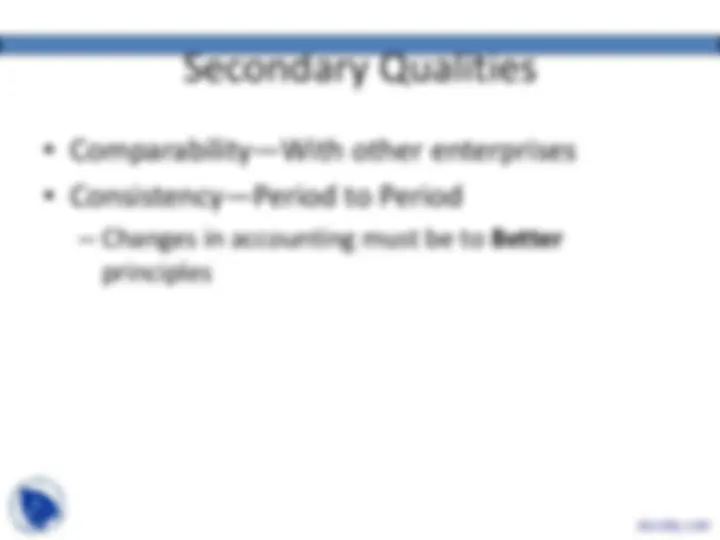

Conceptual Framework SFACs

1 Objectives of Financial Reporting

2 Qualitative Characteristics

4 Objectives for Nonbusiness Organizations

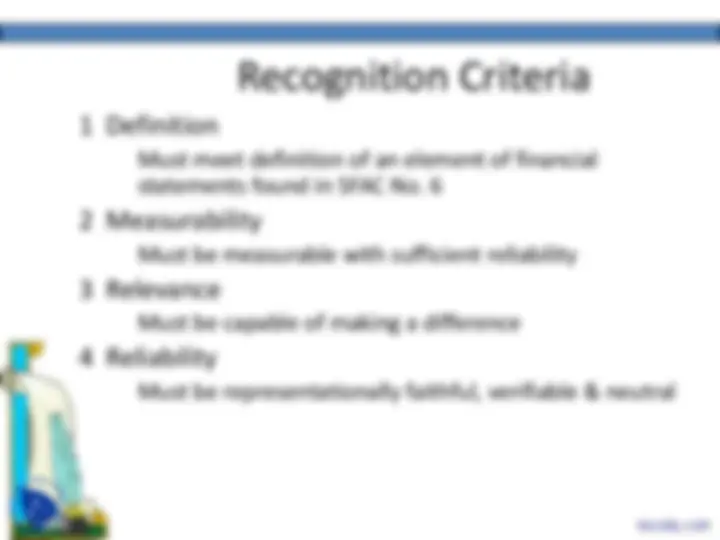

5 Recognition & Measurement

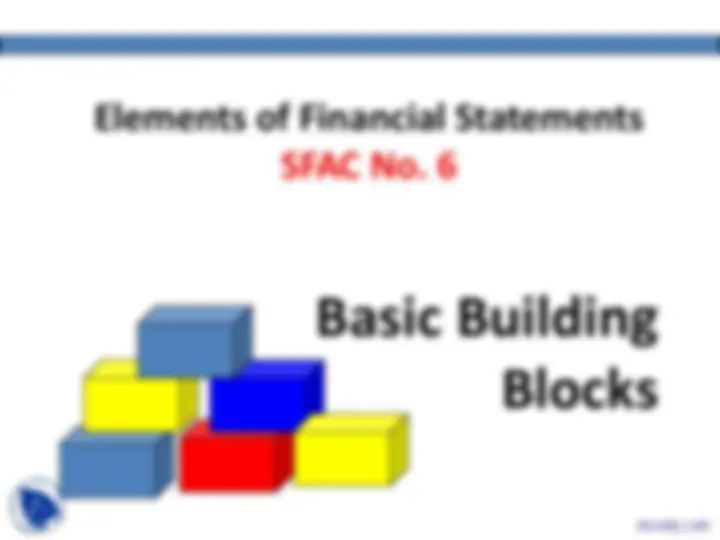

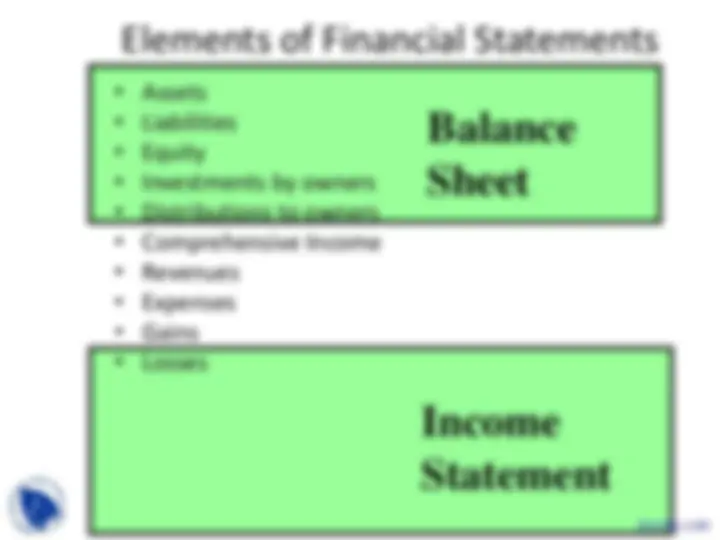

6 Elements of Financial Statements