CS723 - Probability

and

Stochastic Processes

CS723 - Probability

and

Stochastic Processes

docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

A part of the lecture notes for cs723 - probability and stochastic processes, specifically lecture no. 11. The lecture covers conditional probability, expected value, and transformations of random variables. Topics include conditional pmf/cdf, geometric interpretation of expected value, and transformation of random variables. Examples of expected value calculations for bernoulli and poisson distributions are provided, as well as the concept of fairness in gambling games like chuck-a-luck and prize bonds.

Typology: Slides

1 / 12

This page cannot be seen from the preview

Don't miss anything!

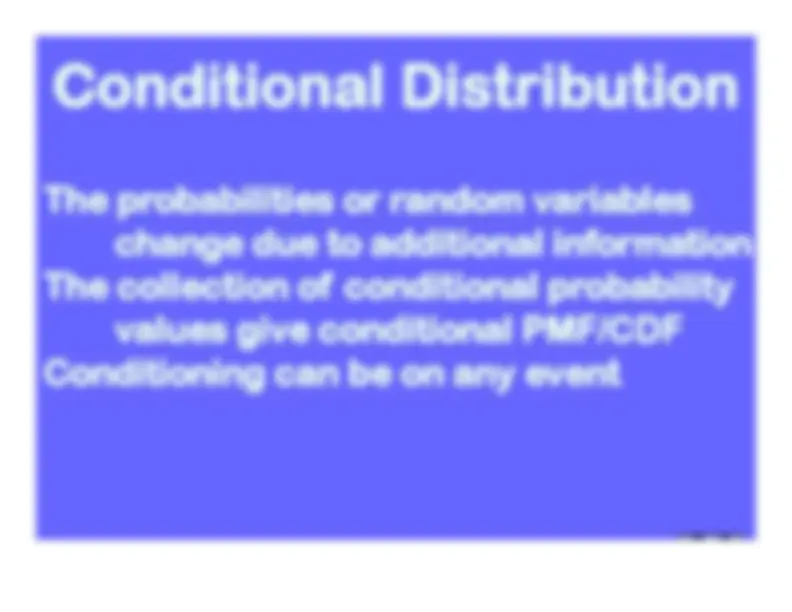

change due to additional information The collection of conditional probability

values give conditional PMF/CDF The probabilities or random variablesConditioning can be on any event

change due to additional information The collection of conditional probability

values give conditional PMF/CDF Conditioning can be on any event

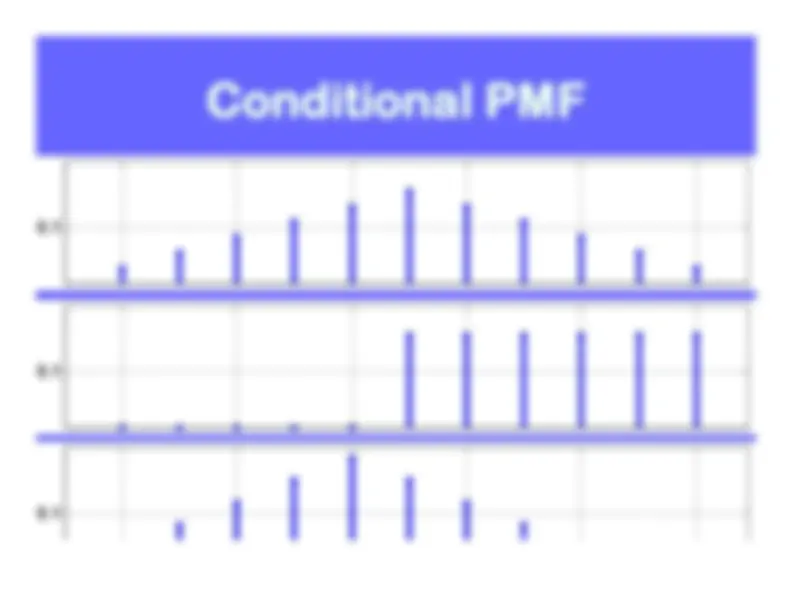

0.1 0.1 0.

Expected value of Bernoulli distribution

B(N,p) is Np Expected number of customers going

into a restaurant in 10 minutes was 24 Expected value of Poisson distributionis^

always

λ

The value of

λ^

chosen for Poisson

approximation was 24 Expected value of Bernoulli distribution

B(N,p) is Np Expected number of customers going

into a restaurant in 10 minutes was 24 Expected value of Poisson distributionis^

always

λ

The value of

λ^

chosen for Poisson

approximation was 24

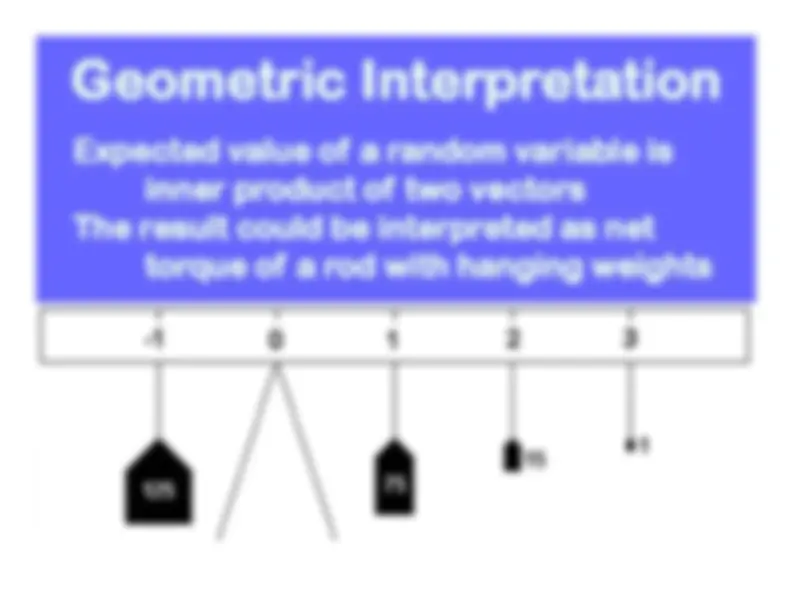

Geometric InterpretationGeometric InterpretationExpected value of a random variable is

inner product of two vectors The result could be interpreted as net

torque of a rod with hanging weights Expected value of a random variable is

inner product of two vectors The result could be interpreted as net

torque of a rod with hanging weights

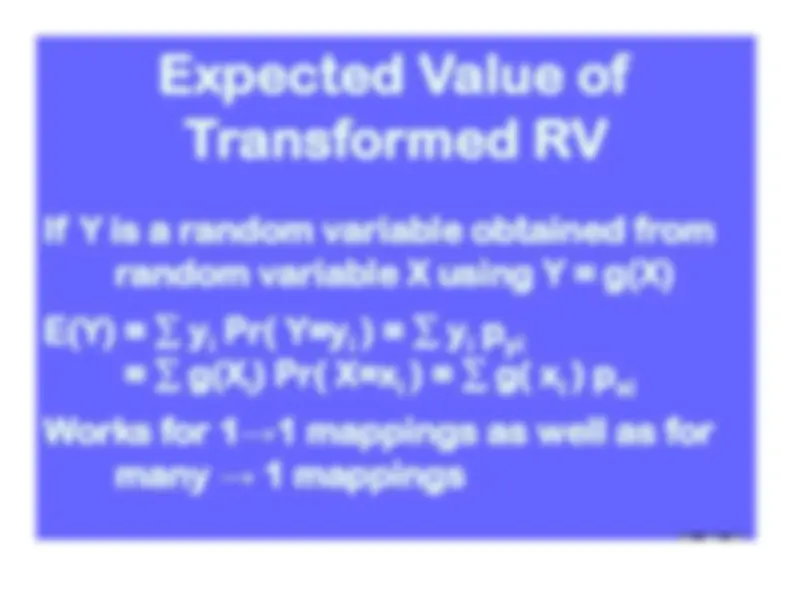

Expected Value ofExpected Value ofTransformed RVTransformed RV

If Y is a random variable obtained from

random variable X using Y = g(X) E(Y) =

y^ Pr( Y=yi^

) =i^

y^ pi^

yi

g(X

) Pr( X=xi^

) =i^

g( x

) pi^

xi

Works for 1

1 mappings as well as for

many

1 mappings

If Y is a random variable obtained from

random variable X using Y = g(X) E(Y) =

y^ Pr( Y=yi^

) =i^

y^ pi^

yi

g(X

) Pr( X=xi^

) =i^

g( x

) pi^

xi

Works for 1

1 mappings as well as for

many

1 mappings

Expectation of Y=g(X)Expectation of Y=g(X) Gambling game of chuck-a-luck run by a

benevolent gambling house You don’t loose your bet and get a

chance to win 4,3, or 2 dollars. Transformed RV is Y = X+1E(Y) = (752 + 153 + 1*4)/216 = 0.92For prize bonds with inflation effectY = X – 30 and E(Y) = E(X) – 30 = -5.56E(X+a) = E(X) + a

& E(bX) = bE(X)

Gambling game of chuck-a-luck run by a

benevolent gambling house You don’t loose your bet and get a

chance to win 4,3, or 2 dollars. Transformed RV is Y = X+1E(Y) = (752 + 153 + 1*4)/216 = 0.92For prize bonds with inflation effectY = X – 30 and E(Y) = E(X) – 30 = -5.56E(X+a) = E(X) + a

& E(bX) = bE(X)