Download Confidence Intervals for λ in Two-Parameter Exponential Distributions and more Exercises Mathematical Statistics in PDF only on Docsity!

Question #1:

(a)

r =

∑^10

i=

ci = 7, and ̂λ =

∑n ∑in=1^ ci i=1 ti^

An approximate 95% confidence interval for λ is given by

ˆλ ± 1. 96 λˆ √ r

→ 0. 047 < λ < 0. 315

Note that the above confidence interval is an approximate confidence interval while for exponential we can find an exact confidence interval. In addition, the confidence interval is based on large sample while we have only 10 observations. Therefore, it is better to use the following formula to find a 95% confidence interval for λ.

ˆλ χ^22 r, 0. 975 2 r < λ <

ˆλ χ^22 r, 0. 025 2 r

ˆλ χ^214 , 0. 975 14 < λ <

ˆλ χ^214 , 0. 025 14

< λ <

−→ 0. 073 < λ < 0. 337

(b) For exponential distribution S(4) = e−^4 λ. A 95% confidence interval for λ, from part (a), is (0. 073 , 0 .337). So a 95% confidence interval for S(4) = e−^4 λ^ is ( e−4(0.337), e−4(0.073)

Another way to find a 95% confidence interval for g(λ) = S(4) = e−^4 λ^ is to use

g(ˆλ) ± 1 .96 S.E.

g(ˆλ)

where

Var

g(ˆλ)

d dλ g(λ)

Var(ˆλ) =

− 4 e−^4 λ

) 2 λ^2 r

→ S.E.

g(λˆ)

= 4e−^4 ˆλ (^) √λˆ r

So a 95% confidence interval for g(λ) = S(4) = e−^4 λ^ is

g(ˆλ) ± 1 .96 S.E.

g(λˆ)

= e−4(0.1809)^ ± 1 .96 4e−4(0.1809)^

Another 95% confidence interval for S(4) is

[̂

S(4)

]exp[± 1 .96 S.E(ˆν)] where

ν = ln [− ln S(4)] = ln 4 + ln λ = g(λ)

So

Var(ˆν) = Var

g(ˆλ)

d dλ

g(λ)

Var(λˆ) =

λ

λ^2 r

r

⇒ S.E(ˆν) =

Therefore a 95% confidence interval for S(4) is

[̂ S(4)

]exp[± 1 .96 S.E(ˆν)]

[

e−4(0.1809)

]exp[± 1. 96 /√ (^7) ] → (0. 219 , 0 .708)

It should be mentioned that the last two confidence intervals are approximate confidence intervals and they are based on large samples while we have only 10 observations in this problem.So we should use the first confidence interval.

Question #2:

(a) For Weibull distribution, ˆγ, Weibull shape, and its standard deviation are given by SAS. To find λˆ and its standard deviation, we have λ = e−β^0 = g(β 0 ). So

Var

ˆλ

d dβ 0

g(β 0 )

Var( βˆ 0 ) =

−e−β^0

Var( βˆ 0 ) → S.E.(λˆ) = e−^ βˆ 0 S.E.( βˆ 0 )

Therefore, for group 1, we have ˆγ 1 = 1.5948, S.E.(ˆγ 1 ) = 0.3230, and

λˆ 1 = e−^ βˆ^0 = e−^3.^1939 = 0. 0410 and S.E.(λˆ 1 ) = e−^3.^1939 (0.1805) = 0. 0074

Similarly, for group 2, we have ˆγ 2 = 0.5402, S.E.(ˆγ 2 ) = 0.1432, and

λˆ 2 = e−^ βˆ^0 = e−^5.^4109 = 0. 0045 and S.E.(λˆ 2 ) = e−^5.^4109 (1.0236) = 0. 0046

(b) The log-likelihoods for Weibull distribution for two groups 1 and 2 are - 32.4241 and -48.0143, respectively. If γ = 1, the Weibull distribution reduces to an exponential distribution. So The log-likelihoods for Exponential distribution for two groups 1 and 2 are -34.5645 and -51.5779, respectively. So for testing H 0 : γ 1 = γ 2 = 1 versus H 1 : γ 1 6 = 1 or γ 2 6 = 1, the test statistic is

T S = − 2 {[(− 34 .5645) + (− 51 .5779)] − [(− 32 .4241) + (− 48 .0143)]} = 11. 368

The test statistic, under null hypothesis, has a chi-square distribution with 4 − 2 = 2 degrees of freedom. Therefore, P -value = P (T S > 11 .368) = 0.0034. Since p-value is less than α = 0.05, we reject H 0.

Question #3:

(a) We find moment generating function of Y = 2nμ/μˆ = 2nλT

E(euY^ ) = E

eu(2nλT^ )

= E

eu(2λ^

∑n i=1 Ti)

= E

( (^) n ∏

i=

e^2 λuTi

∏^ n

i=

E

e^2 λuTi^

(Since Ti are independent.)

The moment generating function of Ti is E(euTi^ ) = (1 − u/λ)−^1. Hence

E(e^2 λuTi^ ) = (1 − 2 λu/λ)−^1 = (1 − 2 u)−^1

Therefore,

E(euY^ ) =

∏^ n

i=

(1 − 2 u)−^1 = (1 − 2 u)−n

Note that (1 − 2 u)−n^ is the moment generating function of a Chi-Square distri- bution with degrees of freedom 2n. Since moment generating function uniquely determine the distribution, Y has a Chi-Square distribution with degrees of freedom 2n and this completes the proof.

(b) Suppose T 1 , T 2 , · · · , Tn is a random sample from an exponential distribution with parameter λ. (We will solve the problem when the distribution is two- parameter exponential after that.) The joint distribution of T(1), T(2), · · · , T(n) is

g

T(1), T(2), · · · , T(n)

= n!

∏^ n

i=

f (T(i)) = n!

∏^ n

i=

λe−λT(i)

= n! λn^ exp

[

λ

∑^ n

i=

T(i)

]

We will find the joint distribution of

W 1 = nT(1) and Wi = (n − i + 1)(T(i) − T(i−1)) for i = 2, · · · , n

Note that

∑n i=1 T(i)^ =^

∑n i=1 Wi^ and the Jacobian of the the transformation is J = 1/n!. Therefore, the joint distribution of W 1 , W 2 , · · · Wn is

f (W 1 , W 2 , · · · , Wn) = n!g (W 1 , W 2 , · · · , Wn) |J|

= λn^ exp

[

λ

∑^ n

i=

W(i)

]

∏^ n

i=

λ e−λWi^

This means that W 1 , W 2 , · · · Wn are independent and Wi has an exponential distribution with parameter λ. On the other hand,

Y =

∑^ n

i=

Ti − T(1)

∑^ n

i=

Ti − nT(1) =

∑^ n

i=

T(i) − nT(1) =

∑^ n

i=

Wi − W 1 =

∑^ n

i=

Wi

The moment generating function of Y is

E(euY^ ) = E

exp

[

u

∑^ n

i=

Wi

])

= E

( (^) n ∏

1=

euWi

∏^ n

1=

EeuWi^ =

∏^ n

1=

(1 − u/λ)−^1

= (1 − u/λ)−(n−1)

This is the moment generating function of a gamma distribution with param- eters n − 1 and λ. Since moment generating function uniquely determine the distribution, Y has a gamma distribution with parameters n − 1 and λ. Now, if T 1 , T 2 , · · · , Tn is a random sample from two-parameter distribution with param- eter λ and G, then T 1 − G, T 2 − G, · · · , Tn − G is a random sample from an expo- nential distribution with parameter λ. Therefore, T(1) −G, T(2) −G, · · · , T(n) −G is the order statistics in a random sample of size nfrom an exponential distri- bution with parameter λ. Hence, by the above results, W 1 = n

T(1) − G

and

Wi = (n − i + 1)

[

(T(i) − G) − (T(i−1) − G)

]

= (n − i + 1)(T(i) − T(i−1)),

i = 2, · · · , n, are independent and have a exponential distribution with param- eter λ. In addition

Y =

∑^ n

i=

Ti − T(1)

∑^ n

i=

Wi

has a gamma distribution with parameters n − 1 and λ.

Question #4:

(a) We proved, in part (b) of question #3, that

W 1 = n (T 1 − G) and Wi = (n − i + 1)(T(i) − T(i−1)) for i = 2, · · · , n

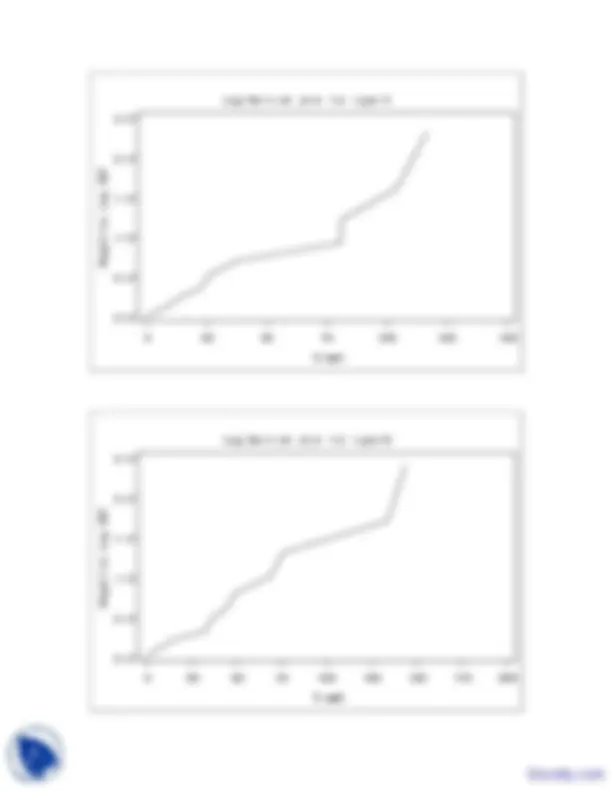

are independent and have a exponential distribution with parameter λ. I will use PROC LIfETEST to check whether W 2 , · · · , Wn is a random sample from an exponential distribution (You can also use Cox-Snell residuals plot to check whether W 2 , · · · , Wn is a random sample from an exponential distribution). The plots on − ln Ŝ(t) versus t for Types A and B are given in the last page. Both plots show no serious deviation from straight line and therefore we cannot reject that the data does not have two-parameter exponential distribution.

(b) As I showed in the class, since T 1 , T 2 , · · · , Tn are independent and have two parameter exponential distribution, the maximum likelihood estimate of λ is

λˆ = ∑nn i=2 Wi

n ∑n i=

T(i) − T(1)

In addition, by using part (b) of question #3, We know that

W 1 = n (T 1 − G) and Wi = (n − i + 1)(T(i) − T(i−1)) for i = 2, · · · , n

(b) The p.d.f. of a gamma distribution is

f (t) =

λ Γ(γ)

(λt)γ−^1 e−λt

So

ln f (t) = ln

λ Γ(γ)

- (γ − 1) ln(λt) − λt ⇒ d ln f (t) dt

γ − 1 t

− λ

Therefore, by using part (a), we have

lim t→∞ m(t) = lim t→∞

d dt

ln f (t)

= lim t→∞

λ − γ − 1 t

= (λ − 0)−^1 =

λ

(f ) The p.d.f. of a log-normal distribution is

f (t) =

tσ

2 π

exp

[

2 σ^2

(ln t − μ)^2

]

So

ln f (t) = − ln(t) + ln

σ

2 π

2 σ^2

(ln t − μ)^2

d ln f (t) dt

t

σ^2

ln t − μ t

t

σ^2

ln t t

μ t

as t → ∞, since, by using L’Hospital’s Rule,

lim t→∞

ln t t

= lim t→∞

1 /t 1

= lim t→∞

t

Therefore, by using part (a), we have

lim t→∞ m(t) = lim t→∞

d dt ln f (t)

−→ ∞, as t → ∞.

Question #6:

H(t) =

∫ (^) t

o

h(x)dx =

∫ (^) t

0

[

α +

β x + γ

]

dx = [αx + β ln(x + γ)]t 0

= αt + β ln(t + γ) − β ln(γ) = αt + β ln

t + γ γ

= αt + ln

t + γ γ

)β

S(t) = exp {−H(t)} = exp

[

αt + ln

t + γ γ

)β ]}

γ t + γ

)β e−αt

f (t) = h(t)S(t) =

[

α +

β t + γ

] (

γ t + γ

)β e−αt

You can also find f (x) by using, for example, f (x) = −S ′ (x).

Question #7:

f (t, λ) = f (t|λ)g(λ) =

λe−λt

λk−^1 e−λ/α αkΓ(k)

λk αkΓ(k)

e−[t+1/α]λ

So

f (t) =

0

f (t, λ) dλ =

0

λk αkΓ(k) e−[t+1/α]λ^ dλ

Let u = [t + 1/α]λ ⇒ du = [t + 1/α] dλ. Then

f (t) =

αkΓ(k)

0

u t + 1/α

)k e−u^

du t + 1/α

=

αk[t + 1/α]k+

0 u

ke−u (^) du Γ(k)

α (αt + 1)k+

Γ(k + 1) Γ(k)

αk (αt + 1)k+

Therefore

f (t) =

kα (1 + αt)k+^

t > 0 , k > 0 , α > 0

and

S(t) =

t

f (x)dx =

t

kα (1 + αx)k+^

dx =

[

−(1 + αx)−k

]∞

t =^

(1 + αt)k

Since h(t) = f (t)/S(t), we have

h(t) =

kα/(1 + αt)k+ 1 /(1 + αt)k^

kα 1 + αt