Download Market Analysis of Continente: Understanding Consumer Preferences and Competition and more Assignments Food Science and Technology in PDF only on Docsity!

Booklet 1 of 2

A Work Project, presented as part of the requirements for the Award of Masters Degree in Management from NOVA School of Business and Economics

Continente Choose&Drive

Pedro Letteri Sepúlveda de Castelbranco

Student number 802

A project carried out on the Management Course, under the supervision of:

Professor Luísa Agante

4 th^ June 2012

- Index 0. Executive Summary

- The Portuguese Context

- 1.1 Economic Situation..........................................................................................................

- 1.2 Retail Market

- 1.3 Trends

- 1.3.1 Savings

- 1.3.2 Cocooning

- 1.3.3 Technology

- Continente World

- 2.1 Continente’s Background

- 2.2 Market Research

- 2.3 SWOT Analysis.................................................................................................................

- 2.4 TOWS

- Strategy

- Who are they?

- What do they value? What needs are not being satisfied?

- What products do they want?

- Why are they important for Continente?.............................................................................

- How can we solve this gap between the market and the needs of this segment?

- Choose&Drive Continente (C&D Continente)

- 4.1 Marketing Mix

- 4.1.1 Product

- 4.1.2 Placement

- 4.1.3 Process

- 4.1.4 People

- 4.1.5 Price

- 4.1.6 Physical Evidence

- 4.1.7 Promotion

- 4.2 Objectives & Issues........................................................................................................

- 4.2.1 Objectives

- 4.2.2 Issues

- Next Steps

- References

1. The Portuguese Context

1.1 Economic Situation

The published projections point to a contraction of the Portuguese economy in 2012, followed by a virtual stagnation in 2013 with unemployment rate expected to rise to 13.6 %. This economic downturn, which is unprecedented in the Portuguese economy, reflects a significant drop in domestic demand, both public and private, within a framework of basic adjustment of macroeconomic imbalances.^1

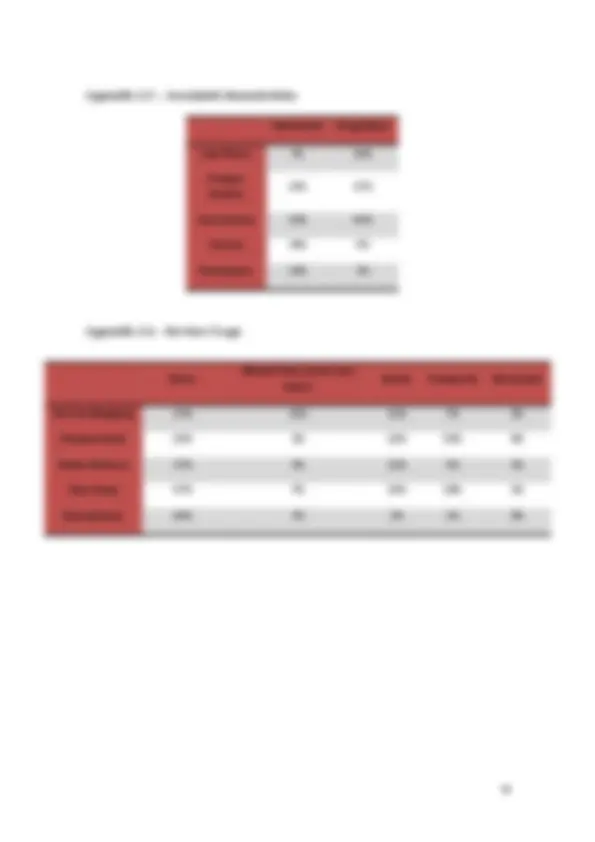

1.2 Retail Market^2 (Table 1)

Business Volume With regard to the business volume (appendix 1.1) of this market there is a clear discrepancy between the two main competitors (Continente and Pingo Doce-which I will call PD from now on) and the rest of the players. And while the Continente brand is the one with the biggest volume in the market, (with volume of 3555 million Euros) PD (with less 103 million Euros) shows the highest growing rate (11% against the 5% of Continente).

Number of Stores In terms of the number of stores (appendix 1.2), there was a slowdown in the growth of the number of stores compared with past years. Minipreço and PD have the largest number of stores (with 524 and 362 respectively).

Total Size of Stores Based on the analysis of the total size of stores (the sum of size of all the Brand’s stores), Continente and PD appear as clear leaders (with 516 thousands square meters

and 421 respectively) although it is Auchan and Minipreço that display the highest growing rate (with 5%) when compared to 2009 (appendix 1.4).

Number of Workers

Finally, in terms of Human Resources (appendix 1.3), Continente and PD appear again as market leaders with more than twice the labor force of the 3rd brand in this department (Auchan). The gap between PD and Continente is small (24152 working for PD and 21263 for Continente), however the growing rate is relevantly different (13% against 4% respectively).

Table 1 – The Market

1.3 Trends

When analyzing upcoming Trends we need to take into account the economic and social environment.

comfortable buying. Buying your milk and pasta on-line through your computer or phone at home is an ever increasing reality.

Specifically, in the food business, technology is also playing an important role. Brands like MacDonald’s are increasing their efficiency and service quality, by applying modern technology, allowing consumers to order their meal technologically^5.

2. Continente World

2.1 Continente’s Background

The brand has its origins in France in 1972 ("Continent"), the group Promodès was established in Portugal in the early 80’s introducing the concept of Hypermarket in the country. At that time Sonae, owned a supermarkets chain called Modelo. The two companies established a partnership that would become Modelo Continente S.A. The adoption of Continente under the "franchising" banner allowed Sonae to purchase the "Know How" of Promodès and in 1985 it opened the first hypermarket located in Matosinhos in Portugal.

In 2004, the Carrefour group exited the capital of Modelo & Continente S.A. and Sonae ended up gaining freely the exclusive rights to the trademark "Continent".

At the end of 2005, the brand underwent in a depth renovation, which changed the brand philosophy, the colors (which is now only Red) and the lettering. The symbol has become a stylized “C" as a target. The whole "rebranding" work was entrusted to the agency EuroRSCG.^6

More recently in 2011 Sonae announced the merger between Continente and Modelo believing that “we are stronger under just one brand” choosing the name Continente to represent both.^7

2.2 Market Research

In order to validate my research and better understand the market, the consumer, the brand and its limitations it is important to carry out surveys that will provide me with the necessary data that will help me strategize, improving what is wrong and better marketing what is right. By understanding consumers’ perception about the market and the brand we are able to sense their needs and wants, attempting to fulfill them and gain their loyalty. Over the last weeks we have started the first stage of this market research by conducting an on-line survey (appendix 10) addressed to 134 people in the 20 to 60 age range (42% from 20 to 29,12% from 30 to 39,23% from 40 to 49, 22% from 50 to 59 and 1% over 60), living in the largest urban centers (58% of the enquired lived were from Lisbon, while 28% where from Porto and 9% from Setúbal), the majority of whom have a university degree (91%). The answers have confirmed my original ideas of the market and the brand and stated Continente and PD as the most popular and visited brands. After a closer analysis (appendix 2.1) I was able to conclude that the brands were similarly beloved (41% choose PD as their favorite supermarket while 42% choose either Continente (34%), Continente Bom Dia (4%) or Continente Modelo(4%)). Moreover, people tend to spend more in each trip to Continente - 35% of Continente’s consumers claimed to spend more than 50 euros/per visit against 16% of PD’s

Weaknesses Stores are too big (making consumers spend more time) - What was once seen as an advantage may now be affecting Continente’s business negatively. Nowadays people tend to visit the store more often as opposed to only making once-a-month shopping. Continente may be perceived as too big a store for the daily quick grocery shopping. Stores less profitable than the competitor’s.^9 According to recent studies, PD has surpassed profitability per square meter, showing a growth of 11% from 2009 to 2010 (from 7409 Euros to 8206 Euros), while the Continente’s brand stated a growth percentage of 3%. Moreover while the company still shows a higher market share, its growing rate in 2010 is smaller than the one of its biggest competitor (a growth of 5% against a growth of 11% from PD). Inefficient Advertising - While the biggest spender in advertising the brand is unable to match the recognition achieved by its competitor showing some signs of inefficiency in their advertising^10. Smaller number of stores- When compared to the competition the 170 stores of Continente stores may seem too small a number (PD owns 362 and Mini Preço 524). This seems to imply that there is still some distance between the stores and the majority of its clients. Dumping- Recent news concerning practice of dumping by the Brand may negatively affect its image.^11 Losing Focus by entering new markets^12 - The brand is expected to enter the African (Angolan) market in 2013, which may imply losing focus on the national market, which is now as competitive as ever.

Opportunities Patriotism- In the current situation of crisis patriotism gains a new importance and Continente may take advantage of this increasing nationalist feeling ( gaining extra status due to the “unpatriotic” move of Jerónimo Martins (owner of PD) to Holland in order to gain tax benefits^13 ) On-line Boom- Taking into account the ever increasing importance of technology and convenience, the website (and all digital platforms) needs to be well prepared for this trend and be able to respond to it. Cocooning – Due to many variables (be it greater house comfort, or even the economic crisis and the consequent growth in unemployment) the cocooning trend has been increasing over the past few years. With people spending more and more time at home it is important for Continente not to overlook this trend and try to find answers for it

Threats Economic Crisis- Due to the economic crisis the company may see its profit decrease both because of the loss of costumers’ wealth and because of higher taxes.

Gas Prices^14 - On account of the location and number of stores problem, people

tend to use the car more to visit Continente’s stores (both because of larger shopping and because of the distance between their home and the store) – appendix 4.

(2)3rd^ Quadrant (Use your opportunities to overcome your weaknesses)

- By getting on-board with the technologic trend , the brand can overcome its location and structure problems (4)4th^ Quadrant (Overcome your weaknesses while minimizing your threats)

- Considering the distance weakness, and the need for a car (and therefore gas) that is associated to it, setting up mini-markets in gas station areas would minimize both issues. 3. Strategy

Based on the research described above it is plausible to say that the main issue of Continente’s lies with its convenience and that, obviously the most distant consumers from the brand are the ones that value convenience the most – “the single young shoppers” (90.3% of the enquired claimed to either value or value a lot convenience, higher than any other characteristic – see appendix 5).

In the last few years I have had the opportunity of coming into contact with their habits and patterns of life and have felt the gap between these new generations of shoppers and the Continente Brand (in the category of people from 20 to 29 on our survey, only 28% claimed Continente, Continente Modelo or Continente Bom-Dia as their favorite brand against a smashing 54% of consumers who choose PD as theirs – see appendix 6 for detailed information).

Given a second a more specific survey to young people living away from their parents’ house, I was able to gather 60 responses from which I extracted their needs, and their shopping pattern (appendix 12).

Who are they? I’ll call this specific segment the “Single Young Shoppers”. These consumer are usually young, living for the first time without their parents, and although may be sharing a house with some friends or other individuals they are for the 1st time shopping only for themselves. These consumers have left their parents’ house either because they are studying/ working far from the residence or because they are eager for independence. They start to feel the need to live their own lives at the pace they want and with the schedules they want.

What do they value? What needs are not being satisfied? For most of these “Single Young Shoppers” it is the first time they experience shopping at a supermarket, or at least alone. Until then, normally they relied on their parents to do the shopping for them. When this situation changes and they start doing their own shopping, they quickly become reluctant to spending time and energy getting out of the house, driving to the supermarket, parking the car, walking through the aisles, collecting the items, standing in line at the cashier, taking the groceries back to their car and driving back home. The whole routine is very unattractive for the “single young shoppers”. Given their busy lives they seek the fastest and easiest way to do their shopping. They want to be able to leave their work late at night, exhausted and tired and have a different and more convenient way to buy their shampoo, pasta, toothbrush or eggs in a fast and easy way, if possible without even leaving the car and be able to enjoy those products that very night.

How can we solve this gap between the market and the needs of this segment? Continente has already two solutions for this segment: Home delivery and the Continente Drive (where you order on-line and pick it up at the store, which service is currently only available at the Colombo Shopping Center).

However these solutions are not enough (see appendix 9): On the one hand, the complexity and confusion of the on-line platform is far from convenient for someone who just needs some pasta and sausages for the weekend, on the other hand both these solutions neglect the fact that these consumers are independent for the first time in their lives and do not want to be bound to neither schedules nor deadlines. These solutions also take away the impulse buying from these consumers since they do not plan ahead when and where they will have dinner. They can be at home one minute and leave to go out the next.

Thus, the solution must be available when they need it, usually after work. In order to gain this segment’s loyalty, Continente must be ready to provide these consumers with what they need in a fast, quick and practical way, when they want any specific item.

They need Choose&Drive Continente.

4. Choose&Drive Continente (C&D Continente)

4.1 Marketing Mix

4.1.1 Product

Choose&Drive Continente is very much like any drive-in at a fast food restaurant.

At Choose&Drive Continente, the consumers would be able to reach the store and if desired could shop directly at the Drive-in instead of the typical in-store shopping, thus all the shopping would be done without having to get out of the car.

This service makes it possible to satisfy the needs of our target group entirely. While not confined to time and place, consumers would be able to acquire their basic and most immediately needed items without losing a lot of time or energy.

The typical “postponed Shopping” that is so characteristic of this segment due to tiredness and demotivation, is minimized with Choose&Drive Continente and it is a practical and easy shopping system.

Convenience, one of the most valued characteristics for this target, would be highly increased, which would therefore boost their loyalty and appreciation for the Brand.

4.1.2 Placement

In terms of distribution it is important to understand consumers’ needs. The goal of Choose&Drive Continente is to be a solution for young workers who want to make their daily/weekly shopping without much trouble. To achieve this Choose&Drive Continente would have to be attached to Continentes near either the “Working” areas or Residential ones. It is also important to open Choose&Drive Continente where there is a

In each sector consumers would have a restricted set of items each one with 3 possible choices (the cheapest, best-sellers, and the Continente brand). In order to reduce time spent per consumer and therefore the waiting time, each costumer would only be able to buy up to 10 items. The payment would be possible thought debit/credit card right after the confirmation of the request in the machine. At the end of this stage, consumers would be given a code (on a small talon) that would later be used to pick up their shopping in the following window. It is also important to reorganize the schedules in order to better serve our consumers. Establishing a night schedule (from 6 to 12pm) would increase the personal costs (since the night shifts are often more expensive) but at the same time it would significantly increase our attendance.

4.1.4 People

In order to provide a good service I believe that 6 people would be needed full time between 6 and 12 p.m. divided by 4 sectors: Food & Drinks; Cleaning Products (and possible malfunctions); Hygiene and Delivery (observe table 3).

In order to better serve our consumers the personnel must be efficient, quick and sharp. Choose&Drive employees must be able to quickly guide themselves through the aisles in order to waste the less amount of time on getting the products and delivering them to

Sector Number of people Food & Drinks 3 Cleaning & Malfunctions 1 Hygiene 1 Delivery 1 Total 6

Table 3 – Number of people

the consumer. This could be optimized by means of a fast workshop were a map of the items would be displayed and techniques taught on how to better communicate between co-workers in order to minimize waste of time. Since Food & Drinks are the most requested products, this section will require 3 people to get the items faster and more efficiently. The employee assigned to the Cleaning items (where the demand is lower) would also be the employee designated to fix malfunctions and would therefore need to have some basic knowledge in that area. Payment: The payment will be restricted to credit/debit card only. It will be done thought the machine.

4.1.5 Price

Based on my survey (see appendix 10), I can safely assume that an additional 5% could be added to the price, with 62% stating they would be willing to pay at least 5% more to enjoy this service (38% claimed they would pay an extra 5%, 18% stated they would pay an extra 10% and 5% claimed they would be willing to pay an extra 15% for this service). This would help the construction of the new facilities (the street, the window and the ordering machine) as well as support the promotion costs.

Given our target’s profile, the availability of a fast, efficient, convenient shopping system would clearly be worth the extra price of the products; also this innovative system does not have any competition that would force Continente to lower the price.