Download Cost Behavior and Cost Estimation and more Slides Cost Management in PDF only on Docsity!

Cost Behavior

and

Cost EstimationCost Estimation

1

Types of Cost Behavior Patterns

Summary of VC and FC Behavior

Cost In Total Per Unit

Total VC is VC per unit remains VC proportional to the activity the same over wide ranges level within the RRlevel within the RR. of activityof activity. Total FC remains the same even when the activity FC per unit goes FC level changes within the down as activity level goes up. RR.

The Activity Base

Units

produced

Machine

hours

A f h t

p

A measure of what

causes the

iincurrence of a VC f VC

Miles

driven

Labor

driven hourshours

3

True VC Example

A VC is a cost whose total dollar amount varies in direct proportion to changes in the activity level. Supposed you had a phone bill that

$

to changes in the activity level. Supposed you had a phone bill that is based on the number of minutes talked.

e Bill $$

Phone

Total

Minutes Talked

Extent of Variable Costs

The proportion of VCs differs across organizations. For example...

A public utility withA public utility with large investments inlarge investments inlarge investments inlarge investments in A manufacturing companyA manufacturing company equipment will tendequipment will tend to haveto have fewerfewer

A manufacturing companyA manufacturing company will often havewill often have manymany VCs.VCs. VCs.VCs.

A merchandising companyA merchandising company usually will have ausually will have a highhigh A service companyA service company will normally have awill normally have a highhigh proportionproportion of VCs,of VCs, like cost of sales.like cost of sales.

will normally have awill normally have a highhigh proportionproportion of VCs.of VCs.

7

Examples of Variable Costs

1. Merchandising companies – cost of goods sold.

2. Manufacturing companies – direct materials,

direct labor and variable overheaddirect labor, and variable overhead.

3. Merchandising and manufacturing companies –

commissions, shipping costs, and clerical costs,

such as invoicing.

4. Service companies – supplies, travel, and

clericalclerical.

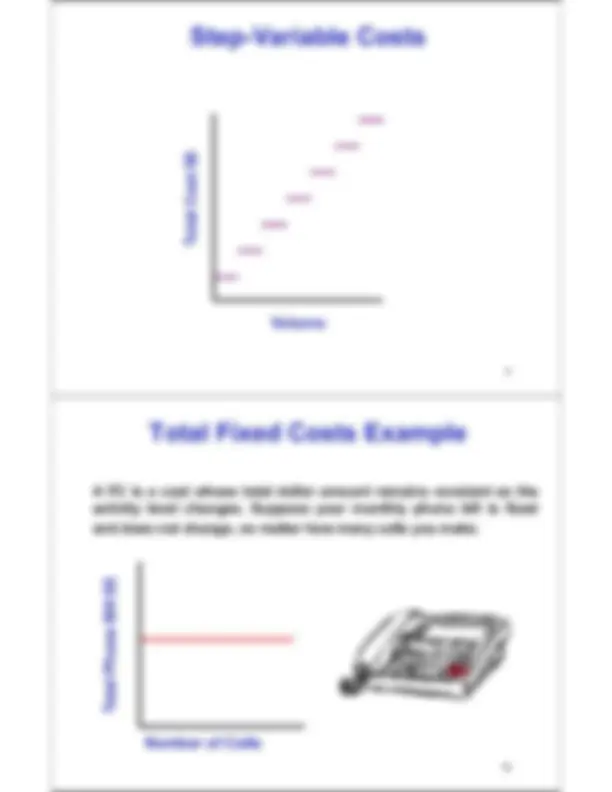

Step-Variable Costs

Cost $$

Total CT

Volume

9

Total Fixed Costs Example

A FC is a cost whose total dollar amount remains constant as the activity level changes. Suppose your monthly phone bill is fixed and does not change, no matter how many calls you make.

$$

ne Bill $

al Phon Tota

Number of Calls

The Linearity Assumption

and the Relevant Rangeg

Relevant s R t $$ Range

tal Cos Tot

Activity

13

Prepare an Income Statement

Using the CM FormatUsing the CM Format

TotalTotal UnitUnit

Revenue $ 100,000 $ 50

Less: VCLess: VC 60 00060,000 3030

CM $ 40,000 $ 20

Less: FC 30,

Net Income $ 10,

ThThThThe CM format emphasizes cost behavior. CM e CM format emphasizes cost behavior. CMCM fCM f tt hh ii t b ht b h ii CMCM

covers FCs and provides for Net Income.covers FCs and provides for Net Income.

Uses of the Contribution (CM) Format

ThThThThe CM income statement format is used as an e CM income statement format is used as anCM iCM i t tt t t ft f t it i dd

internal planning and decision making tool. Usesinternal planning and decision making tool. Uses

of this approach include:of this approach include:f thif thi h ih i l dl d

1.1. CVP analysisCVP analysisyy

2.2. BudgetingBudgeting

3.3. Segmented reporting of profit dataSegmented reporting of profit data

44 4.4. Special decisions such as pricing and make Special decisions s ch as pricing and makeSpecial decisions s ch as pricing and make orSpecial decisions such as pricing and make--ororor--

buy analysisbuy analysis

15

Contribution (CM) Format

Used primarily forUsed primarily for external reportingexternal reporting

Used primarily byUsed primarily by external reporting.external reporting. managementmanagementmanagement.management.

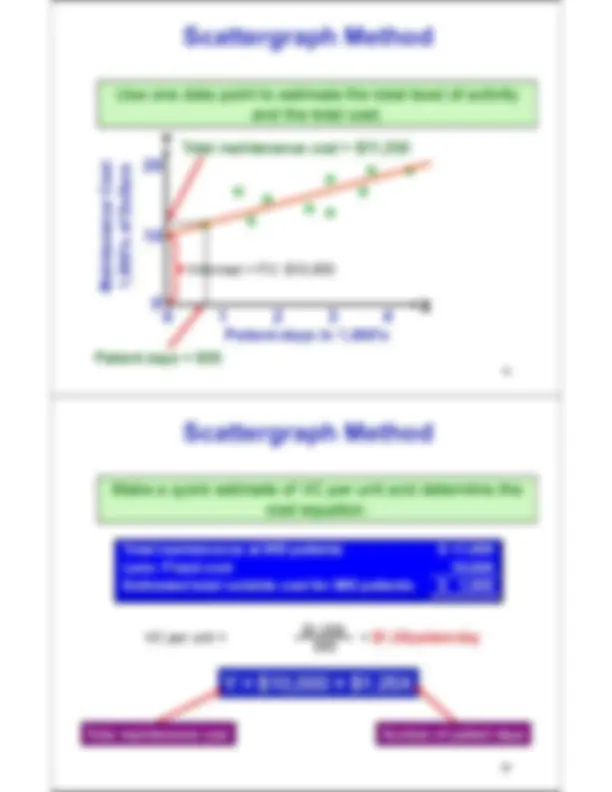

Scattergraph Method

Use one data point to estimate the total level of activityUse one data point to estimate the total level of activity and the total cost.and the total cost. Y (^) Total maintenance costTotal maintenance cost = $11 000 = $11 000

Cost^ * ollars

Total maintenance costTotal maintenance cost $11$11,000,

enances of Do 10 *^ *

Intercept = FC: $10, Mainte1,000’s 0 1 2 3 4

Patient-days in 1,000’s

X

Patient days in 1,000 s Patient days = 800Patient days = 800 19

Scattergraph Method

Make a quick estimate of VC per unit and determine theMake a quick estimate of VC per unit and determine the cost equation.cost equation.

Total maintenance at 800 patientsTotal maintenance at 800 patients $$11 000 11 , Less: Fixed cost 10, Estimated total variable cost for 800 patients $ 1,

VC per unitVC per unit = $1,000 800 = $1 25/patient$1 25/patient-$1.25/patient$1.25/patient day-daydayday

Y = $10 000 + $1 25XY = $10 000 + $1 25XYY $10,000 + $1.25X$10,000 + $1.25X

Total maintenance costTotal maintenance costTotal maintenance costTotal maintenance cost Number of patient daysNumber of patient daysNumber of patient daysNumber of patient days

High-Low Method

TheThe VC per hourVC per hour ofof maintenance is equal tomaintenance is equal to the change in cost dividedthe change in cost divided by the change in hours.by the change in hours.yy gg

= $8.00/hour$8.00/hour

21

High-Low Method

Total FCTotal FC = Total Cost –Total FCTotal FC = Total CostTotal CostTotal Cost – Total VCTotal VCTotal VCTotal VC

Total FC = $9,800Total FC = $9,800 –– ($8/hour($8/hour ×× 800 hours)800 hours)

Total FC = $9,800Total FC = $9,800 –– $6,400$6,

Total FC =Total FC = $3,400$3,

Regression Method

- Software can be used to fit

a regression line through

the data points.

- The cost analysis objectiveThe cost analysis objective

is the same: Y = a + bX

Regression also provides a statistic, called the R 2 , which is a measure of the goodness of fit of the regression line to the data points.

25

Regression Method

RR 2 2 iis the percentage of the variation in total cost th t f th i ti i t t l t explained by the activity.

Y

Cost *

Total

10 *^ * R 2 varies from 0% to 100%, and the higher the percentage the better

the higher the percentage the better.

0 1 2 3 4 X

Activity