COUNTRY

RISK

By:

Saif Ullah

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An historical analysis of sovereign risk events, focusing on debt repudiation and rescheduling. It covers the expansion of loans to less developed countries (ldcs) in the 1970s, the emerging markets crisis in the late 1990s, and the impact of argentina's debt crisis in the early 2000s. The document emphasizes the importance of assessing country risk before making lending decisions and discusses the methods used by financial institutions to evaluate sovereign risk.

Typology: Exams

1 / 37

This page cannot be seen from the preview

Don't miss anything!

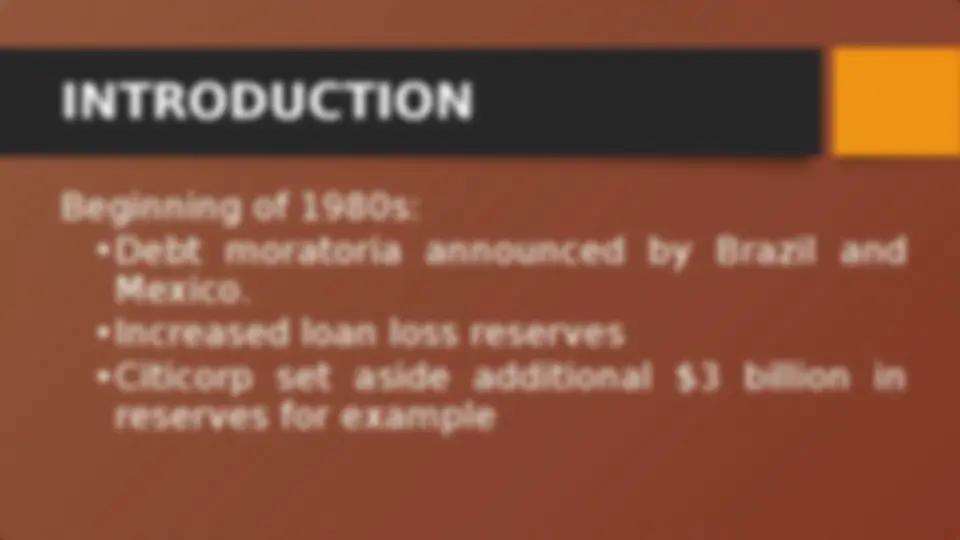

INTRODUCTION

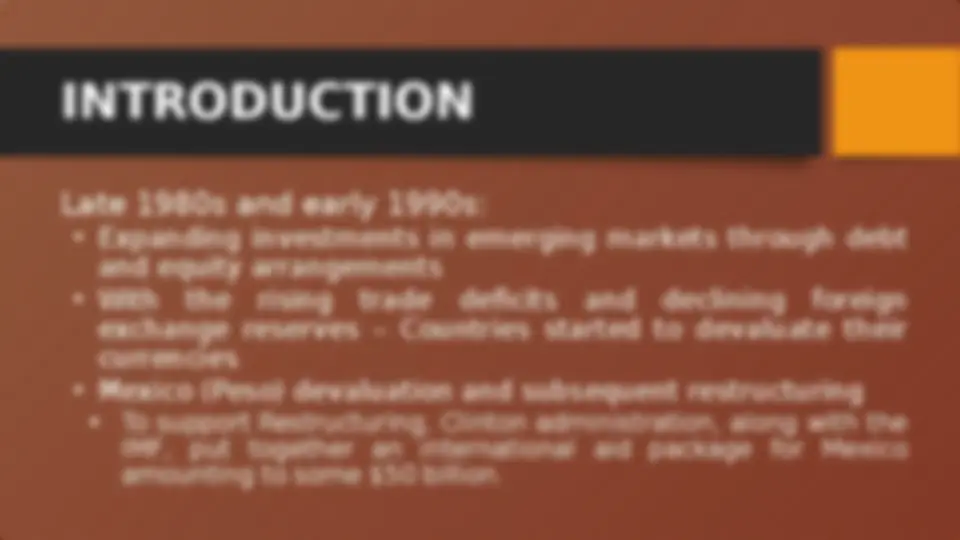

INTRODUCTION Late 1980s and early 1990s:

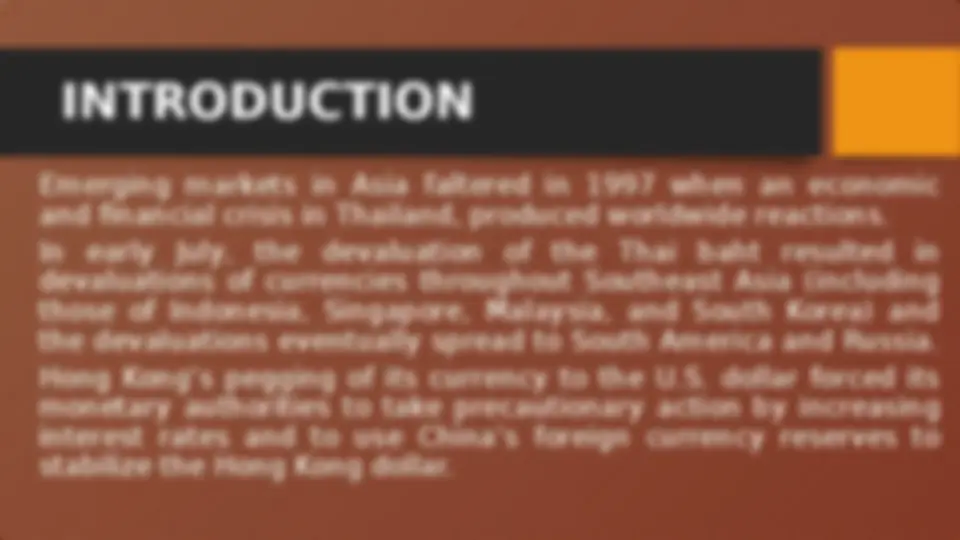

INTRODUCTION Emerging markets in Asia faltered in 1997 when an economic and financial crisis in Thailand, produced worldwide reactions. In early July, the devaluation of the Thai baht resulted in devaluations of currencies throughout Southeast Asia (including those of Indonesia, Singapore, Malaysia, and South Korea) and the devaluations eventually spread to South America and Russia. Hong Kong’s pegging of its currency to the U.S. dollar forced its monetary authorities to take precautionary action by increasing interest rates and to use China’s foreign currency reserves to stabilize the Hong Kong dollar.

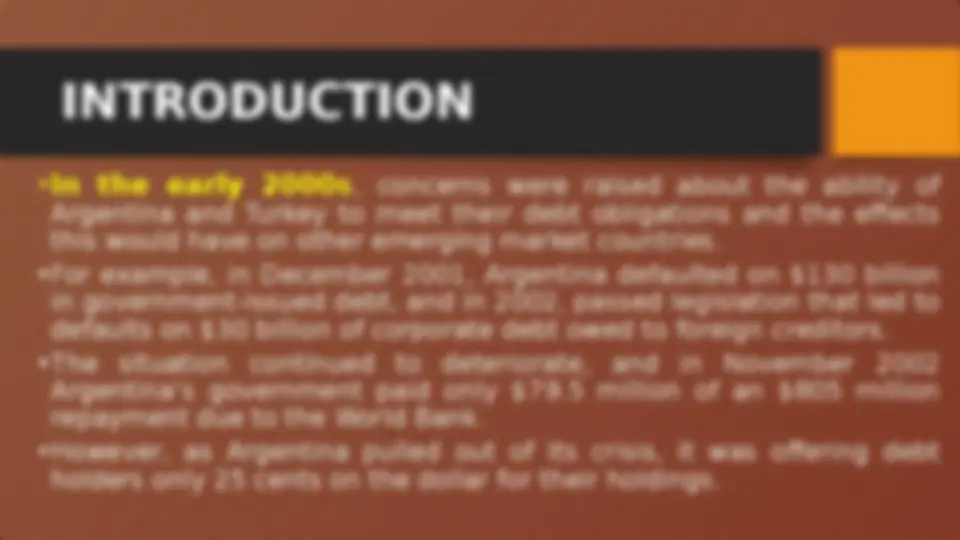

INTRODUCTION

INTRODUCTION

SOVEREIGN RISK

SOVEREIGN RISK

DEBT REPUDIATION VERSUS DEBT RESCHEDULING A sovereign country’s (negative) decisions on its debt obligations or the obligations of its public and private organizations may take two forms: Repudiation Rescheduling

DEBT REPUDIATION Repudiation is an complete cancelation of all a borrower’s current and future foreign debt and equity obligations. Since World War II, only China (1949), Cuba (1961), and North Korea (1964) have followed this course.

DEBT RESCHEDULING First, there are generally fewer FIs in any international lending groups compared with thousands of geographically dispersed bondholders. The relatively small number of lending parties makes renegotiation or rescheduling easier and less costly than when a borrower or a bond trustee has to get thousands of bondholders to agree to changes in the contractual terms on a bond.

DEBT RESCHEDULING Second, many international loan groups comprise the same groups of FIs, which adds to FI giants in loan renegotiations and increases the probability of consensus being reached. For example, Citigroup was chosen the lead bank negotiator by other banks in five major loan rescheduling's in the 1980s, as well as in both the Mexican and South Korean rescheduling's. J. P. Morgan Chase is the lead bank involved in the recent loan rescheduling's of Argentina.

DEBT RESCHEDULING Fourthly, behavior of governments and regulators in lending countries. One of the over-whelming public policy goals in recent years has been to prevent large FI failures in countries such as the United States, Japan, Germany, and the United Kingdom.

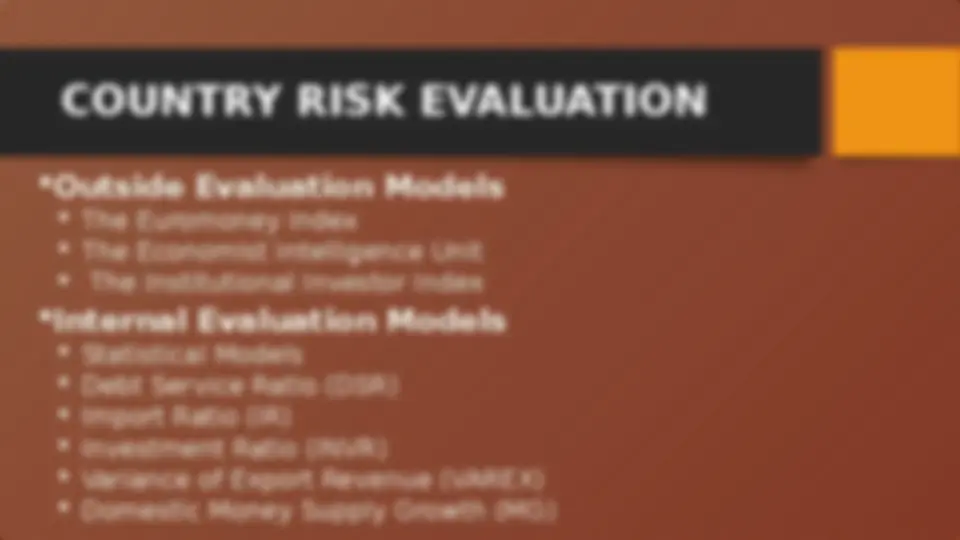

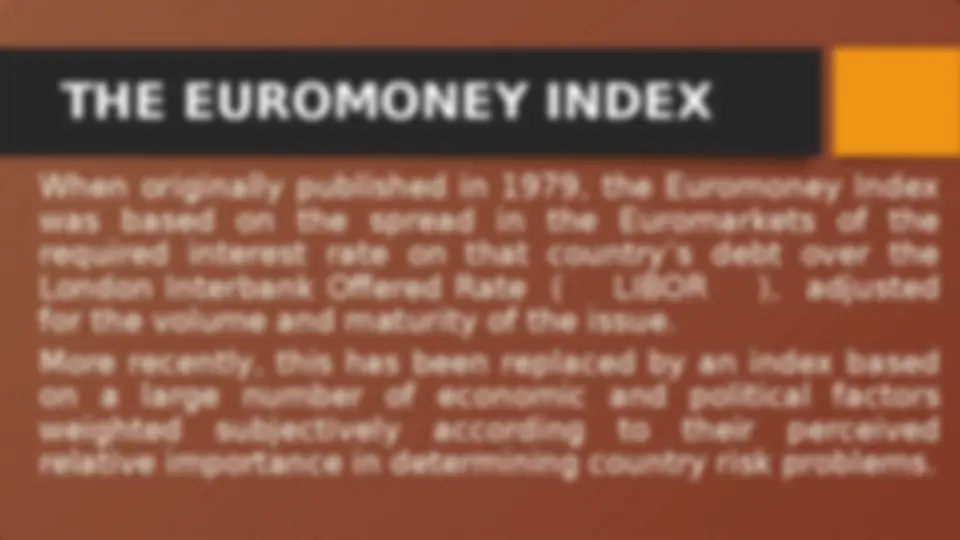

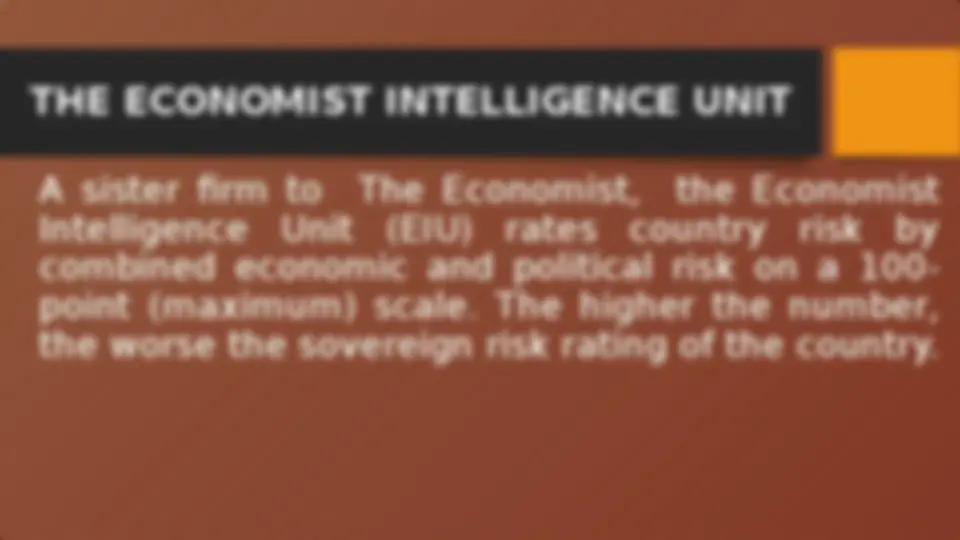

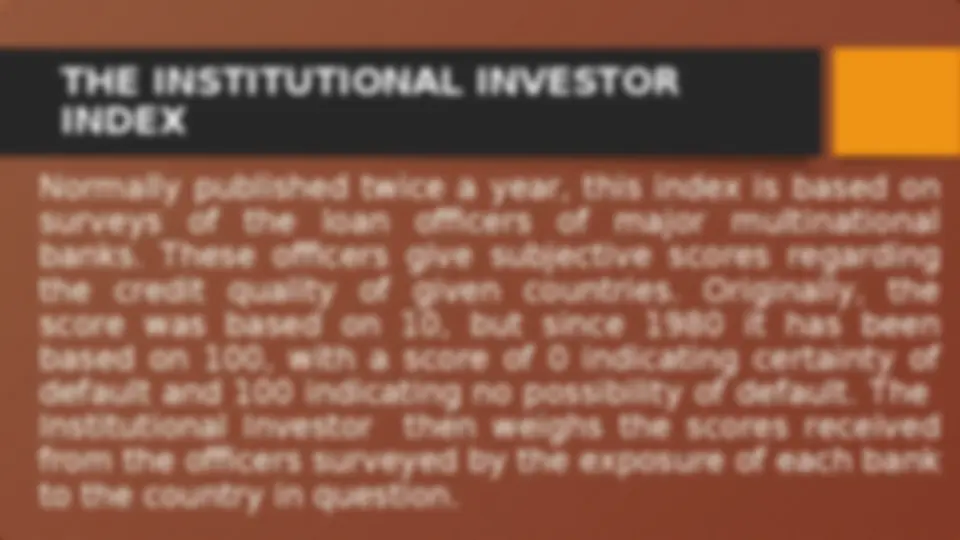

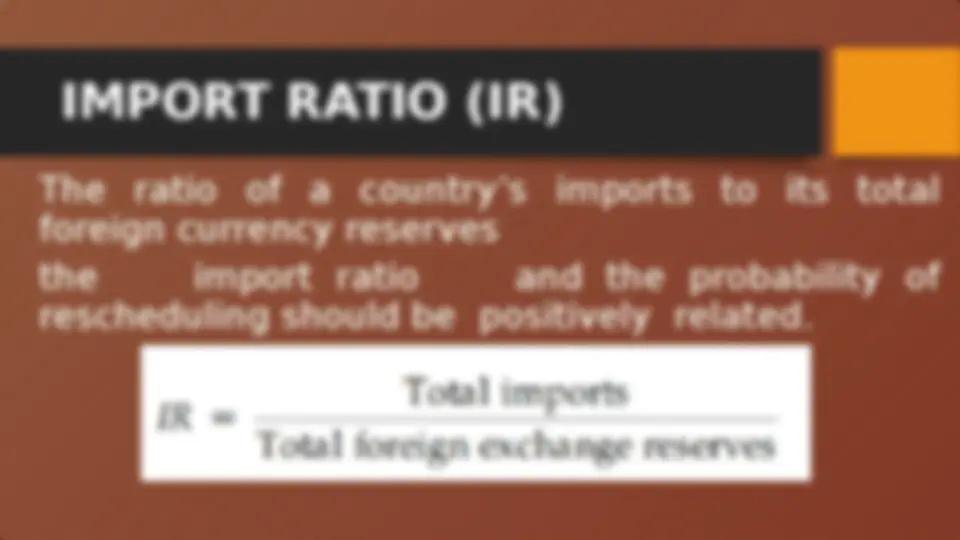

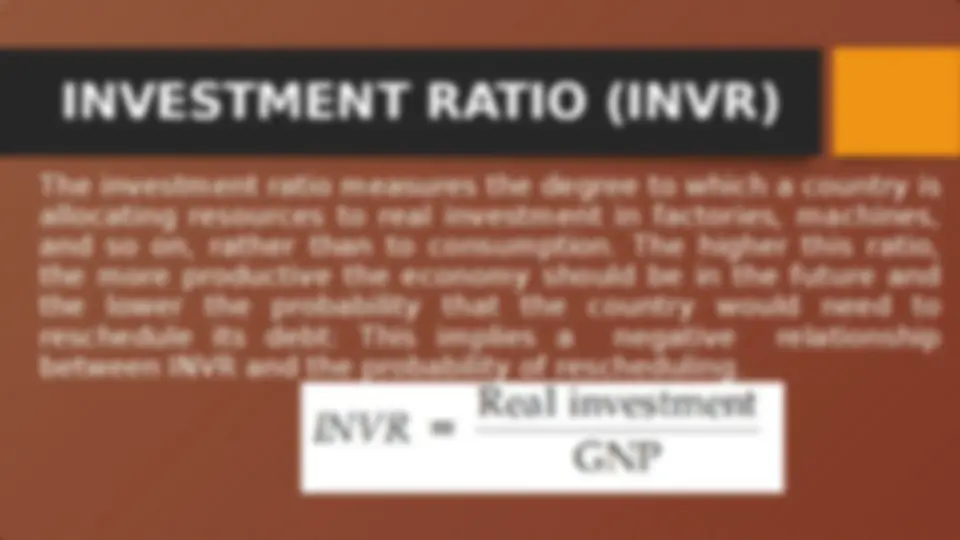

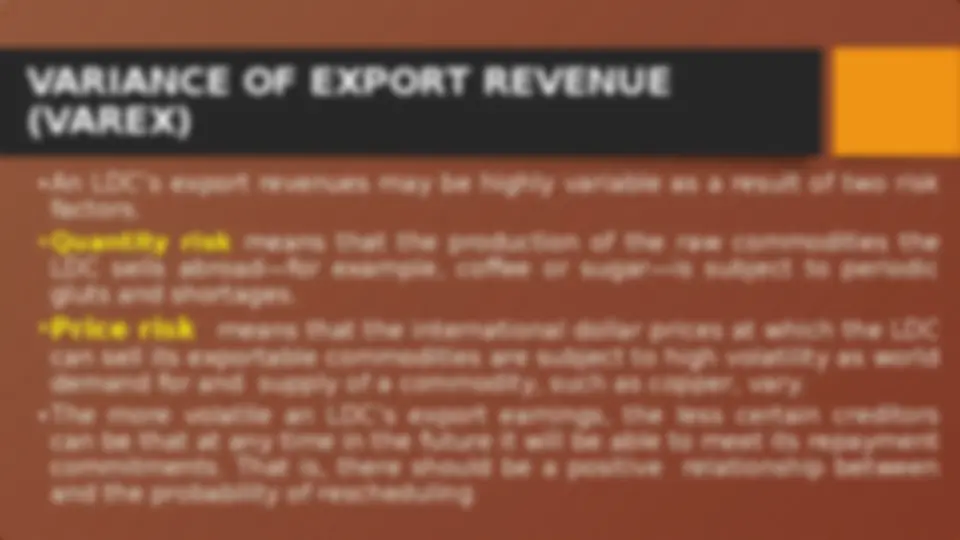

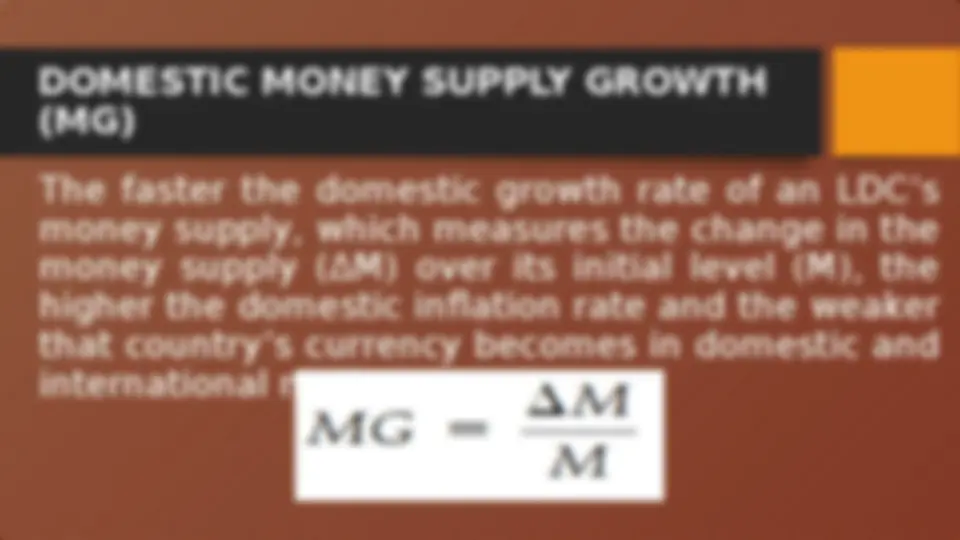

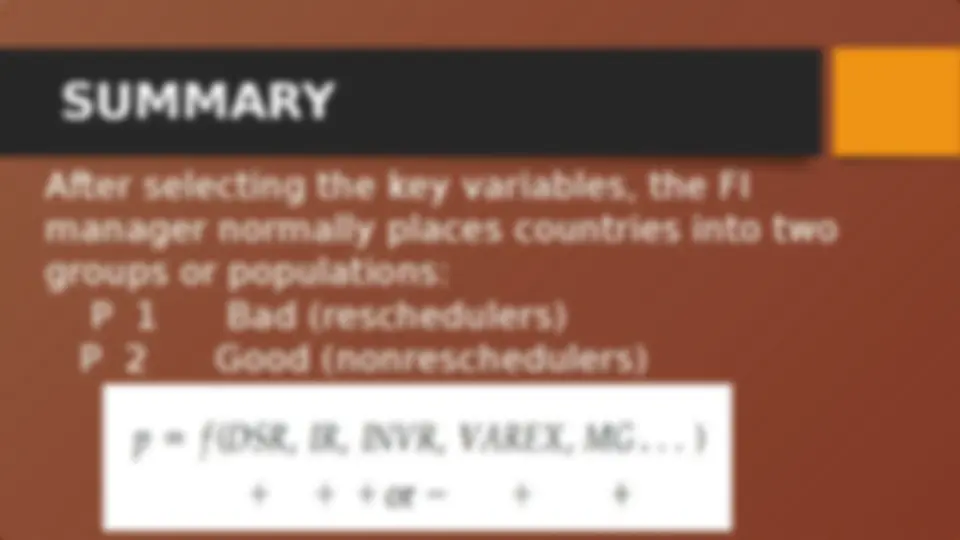

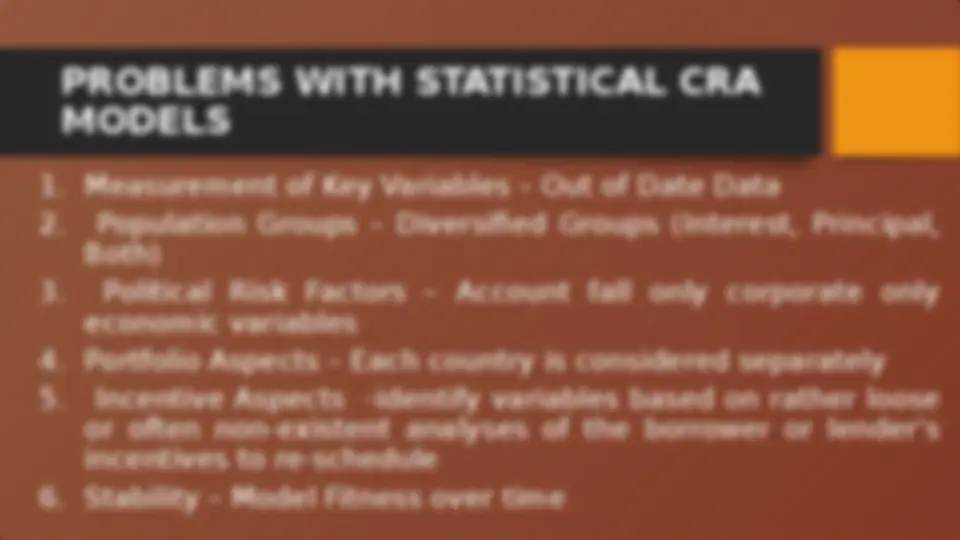

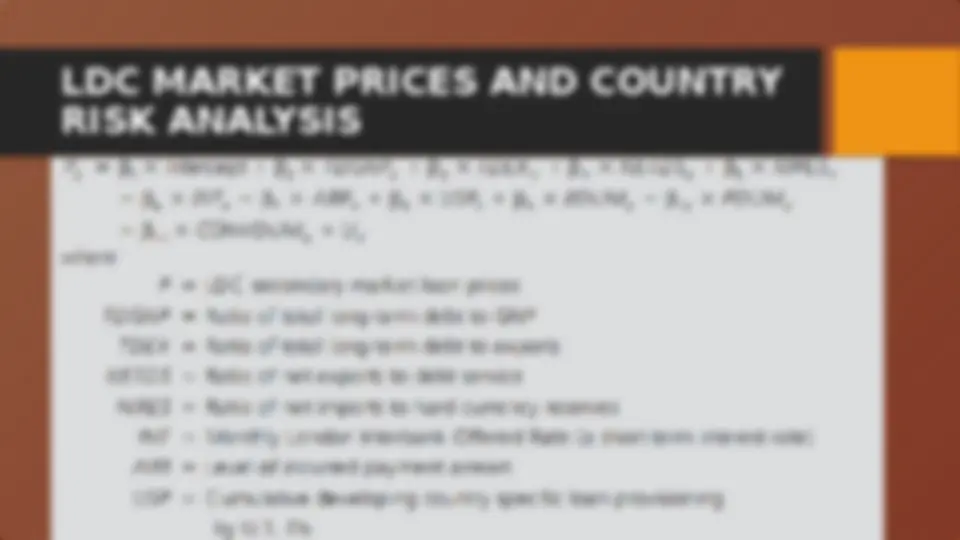

COUNTRY RISK EVALUATION