Credit scoring model

By

Batchu Satish

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Credit scoring can be formally defined as a statistical method that is used to predict the probability that a loan applicant or existing borrower will default or become delinquent

Typology: Lecture notes

1 / 15

This page cannot be seen from the preview

Don't miss anything!

What is credit scoring?

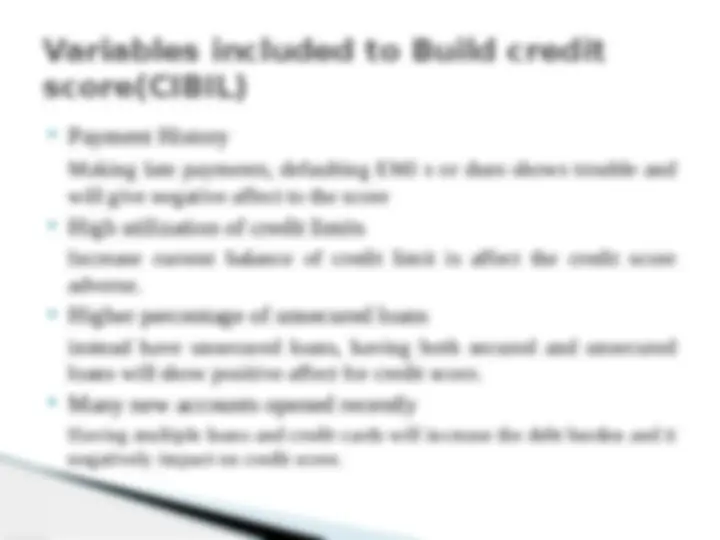

(^) Payment History Making late payments, defaulting EMI s or dues shows trouble and will give negative affect to the score (^) High utilization of credit limits Increase current balance of credit limit is affect the credit score adverse. (^) Higher percentage of unsecured loans instead have unsecured loans, having both secured and unsecured loans will show positive affect for credit score. (^) Many new accounts opened recently Having multiple loans and credit cards will increase the debt burden and it negatively impact on credit score. Variables included to Build credit score(CIBIL)

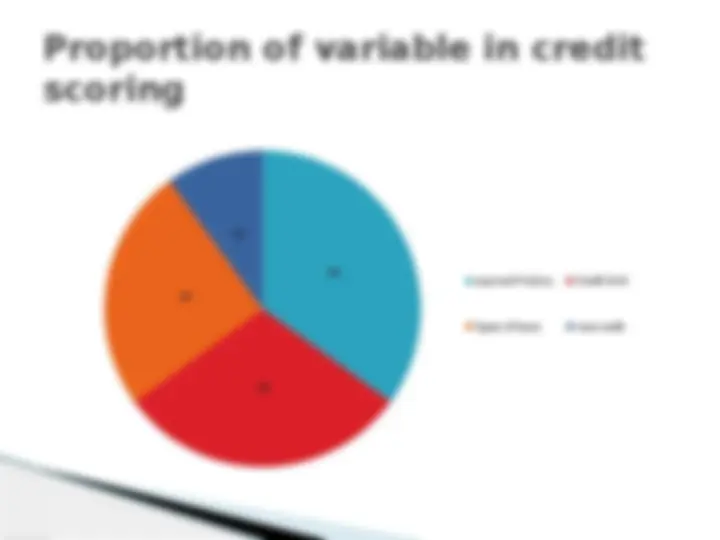

35 30 25 10 payment history Credit limit Types of loans new credit Proportion of variable in credit scoring

(^) A standard life cycle model for credit scoring designed on the basis of A-IRB approach(BASEL II capital requirement) (^) Life cycle of any model is defined three phases i.e. assessment, implementation and validation. (^) Model assessment ◦ (^) In order to develop credit scoring model we need past behavior of client data, so that we can assess the Probability of default or non-default. ◦ (^) If past details of client and sufficient data is available we go for empirical model, it is used for existing clients. ◦ (^) If past data is not available, new client, an expert or generic model is suitable for solution. Credit scoring Models life cycle

(^) It allows the banks to implement automated decision system to manage their retail client (^) In implemented process the main task for credit manager is to define most appropriate and efficient threshold/ cut-off to credit model (^) To maximize the benefit of scoring model, cut-off should be set taking into account of all misclassification accounts of Type-I and Type-II errors. Model Implementation

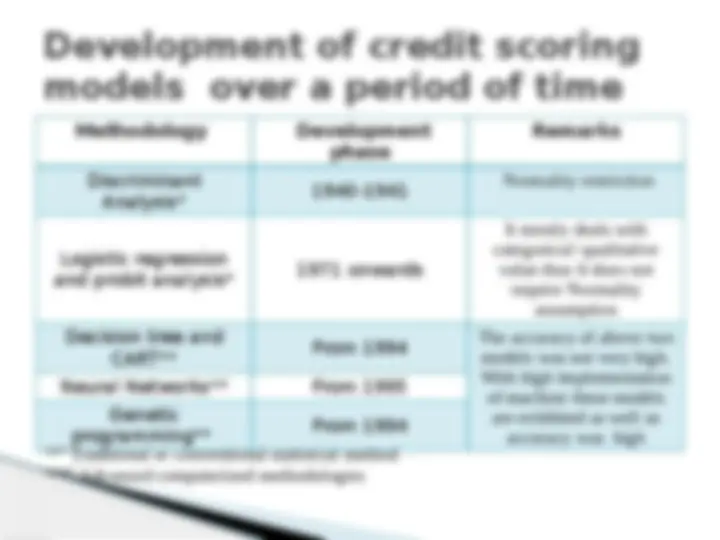

Methodology Development phase Remarks Discriminant Analysis* 1940- Normality restriction Logistic regression and probit analysis* 1971 onwards It mostly deals with categorical/ qualitative value thus It does not require Normality assumption Decision tree and CART** From 1994 The accuracy of above two models was not very high. With high implementation of machine these models are exhibited as well as accuracy was high Neural Networks** From 1995 Genetic programming** From 1994 Development of credit scoring models over a period of time ‘” Traditional or conventional statistical method ‘*” Advanced computerized methodologies

(^) For Individual; With use of some methods we can assess the cut-off as well as comp- re with different methods and then identify the best cut-off. Conceptual framework for credit scoring Individual Borrowers Variable consider for credit scoring Age Time at present address Profession Private/public sector Time at current profession Monthly revenues House owner No previous credits Duration of the loan Amount and type of loan And other demographic Cut-off Approval of loan Include some parameters which can improve the score YE S No

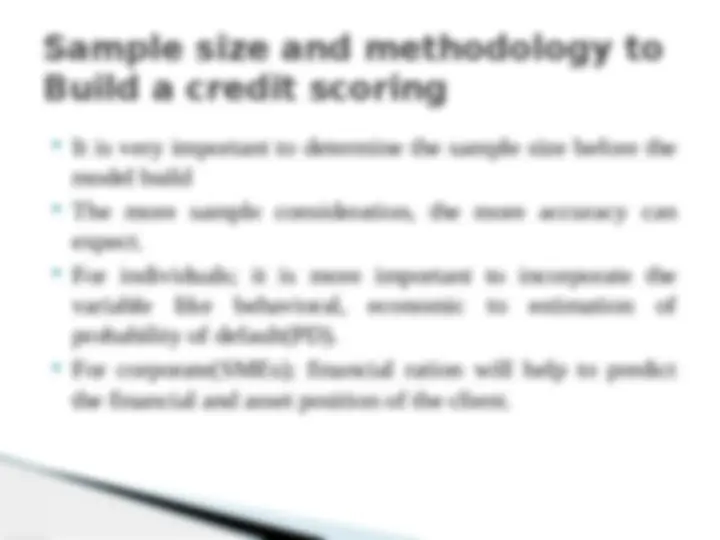

(^) It is very important to determine the sample size before the model build (^) The more sample consideration, the more accuracy can expect. (^) For individuals; it is more important to incorporate the variable like behavioral, economic to estimation of probability of default(PD). (^) For corporate(SMEs); financial ration will help to predict the financial and asset position of the client. Sample size and methodology to Build a credit scoring

(^) For individuals; ◦ (^) credit score be one of the most important factors in determining whether or not you are approved for credit. ◦ (^) it also be a major factor in determining the terms and conditions of the loan/credit extension. ◦ (^) It can help to understand the interest rate structure for loan applicant. low credit score= high interest (vice-versa)