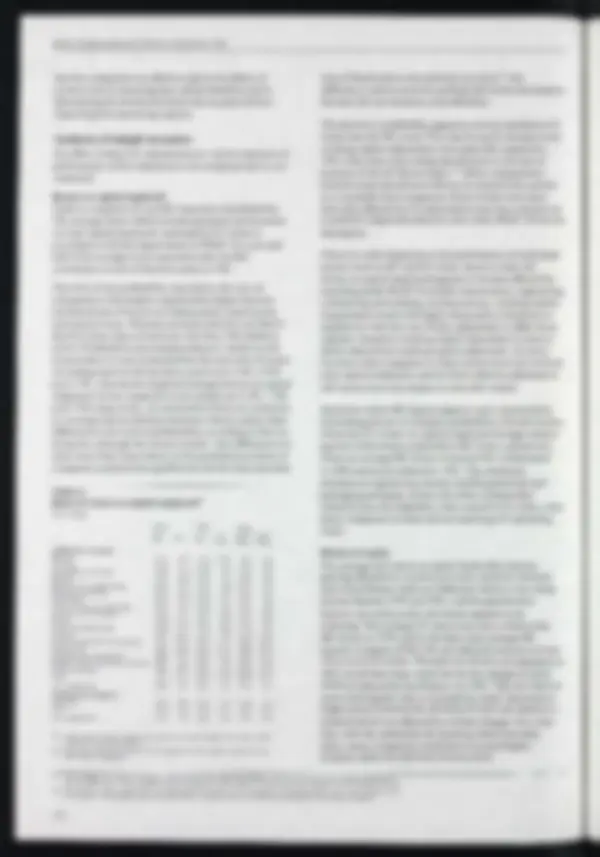

Current cost accounting

This article analyses the accounts of some 250 major companies, prepared according to current cost and

historic cost conventions, for the last three years.

Historic cost accounting generally overstates profitability-the average current cost pre-tax return on

capital is around half the historic cost figure. Industries most affected are textiles, motors, paper and

packaging and chemicals, while construction, engineering contracting and retailing are least affected.

Post-tax returns on equity are reduced even more using current cost accounting.

Around half the companies studied have paid dividends that were not fully covered by current cost profits.

Introduction

In recent years, various articles in the Bulletin have

discussed trends in the real profitability of industrial and

commercial companies (ICCs). (I) These articles were based

on national accounts data, and use aggregate figures for

ICCs;(2) they do not use companies' own current cost (CC)

adjustments. However, most major companies have by

now produced two, and in some cases three, years' results

on a CC basis under the Statement of Standard Accounting

Practice No 16 (SSAP 16) introduced with effect from

January 1980; their accounts, taken together, represent a

substantial body of information on the impact of inflation

on company results and on the effects on management

decisions of CC accounting. This article discusses some

findings of a recent study of the accounts of a sample of

almost 250 major companies, most of which have turnover

in excess of £ 1 00 million; in 1981 the total of their current

cost capital employed was some £165 billion. The aim was

to examine the impact of the SSAP 16 adjustments on

corporate p}ofitability, net earnings and dividend cover as'

reported on an historic cost (HC) basis, distinguishing

where possible between different industrial sectors.

The findings of this study are not directly comparable with

the estimates of company profitability derived from

national accounts data. There are a number of obvious

differences:

• the national accounts data exclude overseas

activities, whereas the analysis described here is

based upon the reported consolidated results ofUK

company groups, including where applicable

overseas activities;

• profitability measures based on national accounts

data exclude non-trading income, which is included

by companies in their accounts;

• the national accounts figures make no allowance for

the accelerated write-off of obsolete or redundant

(I) See for example 'Profitability and company finance' in the June 1982 Bulletin.

plant and machinery-such write-offs by companies

in their accounts may have become increasingly

significant in recent years;

• the companies included in this study are major listed

companies, while the national accounts data seek to

cover the whole corporate sector;

• differences arise between the financial information

reported by companies and the data collected in the

national accounts because of the different treatments

of, inter alia, depreciation, taxation and

extraordinary items (eg redundancy payments);

• the data do not cover identical time periods because

company accounting periods are not uniform and it

is impossible to aggregate company results according

to precise calendar years.

These variations in approach give rise to different absolute

levels of real profitability, but the trends identified in this

study are generally consistent with the trends in real

profitability calculated from national accounts data.

In preparing data for this analysis, the only adjustments

made to companies' reported financial information have

been to remove the effects of any prior-year deferred

taxation adjustments following the changes in stock relief

introduced by the Finance Act 1981; and to reverse,

wherever possible, the effects on the HC accounts of

any revaluations of fixed assets and of any additional

depreciation in the cases of companies which adopt a

modified HC convention. (3) The analysis covers the three

years 1979-81; company results were aggregated on the

basis of accounting periods most closely coinciding with

calendar years. Approximately half of the companies

reviewed chose not to publish comparable figures

for 1979 in their 1980 CC statements; this was permitted by

SSAP 16. Those companies whose real profitability was

most depressed were perhaps more likely to choose not to

(2) However, some work has been done on a sectoral breakdown of real profitability: see, N P Williams, influences on the

profitability 0/ twenty-two industrial sectors, Bank of England Discussion Paper No 1 S, March 1981.

(3) However, in the majority of cases where companies have incorporated revaluations into their He accounts, it has not been

possible to identify the effects, if any, on capital employed or on the depreciation charge, and the results should be interpreted

in this light.

376