CVP Analysis

1

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An in-depth analysis of the contribution format used by Racing Bicycle Company for internal planning and decision making. the uses of the contribution format, the contribution margin format, CVP relationships in graphic form, contribution margin ratio, break-even analysis, target profit analysis, and the margin of safety. The document also explains the contribution margin method and its equations to calculate the break-even point and the target profit.

Typology: Study notes

1 / 28

This page cannot be seen from the preview

Don't miss anything!

Th

t ib ti

i^

t t

t f

t i

d

Th

t ib ti

i^

t t

t f

t i

d

Th

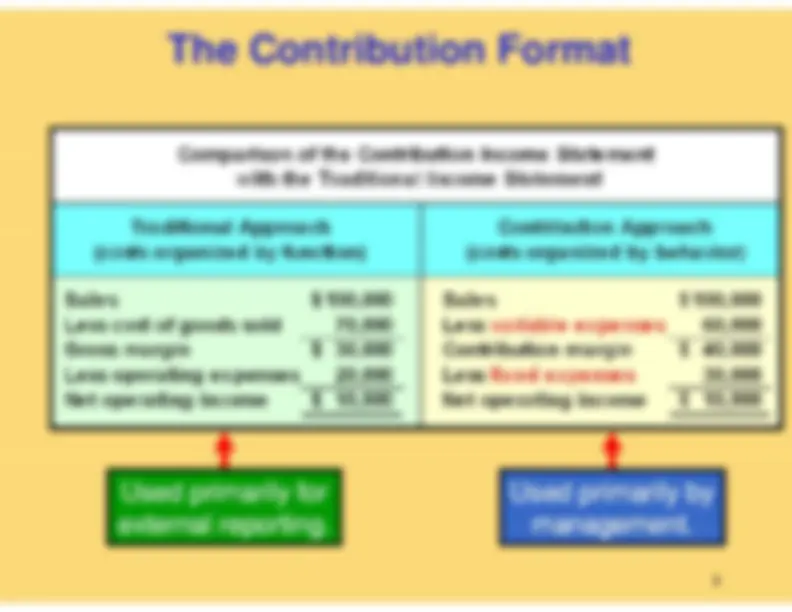

e contribution income statement format is used The contribution income statement format is used

as an internal planning and decision making tool.as an internal planning and decision making tool.Thi

h i

f l f

Thi

h i

f l f

This approach is useful for:This approach is useful for: 1.1. Cost

Cost-

-volumevolume-

-profit analysisprofit analysisp

y

p^

y

2.2. Budgeting

Budgeting 3.3. Segmented reporting of profit

Segmented reporting of profit data

data

Special decisions s ch as pricing and makeSpecial decisions s ch as pricing and make or

or

4.4. Special decisions such as pricing and make

Special decisions such as pricing and make-

-oror-

buybuy analysis

analysis

2

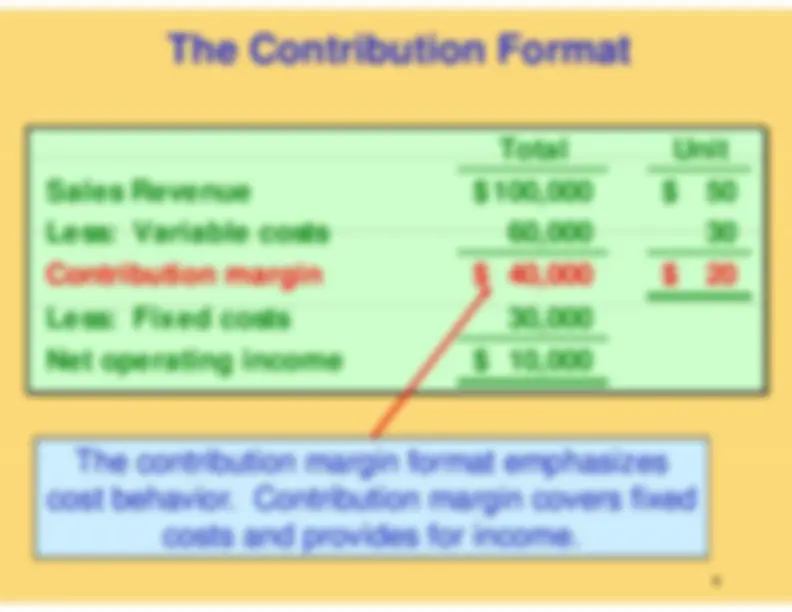

Total

Unit

Total

Unit

Sales Revenue

100, $^

50 $

Less: Variable costs

60 000

30

Less: Variable costs

60,

30

Contribution margin

40, $^

20 $

Less: Fixed costs

30,

Net operating income

10, $

Th

t ib ti

i^

f^

t^

h^

i

Th

t ib ti

i^

f^

t^

h^

i

Th

e contribution margin format emphasizes The contribution margin format emphasizes cost behavior. Contribution margin covers fixedcost behavior. Contribution margin covers fixed

t^

d^

id

f^

i

t^

d^

id

f^

i

costs and provides for income.costs and provides for income.

3- 5

4

0 000 450,000 400,000 350 000

Total Sales

350,000300,000 250,

Total Expenses

Total

Sales

200,000 150,

,

Fixed Expenses

Total Expenses

100,000^ 50,

100

200

300

400

500

600

700

800

U itUnits

4

0 000 450,000 400,000 350 000

BreakBreak-

-even pointeven point

(400 units or $200,000 in sales)(400 units or $200,000 in sales)

350,000300,000 250,000200,000150,

, 100,00050,

100

200

300

400

500

600

700

800

U itUnits

i^

t^

f^

it

th

t ib ti

i^

ti

i

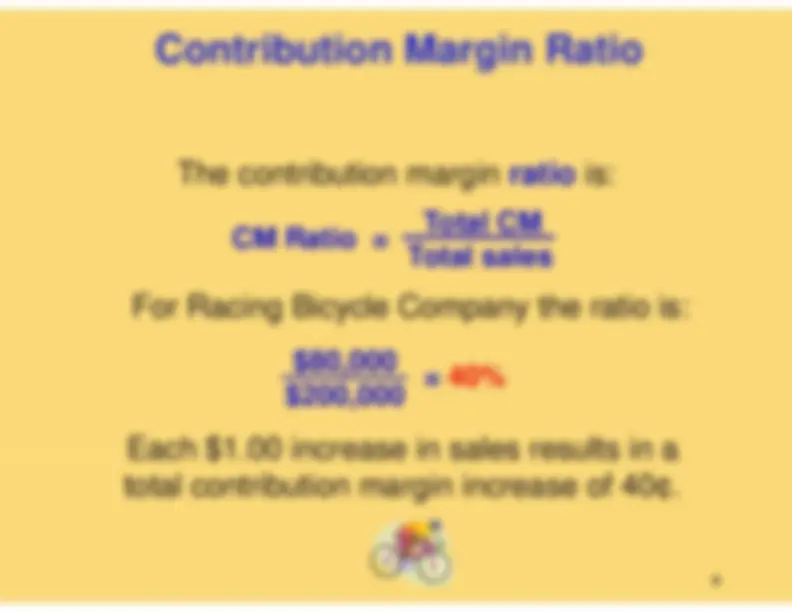

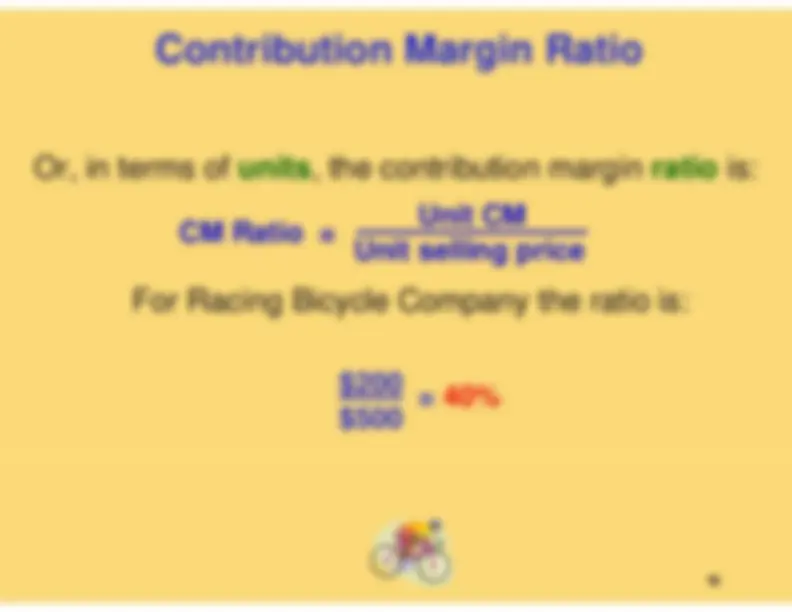

r, in terms of

units

, the contribution margin

ratio

is:

Unit CM

CM Ratio = For Racing Bicycle Company the ratio is:

Unit selling price

CM Ratio = For

Racing Bicycle Company the ratio is:

$200$200 $

= 40%

10

400 Bikes

500 Bikes

Sales

200, $^

250, $

Less: variable expenses

120,

150,

Contribution margin

80,

100,

L^

fi^

d^

80 000

80 000

Less: fixed expenses

80,

80,

Net operating income

$^

20, $

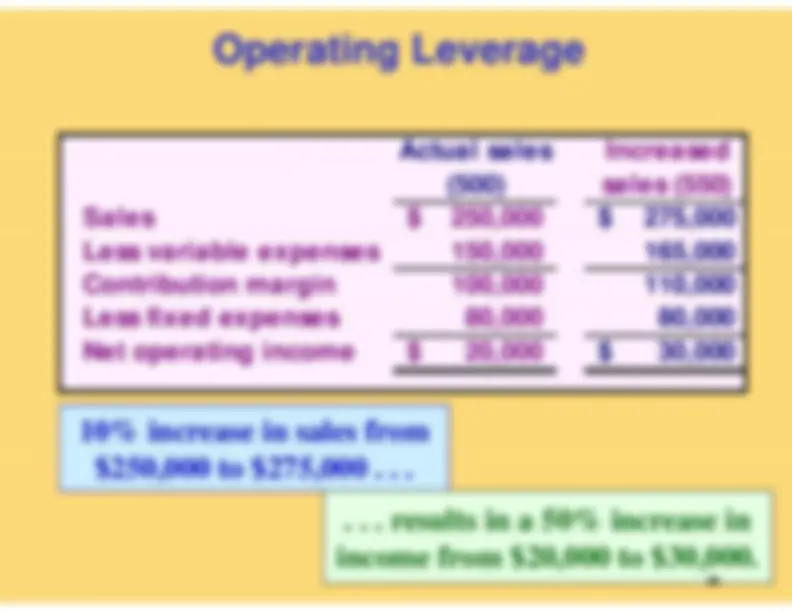

A $50,000 increase in sales revenueA $50,000 increase in sales revenueresults in a $20 000 increase in CMresults in a $20 000 increase in CMresults in a $20,000 increase in CM.results in a $20,000 increase in CM.

($50,000($50,000 ×

× 40% = $20,000)

40% = $20,000)

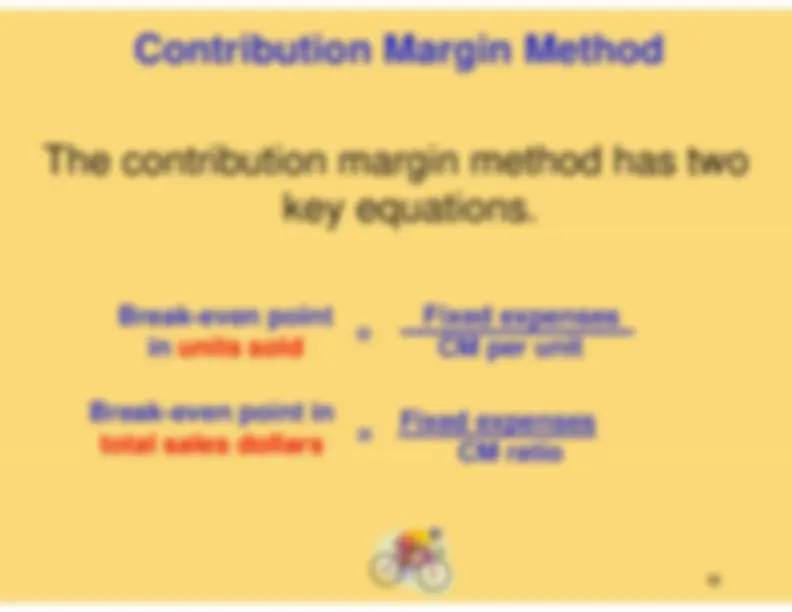

Fi

d

B

k^

i^

Fi

xed expensesCM per unit

=

Break-even point

in units sold

Fixed expenses

CM ratio

=

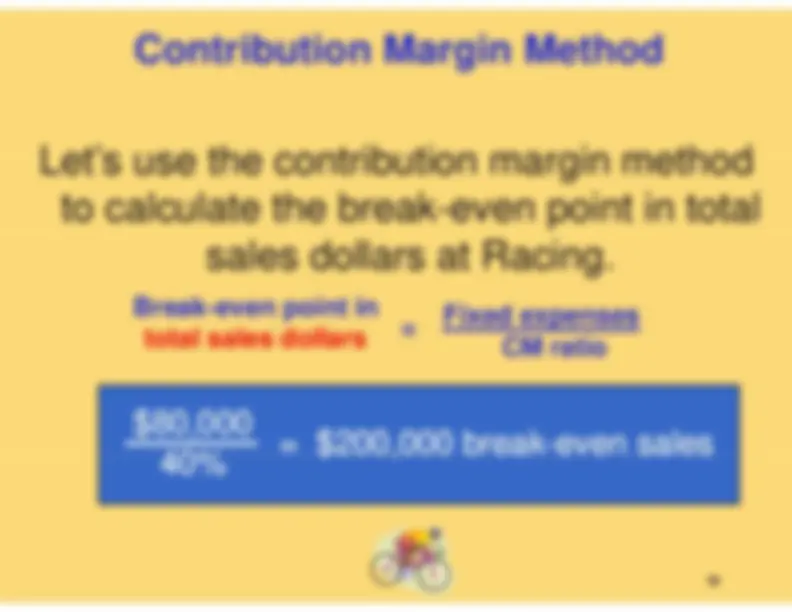

Break-even point intotal sales dollars

CM ratio

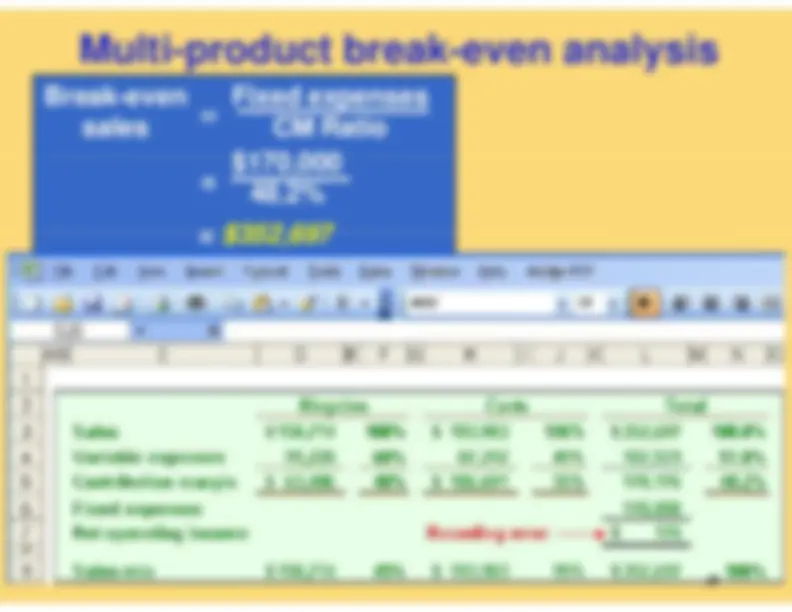

Fi

d

Break

even point in

Fi

xed expenses

CM ratio

=

The Contribution Margin Approach The contribution margin method can beThe

contribution margin method can be

used to determine that 900 bikes must be

f^

f $100 000

sold to earn the target profit of $100,000.

Fi

d^

+^

T^

t^

fit

U^

it^

l^

t^

tt i

Fi

xed expenses + Target profit

CM per unit

=

Unit sales to attain the target profit$80,000 + $100,

$200/bik

=

900 bikes

$200/bike

900

bikes

16

Th

i^

f^

f t

i^

th

f

Th

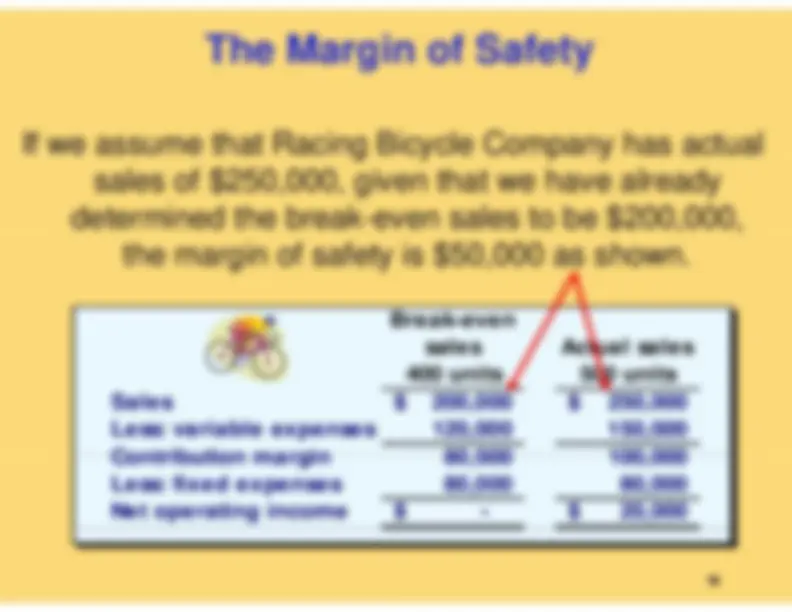

e margin of safety is the excess ofbudgeted (or actual) sales over the

break-even volume of sales.

i^

f^

f t

T t l

l^

k^

l

argin of safety = Total sales - Break-even sales^ Let’s look at Racing Bicycle Company and

determine the margin of safety.

g

y

17

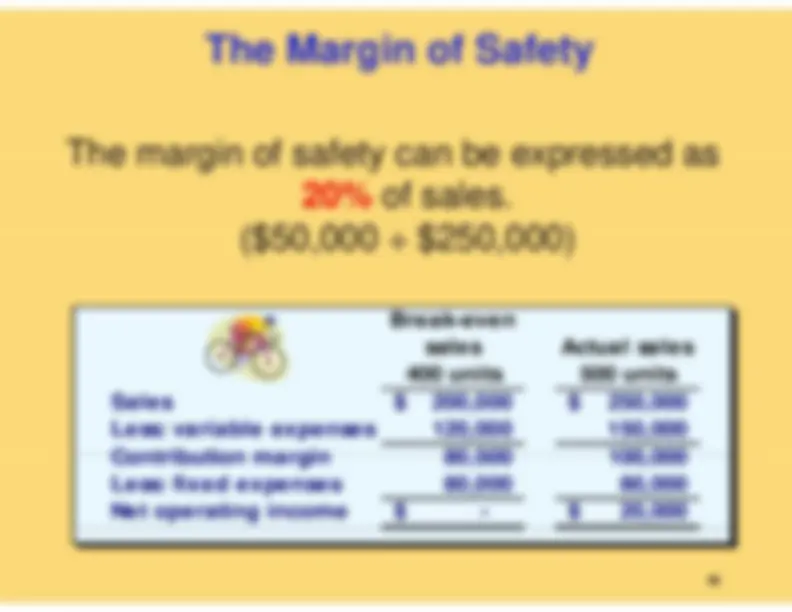

The margin of safety can be expressed asThe

margin of safety can be expressed as

20%

of sales.

($50 000 ÷ $250 000)($50,000 ÷ $250,000)

Break-even

sales 400 units

Actual sales

500 units

400 units

500 units

Sales

200, $^

250, $

Less: variable expenses

120,

150,

Contribution margin

80 000

100 000

Contribution margin

80,

100,

Less: fixed expenses

80,

80,

Net operating income

$^

20, $

The margin of safety can be expressed inThe

margin of safety can be expressed in terms of the number of units sold. The margin of safety at Racing is $50 000 andmargin of safety at Racing is $50,000, and

each bike sells for $500.