Introduction Extrapolation Forecasting Causal Forecasting Reference

Demand Forecasting

Siqian Shen1

1Dept. of Industrial and Systems Engineering

University of Florida

Fall 2009

1/ 46

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An overview of extrapolation and causal forecasting methods, including moving-average and exponential smoothing techniques, as well as simple linear regression analysis. The document also covers the concepts of trend and seasonality in demand forecasting and discusses the importance of forecasting accuracy.

Typology: Study notes

1 / 46

This page cannot be seen from the preview

Don't miss anything!

Siqian Shen^1

(^1) Dept. of Industrial and Systems Engineering University of Florida

Fall 2009

(^1) Introduction

(^2) Extrapolation Forecasting Moving-Average Forecast Methods → “Random" Simple Exponential Smoothing → “Random" Holt’s Method: Exponential Smoothing → “Linear Trend" Winter’s Method: Exponential Smoothing → “Seasonality" Forecasting Accuracy

(^3) Causal Forecasting Simple Linear Regression The Real World Can Be Much More Complicated...

(^4) Reference

Natural variation

Competitor

Customer preference

Changes in related goods

It takes time to source

It takes time to produce

It takes time to deliver

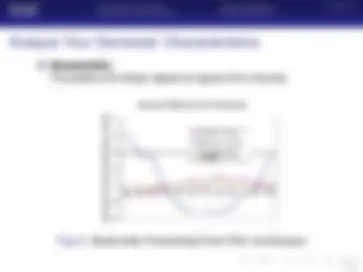

Trend : A time series that follows a particular pattern of function.

Figure: Trend Forecasting Chart (Ref: techcrunch.com)

Seasonality : The peaks and valleys repeat at regular time intervals.

Figure: Seasonality Forecasting Chart (Ref: eia.doe.gov)

Moving-Average Forecast Methods → “Random"

(^1) Introduction

(^2) Extrapolation Forecasting Moving-Average Forecast Methods → “Random" Simple Exponential Smoothing → “Random" Holt’s Method: Exponential Smoothing → “Linear Trend" Winter’s Method: Exponential Smoothing → “Seasonality" Forecasting Accuracy

(^3) Causal Forecasting Simple Linear Regression The Real World Can Be Much More Complicated...

(^4) Reference

Moving-Average Forecast Methods → “Random"

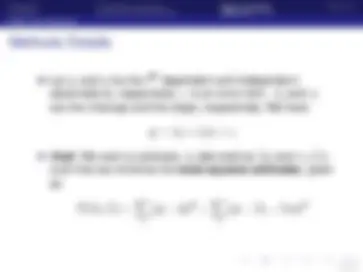

xt : observed data at time period t, t = 1 , 2 ,...

ft,k : forecast for time period t + k after observations of x 1 ,... , xt. In this course, we only consider ft, 1 , i.e., we use observations from time 1 to t to predict period t + 1 outcome.

ft, 1 =

∑t i=t−N+ 1 xi^ /N,^ ∀t^ ≥^ N where N is a given parameter, i.e., how many periods a decision maker thinks are enough to be looked back to predict the value of next period?

Simple Exponential Smoothing → “Random"

(^1) Introduction

(^2) Extrapolation Forecasting Moving-Average Forecast Methods → “Random" Simple Exponential Smoothing → “Random" Holt’s Method: Exponential Smoothing → “Linear Trend" Winter’s Method: Exponential Smoothing → “Seasonality" Forecasting Accuracy

(^3) Causal Forecasting Simple Linear Regression The Real World Can Be Much More Complicated...

(^4) Reference

Simple Exponential Smoothing → “Random"

Generally performs better than the Moving-average when forecasting random data.

Let At = forecast at the end of time period t, i.e., At = ft,k for some value setting of k (we assume k = 1 in this class.)

Given α as a smoothing constant , At = αxt + ( 1 − α)At− 1

Recall that et = xt − ft− 1 , 1 = xt − At− 1 At = At− 1 + α(xt − At− 1 ) = At− 1 + αet ⇒ we see et as an adjustment, which modifies our previous forecast At− 1.

Simple Exponential Smoothing → “Random"

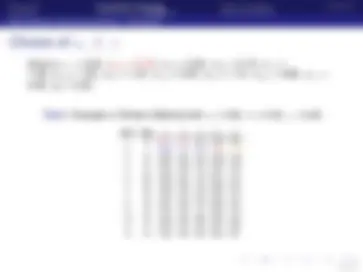

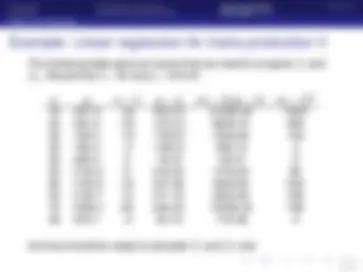

Table: Example 2: Exponential Smoothing with α = 0 .1 (Ref: [1]) Month Sales At− 1 At et 1 30 32 31.8 -2. 2 32 31.8 31.82 0. 3 30 31.82 31.64 -1. 4 39 31.64 32.37 7. 5 33 32.37 32.44 0. 6 34 32.44 32.60 1.

MAD= |−^2 |+|^0.^2 |+|−^1.^82 |+ 6 | 7.^36 |+|^0.^63 |+|^1.^56 |= 2. 26 We can change the value of α and compare the resulting corresponding MADs ⇒ The best value of α appears between 0.2 and 0.3.

Holt’s Method: Exponential Smoothing → “Linear Trend"

(^1) Introduction

(^2) Extrapolation Forecasting Moving-Average Forecast Methods → “Random" Simple Exponential Smoothing → “Random" Holt’s Method: Exponential Smoothing → “Linear Trend" Winter’s Method: Exponential Smoothing → “Seasonality" Forecasting Accuracy

(^3) Causal Forecasting Simple Linear Regression The Real World Can Be Much More Complicated...

(^4) Reference

Holt’s Method: Exponential Smoothing → “Linear Trend"

Let Lt and Tt represent estimates of base level and increase/decrease per-period at the end of time period t, respectively. Given smoothing constants α and β ∈ [ 0 , 1 ]

Lt = αxt + ( 1 − α)(Lt− 1 + Tt− 1 ) (1) Tt = β(Lt − Lt− 1 ) + ( 1 − β)Tt− 1 (2)

To obtain an estimation for time period t + k at the end of period t, simply use

ft,k = Lt + kTt

What is the intuition behind equations (1) and (2)?

Holt’s Method: Exponential Smoothing → “Linear Trend"

Regarding the example 3 in next slide, assume that we are given all x and L 1 , T 1 , First, given L 1 = 37. 71 , T 1 = 2 .83, we know that our prediction at the end of the first period will be f 1 , 1 = 37. 71 + 2. 83 = 40 .54 (colored in red) Since the actual sale in period t = 2 is x = 47, the resulting error is e 2 = x 2 − f 1 , 1 = 47 − 40. 54 = 6 .46 (colored in orange) Now in the end of period t = 2, what should be our predictions of L 2 and T 2? Recall holt’s method, L 2 = αx 2 + ( 1 − α)(L 1 + T 1 ) = 0. 30 ( 47 ) + 0. 70 ( 37. 71 + 2. 83 ) = 42. 48 (colored in blue) T 2 = β(L 2 − L 1 ) + ( 1 − β)T 1 = 0. 10 ( 42. 48 − 37. 71 ) + 0. 90 ( 2. 83 ) = 3. 02 (colored in blue)