Download Developing and Implementing a Water Conservation Plan and more Exercises Accounting in PDF only on Docsity!

DEVELOPING AND IMPLEMENTING

A WATER CONSERVATION PLAN

Guidance For

Maryland Public Water Systems

On Best Management Practices

For Improving Water Conservation

And Water Use Efficiency

Maryland Department of the Environment

Water Supply Program

1800 Washington Boulevard, Suite 450 Baltimore, Maryland 21230

TABLE OF CONTENTS

BACKGROUND ..................................................................................................................

DEVELOPING A WATER CONSERVATION PLAN ...................................................

REFERENCES.....................................................................................................................

APPENDICES

APPENDIX A-1 MDE Water Audit Guidance

APPENDIX A-2 MDE Water Audit Instructions and Worksheet

APPENDIX A-3 MDE Annual Water Audit Summary

APPENDIX B –1 EPA Water Accounting and Loss Control

APPENDIX B-2 EPA Preliminary Water Demand Forecast Worksheet

APPENDIX B-3 EPA Cost of Supply-Side Facilities Worksheet

APPENDIX B-4 EPA Analysis of Each Conservation Measure Worksheet

APPENDIX C Water Conservation Public Education

APPENDIX D Case Studies

DEVELOPING A WATER CONSERVATION PLAN

Water conservation plans should address conservation on the supply side as well as on the demand side. Conservation plans for the supply side (i.e., leak detection and repairs, metering, etc.) may require additional financial resources, however there is some potential for reduction in operating costs and recovery of lost revenues. Conservation plans for the demand side (i.e. reductions in consumer usage) may result in lost revenues, however, a well-designed pricing program can offset potential losses in revenue. Other benefits associated with implementing a conservation plan (which include eliminating, downsizing, or postponing the need for capital projects, improving the utilization and extending the life of existing facilities, lowering variable operating costs, avoiding new source development costs, improving drought or emergency preparedness, educating customers about the value of water, improving reliability and margins of safe and dependable yields, and protecting and preserving environmental resources) may also help to balance losses in revenue.

Water conservation plans will vary based on many factors including the size of the water utility. Large water systems serving more than 10,000 persons will require a more complex and detailed water conservation plan than smaller water systems. The U.S. Environmental Protection Agency published Water Conservation Plan Guidelines in 1998. This helpful reference can be found at the following Internet address: http://www.epa.gov/owm;/water-efficiency/wecongid.htm. Hard copies of the document can be obtained by contacting the Water Resource Center by phone at 202-260-7786 or by email at [email protected] and requesting EPA document: EPA-832-D-98-001.

MDE endorses a format similar to that recommended in EPA’s Guidelines, which offers instruction on completing conservation plans of varying complexity: Basic, Intermediate, and Advanced. Maryland water systems should use either the Intermediate or Advanced Guidelines as a reference when writing their own conservation plans. The Advanced guidelines may be more appropriate for systems serving more than 10,000 persons, or for systems likely to experience water supply problems (i.e. where water production is close to capacity, where significant growth is expected, or where dry weather conditions result in water supply deficiencies.) Worksheets provided in Appendix A of this document were obtained from the Intermediate Guidelines. Developing a water conservation plan involves the following steps:

I. Establish the goals of the water conservation plan. The first step in developing a water conservation plan is for the utility to establish a list of conservation planning goals. Measurable goals, such as a water use reduction goal (in terms of percentage of baseline water usage), are useful for later evaluation of the conservation plan. Other common goals for water utilities include postponing or eliminating the need for capital projects or new source development, and improving drought preparedness. Utilities should consider involving their communities in the goal development and implementation process. In addition to helping to develop goals, participants can act as a focus group and serve as a gauge for the public’s reaction to possible conservation measures.

II. Conduct a water system audit. Completing an initial water system audit is an integral part of developing a water conservation plan because it will serve as a baseline measure of water use. Subsequent annual audits can track progress towards meeting established goals. Most water systems already have the basic information necessary to complete a water audit. MDE guidance instructions for

2

completing a Water System Audit and a template for reporting results can be found in Appendix A- and A-2 or at the following web address: http://www.mde.state.md.us/Programs/WaterPrograms/Water_Conservation/Water_Auditing/index.asp

A water system audit collects data on accounted and unaccounted water. Unaccounted water includes water that is metered but not billed and water that is not metered. Unmetered water consists of authorized uses (fire protection, flushing mains, etc.), as well as unauthorized uses (losses due to accounting errors, thefts, inaccurate meters, and leaks). Utilities should strive to minimize the quantity of unmetered, unauthorized water use. A water system audit should also provide information about the quantity and type of population served, geographic considerations, number of total connections and metered connections, and the average and peak demands. EPA’s worksheet “Water Accounting and Loss Control” is available in Appendix B-1.

A discussion summarizing conditions that might affect the water system and conservation planning should also be provided. Issues such as anticipated population growth, large quantities of unaccounted water, and major planned improvements should be included in this discussion.

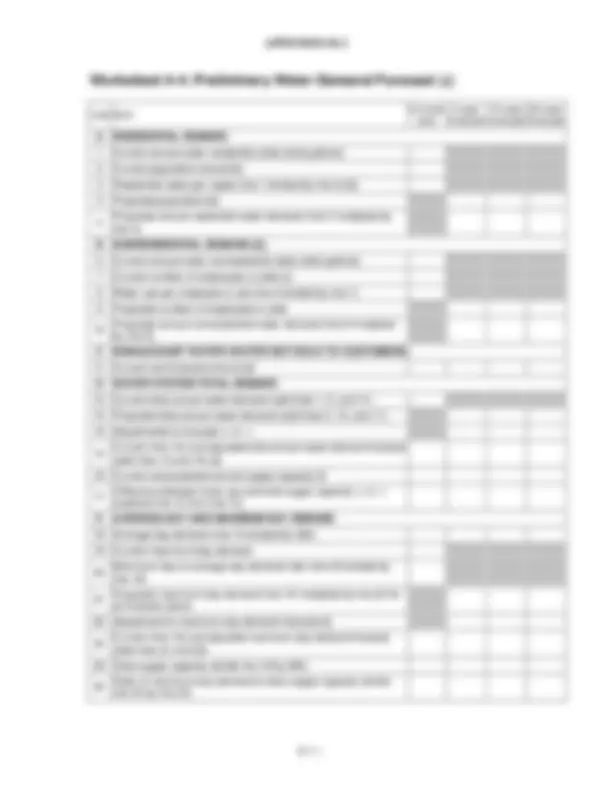

III. Prepare a demand forecast. A demand forecast estimates water use requirements into the future. Demand forecasts can range from a simple projection based on population growth to complex models that contain several variables. The size of the utility will dictate the complexity of the projection. It is suggested that forecasts be prepared for 5, 10, and 20 years into the future. If a water system has prepared a demand forecast within the past two years, calculating a new demand forecast is probably not necessary. It is also recommended that forecasts be made for each water end user group (residential, commercial, etc.) as opposed to the water system as a whole, unless the water system serves a population of fewer than 10,000. The forecast should take into account any known, planned, or measurable changes that will have an effect on demand, with the exception of additional conservation measures considered in this plan. Uncertainties in the demand forecast should be highlighted and discussed. EPA has published a “Preliminary Water Demand Forecast” that can be used as a guide to calculating a water demand forecast. A copy of this publication is included as Appendix B-2.

When the growth in projected demand is large, it may be useful to prepare an estimate of supply costs necessary to meet increased demand. In some cases increased demand will require improvements or additions to the water system. Anticipated supply costs are needed to compare the costs of supply-side and demand-side conservation measures. Appendix B-3 contains a worksheet from EPA’s guidance designed to help calculate the costs of any improvements and/or additions.

IV. Identify and select potential water conservation measures. MDE has categorized water conservation measures into Required Elements and Recommended Elements. Required elements should be included for all water utilities, while the recommended elements may be evaluated for inclusion as appropriate. An integral part of evaluating these various conservation measures is a cost analysis. For each conservation measure the utility should estimate implementation costs and projected water savings. A cost analysis worksheet entitled, “Analysis of Each Conservation Measure or Group of Measures” from EPA’s guidance is included in Appendix B-4.

A. Required Elements. These elements should be included in all water conservation plans for Maryland public water systems.

3

- Provide understandable and informative water bills to customers. The water bill should contain consumer usage in terms of gallons per day. When customers are aware of their daily water use, they are more likely to conserve.

- Provide educational information through water bill inserts or other means. For water systems where residential water use is greater than 100 gallons per capita per day, this should occur at least once a year.

- Additional recommendations for public education are described in Appendix C.

B. Recommended Elements

1. Develop outreach for specific users. Utilities typically serve three types of customers: residential, municipal, and industrial/commercial customers. Each of the outreach efforts described below is geared to one or more user types, which are identified in parenthesis. Recommendations:

- Conduct Water Use Audits for Consumers ( Residential, Industrial/Commercial, and Municipal ). Water use audits can provide water systems and their customers with information about how water is used and help identify potential conservation strategies. Audits can be particularly effective when targeted towards large volume users, or other selective end use customers (e.g., single family homes with large yards, parks or other large landscapes, etc.).

- Offer fixture retrofits and replacements ( Residential, Industrial/Commercial, and Municipal ). Retrofitting involves making an improvement to an existing fixture, as opposed to replacing an existing fixture. Retrofit programs usually target plumbing fixtures and can be made available to customers free or at cost. Retrofit kits can be distributed directly, through community organizations, in conjunction with water audits, or to other targeted customer groups.

- Offer rebates and incentives ( Residential, Industrial/Commercial ). Options include having utilities install water-efficient fixtures by providing them at no cost, giving rebates for consumer purchased fixtures, or arranging for suppliers to provide fixtures at a reduced price.

- Promote water reuse and recycling ( Industrial/Commercial ). Some industries can reduce water demand by reusing water in the manufacturing process. In some cases, using gray water or treated wastewater for nonpotable water uses may be appropriate. Reuse and recycling can also be encouraged for large-volume irrigation applications. Water reuse applications must meet applicable State and federal wastewater disposal regulations.

- Encourage landscape efficiency ( Municipal, Industrial/Commercial ). Utilities can promote water conservation principles into the planning, development, and management of new landscape projects such as public parks, building grounds, and golf courses. Existing projects can also be renovated to incorporate water-conserving practices. Water utilities can also work with commercial and industrial customers to plan and renovate their landscapes.

5

2. Pressure Management. Reducing excessive pressures in the distribution system can save water by reducing stresses that could result in leakage, decreasing quantities of water that are currently leaking, and reducing the amount of flow through fixtures. Recommendations: - Assess the need for pressure management in residential areas with pressures greater than 80 pounds per square inch. - Install pressure reducing valves in street mains and in buildings where appropriate. 3. Water-Use Regulations. Water utilities may wish to consider having regulations in place that manage water use during normal times as well as during times of drought or other water supply emergencies. Recommendations:

- Institute restrictions or bans on certain non-essential water uses.

- Develop standards for new developments with respect to landscaping, drainage, and irrigation practices.

- Develop a fine or penalty system for frequent misuse of water during drought emergencies.

V. Develop and present implementation strategy.

The water utility should develop a schedule and timetable for implementing the water conservation strategies. Implementation actions should include a timetable for securing budgetary resources, hiring staff, procurement of materials, acquisition of any necessary permits, and activity milestones.

6

APPENDIX A-

A-1-

MDE Water Audit Guidance

INTRODUCTION

What is a water audit?

A water audit determines the amount of water lost from a distribution system (due to leakage, storage overflow, meter malfunctions, and theft) and the cost of this loss to the utility. Water audits balance the amount produced with the amount billed and account for the remaining water (loss). Comprehensive audits can give the utility a detailed profile of the distribution system and water users, allowing easier management of resources and improved reliability. It is an important step towards water conservation and, linked with a leak detection plan, can save the utility a significant amount of money and time.

Elements of the audit include

- Record of the amount of water produced

- Record of the amount delivered to metered users

- Record of the amount delivered to unmetered users

- Record of amount of water loss (balance of water, including leaks)

- Measures to address water loss (leaks and other unaccounted water)

What is Water Loss?

There are two types of loss: real and apparent losses. Real loss includes water lost through leakage of distribution systems, service connections, and storage tanks (including overflow). Apparent loss includes meter and record inaccuracies and unauthorized water uses such as theft and unauthorized connections. Authorized unmetered uses can be considered a special type of lost water, and they can also represent lost revenue so should be estimated carefully.

What are the benefits of a water audit?

Benefits of an audit include improved knowledge and documentation of the distribution system including problem and risk areas. By providing a better understanding of what is happening to the water after it leaves the treatment plant, the audit can be a valuable tool to manage resources.

According to the American Water Works Association, water audit programs lead to reduced water losses, financial improvement, increased knowledge of the distribution system, more efficient use of existing supplies, increased safety for public health and property, improved public relations, reduced legal liability, and reduced disruption to customers.

How do I perform a water audit?

This document includes a model water audit worksheet and instructions based on one developed by the Texas Water Development Board. This worksheet is simple, but it is sufficient to account for water usage and quantify lost water. A water audit can be completed in one day if meter-reading records are easily available and significant adjustments to the records are not necessary. The audit should use existing records to the extent possible to produce the most accurate results.

Audits are completed by calculating the difference between the amount of water produced and the amount sold (metered sales) then addressing the difference. Metered sales are compiled and remaining difference between produced water is lost. An audit records the amount of water produced, amount delivered to metered users, amount delivered to unmetered users, and water loss, along with likely causes for the unaccounted water. Then the results are analyzed and estimates are made for recoverable leakage.

APPENDIX A-1 (cont.)

A-1-

Corrective measures should be evaluated and any needed distribution system improvements should be described. Cost benefit analyses should be performed and an effective course of action implemented.

Once the efficiency of the water system is evaluated, the system should take necessary steps to reduce the amount of recoverable water loss. Effective water audits usually result in leak detection programs, which identify and correct problems in the distribution system. A leak detection programs is an effective way to minimize leakage and to fix small leaks before they become major problems. A comprehensive follow up audit might be necessary to determine the accuracy of meters, track unmetered use, and locate and repair leaks.

Recommended Strategy

A preliminary audit should be undertaken to determine the amount of water loss, then followed up with congruous measures as determined by the findings of the audit. If water loss is significant, a more detailed study should be undertaken. If a detailed study shows water loss is significant, measures should be taken to reduce the loss.

PLANNING THE WATER AUDIT

Considerations

Water audits can be designed by reviewing the system records and staff expertise and using these resources to develop and complete effective worksheets. Distribution system characteristics vary, so each utility will have different challenges in performing the water audit. Each system will need to decide how it can perform the audit accurately with the least cost. A worksheet should be developed, and a study period set.

Set Study Period

A study period should be set to allow an evaluation of the complete water system. One year is recommended because it includes all seasons and gives enough time to eliminate the effect of meter reading lag. Shorter periods might not give a complete picture of the water system, and longer periods can be difficult to manage.

Develop a worksheet

MDE has attached a spreadsheet that utilities are encouraged to use; however, utilities may develop their own worksheet. The worksheet, similar to an accounting spreadsheet, should make the computations clear and simple and allow the utility to balance water produced with water used. As well as balancing water in and out of the distribution system, the worksheet should list and account for various water usages.

Water is the commodity and assets (gallons water produced) will be balanced with liabilities (gallons sold) to determine the loss of commodity. If the worksheet is properly designed, a preliminary audit should be able to be completed in a day if using existing meter reading data.

Worksheets can vary in detail and will determine how well the distribution system is described. A more detailed worksheet will provide better understanding of the water usage and could be a useful tool for the water utility.

APPENDIX A-1 (cont.)

A-1-

eliminating unmetered accounts. Cost benefit analyses should be conducted to choose the right option. If future annual audits continue to show unmeasured water greater than 10%, the plan for reducing water losses should be updated and re-submitted.

Benefits of recovering leakage

Benefits the utility should consider are the lost commodity, risk of allowing leaks, and the liability of not addressing leaks. Lost commodity is easy to quantify, as it should be the bottom line of the audit worksheet. Risks include letting small problems continue that might cause major outages and emergency repairs. Liabilities of leakage, or inaction, include capacity waste, water theft (or dead meters), road or foundation collapse, and flooded basements. Leaks also pose a serious cross connection threat, as leaks can be a direct conduit into the distribution system whenever pressure fluctuates.

Cost of recovering leakage

Costs include the personnel and the equipment required to make improvements. Repair costs should not be included because these need to be done eventually.

Long-term goals

Long-term follow up should include updating the audit, reducing loss and checking meters. After the first audit, areas where data is lacking should be identified and addressed. Subsequent audits should provide greater accuracy and reduction of water losses.

More Information

Sources of information on Water Audits include:

AWWA manual M36 Water Audits and Leak Detection

International Water Association Losses from Water Supply Systems: Standard Terminology and Recommended Performance Measures

APPENDIX A-

Water Audit Instructions and Worksheet

Note: Units should be reported in millions of gallons for larger systems. For small water systems, reporting in thousands of gallons may be more appropriate.

Line 1 – Total Water Supply to Distribution System

This is the total volume of all water supplied to the system as measured by the master meter(s) and interconnects with other sources of supply. If water is purchased from an interconnected system, please include detailed quantities in the spreadsheet.

Line 2 – Adjustments to Water Delivery

Adjustments may be an increase or a decrease in storage capacity from the beginning to the end of the study period, or adjustments for known broken, or inaccurate master meters.

Line 3 – Net Water Produced

This is the net adjusted water produced and/or measured through the master meters, from plants and interconnections, after adjustments.

Line 4 – Gallons of Metered Water Sold

This lists the total amount of water that is sold through meters in the system. This includes residential, commercial, industrial, institutional, and other metered sales such as standpipes for water haulers. It is important to evaluate when the meters are read so that the readings can be adjusted to reflect the time it takes to actually read the meters. To assure that the production/purchase records are comparable to the customers’ meter readings, consumption during the meter-reading period must be adjusted to match the production/purchase period.

Line 5 – Billed Unmetered Sales

These are sales to customers that are not metered. They include connections that are not metered and any bulk sales (e.g. through hydrants). These amounts should be detailed in the spreadsheet.

Line 6 – Unbilled Authorized Consumption

Provided on the chart is a general listing of potential uses that are frequently not metered, however, if these facilities are metered they should be included in Line 4. You may use this list or make your own estimates of unmetered users and accounts. Please include detail amounts with documentation in the spreadsheet.

Line 7 – Apparent Water Losses

These consist of unauthorized consumption and meter inaccuracies. Meter inaccuracy includes production meters and customer meters. These amounts should be documented in the spreadsheet.

A-2-

Appendix A-2 (cont.)

JAN

FEB

MAR

APR

MAY

JUN

JUL

AUG

SEP

OCT

NOV

DEC

TOTAL

WATER DELIVEREDWATER USED

ResidentialCommercialIndustrialInstitutionalOther

Total

- Billed Unmetered Sales

Water Main FlushingSewer/Storm Drain FlushingParks/Playgrounds/Swimming PoolsGolf CoursesCemeteriesRoad MediansSchoolsTraining/Fire FightingConstructionStorage Tank DrainageSewer Plant Uses

Total

Water Meter MalfunctionTheftOther

Total

8.^

Real W ater Losses

LeaksStorage OverflowOther

Total

Source: Ada

pted from the Texas Water Develo

pment Board

- Worksheet is also available as an Excel s

preadsheet WATER AUDIT WORKSHEET FOR TREATED WATER*

(units should be reported in millions of gallons)

- Total W ater Supply to Distribution System2. Adjustments to W ater Delivery3. Net W ater Produced4. Gallons of Metered W ater Sold6.^ 7. Apparent W ater Losses 9. Net Lost or Unmeasured W ater10. Percentage of Lost or Unmeasured W ater

Unbilled Authorized Consumption

A-2-

APPENDIX A-

ANNUAL WATER AUDIT SUMMARY

SYSTEM INFORMATION

SYSTEM NAME:

SYSTEM ID: ________________________

WATER AUDIT INFORMATION

A. Total Water Produced Annually (Line 3*):

B. Total Lost or Unmeasured Water (Line 3* minus the sum of Line 4, Line 5, and Line 6) or (Line 7 plus Line 8*):

C. Percentage of Water Lost or Unmeasured to Total Water Produced (Line 9* divided by Line 3*): Note: If greater than 10 percent, a plan should be prepared outlining steps to identify and reduce water system losses.

WATER AUDITOR

Name of person completing this report:

Signature: Date:

Phone Number: E-mail Address:

Please mail this summary page, the worksheet, and any other supporting documents that you may want to submit to:

Maryland Department of the Environment Water Supply Program 1800 Washington Boulevard, Ste. 450 Baltimore, Maryland 21230

For questions, please call (410) 537-

- Line numbers refer to table in Appendix A-

A-3-

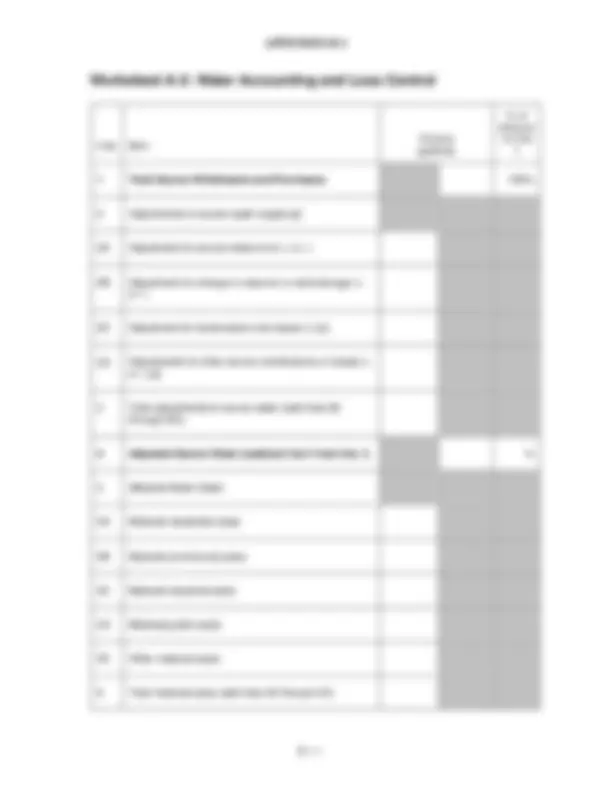

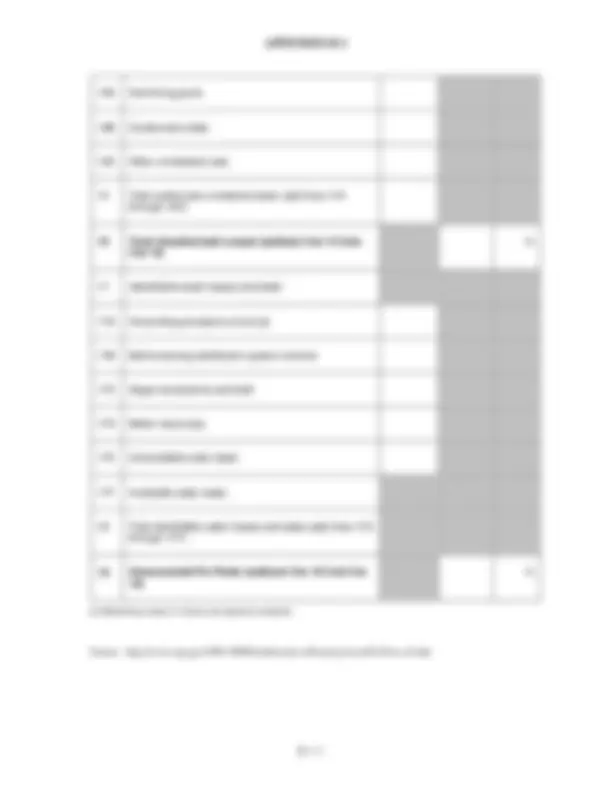

APPENDIX B-

7 Adjustment for meter reading lag time (+ or -)

8 Adjustment for meter errors (+ or -) [a]

9 Adjusted total meter sales (add lines 6 through 8)

10 Nonaccount Water (subtract line 9 from line 4) %

11 Metered and accounted-for but not billed

11A Public-use water metered but not billed

11B Other water metered but not billed

12 Authorized unmetered water: operation and maintenance

12A Main flushing

12B Process water at treatment plant

12C Water quality and other testing

13 Authorized unmetered water: public use

13A Storm drain flushing

13B Sewer cleaning

13C Street cleaning

13D Landscaping in large public areas

13E Firefighting, training, and related maintenance

14 Other authorized unmetered use

B-1-

APPENDIX B-

14A Swimming pools

14B Construction sites

14C Other unmetered uses

15 Total authorized unmetered water (add lines 11A through 14C)

16 Total Unauthorized Losses (subtract line 15 from line 10)

%

17 Identifiable water losses and leaks

17A Accounting procedure errors [a]

17B Malfunctioning distribution system controls

17C Illegal connections and theft

17D Meter inaccuracy

17E Unavoidable water leaks

17F Avoidable water leaks

18 Total identifiable water losses and leaks (add lines 17A through 17F)

19 Unaccounted-For Water (subtract line 18 from line 16)

%

[a] Methodology subject to industry and regulatory standards.

Source: http://www.epa.gov/OW-OWM.html/water-efficiency/wave0319/ws-a2.htm

B-1-