DIVIDEND POLICY

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

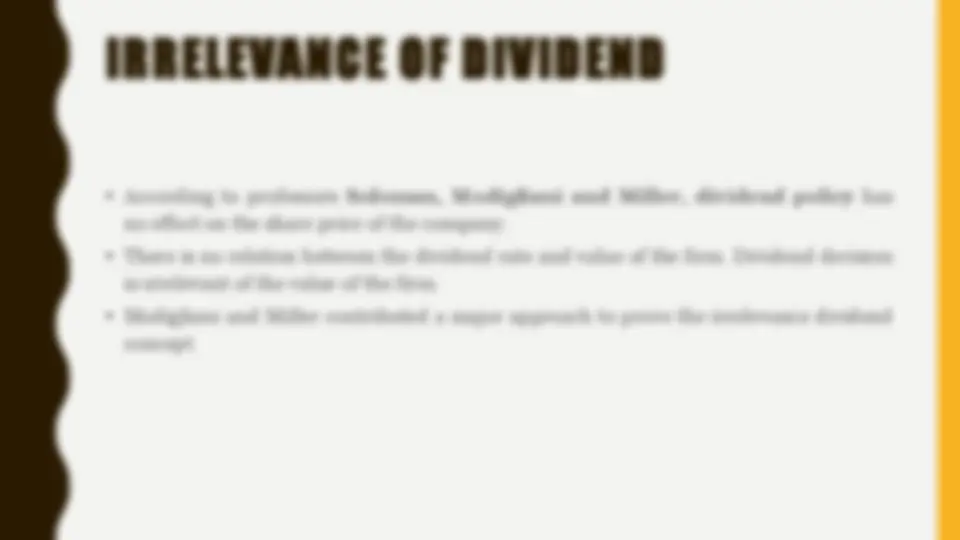

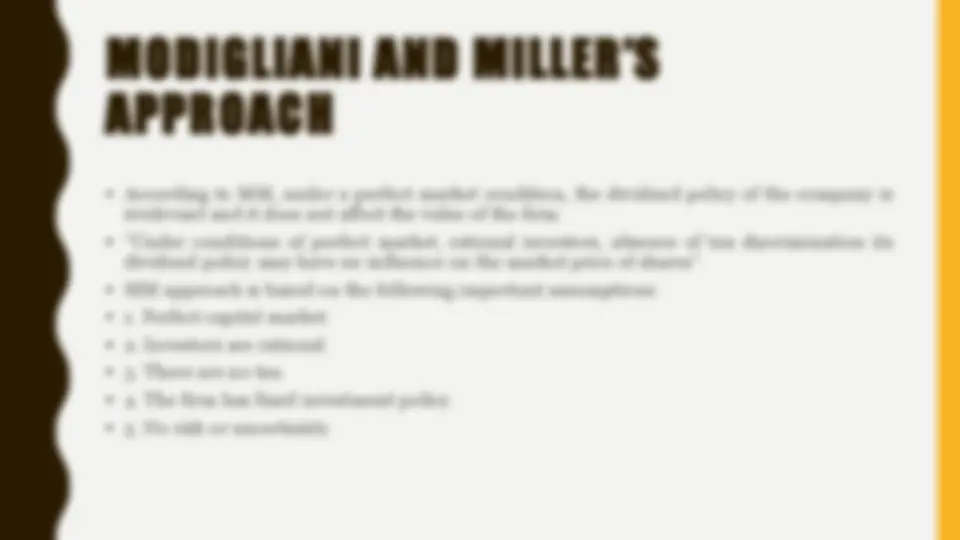

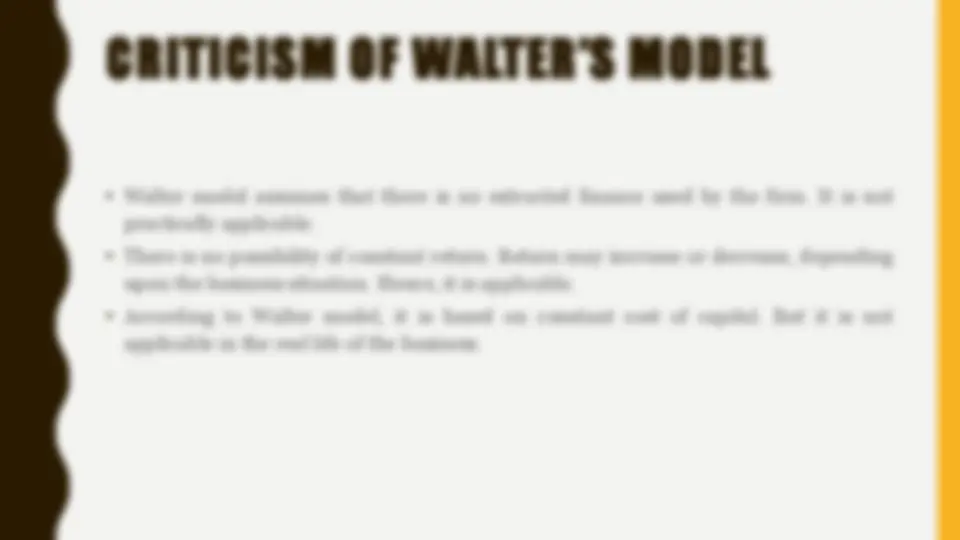

An overview of the Modigliani-Miller (MM) dividend irrelevance theory, which argues that under perfect market conditions, the dividend policy of a company has no effect on the value of the firm. the assumptions and approach of MM, as well as criticisms of their theory by Walter and Gordon.

Typology: Lecture notes

1 / 14

This page cannot be seen from the preview

Don't miss anything!