Download Double-Entry Bookkeeping: Journal Entries and Examples and more Study notes Financial Accounting in PDF only on Docsity!

📘 Double-Entry Bookkeeping – Notes with Journal Entries & Examples

- Introduction to Double-Entry Bookkeeping Double-entry bookkeeping is the system of recording transactions where every transaction affects at least two accounts: Debit (Dr) → What the business receives. Credit (Cr) → What the business gives. 👉 Golden Rule: “For every debit, there is an equal and opposite credit.”

- Rules of Debit and Credit Account Type Debit (Dr) Increases Credit (Cr) Increases Assets ✅ Increase ❌ Decrease Liabilities ❌ Decrease ✅ Increase Equity/Capital (^) ❌ Decrease ✅ Increase Revenue/Income ❌ Decrease ✅ Increase Expenses ✅ Increase ❌ Decrease

- Format of a Journal Entry Date Particulars Debit (Dr) Credit (Cr) yyyy-mm-dd Account to be debited xxx To Account to be credited xxx (Brief explanation)

- Examples with Journal Entries Example 1: Owner invests cash into business ($10,000) Cash (Asset) increases → Debit Capital (Equity) increases → Credit Date Particulars Debit (Dr) Credit (Cr) 2025 - 01 - 01 Cash A/c 10, To Capital A/c 10, (Owner invested cash) Example 2: Business purchases furniture for cash ($2,000) Furniture (Asset) increases → Debit Cash (Asset) decreases → Credit Date Particulars Debit (Dr) Credit (Cr) 2025 - 01 - 02 Furniture A/c 2, To Cash A/c 2, (Furniture purchased)

Example 5: Business buys inventory on credit ($3,000) Purchases (Expense) increases → Debit Accounts Payable (Liability) increases → Credit Date Particulars Debit (Dr) Credit (Cr) 2025 - 01 - 05 Purchases A/c 3, To Accounts Payable A/c 3, (Inventory bought on credit) Example 6: Business takes a bank loan ($5,000) Cash (Asset) increases → Debit Loan Payable (Liability) increases → Credit Date Particulars Debit (Dr) Credit (Cr) 2025 - 01 - 06 Cash A/c 5, To Bank Loan A/c 5, (Loan received)

Example 7: Paying salary to employees ($1,200) Salary Expense increases → Debit Cash decreases → Credit Date Particulars Debit (Dr) Credit (Cr) 2025 - 01 - 07 Salaries Expense A/c 1, To Cash A/c 1, (Salaries paid) Example 8: Business buys insurance ($600) Insurance Expense increases → Debit Cash decreases → Credit Date Particulars Debit (Dr) Credit (Cr) 2025 - 01 - 08 Insurance Expense A/c 600 To Cash A/c 600 (Insurance premium paid)

Example 11: Business receives cash from a debtor ($1,000) Cash (Asset) increases → Debit Accounts Receivable decreases → Credit Date Particulars Debit (Dr) Credit (Cr) 2025 - 01 - 11 Cash A/c 1, To Accounts Receivable A/c 1, (Received from debtor) Example 12: Business declares owner’s withdrawal ($700) Drawings (Equity reduction) increases → Debit Cash decreases → Credit Date Particulars Debit (Dr) Credit (Cr) 2025 - 01 - 12 Drawings A/c 700 To Cash A/c 700 (Owner withdrawal)

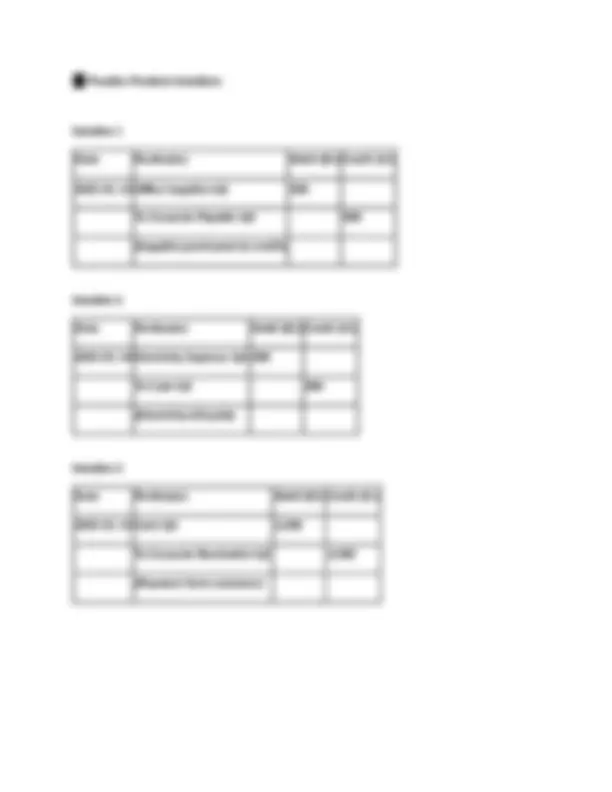

📘 Practice Problems – Double-Entry Bookkeeping Practice Problem 1 A business purchases office supplies worth $500 on credit. 👉 Record the journal entry. Practice Problem 2 The business pays the electricity bill of $300 in cash. 👉 Record the journal entry. Practice Problem 3 A customer pays the business $2,500 in cash for goods previously sold on credit. 👉 Record the journal entry.