Download Economics: Demand and Supply Analysis and more Transcriptions Economics Concepts for Engineers in PDF only on Docsity!

Economics for Engineers

Unit 1 Introduction to Economics - Definition Basic Economic Problems Resource Constraints and Welfare Maximization Microeconomics and Macroeconomics Production Possibility Curve Circular Flow of Economic Activities Basics of Demand, Supply, and Equilibrium: Demand Side and Supply Side of the Market Factors Affecting Demand and Supply Elasticity of Demand and Supply: Price, Income, and Cross-Price Elasticity Market Equilibrium Price Unit 2 Theory of Consumer Choice - Theory of Utility and Consumer's Equilibrium Indifference Curve Analysis Budget Constraints Consumer Equilibrium Demand Forecasting: Regression Technique Time-Series Forecasting Smoothing Techniques: Exponential Moving Averages (EMA) and Moving Averages (MA) Method Unit 3 Introduction to Cost Theory: Nature and Types of Costs What is Short Run Costs? What is Long Run Cost? Difference Between Short Run and Long Run Cost Types of Short Run Costs

**1. Short Run Total Cost (STC)

- Short Run Average Cost (SAC)

- Short Run Marginal Cost (SMC) Types of Long Run Costs

- Long Run Total Cost (LTC)

- Long Run Average Cost (LAC)**

**3. Long Run Marginal Cost (LMC) Long Run Total Cost Curve Short Run Total Cost Curve Relationship Between Long Run Cost and Short Run Cost Final Word Cost Functions: Short Run and Long Run Economies and Diseconomies of Scale Economies of Scale: Diseconomies of Scale: Market Structure

- Perfect Competition:

- Monopoly:

- Monopolistic Competition:

- Oligopoly:**

- Duopoly: Unit 4 National Income Accounting

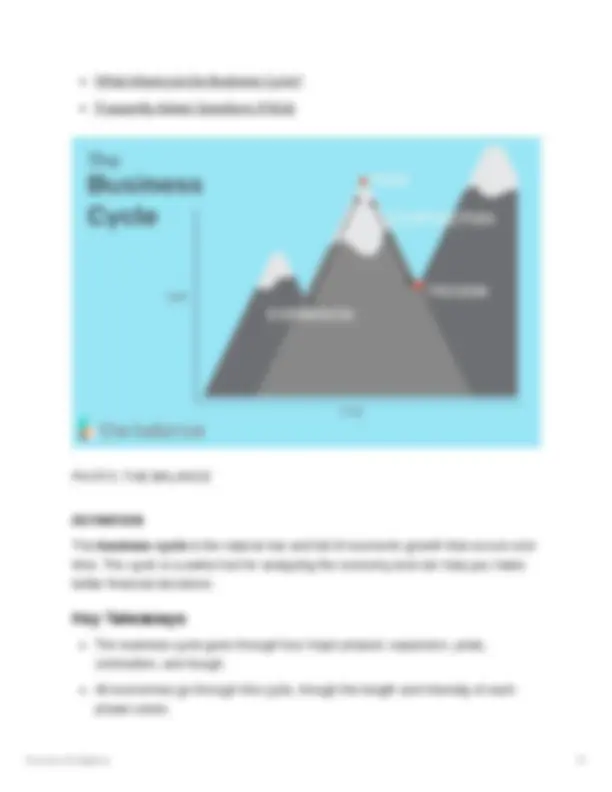

Overview of Macroeconomics What Is a Business Cycle? Understanding the Business Cycle Macro Economics Issues

Inflation Causes Consequences of Inflation: Monetary Policy: Fiscal Policy: Remedies: Key Takeaways How Does the Business Cycle Work? Note The Four Phases of the Business Cycle Expansion Note Peak Contraction

decisions, interact, and allocate resources efficiently.

- Macroeconomics: Macroeconomics, on the other hand, looks at the economy as a whole. It studies national and international economic issues, including economic growth, inflation, unemployment, and government policies that affect the entire economy.

Scope of Economics:

Economics has a broad scope and covers a wide range of topics, including but not limited to:

Demand and Supply: Analyzing how markets determine prices and quantities of goods and services based on consumer demand and producer supply. Production and Costs: Examining how businesses produce goods and services, including the factors of production, production functions, and cost structures. Market Structures: Evaluating different market structures like perfect competition, monopoly, oligopoly, and monopolistic competition and how they impact the behavior of firms. National Income and Business Cycles: Studying how a country's income is measured and how fluctuations in economic activity, known as business cycles, affect an economy.

Formulas and Equations:

While the introductory definition of economics doesn't involve specific formulas, you will encounter various mathematical and graphical tools in microeconomics and macroeconomics to analyze economic concepts and relationships. These may include equations for supply and demand, production functions, and economic indicators.

Examples:

An individual decides to spend their income on either buying a smartphone or a laptop. The opportunity cost is the value of the item they didn't choose.

A business must decide how many workers to hire. They will consider the marginal cost of hiring an additional worker and the additional output or revenue that worker will generate. A government implements a policy to reduce inflation. Macroeconomists will study the effects of this policy on the overall economy, including unemployment rates and GDP growth.

In summary, economics is the study of how individuals and societies make choices in the face of limited resources to meet their needs and wants. It is a diverse field with both microeconomic and macroeconomic components, and it provides valuable insights into decision-making, resource allocation, and the functioning of economies.

Basic Economic Problems

Introduction: Basic economic problems, also known as fundamental economic problems, are the central issues that all economic systems must address. These problems stem from the scarcity of resources relative to unlimited human wants and needs. Understanding and solving these problems is fundamental to the study of economics. The three primary basic economic problems are:

- What to Produce: This problem concerns the allocation of resources to the production of various goods and services. Every society must decide which goods and services to produce based on the preferences and needs of its population. The choice of what to produce is influenced by factors such as consumer demand, resource availability, technology, and government policies. For example, a society must decide whether to allocate resources to produce more food, healthcare, or entertainment goods.

- How to Produce:

In the face of environmental challenges, economies must also consider how to produce and consume in a manner that is sustainable and environmentally responsible.

Impact of Basic Economic Problems: The way a society addresses these economic problems has significant implications for its economic structure, distribution of wealth, and overall well-being. Different economic systems, such as capitalism, socialism, and mixed economies, approach these problems in distinct ways.

Capitalist economies rely on market forces to determine what to produce, how to produce, and for whom to produce. Prices play a crucial role in these decisions. Socialist economies may involve central planning to make decisions on what, how, and for whom to produce, with a focus on social equity. Mixed economies combine elements of both capitalism and socialism, attempting to strike a balance between efficiency and equity.

In summary, basic economic problems arise from the scarcity of resources relative to human wants and needs. Addressing these problems is central to the functioning of economic systems, and how they are addressed varies depending on the economic system in place. These decisions have far-reaching effects on the distribution of resources and the overall well-being of a society.

Resource Constraints and Welfare Maximization

Resource Constraints in Economics:

Resource constraints refer to the limitations and scarcity of resources that an economy faces when making choices about what to produce, how to produce, and for whom to produce. These constraints are a fundamental aspect of economic decision-making and impact the welfare and well-being of individuals and society as a whole. Several key points related to resource constraints include:

- Limited Resources: Resources such as land, labor, capital, and entrepreneurship are limited and finite. In economic terms, this is often referred to as scarcity. Since resources are scarce, choices must be made regarding their allocation.

- Opportunity Cost: When resources are allocated to produce one good or service, there is an opportunity cost associated with forgoing the production of other goods and services. Opportunity cost represents the value of the next best alternative that had to be sacrificed.

- Trade-offs: Because of resource constraints, individuals, businesses, and governments must make trade-offs. They must balance competing interests and allocate resources in a way that maximizes their utility or benefit.

Welfare Maximization in Economics:

Welfare maximization is the goal of economic decision-making, where the objective is to maximize the overall well-being and satisfaction of individuals and society. In the context of resource constraints, welfare maximization involves making choices that lead to the highest possible level of overall satisfaction. Key concepts related to welfare maximization include:

- Utility: In economics, utility is a measure of an individual's satisfaction or well- being. Welfare maximization seeks to increase the utility of individuals and society as a whole.

- Pareto Efficiency: A situation is said to be Pareto efficient when it is impossible to make any individual better off without making someone else worse off. Achieving Pareto efficiency is a way to maximize overall welfare without harming anyone.

- Equity and Fairness: While maximizing welfare is essential, equity and fairness considerations are also important. Welfare maximization should be achieved in a way that doesn't lead to extreme inequalities and considers the distribution of resources and benefits.

Optimal Resource Allocation for Welfare Maximization:

In summary, resource constraints are a fundamental aspect of economic decision- making, and welfare maximization is the goal of allocating resources to achieve the highest level of well-being for individuals and society. Achieving this goal requires balancing efficiency, equity, and fairness, and it often involves a combination of market mechanisms, government intervention, and social safety nets. Cost-benefit analysis and technological advancements also play a role in optimizing resource allocation for maximum welfare.

Microeconomics and Macroeconomics

Microeconomics:

Microeconomics is the branch of economics that focuses on the behavior of individual economic agents and small economic units, such as households, firms, and markets. It examines how these units make decisions, interact with each other, and allocate resources efficiently. Key concepts and topics in microeconomics include:

- Demand and Supply: Microeconomics analyzes how consumers and producers interact in markets. Demand refers to the quantity of a good or service that consumers are willing and able to buy, while supply represents the quantity that producers are willing and able to sell. Equilibrium in the market occurs when demand equals supply, determining prices and quantities.

- Consumer Behavior: Microeconomics delves into how consumers make choices, considering factors like preferences, budget constraints, and utility maximization. It explores concepts such as indifference curves and consumer surplus.

- Production and Costs: Microeconomics examines the production processes of firms and the costs associated with producing goods and services. Topics include production functions, cost curves, and profit maximization.

- Market Structures: Microeconomics categorizes markets into various structures, including perfect competition, monopoly, oligopoly, and monopolistic

competition. Each structure has unique characteristics that influence the behavior of firms and the allocation of resources.

- Factor Markets: The analysis of factor markets focuses on the supply and demand for factors of production, such as labor and capital. Wage determination, rent, and interest rates are explored in this context.

- Price Elasticity of Demand and Supply: Understanding how sensitive the quantity demanded or supplied is to changes in price is critical in microeconomics. Price elasticity measures the responsiveness of buyers and sellers to price changes.

Macroeconomics:

Macroeconomics, in contrast, studies the economy as a whole. It deals with aggregate economic phenomena and aims to understand the broader issues affecting an entire nation or the global economy. Key concepts and topics in macroeconomics include:

- Gross Domestic Product (GDP): GDP is a fundamental macroeconomic indicator that measures the total value of goods and services produced within a country's borders over a specific period. It provides insight into an economy's size and growth.

- Inflation and Deflation: Macroeconomics examines changes in the general price level. Inflation refers to the increase in prices over time, while deflation is the opposite. Central banks monitor and control inflation to maintain price stability.

- Unemployment: Macroeconomics analyzes the labor market and measures the percentage of the labor force that is unemployed. It investigates the causes and consequences of unemployment.

- Monetary Policy: Central banks, such as the Federal Reserve in the United States, implement monetary policy to control the money supply, interest rates, and credit conditions. These policies impact inflation, employment, and economic stability.

Production Possibility Curve

Definition:

A Production Possibility Curve (PPC), also known as a Production Possibility Frontier (PPF), is a graphical representation used in economics to demonstrate the maximum combination of two or more goods and services that an economy can produce given its available resources and technology, assuming full utilization of resources and efficiency in production.

Key Concepts:

- Scarce Resources: The PPC is based on the fundamental economic concept of scarcity, which means that resources (such as labor, capital, land, and technology) are limited, and choices must be made about how to allocate them efficiently.

- Opportunity Cost: The PPC illustrates the concept of opportunity cost, which is the cost of forgoing the production of one good or service to produce more of

another. As an economy moves along the PPC, it must give up some of one good to produce more of another.

- Efficiency: The PPC assumes that the economy is operating at full efficiency, meaning that it is using all available resources to their maximum potential.

Characteristics of the PPC:

- Bowed-Outward Shape: The typical PPC has a bowed-outward or concave shape. This shape represents the idea that resources are not equally productive in all activities. As an economy specializes in producing more of one good, the opportunity cost of producing that good increases, causing the PPC to curve outward.

- Boundary: The PPC is a boundary or frontier that shows the maximum possible combinations of goods that an economy can produce. Points on the curve represent efficient allocation of resources, while points inside the curve represent underutilization of resources, and points outside the curve are unattainable given the current resources and technology.

- Shifting the PPC: The PPC can shift over time due to changes in resource availability, technological advancements, and changes in the labor force. An outward shift of the PPC represents economic growth, while an inward shift may indicate resource depletion or economic decline.

Illustration and Interpretation:

Let's consider a simplified example of a PPC with two goods: "Cars" and "Computers." The PPC demonstrates the trade-off between these two goods. Here are some points of interpretation:

Point A: This point represents a situation where the economy is producing a balanced mix of cars and computers. It's an efficient use of resources, and it's on the PPC. Point B: At this point, the economy is producing more computers but fewer cars. The opportunity cost of producing more computers is fewer cars. It's still on the PPC but is an allocation choice.

Circular Flow of Economic Activities

Definition:

The circular flow of economic activities is a simplified model used in economics to illustrate how the different sectors of an economy interact and exchange goods, services, and money. This model is designed to show the flow of resources, income, and expenditures between households, businesses, and the government. It provides a basic framework for understanding the functioning of an economy.

Key Components:

The circular flow model consists of the following key components:

- Households: This represents the individuals or consumers in the economy. Households supply factors of production (labor, capital, land, and entrepreneurship) to businesses and receive income in the form of wages, rent, interest, and profit.

- Businesses (Firms): Businesses are the producers in the economy. They hire factors of production from households and produce goods and services. In return, businesses pay income to households, which includes salaries, rents, and dividends.

- Product Market: This is where businesses sell goods and services to households. Households purchase goods and services from businesses, and in return, businesses receive revenue.

- Factor Market: This is where households supply factors of production (e.g., labor, land, capital) to businesses. In exchange, households receive income in the form of wages, rent, interest, and profit.

- Government: The government plays a role in the circular flow model by collecting taxes from households and businesses. It then uses these funds to provide public goods and services (e.g., education, healthcare, infrastructure) and transfer payments (e.g., social security, welfare).

- Government Purchases: The government also purchases goods and services from businesses, creating an injection of funds into the economy. This includes government spending on defense, healthcare, education, and other services.

- Taxes: Taxes represent the funds collected by the government from households and businesses. Taxes are used to finance government activities and programs.

Flow of Economic Activities:

In the circular flow model, economic activities flow in a circular manner through the following processes:

- Households supply factors of production: Households provide labor, land, capital, and entrepreneurship to businesses through the factor market.

- Businesses pay income to households: In return for the factors of production, businesses pay income to households. This income includes wages, rent, interest, and profit.

- Households spend on goods and services: Households use the income received from businesses to purchase goods and services in the product market.

Demand and supply are two fundamental concepts in economics that play a central role in determining prices and quantities of goods and services in the market. They represent the forces that interact to establish market equilibrium. Let's explore the demand side and supply side of the market:

Demand:

Definition:

Demand represents the quantity of a good or service that consumers are willing and able to buy at various price levels during a specific period.

Key Concepts:

- Law of Demand: The law of demand states that, all else being equal, there is an inverse relationship between the price of a good and the quantity demanded. In other words, as the price of a good decreases, the quantity demanded increases, and vice versa.

- Demand Curve: The demand curve is a graphical representation of the relationship between price and quantity demanded. It slopes downward from left to right to illustrate the law of demand.

- Determinants of Demand: Several factors affect demand, including consumers' income, preferences and tastes, the prices of related goods (substitutes and complements), and population demographics.

Supply:

Definition:

Supply represents the quantity of a good or service that producers are willing and able to sell at various price levels during a specific period.

Key Concepts:

- Law of Supply: The law of supply states that, all else being equal, there is a direct relationship between the price of a good and the quantity supplied. In other words, as the price of a good increases, the quantity supplied increases, and vice versa.

- Supply Curve: The supply curve is a graphical representation of the relationship between price and quantity supplied. It slopes upward from left to right to illustrate the law of supply.

- Determinants of Supply: Various factors influence supply, including production costs, technology, government policies, and the number of suppliers in the market.

Market Equilibrium:

Market equilibrium is the point at which the quantity demanded by consumers equals the quantity supplied by producers. In equilibrium, there is no excess supply (surplus) or excess demand (shortage). Key points about market equilibrium include:

At the equilibrium price, the quantity that consumers are willing to buy (demand) is exactly equal to the quantity that producers are willing to sell (supply). Equilibrium is determined by the intersection of the demand and supply curves on a graph, where the two curves meet. If the price is above the equilibrium level, there will be a surplus of the product, leading to downward pressure on prices. Producers may need to reduce prices to clear the surplus. If the price is below the equilibrium level, there will be a shortage of the product, leading to upward pressure on prices. Producers may raise prices to take advantage of the shortage.

Illustration:

Consider a simple example with the market for smartphones:

Demand for smartphones may increase if consumer incomes rise, if consumers prefer smartphones to other devices, or if the population grows. Supply of smartphones may increase if production costs decrease, if new technology allows for more efficient production, or if more smartphone manufacturers enter the market.