Efficient frontier

Ρ = +1

Ρ = -1

-1 < Ρ < +1

E(Rp)

σp

Docsity.com

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

Banking is an ever green field of study. In these slides of Banking, the Lecturer has discussed following important points : Efficient Frontier, Assets, General Case, Introduce a Risk, Portfolio, Government, Commercial Bank Deposit, Risky Assets, Levered Portfolio, Borrowing

Typology: Slides

1 / 19

This page cannot be seen from the preview

Don't miss anything!

The general case – applied to two

assets

[ ]

( )

[ 2 ]

( )

( 2 )

( ) 2

( 1 ) 2 0

2 2 ( 1 ) 2 4 0

( 1 ) 2 ( 1 )

( 1 ) 2 ( 1 )

σ σ ρ ωσ σ

σ σ ρ σ ω

ω σ σ ρ ωσ σ σ ρ σσ

ω σ σ σ ρ ωσσ ρ σ σ

ωσ ω σ ρ σ σ ρ ωσσ

ωσ ω σ ρ σ σ ρ ωσσ ω

σ

σ ω σ ω σ ρ ω ω σ σ

σ ω σ ω σ ρ ω ω σσ

⇒= + − = −

⇒= + − − =−

⇒= − − + − =

= − − + − =

= + − + −

= + − + −

d

d (^) p

p

p

Risk-free asset

of interest R f

.

zero variance and therefore no covariance

with the portfolio.

bill or commercial bank deposit.

or borrow at the safe rate of interest. The investor can;

lending or borrowing.

the rest in the risk-free asset.

borrowing at the risk-free rate and hold a levered portfolio.

relates the return on the portfolio with one risk-free asset and

risk.

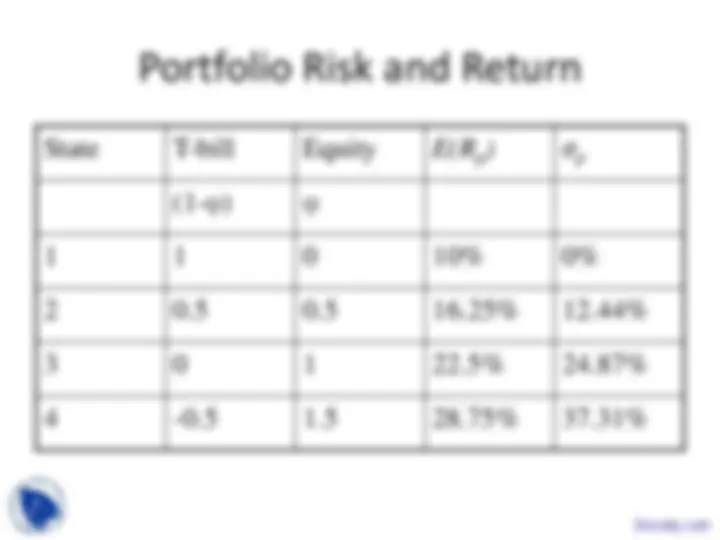

bundle of assets R (^) N = 22.5%.

σN = 24.87%.

asset can be varied to produce a range of new

portfolio returns.

State T-bill Equity E(Rp) σp

(1-φ) φ

1 1 0 10% 0%

2 0.5 0.5 16.25% 12.44%

3 0 1 22.5% 24.87%

4 -0.5 1.5 28.75% 37.31%

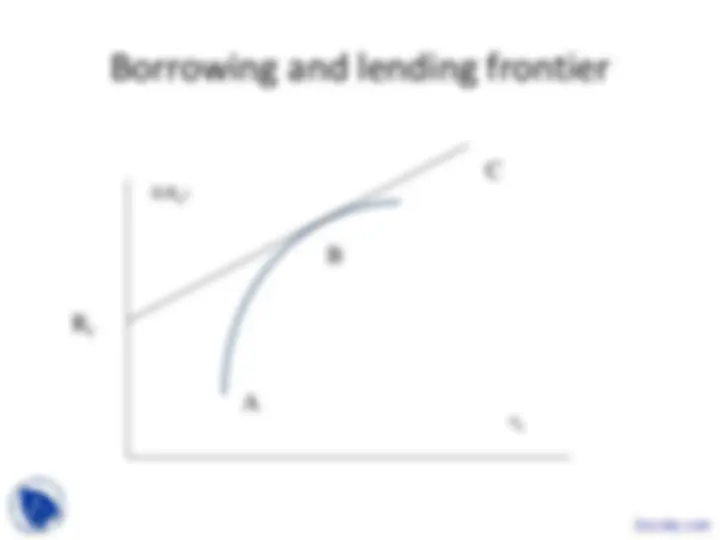

Transformation line

σp

A riskless asset and a risky portfolio

from the London Stock Exchange).

efficient portfolios.

asset that will be superior to all other combinations.

free rate of interest rate.

represents the

rate on Treasury Bills or some other risk-free

asset.

include borrowing.

Borrowing and lending frontier

Rf

A

B

C

Combining borrowing and lending

Rb

A

B

C

D

Rf

P

Q

covariances the investor determines the efficient

frontier. The point M is located with reference to Rf.

portfolio and the safe asset (lending) or a leveraged

portfolio (borrowing).

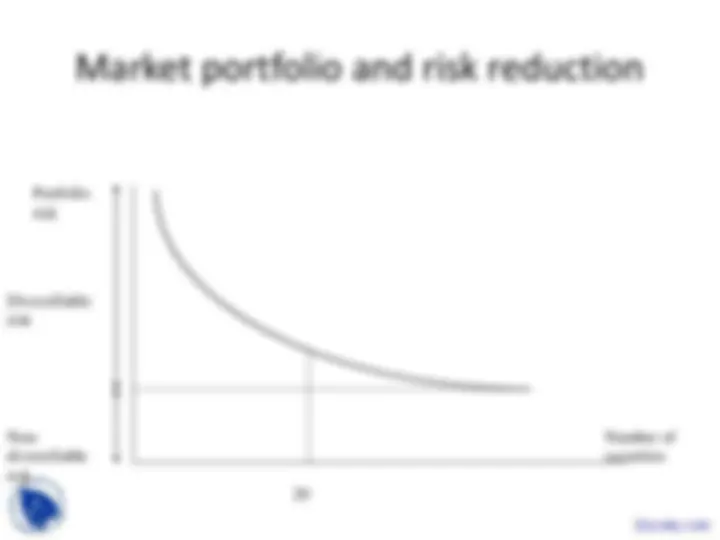

diversification

constructed.

reduces risk to the non-diversifiable

component.