Download Engineering Economics: Cost and its Types - Lecture Notes and more Lecture notes Economics in PDF only on Docsity!

MG 434

Engineering Economics

Lecture#

Cost and its Types

Costs

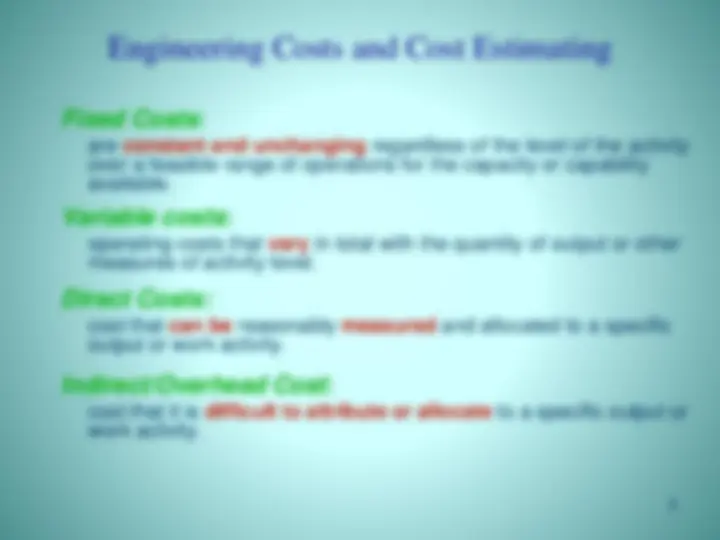

Costs: Fixed and Variable Direct and Indirect Marginal and Average Sunk and Opportunity Recurring and Non-Recurring Incremental Cash and Book Life-Cycle Cost Indices Estimating Benefits Cash Flow Diagrams

Engineering Costs

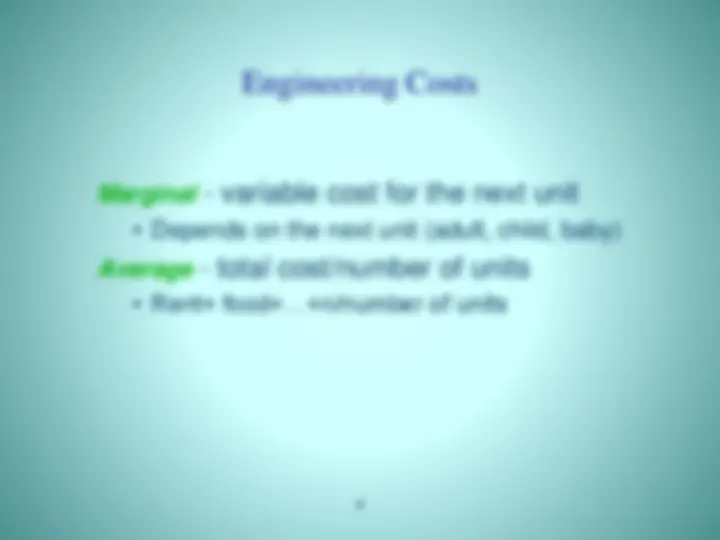

Marginal - variable cost for the next unit

- Depends on the next unit (adult, child, baby) Average - total cost/number of units

- Rent+ food+…+n/number of units

Engineering Costs and Cost Estimating

Key Question: Where do the numbers come from that we

use in engineering economic analysis?

- Cost estimating is necessary in an economic analysis

- When working in industry, you may need to consult

with professional accountants to obtain such

information

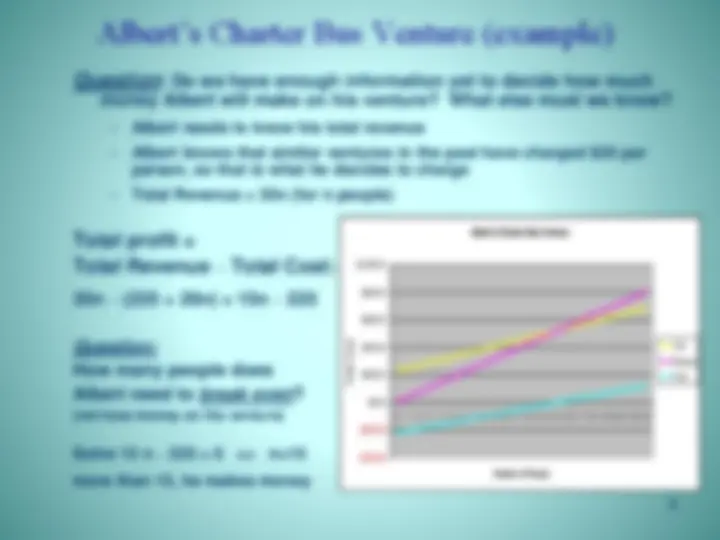

Albert’s Charter Bus Venture (example)

- Answer: Total Cost = $225 + $20 n.

Graph of Total Cost Equation:

n Total cost

Albert’s Charter Bus Venture (example)

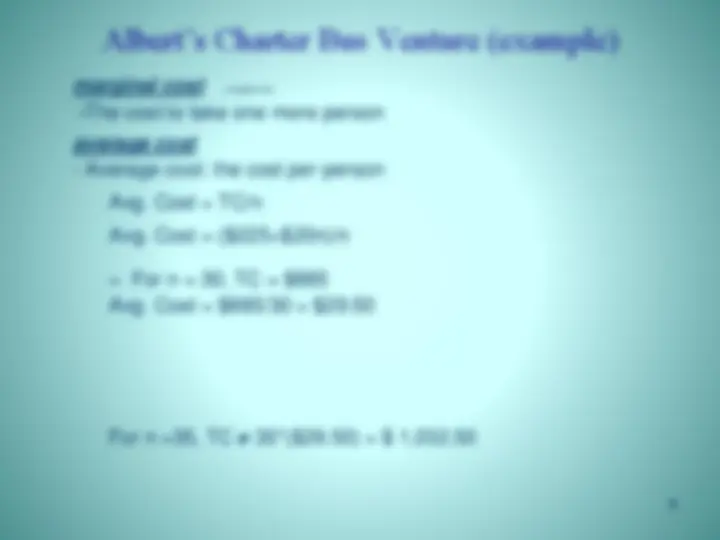

marginal cost (marginal tax)

- The cost to take one more person average cost

- Average cost: the cost per person Avg. Cost = TC/n Avg. Cost = ($225+$20n)/n

- For n = 30, TC = $ Avg. Cost = $885/30 = $29. For n =35, TC 35*($29.50) = $ 1,032.

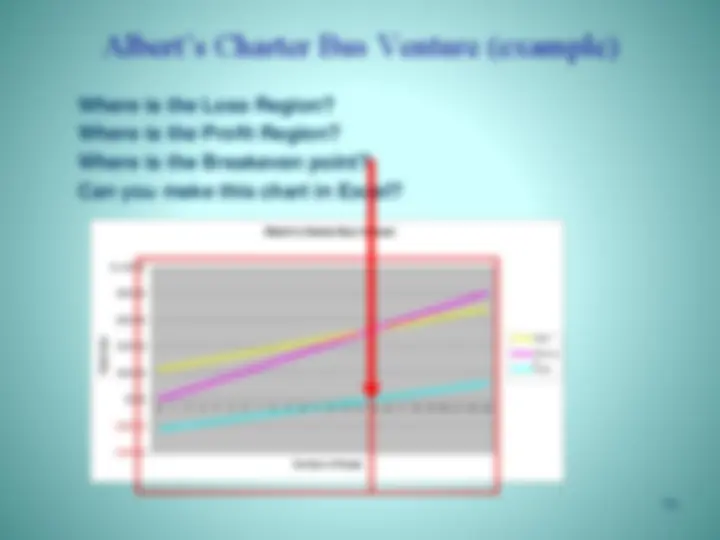

Albert’s Charter Bus Venture (example)

Where is the Loss Region? Where is the Profit Region? Where is the Breakeven point? Can you make this chart in Excel? -$400. -$200. $0. $200. $400. $600. $800. $1,000. 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 Total Cost Number of People Albert's Charter Bus Venture Cost Revenu e Profit

Sunk Costs

A sunk cost is money already spent due to a past decision.

- As engineering economists we deal with present and future opportunities

- We must be careful not to be influenced by the past

- Disregard sunk costs in engineering economic analysis Example : Suppose that three years ago your parents bought you a laptop PC for $2000.

- How likely is it that you can sell it today for what it cost?

- Suppose you can sell the laptop today for $400. Does the $ purchase cost have any effect on the selling price today? The $2000 is a sunk cost. It has no influence on the present opportunity to sell the laptop for $400. ( stock costs now $20 you bought for $80)

Sunk and Opportunity Cost

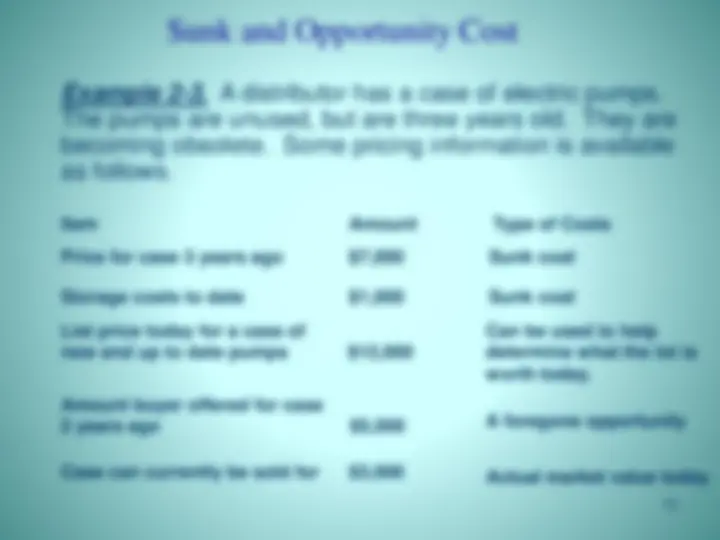

Example 2-3. A distributor has a case of electric pumps.

The pumps are unused, but are three years old. They are

becoming obsolete. Some pricing information is available

as follows.

Item Amount Type of Costs Price for case 3 years ago $7,000 Sunk cost Storage costs to date $1,000 Sunk cost List price today for a case of new and up to date pumps $12, Can be used to help determine what the lot is worth today. Amount buyer offered for case 2 years ago $5,000 A foregone opportunity Case can currently be sold for $3,000 (^) Actual market value today

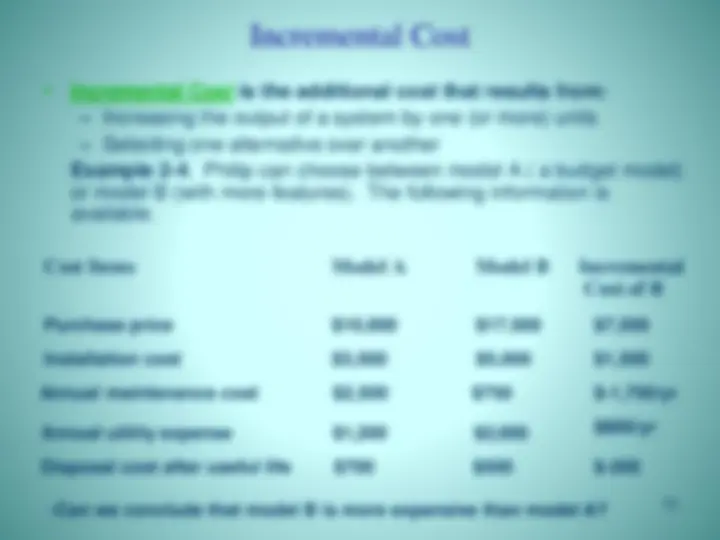

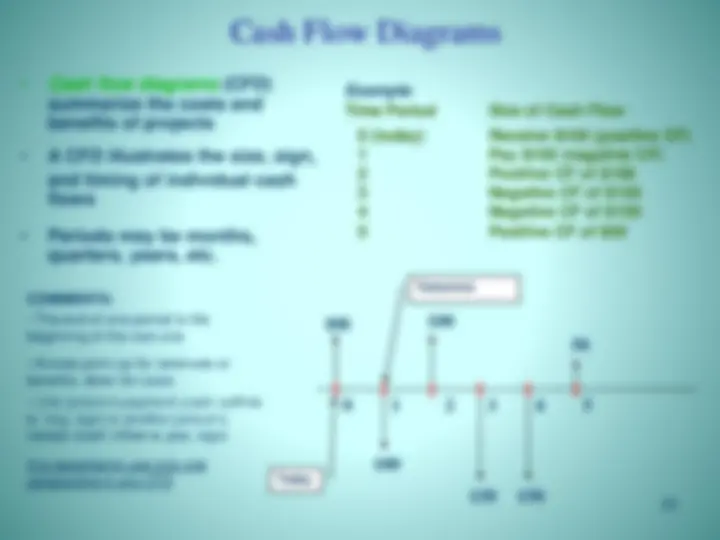

Recurring and Non-Recurring Costs

- Recurring costs are those expenses that are known, anticipated, and occur at regular intervals. These costs can be modeled as cash flows.

- Non-recurring costs are one-of-a-kind and occur at irregular intervals. They are difficult to plan for or anticipate.

Cash Costs vs. Book Costs

Cash costs

require the cash transaction of dollars from “one pocket

to another”.

Book costs

are cost effects from past decisions that are recorded in

the books (accounting books) of a firm

- Do not represent cash flows

- Not included in engineering economic analysis

- One exception is for asset depreciation (used for tax

purposes).

Example : You might use Edmond’s Used Car Guide to

conclude the book value of your car is $6,000. The book

value can be thought of as the book cost. If you actually

sell the car to a friend for $5,500, then the cash cost to

your friend is $5,500.

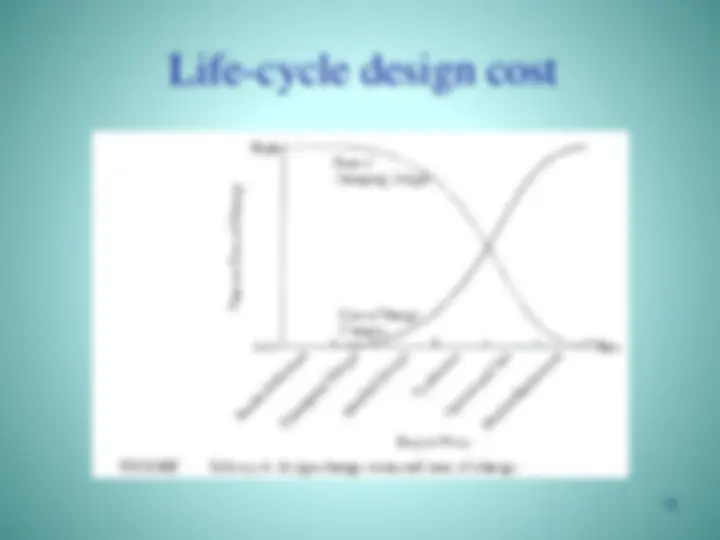

Life-Cycle Costs

Life-cycle costs are the summation of all costs, both

recurring and nonrecurring, related to a product,

structure, system, or service during its life span

Products go through a life cycle, just like people

- Assessment & Justification Phase

- Conceptual or Preliminary Design Phase

- Detailed Design Phase

- Production or Construction Phase

- Operational Use Phase

- Decline and Retirement Phase

Life-Cycle Costs

Comments:

- The later design changes are made in the life-cycle, the

higher the costs.

- Decisions made early in the life-cycle tend to “lock in”

costs incurred later in the life cycle:

Nearly 70 to 90% of all costs are set during the

design phases, while only 10 to 30% of the cumulative

life-cycle costs have been spent.

- Question. When is the best time to consider all life-cycle

effects, and make design changes?

- Bottom Line. Engineers should consider all life-cycle

costs when designing products and the systems that

produce them.

Estimating Benefits

For the most part, we can use exactly the same

approach to estimate benefits as to estimate costs:

- Fixed and variable benefits

- Recurring and non-recurring benefits

- Incremental benefits

- Life-cycle benefits

- Rough, semi-detailed, and detailed benefit estimates

- Difficulties in estimation

- Segmentation and index models

Major differences between benefit and cost

estimation:

- Costs are more likely to be underestimated

- Benefits are most likely to be overestimated

- Benefits tend to occur further in the future than costs