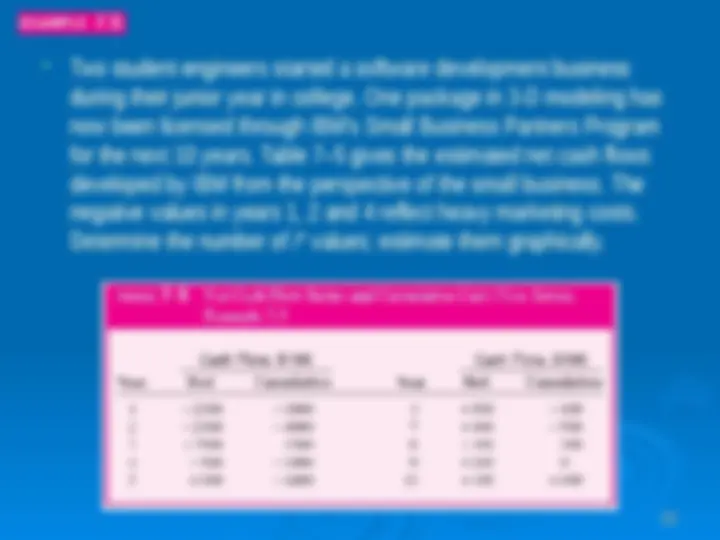

Rate of Return Analysis

Rate of Return Analysis

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

In this document description about Rate of Return Analysis,Rate of Return,Solution,Assumptions and Difficulties with ROR analysis

Typology: Lecture notes

1 / 28

This page cannot be seen from the preview

Don't miss anything!

Rate of return (ROR) is the rate paid on the unpaid

balance of borrowed money, or the rate earned on

the unrecovered balance of an investment, so that

the final payment or receipt brings the balance to

exactly zero with interest considered.

In ROR problems you are trying to find an unknown

interest rate (i*) that satisfies the following:

PWi(+ cash flows) – PWi( - cash flows) = 0

This means that the interest rate (i*) is an unknown

parameter.

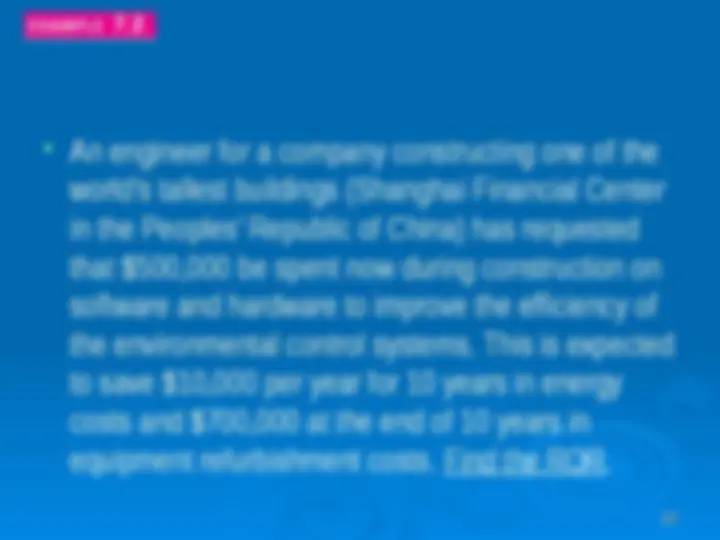

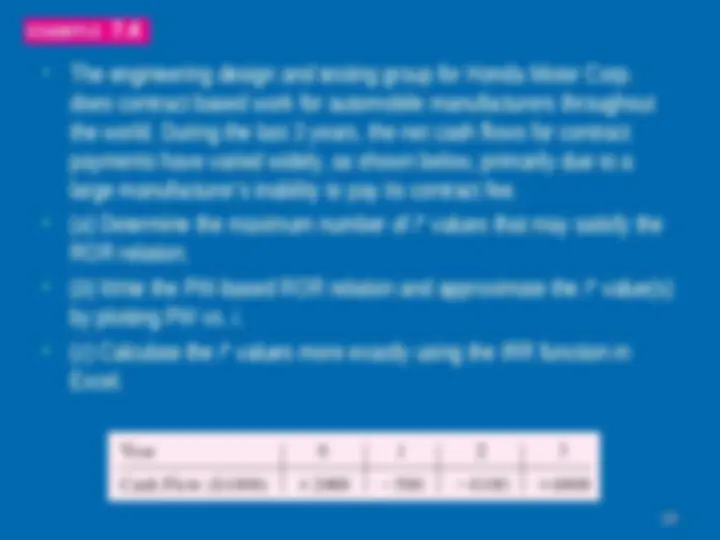

An engineer for a company constructing one of the

world’s tallest buildings (Shanghai Financial Center

in the Peoples’ Republic of China) has requested

that $500,000 be spent now during construction on

software and hardware to improve the efficiency of

the environmental control systems. This is expected

to save $10,000 per year for 10 years in energy

costs and $700,000 at the end of 10 years in

equipment refurbishment costs. Find the ROR.

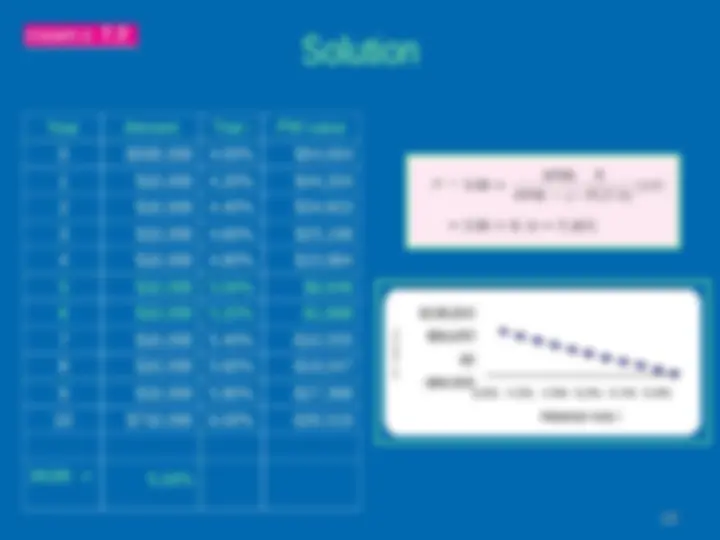

Use the trial-and-error procedure based on a PW equation.

0 = - 500,000 + 10,000 ( P/A , i *,10) + 700,000 ( P/F , i *,10) [7.5]

Use the estimation procedure to determine i for the first trial. All income will be

regarded as a single F in year 10 so that the P/F factor can be used. The P/F factor is

selected because most of the cash flow ($700,000) already fits this factor and errors

created by neglecting the time value of the remaining money will be minimized. Only

for the first estimate of i , define

P = $500,000, n = 10, and F = 10(10,000) + 700,000 = $800,000.

PWi(+ cash flows) – PWi( - cash flows) = 0

Year Amount Trial i PW value

0 -$500,000 4.00% $54,

1 $10,000 4.20% $44,

2 $10,000 4.40% $34,

3 $10,000 4.60% $25,

4 $10,000 4.80% $15,

5 $10,000 5.00% $6,

6 $10,000 5.20% -$1,

7 $10,000 5.40% -$10,

8 $10,000 5.60% -$19,

9 $10,000 5.80% -$27,

10 $710,000 6.00% -$35,

ROR =

5.16%

Solution

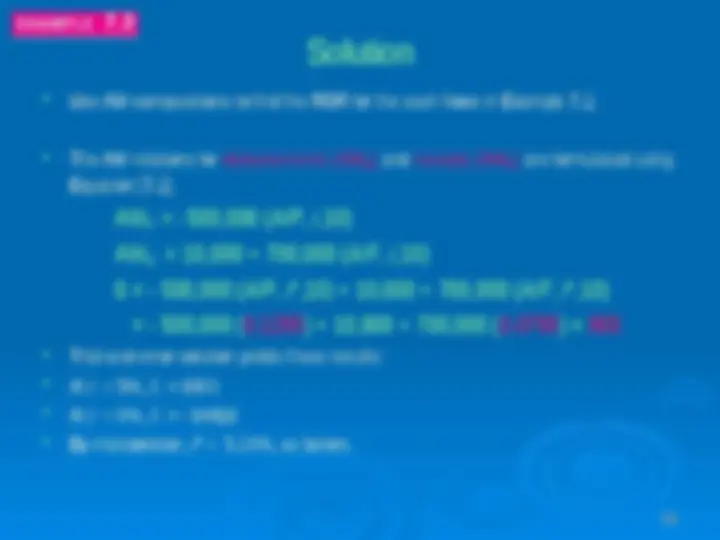

Use AW computations to find the ROR for the cash flows in Example 7.2.

The AW relations for disbursements (AW

D

) and receipts (AW

R

) are formulated using

Equation [7.2].

D

R

Trial-and-error solution yields these results:

At i = 5%, 0 < $

At i = 6%, 0 > - $

By interpolation, i * = 5.16%, as before.

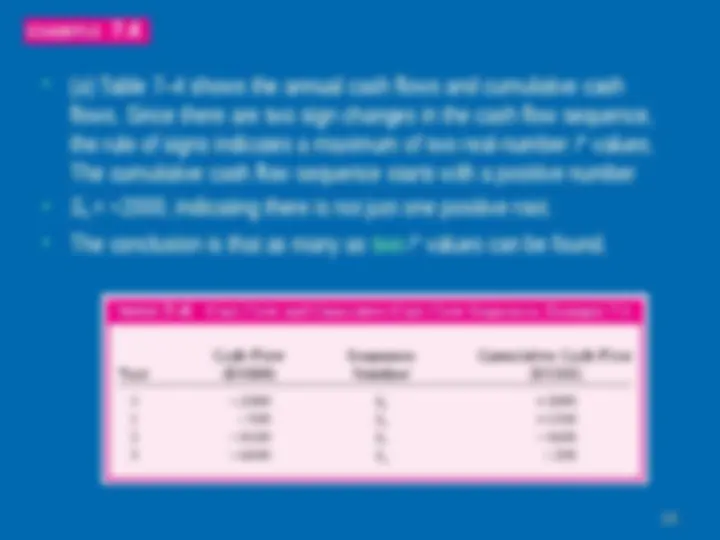

So far we have dealt with conventional (or simple) cash flow series. The algebraic signs on

the net cash flows changed only once, usually from minus in year 0 to plus at some time

during the series.

However, for many series the net cash flows switch between positive and negative from one

year to another, so there is more than one sign change. Such a series is called

nonconventional (nonsimple).

When there is more than one sign change in the net cash flows, it is possible that there will

be multiple i * values in the - 100% to plus infinity range.

There are two tests to perform in sequence on the nonconventional series to

determine if there is one unique or multiple i * values that are real numbers. The first

test is the (Descartes’) rule of signs states that the total number of real-number roots

is always less than or equal to the number of sign changes in the series. This rule is

derived from the fact that the relation set up by Equation [7.1] or [7.2] to find i * is an

n th-order polynomial.

(It is possible that imaginary values or infinity may also satisfy the equation.) The

second and more discriminating test determines if there is one, real number, positive

i * value. This is the cumulative cash flow sign test, also known as Norstrom’s

criterion_._ It states that only one sign change in the series of cumulative cash flows

which starts negatively, indicates that there is one positive root to the polynomial

relation. To perform this test, determine the series

t

Observe the sign of S 0 and count the sign changes in the series S

0

1

n

. Only

if S 0

0 and signs change one time in the series is there a single, real number,

positive i *.

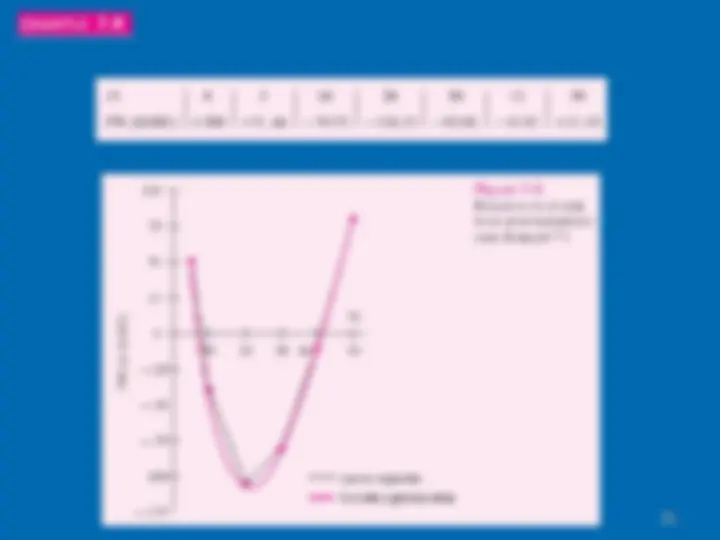

0

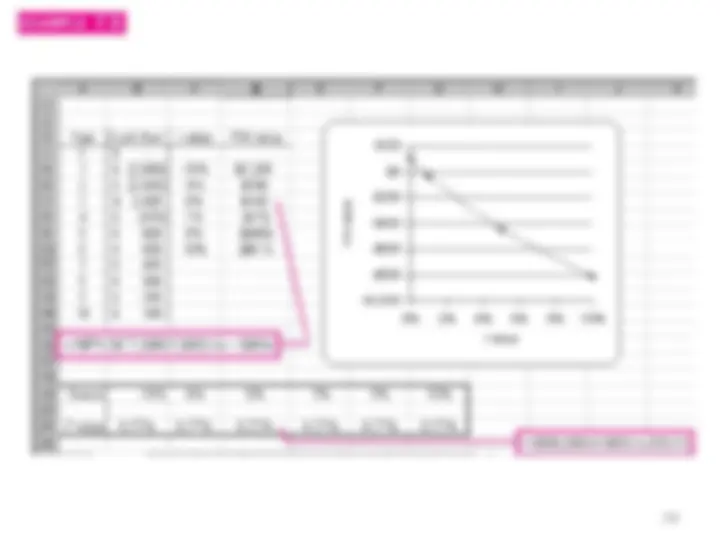

(b) The PW relation is:

PW = 2000 – 500 ( P/F , i ,1) – 8100 ( P/F , i , 2) + 6800( P/F , i , 3)

Select values of i to find the two i * values, and plot PW vs. i. The PW values are shown

below and plotted in Figure 7–5 for i values of 0, 5, 10, 20, 30, 40, and 50%.

The characteristic parabolic shape for a second-degree polynomial is obtained, with PW

crossing the i axis at approximately i

1

i

2