Engineering and Financial Cost Analysis

Variance Analysis

Study with the several resources on Docsity

Earn points by helping other students or get them with a premium plan

Prepare for your exams

Study with the several resources on Docsity

Earn points to download

Earn points by helping other students or get them with a premium plan

An overview of variance analysis in engineering and financial cost, focusing on monthly budget reports. It explains the sources of variance between budgets and actuals, the variance format, and how to calculate spending and volume variances. It also introduces the concept of full-absorption overhead variance analysis.

Typology: Lecture notes

1 / 9

This page cannot be seen from the preview

Don't miss anything!

AQ x A P

AQ x SP

SQ x S P

(1) Actual $$$ given on monthly Variance Analysis report (3) Budgeted $$$ given on monthly Variance Analysis report (2) Calculated by getting AQ and SP from Accounting or other source of budget information = AQ x AP = AQ x SP = SQ x SP

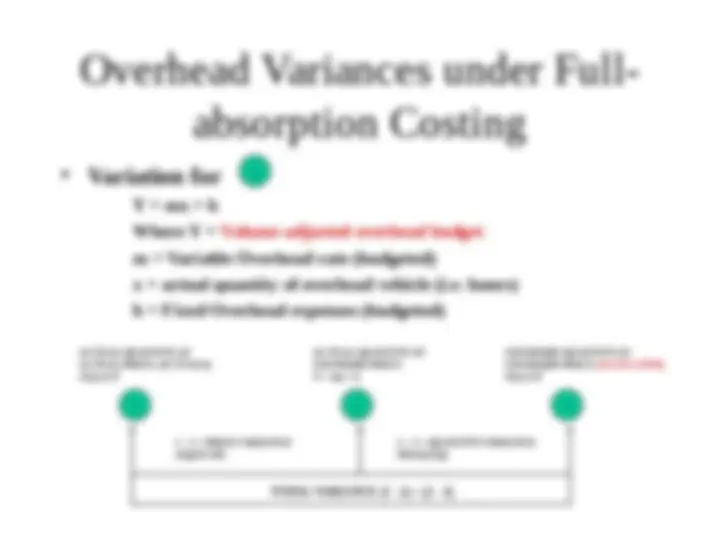

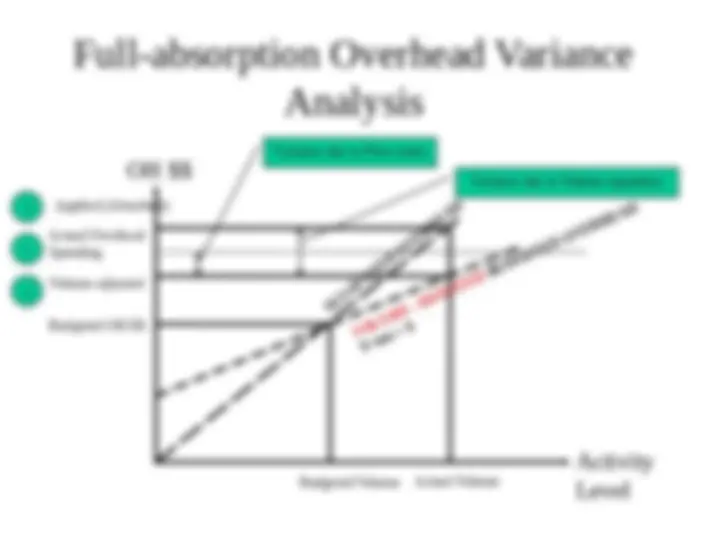

Y = mx + b Where Y = Volume-adjusted overhead budget m = Variable Overhead rate (budgeted) x = actual quantity of overhead vehicle (i.e. hours) b = Fixed Overhead expenses (budgeted) ACTUAL QUANTITY AT ACTUAL PRICE (ACTUALS) AQ x A P

Y = mx + b

SQ x S P