Download Executive Compensation: Agency Theory, Optimal Contracting, and Accounting Manipulation and more Slides Banking and Finance in PDF only on Docsity!

Executive compensationExecutive compensation

Alchian and Demsetz (1972) & Jensen and

Meckling (1976): Manager should be a ‘residual claimant’

Agency theory: tradeoff between risk-sharing

and incentives

Jensen and Murphy (1990): median CEO

earns ‘only’ $3 for every $1000 increase in share value. Huge increase in use of options over last decade.

Executive compensationExecutive compensation

Modern agency theory of executive pay,

Holmstrom and Tirole (1993):

z

Stock-based compensation:

Stock price an unbiased estimate offundamentals

Induces managers to focus on long-run value

performance measure that cannot be

manipulated easily

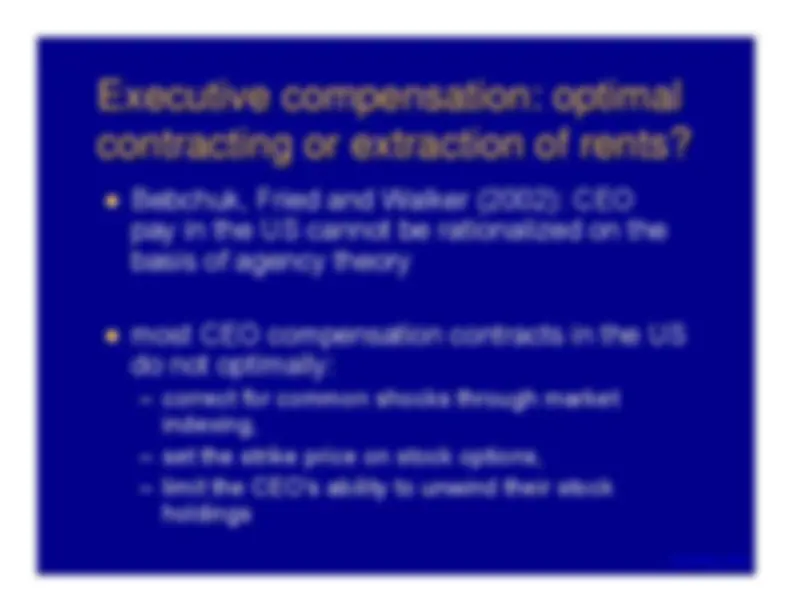

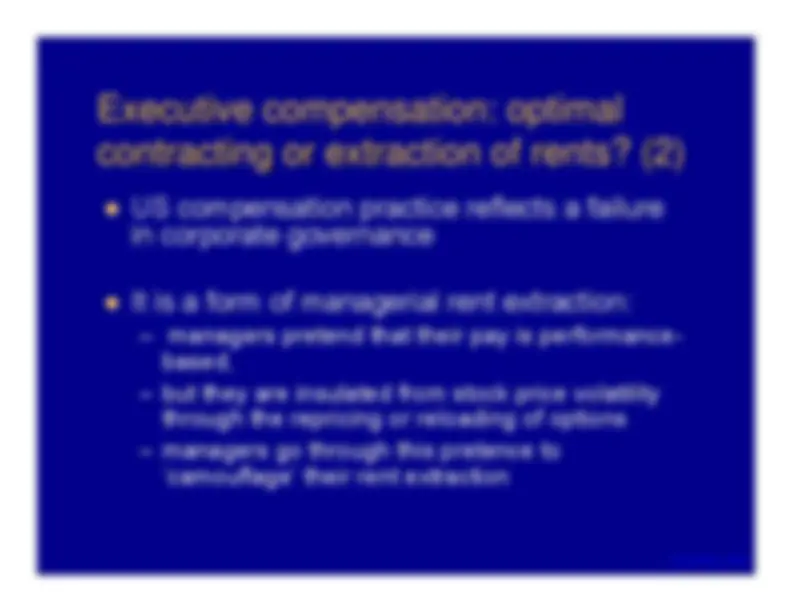

Executive compensation: optimalExecutive compensation: optimalcontracting or extraction of rents? (2)^ contracting or extraction of rents? (2)

z

US compensation practice reflects a failure in corporate governance

z

It is a form of managerial rent extraction:

managers pretend that their pay is performance- based,

- but they are insulated from stock price volatility

through the repricing or reloading of options

- managers go through this pretence to

‘camouflage’ their rent extraction

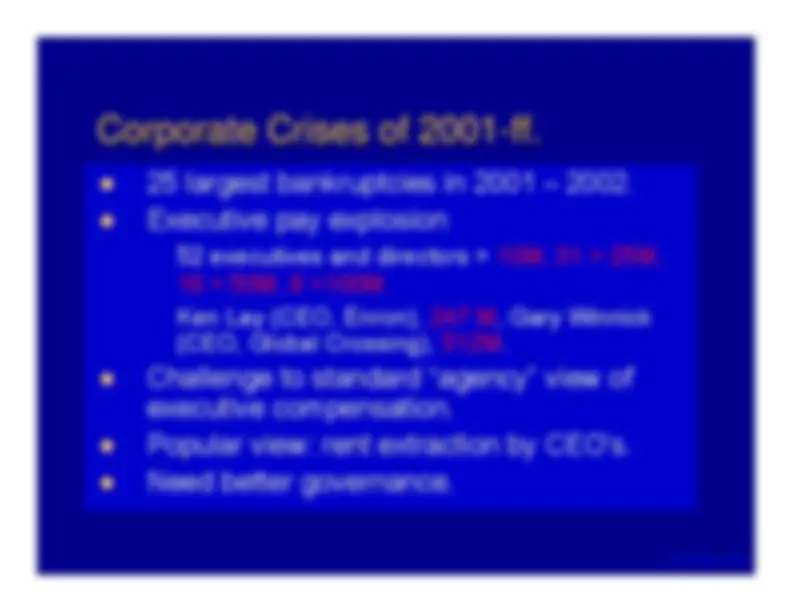

Corporate Crises of 2001Corporate Crises of 2001

ff.ff.

z

25 largest bankruptcies in 2001 – 2002.

z

Executive pay explosion

52 executives and directors > 10M, 31 > 25M,16 > 50M, 8 >100M.Ken Lay (CEO, Enron), 247 M, Gary Winnick(CEO, Global Crossing), 512M.

z

Challenge to standard “agency” view ofexecutive compensation.

z

Popular view: rent extraction by CEO's.

z

Need better governance.

ScandalsScandals

Recessions catch what the auditors

miss.

J.K. Galbraith

z

Securities fraud

z

Stock price manipulation

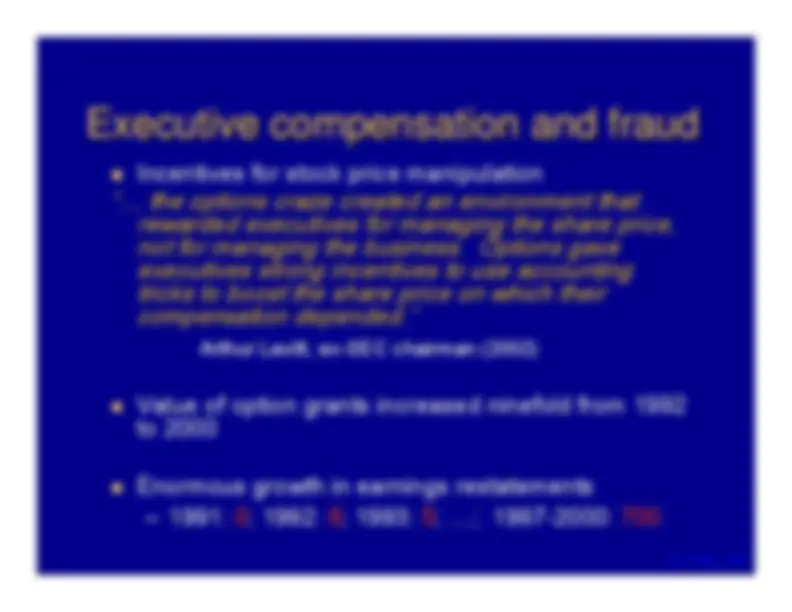

StockStock

based compensation inbased compensation in

speculative marketsspeculative markets

z

Perverse incentives “

In the bubble, the carrots (stock options) became

managerial heroin, encouraging a focus on short-term prices with destructive long-term consequences. ... It also encourages behavior that actually reduced the value of some firms to their shareholders - s

uch as

making an acquisition or spending a fortune on an internet venture to satisfy the whims of an irrational market.

Michael Jensen,

The Economist, November 16, 2002

z

Bolton, Scheinkman and Xiong (2003) model

executive

compensation •

level

sensitivity

accounting irregularities •otherdisinformation

shareholder class

action litigation

incidence •outturn

company

characteristics

(size, industry,

growth, etc.)

corporate governance

(board structure, insider

holdings, etc.)

align incentives

Pricedrop

SEC enforcement

actions

earnings

restatements

Compensation and accountingCompensation and accountingchoices/^ choices/

selfdealingselfdealing

z

Bonus contract incentives drive accountingdecisions

z

Healy (1985), Holthausen

et al

. (1995), Guidry

et al

. (1999)

z

Equity-based compensation (options) predictsdiscretionary accruals

z

Bergstresser and Philippon (2002), Gao and Shrieves (2002),Peng and Roell (2004), Cheng and Warfield (2003)

z

Equity-based compensation and option exercisepredicts SEC accounting enforcement actions

z

Johnson

et al.

(2003), Erickson

et al.

(2003)

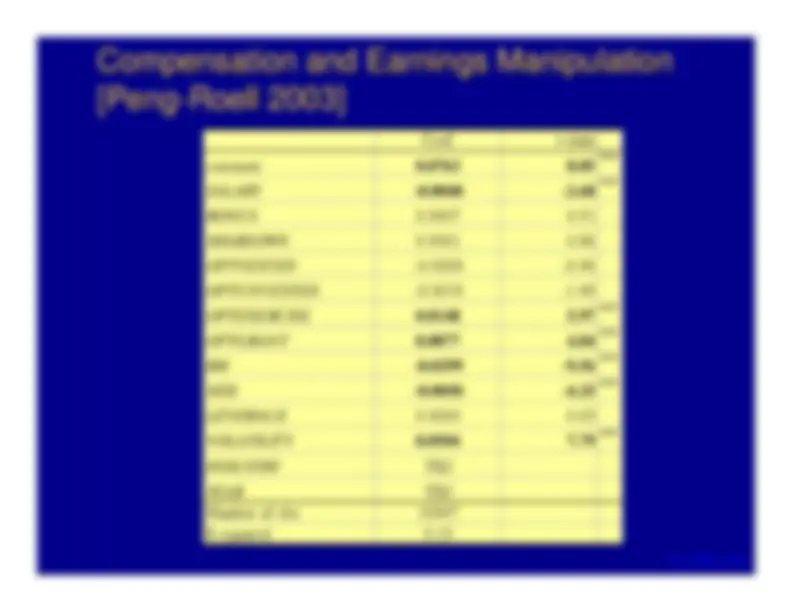

Compensation and Earnings ManipulationCompensation and Earnings Manipulation[^ [

PengPeng

RoellRoell

2003]2003]

Coef.

t-stats

constant

SALARY

BONUS

SHAREOWN

OPTVESTED

OPTUNVESTED

OPTEXERCISE

OPTGRANT

BM

SIZE

LEVERAGE

VOLATILITY

INDUSTRY

YES

YEAR

YES

Number of obs

R-squared

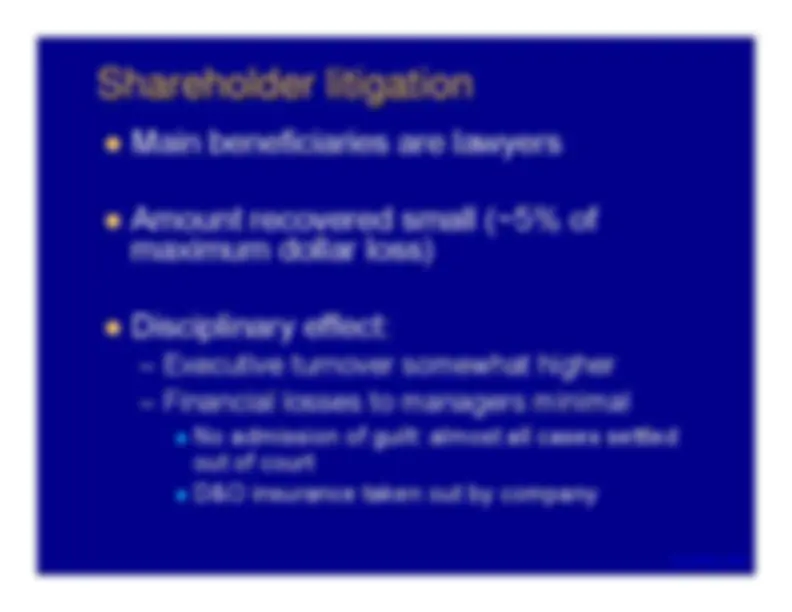

Accounting manipulation andAccounting manipulation andprivate securities litigationprivate securities litigation

z

Johnson

et al. (2002)

z

aggressive accounting

⇒

litigation (post-PSLRA 1995)

z

Lu (2003)

z

earnings management

⇒

litigation

z

DuCharme

et al. (2003)

z

abnormal accruals in IPOs/SEOs

⇒

litigation

z

Heninger (2001)

z

+ve abnormal accruals

⇒

lawsuits against

f

i

rm auditors

Compensation and litigationCompensation and litigation[Peng[

Peng-

-Roell

Roell 2003]

2003]

variable

Coef.

t-stats

Prob

constant

SALARY

BONUS

SHAREOWN

OPTVESTED

**

OPTUNVESTED

OPTEXERCISE

OPTGRANT

**

BM

SIZE

LEVERAGE

VOLATILITY

industry dummies

Yes

Year dummies

Yes

n obs (Prob of 1s)

Pseudo R

2

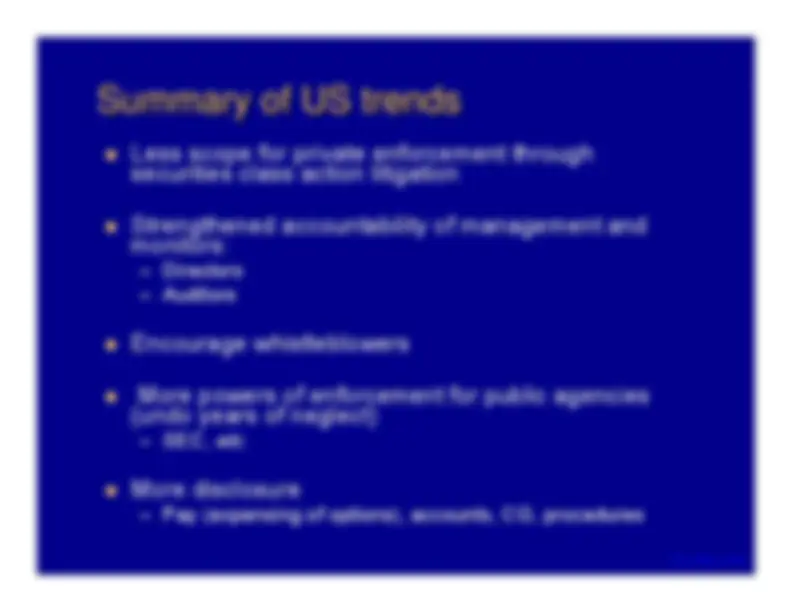

Recent legal reforms discourageRecent legal reforms discouragesecurities class action litigation^ securities class action litigation

z

1998 securities class actions to be brought only in Federalcourts

Curtails jurisdiction shopping

z

1995 Private Securities Litigation Reform Act

Discourages frivolous litigation

e.g.

reduced liability for unknowing parties (outside directors),

limits on attorney’s fees, shift of defendant’s legal fees toplaintiff if suit is baseless, lead plaintiff requirements

z

1994 Supreme Court decision

Curtails liability of “aiders and abettors”

z

1991 statute of limitations (1 year from discovery, 3years from offense)

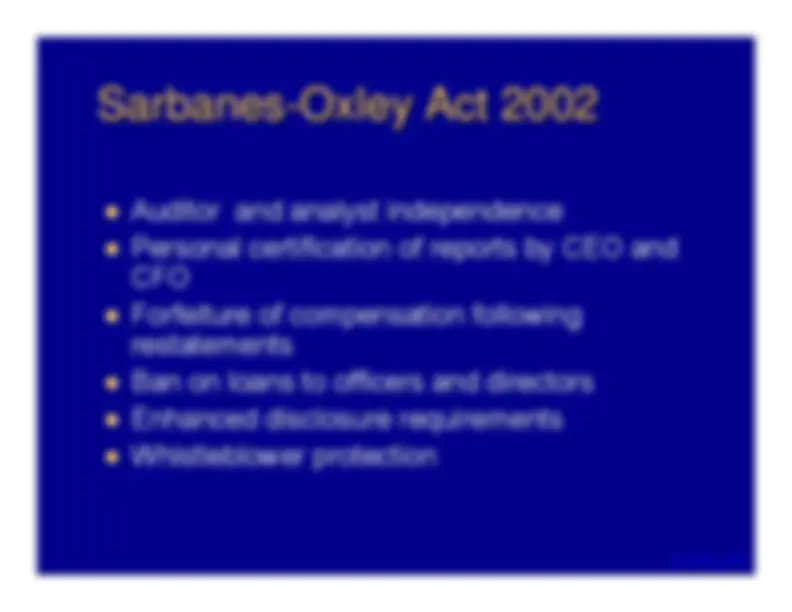

SarbanesSarbanes

OxleyOxley

Act 2002Act 2002

z

Auditor and analyst independence

z

Personal certification of reports by CEO and CFO

z

Forfeiture of compensation following restatements

z

Ban on loans to officers and directors

z

Enhanced disclosure requirements

z

Whistleblower protection

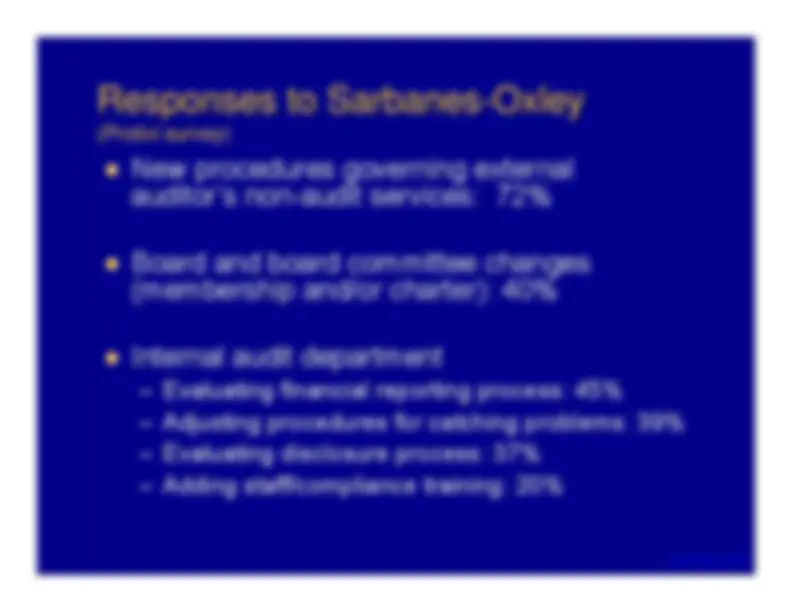

Responses to SarbanesResponses to Sarbanes

OxleyOxley

((

ProtiviProtivi

survey)survey)

z

New procedures governing external auditor’s non-audit services: 72%

z

Board and board committee changes (membership and/or charter): 40%

z

Internal audit department

- Evaluating financial reporting process: 45% – Adjusting procedures for catching problems: 39% – Evaluating disclosure process: 37% – Adding staff/compliance training: 20%